-

The US trade deficit is one of the most misunderstood concepts of all time, and it has spawned numerous bad policies.

-

Continuing this tradition, some policymakers want to shrink the trade deficit by taxing international capital flows.

-

Policies to shrink the trade deficit, including those that would tax capital flows, are highly flawed on theoretical, empirical, and practical grounds.

Introduction

The US dollar is the most coveted national currency, and America’s financial markets are the envy of the world. Because US financial markets provide more trading opportunities, liquidity, and security than those of any other country, it is easier for both Americans and foreign residents to invest, efficiently allocate capital, and diversify their risks. Ultimately, these benefits from such a high demand for dollar-denominated assets make it easier for people to earn income and build wealth. Yet, some critics of US economic policy want to suppress investment in America for the sake of reducing the country’s trade deficit.

The US trade deficit is defined as the value of America’s imports exceeding the value of its exports during a given period. It is one of the most misunderstood concepts of all time, and it has spawned numerous bad policies. One of the latest examples is a proposal to “balance trade” by taxing international capital flows. Supporters of this policy aim to shrink the trade deficit (i.e., to balance trade) by taxing the capital surplus that goes along with a trade deficit to zero out the balance of payments. Such a policy is highly flawed on theoretical, empirical, and practical grounds.

These concepts—trade deficits and capital surpluses—are merely part of a national accounting system. At best, taxing international capital flows would fail to change the incentives that drive US consumers’ high demand for imports. At worst, the tax would cause a global economic recession that would threaten to impoverish millions of people and generally make Americans poorer. Regardless, taxing foreign residents’ purchases of US assets to “balance” trade flows would raise the cost of capital in the United States for a pointless goal.

American Capital Markets Are the Envy of the World

Currently, the United States has the deepest, most liquid, most secure financial markets in the world. Some economists even argue that investors are willing to accept a lower return on investments in US assets because of the additional security and liquidity provided by US financial markets. Regardless, this position makes it easier for both Americans and foreign residents to more accurately price assets because so many people can reveal what they believe these assets are worth. It also helps people to more efficiently allocate capital and diversify their risks and to earn more income. Ultimately, the scope and size of US capital markets makes it easier for people—both Americans and foreign residents—to invest internationally and domestically.

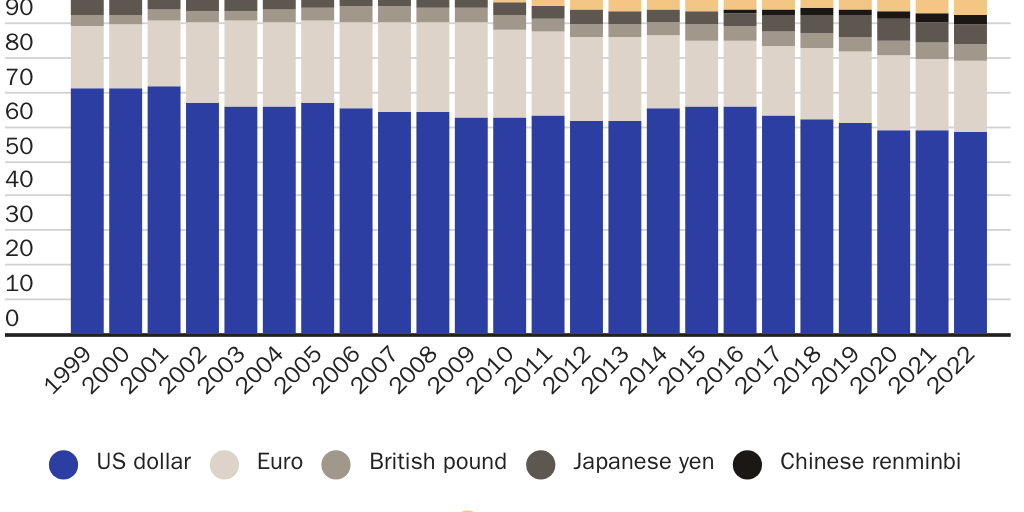

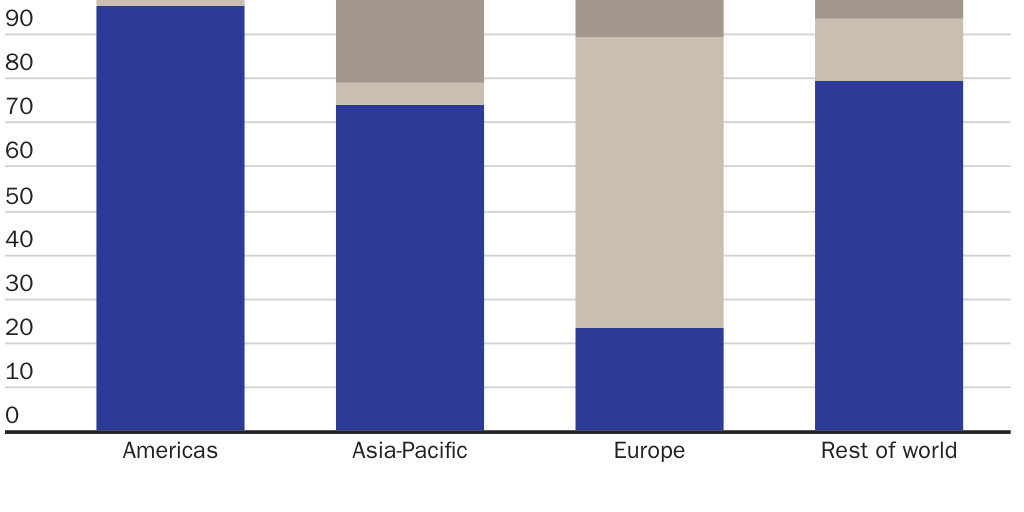

Simultaneously, the US dollar is the dominant reserve asset in foreign-exchange markets (Figure 1), and it is by far the dominant currency for invoicing and settling international trade (Figure 2). About half of all US currency circulates abroad as a medium of exchange in other countries. Because the United States does not have to pay for these purchases of its currency, the result is effectively an interest-free loan to the Federal Reserve. These features derive from America’s open economy and stable institutions, and they are inextricably tied to people’s—both Americans and foreign residents—ability to earn income and build wealth. Ultimately, these financial markets make it easier for people to produce and buy more of the products and services that improve their lives.

These benefits apply even to secondary markets, where securities trades do not directly fund businesses. That is, people who purchase US financial assets by directly funding a business can typically sell that asset to someone else with little trouble. The incredible ease with which people can buy US financial assets—including everything from US Treasury securities to corporate stocks and bonds—from their original owners makes it that much easier to raise capital in the first place. Naturally, the more foreign residents who have access to these markets, the more liquid these markets become, thus improving people’s ability to earn income, raise capital, and buy (and sell) goods and services.

Restricting Foreign Capital Inflows Hurts Americans

Restricting inflows of capital from abroad, such as by imposing a tax on foreigners’ purchases of US securities or other assets, would reduce both investment and consumption by residents of other countries and by Americans. That is, the tax would shrink all economic activity. It would make people worse off by lowering the amount of goods and capital exchanged, as well as people’s income. A tax on international residents would make it more costly for them to invest in the United States, and it would hurt Americans because the reduced demand for dollar-denominated assets would (at the very least) put downward pressure on the real value of these assets.

Taxing capital flows to make investing in US assets more costly is akin to closing American markets through a capital control regime, a policy that has repeatedly produced poor economic results throughout the world. Evidence shows, for instance, that such efforts to decrease capital flows out of a given country results in higher interest rates and produces costly incentives to avoid the controls. Combined, these factors tend to discourage investment in those countries, thus making their citizens worse off (and less able to buy, for example, US products and services).

All types of investment contribute to economic activity through different channels that are often interconnected. Imposing a tax to reduce investment, therefore, threatens all the potential benefits from these varied relationships. Put differently, purposely shrinking investment flows threatens the many channels through which people use production, trade, and innovation to earn income and build wealth. Imposing a tax on capital is also unlikely to boost jobs in specific sectors that the government is targeting, such as manufacturing. In fact, available data suggest that taxing investment flows would likely decrease manufacturing jobs.

Research shows that US transnational manufacturers dominate the manufacturing industry. They are heavily involved in international trade, and they import nearly as much as they export—about four times as much as all the other types of manufacturing firms combined. Though it may seem surprising, the truth is that America’s largest importing companies are also among its largest exporting companies. Choking off these companies’ investment, therefore, threatens both types of international goods flows.

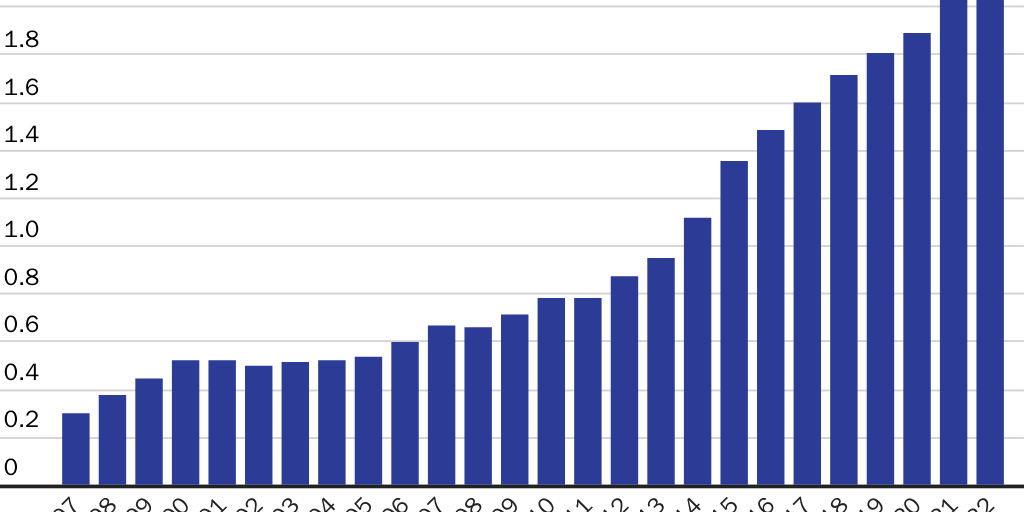

The value of these activities is far from trivial. Figures from the Bureau of Economic Analysis demonstrate that US affiliates of foreign multinational firms inject hundreds of billions of dollars per year into the United States for research and development and capital expenditures. The largest share of these flows during the past decade has typically gone into the manufacturing industry. More broadly, total foreign direct investment (FDI) in the US manufacturing sector alone reached $1.8 trillion prior to the pandemic (Figure 3), and majority-owned affiliates of all foreign multinationals employed nearly eight million American workers, contributing $1.1 trillion to US gross domestic product (GDP). Taxing investment flows threatens these jobs and the broader economic gains that these investments produce.

Ultimately, taxing international capital flows to “balance” trade flows would weaken the position of US financial markets and the dollar, thus diminishing all the economic benefits associated with its dominant position. Simply put, this kind of policy would make it more difficult for people to invest in the United States, making both Americans and foreign residents poorer. Even if such a policy were implemented for a worthy economic goal, policymakers should avoid making it more difficult for people to invest in the United States.

There Is No Good Reason to “Balance” Capital and Trade Flows

Trying to ensure that trade flows—or capital flows—are regularly “balanced” has no foundation in economic theory. Simply put, a country’s capital inflows do not have to match its capital outflows, just as a country’s trade inflows (imports) do not have to match its trade outflows (exports). The failure of these flows to “balance” does not prevent a nation from reaching its maximum economic potential. Economically, it would make as little sense to try to balance these figures as it would to try to balance the goods or capital flows between Walmart and American consumers.

The residents of any country can, for instance, finance their own expenditures entirely through domestic markets regardless of whether the country’s current account (or trade account) is in deficit or surplus with any other country. Even when consumers and businesses do rely on some external financing (directly or indirectly), their domestic spending on goods and services does not have to match these investment flows, just as Walmart can rely on external financing without “balancing” the amount investors contribute against what they spend in Walmart’s stores.

Put differently, the source of Walmart’s sales revenue is independent of its source of financing, just as Americans’ demand for imports is independent of how Americans finance their purchases. Nonetheless, some might argue that when foreign investors use dollars to buy, for example, American citizens’ shares of Apple and Exxon, they help to “finance” Americans’ purchases. Still, these types of share purchases do not have to balance against Americans’ goods purchases. It makes just as little sense to try to force such share purchases into balance as it would to try to force US pension funds’ stock purchases to balance Americans’ good purchases.

The flawed idea of balancing trade is a long-running misconception dating back to the days of Adam Smith (“Nothing, however, can be more absurd than this whole doctrine of the balance of trade”). The concept’s modern roots, which continue to bear rotten fruit even today, lie in a misunderstanding of the accounting framework used to create international (and national) economic accounts. These modern accounts can be traced to the 1920s, when the US Department of Commerce first published the balance of payments accounts, a system designed to measure the flow of goods and services abroad. Many aspects of these accounts have an arbitrary nature that if handled differently would result in a very different set of accounting outcomes.

For instance, all real estate transactions are classified as capital purchases (or sales), but there is no reason why these transactions could not be classified as consumption expenditures. Under the existing framework, if a Chinese resident buys a newly built house in the United States for $1 million, the transaction increases the US current account deficit. If, however, the same transaction was recorded as a consumption expenditure, it would decrease the current account deficit because it would be treated as an exported good (a US-produced good sold to a foreign resident). More broadly, if the overall accounting framework was designed, instead, to track the quantity of goods, a trade deficit would be referred to as a “goods surplus.” Regardless, a trade deficit does not indicate that anyone has lost anything or that anyone is owed anything.

Setting aside the arbitrary nature of these concepts and naming conventions, the core accounting framework remains the same for what has evolved into the present-day international economic accounts. These accounts are still designed to keep track of where all the money in the economy is going and where it is coming from. Thus, in theory, these accounts must balance because they account for all the different flows.

Still, this accounting requirement does not mean that US consumers must finance their spending from abroad to import more than they export. Similarly, the accounting requirement does not indicate that any amount of international financing must equal what any group of consumers spends on goods and services from abroad. Thus, on the surface, trying to make these amounts balance appears to be a misguided policy. In practice, this type of policy would be problematic because even the accounting balance that exists in the international accounts is not so easily achieved. Unsurprisingly, the empirical evidence does not support the notion that balancing trade flows is a worthy economic goal.

Trade Deficits Exist through All Phases of US Business Cycles

Conceptually, it is a mistake to associate foreign countries’ aggregate savings and investment relationships with individual choice. In other words, foreign residents and businesses do not choose to sell Americans goods and services so that they can simply turn around and invest their proceeds in American financial assets. That sort of reciprocity is not what drives the US economy or even the US balance of payments outcomes for that matter. It is not the case that the exporters from foreign countries are literally financing Americans’ purchases of goods and services.

It is unsurprising, therefore, that there is no solid empirical support for the notion that trade deficits (or surpluses) cause economic problems. Nor is it surprising that the United States has run a trade deficit for most of its history, through all phases of its many business cycles. For instance, on an annual basis, the United States ran a trade surplus only 2 times from 1790 to 1819, 11 times from 1820 to 1860, and 23 times from 1861 to 1900—a surplus in only 36 of 108 years. In the post–World War II era, from 1960 to 2022, the United States ran a trade surplus in 13 of 62 years. And in the 1930s, one of the most dismal economic periods on record, the United States had a trade surplus for 102 of the decade’s 120 months.

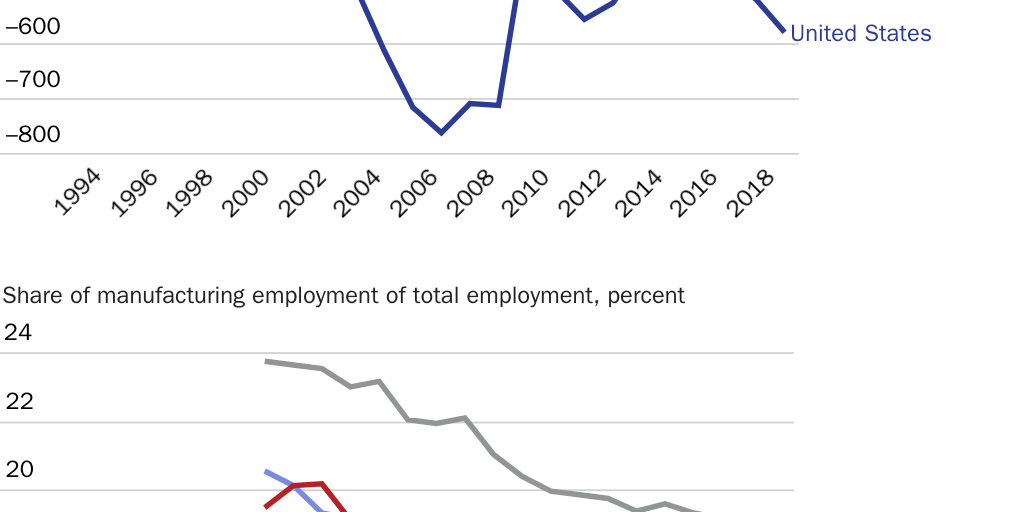

Still, supporters of restricting US trade exploit the negative-sounding term “trade deficit.” They often argue that policies to balance imports and exports are necessary to protect American workers in manufacturing. Yet, they ignore the fact that most industrialized countries are experiencing a downward trend in manufacturing jobs—very much like America did after 1979—despite the fact that they consistently experienced trade surpluses. For instance, the same type of employment declines are found in “countries such as Germany, Japan, and Italy, which have had trade surpluses in manufacturing trade that between 1973 and 2010 averaged 7.6, 6.2, and 4.2 percent of their GDPs, respectively.” From 1994 to 2018, in a nine-country sample of developed and underdeveloped nations, some with trade surpluses and others with trade deficits, all but India and Pakistan displayed a decline in the percentage of their population employed in manufacturing (Figure 4).

Separately, as international trade increased in the 1980s, the share of manufacturing employment in the United States fell at nearly the same rate (0.4 percentage points per year) as it did in the 1960s and 1970s, when the country experienced a much lower share of trade in the economy. The US data also show that the respective shares of imports and exports to GDP rose almost in tandem from 1960 to 2018. Thus, US manufacturing employment has fallen while both imports and exports (as a share of the economy) have been rising at nearly the same rate. Internationally and domestically, there simply is no clear negative relationship between a trade imbalance and a nation’s manufacturing employment. Nonetheless, politicians continue to propose ideas for eliminating trade imbalances.

Recent Proposals to Tax Capital Flows Are Badly Misguided

One recent example of a proposal to balance trade by taxing capital flows is the 2019 Competitive Dollar for Jobs and Prosperity Act, introduced by Senators Tammy Baldwin (D‑WI) and Josh Hawley (R‑MO). Specifically, the bill would require the Federal Reserve to impose a tax on “foreign purchases of US stocks, bonds, and other assets” to achieve a current account balance (defined as a deficit or surplus no greater than an average of 0.5 percent of GDP in any five-year period) no later than five years after the bill is enacted.

Supporters of such policies argue that taxing capital flows would be beneficial because the “trade shortfalls that plague the US economy are chiefly a product of imbalanced capital flows.” Thus, the purpose of the tax would be to reduce the abundance of capital that flows into the United States (a capital surplus) until the value of US imports roughly equals the value of US exports. This kind of proposal is highly flawed. Trade deficits and capital surpluses are merely part of a national accounting system, and there is no good economic reason for attempting to force them into “balance.” At best, taxing international capital flows would fail to change the incentives that drive US consumers’ high demand for imports.

While it is doubtful whether this kind of tax could shrink the trade deficit, it would certainly make investing in US assets more costly. Over time, the reduction in capital flowing into the United Sates would likely reduce productivity, thus resulting in slower real-wage growth. There is absolutely no reason to believe that Americans would be better off if foreign capital flows were somehow reduced. In fact, trying to control capital flows is a harmful policy with a long history of failure.

Research has consistently shown that more foreign investment is good for American workers and the communities in which they live. It has resulted in outsized economic performance that benefits Americans directly employed by foreign affiliate companies as well as those living and working in surrounding communities. Much of the foreign direct investment (FDI) coming into the United States is from traditional allies, including Japan, Canada, Germany, and the United Kingdom, and 40–70 percent of annual FDI goes into the manufacturing industry.

Much of the FDI comes through US affiliates of foreign multinationals, and these companies spend hundreds of billions of dollars per year in the United States on research and development and capital expenditures, with the biggest shares going to manufacturing. The foreign-based parent companies tend to be among the best in their industries, and they tend to bring their knowledge and high productivity to the United States, contributing disproportionately to US economic performance. For instance, in 2018, even though these companies accounted for less than 1.5 percent of all American businesses, they accounted for 6.5 percent of US GDP (private‐sector value-added), 5.5 percent of all private-sector employment, and 14.8 percent of US private‐sector employee benefits.

One study suggests that American workers would have been $36 billion poorer in 2015 if domestic companies would have had to replace all the FDI from these foreign affiliates. It would make little sense to drive FDI away, just as it would make little sense to stop Americans from making capital expenditures. Congress should avoid policies designed to shrink investment, regardless of the source of those funds.

Conclusion

US financial markets are the most liquid and secure in the world, and the US dollar is the most sought-after national currency, making it is easier for foreign residents to invest in the United States. This status helps both Americans and foreign residents more efficiently allocate capital and diversify their risks, thus increasing their ability to earn income and build wealth. This strength, derived from America’s open economy and stable institutions, ultimately makes it easier for more people to buy more of the products and services that improve their lives. Imposing a tax to suppress capital flows would mitigate these benefits, reducing both investment and consumption by Americans and foreign residents, leaving both poorer.

Critics who call for taxing capital flows to “balance” the trade deficit misunderstand—or misrepresent—a completely benign accounting artifact that happens to sound negative. In truth, though, neither a trade deficit nor a capital surplus plagues the American economy. Imposing a tax on foreign residents’ purchases of US assets threatens all the economic benefits associated with the dollar’s renowned status, for both Americans and foreign residents. This misguided trade policy would directly raise the cost of capital in the United States for a pointless goal.

About the Author