-

Protectionist policies intended to reduce imports and boost exports often backfire because imports and exports are interconnected and tend to rise and fall in tandem.

-

Retaliation hurts exports: Tariffs on imports provoke foreign retaliation against US exports, demonstrating that restricting imports directly harms export markets.

-

Import taxes act like export taxes: The Lerner symmetry theorem demonstrates that tariffs raise costs and reduce competitiveness, harming a country’s ability to sell abroad.

-

Exporters rely on imports: Most manufacturers that export also import raw materials, parts, and equipment. Tariffs raise the costs of these inputs and disrupt production, weakening export capacity and global competitiveness.

-

A country can’t boost exports with fewer imports: Export-led growth requires access to imports. Blocking one side of trade undermines the other.

Out with the new Washington consensus, in with the old protectionist consensus. At the heart of protectionist policy is the belief that broad, hefty tariffs were once used to meet policy objectives such as boosting manufacturing, convincing trading partners to remove barriers to US exports, compelling US companies producing abroad to move production back to the United States, and reducing the trade deficit. To that effect, President Trump has implemented a wide array of tariffs in 2025 and has promised even more in the months ahead. He also discussed imposing a 25 percent—or possibly even 100 percent—tariff on all goods from Mexico. However, the cheerleaders for this new consensus are about to get a big, nasty surprise.

That’s because tariffs will reduce not only American imports but also exports, including exports of manufactured goods. Imports and exports are deeply interconnected—trade flows are not isolated but part of a larger economic system. The Lerner symmetry theorem posits that imposing tariffs on imports reduces a country’s ability to earn foreign currency, which in turn dampens export capacity. Additionally, the global supply chain further illustrates this relationship: Imports often provide the inputs necessary for producing exportable goods. As you will see, tariffs hurt both imports and exports, undermining the overall economic benefits of trade. For this reason, protectionists will not achieve their stated objectives.

The Most Immediate Problem: Retaliation

Retaliation is the most obvious way that tariffs hurt exports. History provides clear evidence of tariffs triggering retaliatory measures with significant consequences for international trade. The Smoot–Hawley Tariff of 1930 is the most frequently cited example of tariff retaliation in modern economic history. When the United States raised tariffs by 20 percent on imported goods, 25 countries responded with retaliatory measures. The consequences were severe. According to a recent study, exports to retaliators fell between 28 and 33 percent. Along with deflation, lower demand deepened the Great Depression.

Foreign governments also retaliated in response to the 2018–2019 US tariffs on imports from China and other trading partners, with US agricultural products being hit the hardest. China led the coalition, enacting retaliation on about $93.5 billion worth of US goods. Other trading partners, including Canada, the European Union, India, Mexico, Russia, and Turkey, imposed their own tariffs, affecting an additional $6.5 billion in exports. These retaliatory duties, ranging from 5 to 50 percent, targeted politically sensitive goods, particularly dairy, pork, soybeans, and other farm products. In total, approximately $97.5 billion in US exports were affected, leading to a steep decline in agricultural trade, with exports of affected products falling by about 27 percent in 2018 alone.

To counteract these economic losses, the US government provided $28 billion in emergency relief to American farmers through two aid packages in 2018 and 2019. Administered by the Department of Agriculture, these funds were distributed through the Market Facilitation Program, commodity purchases, and trade promotion initiatives. The 2018 package allocated $12 billion in assistance, primarily in direct payments, to corn, livestock, soybean, and wheat producers, while the 2019 package expanded this relief to $16 billion and covered a broader range of agricultural commodities. Though these subsidies helped mitigate some financial losses, they did not fully compensate for the long-term disruptions to global trade relationships and market access caused by the trade war.

One easily seen consequence of tariffs is retaliation from other countries. There is another consequence, though, that is harder to see but perhaps even more important: Because tariffs reduce foreigners’ power to purchase home-country exports, exporters will pay a price for tariffs even in the absence of retaliation. This reality makes the tight connection between imports and exports one of the most misunderstood aspects of international trade.

A Tax on Imports Is a Tax on Exports: The Lerner Symmetry Theorem

The Lerner Symmetry Theorem was first published by Abba Lerner in his 1936 paper “The Symmetry Between Import and Export Taxes” in Economica. This formal theorem became one of the fundamental principles in international trade theory, although the general idea was widely recognized in earlier works by other trade theorists at least as far back as Adam Smith.

The Lerner symmetry theorem is also one of the most counterintuitive discoveries in international trade theory: Setting a tax on imports produces the same economic effects as setting a tax on exports. It is also true that a policy to expand exports will, if successful, increase imports. The theorem is foundational and provides crucial insights for modern trade policy decisions that challenge many of the public’s beliefs about how trade and trade barriers work.

To understand the symmetry theorem, consider a hypothetical country called Tradeland that primarily produces computers to export while importing cars from other nations. When Tradeland’s government imposes a 20 percent tax on imported cars, this immediately makes vehicles more expensive in its domestic market. As automobile prices rise, Tradeland’s citizens purchase fewer imported cars, decreasing the flow of Tradeland’s currency to foreign markets. This reduction in currency flow has a crucial secondary, yet inescapable, effect: Foreign buyers now have less access to Tradeland’s currency to purchase computers produced in Tradeland. Consequently, these computers become more expensive for foreigners to buy, and in turn, Tradeland exports fewer computers. Tradeland’s imports and exports fall.

The same outcome would occur if Tradeland decided instead to tax computer exports at 20 percent. When computers become more expensive for foreign buyers, export sales decline, reducing the flow of foreign currency into Tradeland. This reduced supply of foreign currency raises the price Tradelanders pay for the currency and makes it more difficult to purchase imported cars. The higher relative price of imported cars increases Tradelanders’ demand for domestically produced vehicles. The result mirrors that of the import-tax scenario: reduced trade in both directions.

While there are several factors at play in explaining the symmetry, an important one is that a citizen’s ability to afford goods and services from other nations depends on their own country’s ability to earn sufficient income by exporting its own products. The earnings from exports provide the financial means to pay for imports. On the flip side, the products that a country exports are goods (and services) that it produces for the global market rather than its own domestic use.

The Lerner symmetry theorem stipulates specific economic conditions, such as two countries with perfect competition, two final goods, floating exchange rates, and no capital exchange. Over the years, economists have examined the Lerner symmetry theorem and found that it still holds even when the strict conditions of Lerner’s original exposition of the theorem are relaxed or absent.

Perhaps the most significant divergence of today’s reality from Lerner’s assumptions is that capital is now, and has been for the past half century, generally free to flow internationally. Whenever capital is free to move across borders, foreign currencies can be used not only to purchase imports but, alternatively, to pay for foreign investments. Therefore, if Tradeland’s trading partners are willing and able to invest in Tradeland, they cannot use all their Tradeland currency to buy Tradeland exports. Under these circumstances, not all Tradeland currency held by foreigners returns to Tradeland as demand for its exports, but it returns nevertheless—as demand for investments in Tradeland.

While capital flows break Lerner symmetry strictly defined—that is, as any change in imports being offset dollar for dollar by a change in exports—they neither completely disconnect imports from exports nor diminish the underlying significance of Lerner symmetry. When foreigners receive more Tradeland currency, they will, as a practical matter, also increase their demand for Tradeland’s exports. To the extent that they don’t increase their demand for Tradeland’s exports dollar for dollar with the increase in Tradeland’s imports, foreigners will invest in Tradeland. In this case, Lerner symmetry still demonstrates that an increase in Tradeland’s imports does not reduce aggregate demand in Tradeland because foreign investment in Tradeland contributes to aggregate demand in Tradeland no less than does foreign demand for Tradeland’s exports. There is, in short, no reason to fear that a Tradeland trade deficit will reduce either business activity or employment in Tradeland.

Put differently, even when a $1 reduction in imports doesn’t lead to a $1 reduction in exports, as is often the case when there are no or few restrictions on international capital flows, the basic symmetry nevertheless holds: Artificial barriers to imports inevitably create artificial barriers to exports and to inflows of foreign capital. Concretely, this means that if the United States raises tariffs, some US firms and their workers will pay a price as the demand for their outputs will fall. Capital and labor in the United States will shift from industries in which Americans have a comparative advantage to less productive ones in which Americans have a comparative disadvantage. And this reallocation of US resources will occur regardless of whether foreign countries respond to US tariffs by retaliating against US exports.

Historical Evidence of Lerner Symmetry

Protectionists and free traders have understood the interdependence between imports and exports since at least the 17th century. Douglas A. Irwin reports that “the principle was used extensively in the House of Commons in the early 1840s and before, when Parliament was considering whether to repeal the Corn Laws, legislation that limited British grain imports. Members in favor of repeal argued that the import tariffs restrained exports of manufactures, and that allowing greater imports of wheat would lead directly to greater exports of textiles.” Even the mercantilists of the 17th century recognized this interdependence. As a result, the more thoughtful of them realized that import tariffs could become so excessive or high that these levies might undermine their goal of a “favorable” balance of trade—that is, of exports exceeding imports.

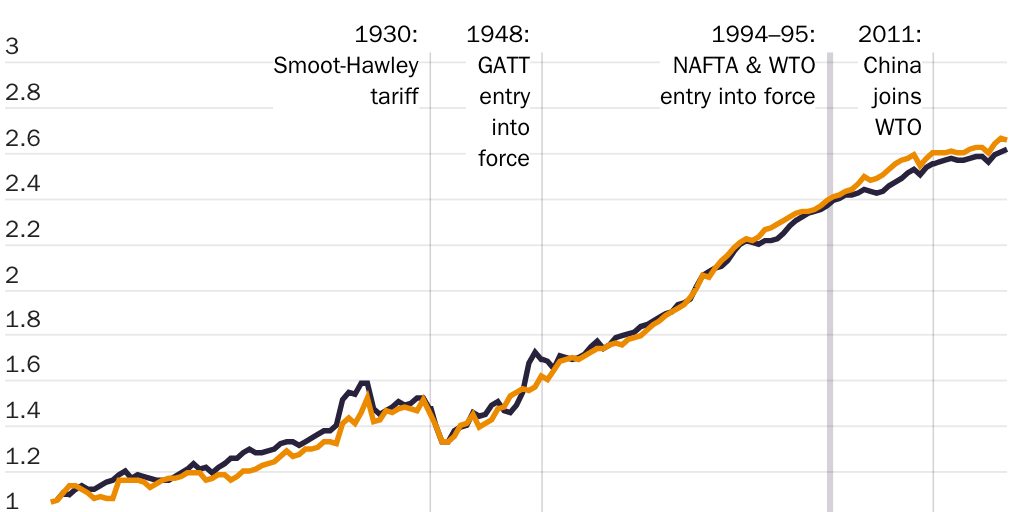

This theory is supported by empirical evidence. Figure 1, produced with help from Professor Irwin, shows the growth of US exports and imports in millions of dollars from 1869 to 2019. It uses the export and import logs to illustrate proportional changes. As illustrated, no matter what happened over the period—the Smoot–Hawley Tariff Act, the North Atlantic Free Trade Agreement, or China’s accession to the World Trade Organization—exports and imports move together.

So next time you hear someone complain about the United States’ one-sided opening of its markets after the postwar period, other countries’ unfair trade practices, and the United States’ unwillingness to fight them with trade barriers, make sure to point out that whatever happened, it didn’t make any difference in export and import levels.

The symmetry can also be seen in the aftermath of the adoption of the North American Free Trade Agreement, which took effect in January 1994 and removed most tariffs and quotas on goods traded among Canada, Mexico, and the United States. This reduction in trade barriers led to fears that flows of cheap imports would cause the US trade deficit to rise. Instead, what we saw were significant increases in both imports and exports. Between 1993 and 2016, total trade among the three countries more than tripled, rising from approximately $290 billion to over $1.1 trillion. Focusing on the United States, imports from these countries tripled, rising from $159 billion to $599 billion. Meanwhile, exports to Canada and Mexico also tripled, from $142 billion in 1993 to $497 billion in 2016.

The symmetry holds even when countries have very different commercial and trade policies from those of the United States. Whether a country pursues import substitution policies (such as tariffs, licensing requirements, or quotas) or export promotion policies (such as export subsidies, deregulation, or trade liberalization), we see both its import and export levels rise or fall in sync. Irwin states that “this illustrates the functional importance of the Lerner symmetry theorem. It is not just a hypothetical abstraction. If a government undertakes policies that systematically reduce the volume of imports, it also systematically reduces the volume of exports. The reasons may be indirect and less than obvious, but they are still present and have to be reckoned with.”

Understanding the Lerner symmetry theorem is essential for crafting effective trade policy. It reveals the futility of mercantilist trade policy and illustrates how attempts to manipulate one aspect of international trade inevitably affect other areas, often in ways that counteract the policy’s intended benefits. As policymakers consider trade interventions, they must carefully weigh these symmetric effects to avoid unintended consequences that could undermine their economic objectives.

Export-Import Interconnection: The Global Supply Web

Modern commerce, with its symbiotic connections between services, foreign investments, global production, and supply chains, also demonstrates why broad-based tariffs will hurt a nation’s exporters. Though trade is often described as occurring among unitary national teams and involving goods made entirely in their respective territories, today most imports are actually inputs in a production process, and a vast share of international trade is intrafirm trade with foreign affiliates, rather than unrelated foreign parties.

The BMW Spartanburg manufacturing plant is BMW’s largest global manufacturing facility, located in Greer, South Carolina. It opened in 1994, employs around 11,000 workers, and produces about 1,500 vehicles daily. The plant plays a pivotal role in US automotive exports; it regularly leads the nation in automotive export value. In 2023 alone, the plant exported 225,276 vehicles, valued at nearly $10.1 billion, to approximately 120 countries.

On the surface, this BMW plant is the role model for the kind of manufacturing modern protectionists would like to see in the United States. It’s a German carmaker that uses the United States to produce a large share of its worldwide production, 60 percent of which is exported. According to the company, “The plant is supported by more than 300 suppliers in the U.S., including over 40 direct tier 1 suppliers in South Carolina alone.” Companies such as Michelin and Goodyear supply tires. Plastics and interiors for dashboard assemblies, seats, and plastic components are sourced from nearby suppliers in South Carolina or neighboring states. US factories provide windshields and coatings tailored to BMW specifications.

However, while the BMW facility’s exports are impressive, they wouldn’t be possible without importing many high-value components and materials. Engines and transmissions are manufactured in BMW plants in Germany and Austria. Electronic systems, including control modules, sensors, and infotainment systems, are sourced from specialized suppliers in Asia, Europe, and North America. Though 70 percent of the steel used in assembling cars at the Greer plant is sourced domestically, it also imports high-quality steel. Other raw materials, such as aluminum and composite materials, are imported from suppliers worldwide. Other specialized parts, such as high-performance suspensions, braking systems, and turbochargers, often come from BMW’s European partners.

This balance between importing components and exporting finished vehicles exemplifies the integrated nature of modern manufacturing supply networks. Because of this system, imposing broad-based tariffs would raise the price of American manufacturers’ imported components, make their exports less competitive globally, and significantly harm the US manufacturing sector overall. For BMW Spartanburg’s operations, increased costs for imported parts will lead to higher production expenses, including for its American-produced inputs, reducing the plant’s competitiveness compared with global players that don’t have the same tariff burden. Tariffs will therefore result in decreased exports and could seriously disrupt the plant’s access to supplies, causing production delays and inefficiencies. Given that the plant contributes to over 100,000 jobs in the US economy, any hit to its operations would cause broader economic harm, including to other American automotive companies.

BMW isn’t the only automaker that produces and assembles cars in the United States made of hundreds of different parts from all over the world and then exports them to other countries (Table 1). The same is true for American automakers that have both domestic and international locations from which they produce for exportation and domestic consumption. In fact, a look at the top-10 list of the most American-made or ‑sourced cars in 2024 reveals that while the Tesla Model Y is number one, only four American-brand cars made the list. Three of the four are Tesla models.

In other words, no automaker—especially not GM or Ford—will be safe from the harm caused by broad-based tariffs. All manufacturers will face rising costs, much of which they will shift to consumers in the form of higher prices. That will, in turn, affect their exports. These disruptions to exports will happen even before any trading partners start retaliating against American products sold abroad.

Automakers aren’t unique in the large amount of input they import to produce in the United States. In fact, half of all imports to the United States are either intermediate components or raw materials used as input in the production of American products. Also, in the same way that BMW produces cars in the United States for exports while importing parts from other BMW plants around the world, around half of US imports and nearly a third of exports are between related parties (i.e., multinational corporations).

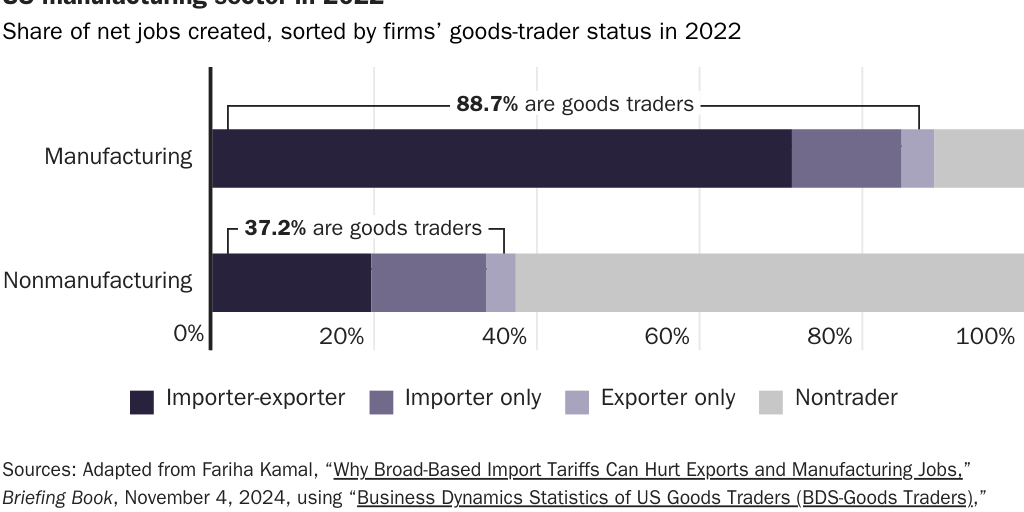

These dynamics explain why large US exporters, especially the top exporters, are also large importers. The same holds for exporting countries, as well. Writing in her Substack, Briefing Book, trade economist Fariha Kamal explains that “firms that both export and import goods account for 84% of the total value of exports and 91% of the total value of imports. Manufacturers [italics in original] that both export and import represent half of all exports and 40% of all imports, underscoring the complementarities between exports and imports in US production.”

In other words, don’t expect a manufacturing boom from the implementation of large tariffs on imports. These import taxes can’t be implemented without hurting both exports and manufacturing. They will also hurt manufacturing jobs in the process. According to Kamal, 80 percent of manufacturing jobs are in exporter-importer manufacturing firms, and these firms drive growth in manufacturing jobs.

These effects shouldn’t come as a surprise to the upcoming administration. Studies of the effects of the first Trump administration’s tariffs find that they hurt US exports through several channels, including supply chains. A 2020 paper, for instance, by Kyle Handley, Fariha Kamal, and Ryan Monarch, found that for the average firm affected by the 2018–2019 US import tariffs, the implied duty cost was $900 per worker and about $1,600 per worker in the manufacturing sector. Also, the paper demonstrates that the most exposed products had relatively lower export growth. The authors state that “by 2019, this spillover friction from import tariffs to exports was equivalent to an ad valorem tariff of about 1.5% on US exports at mean exposure and 3–4% for products one or two standard deviations above the mean. Moreover, the export growth reductions would have been 35% smaller if the new import tariffs were not levied on products likely to be part of the average firm’s supply chain.”

Conclusion: There’s No Such Thing as Export-Led Growth

The next time you hear someone talk about boosting exports while restricting imports, remember: It’s like trying to fill a bucket with water while simultaneously punching holes in the bottom. There are two sides to trade—the imports that enrich our lives and lower the costs of production, and the exports that pay for them. There is a tight connection between exporting and importing, so protective tariffs will not fuel the manufacturing renaissance or export boom that modern protectionists want.

This economic reality punctures the myth of export-led growth. The Lerner symmetry theorem tells us that subsidizing exports is equivalent to subsidizing imports because of general-equilibrium effects working through the exchange rates and relative prices. In particular, when a country implements export subsidies, exports will initially become more competitive, increasing foreign demand for subsidized goods. This increased demand for exports leads to an appreciation of the domestic currency as foreigners need more of it to buy the subsidized exports. The stronger currency then makes imports relatively cheaper for domestic consumers and firms, thus offsetting the growth in exports.

Trade liberalization, and especially the lowering of import taxes, offers a better path to becoming an exporting powerhouse. Indeed, China’s global trading transformation began with aggressive tariff reductions in the early 1990s. As Bryan Riley of the National Taxpayers Union pointed out recently, when China initiated major trade reforms in 1992, its average import tariff rate stood at approximately 32 percent. By 2020, China’s average import tariff rate had declined to approximately 2.5 percent, though, as it is in nearly all countries, specific rates varied significantly across different sectors and products. Notably, tariffs on industrial inputs and machinery saw particularly steep declines to support domestic manufacturing, while some agricultural products maintained higher protective tariffs.

According to Scott Lincicome and Arjun Anand’s essay, “The ‘China Shock’ Demystified: Its Origins, Effects, and Lessons for Today,” lower tariffs on imported materials and components allowed Chinese manufacturers to access higher-quality inputs at competitive prices, significantly improving their export competitiveness. Also, the increased exposure to foreign competition and technology forced domestic firms to innovate and improve. As imports dramatically increased, foreign direct investment and exports grew. Chinese exports increased from $85 billion in 1992 to over $2.5 trillion by 2020. Manufacturing became increasingly sophisticated, with China moving up the value chain from producing simple textiles and toys to manufacturing complex electronics, machinery, and high-tech products. As Riley states, “China’s share of global manufacturing increased from 5% to 35%,” transforming China into the world’s largest exporter.

But crucially, China’s lower tariffs facilitated more imports, which in turn led to more exports and foreign direct investment in China. It’s not the other way around: China did not increase its wealth simply by producing things and shipping them abroad. The exports that are said to have led to China’s growth contributed to it only by bringing in imports and foreign capital. It is therefore no less accurate to say that China’s growth was led by imports and foreign investment than it is to say that its growth was led by exports. Exports are a means of acquiring imports and foreign capital.

The United States should remember this lesson. Trade isn’t a zero-sum game in which exports are victories and imports are defeats. It’s a positive-sum exchange that benefits both sides and in which both exporting and importing are beneficial. Understanding this simple truth would revolutionize our trade policy debates. The sooner we accept the fundamental and unbreakable connection between exports and imports, the sooner we can move past destructive trade policies and toward policies that better promote prosperity.

About the Author

This work is licensed under a Creative Commons Attribution-NonCommercial-ShareAlike 4.0 International License.