-

Whether you are sending support to distant loved ones or fleeing a war-torn nation, moving money across borders is not easy in the traditional financial system.

-

Cryptocurrency has emerged as not only a solution to inefficiencies in payments but also as a reminder that issuing money is not a role that is exclusive to governments.

-

Rather than seek to stomp out competition, policymakers should welcome currency competition as both a source of innovation and inspiration.

Across the world, money has been locked away—restricted from being used to its full potential. Yet, these restrictions are not due to money being sealed within vaults or behind armed guards. Rather, the laws governing national borders have restricted money from achieving its full potential in global commerce. Around the world, people sending money abroad pay a myriad of processing fees only to be stuck waiting days for transactions to clear. Others have become trapped and cut off from society as authoritarian governments freeze their finances in a bid to stomp out opposition. And still more have been forced to watch as their wealth decays under mismanaged currencies with no other alternative available. Although it may be easy to take a smooth payments system for granted, the existing system has all too often isolated people from the rest of the world.

A new challenger has emerged in recent years that may put an end to these struggles: cryptocurrency. What began in 2008 with the introduction of a single white paper about a peer-to-peer electronic cash system has since become a global phenomenon. And since its introduction, Bitcoin has inspired people around the world to innovate and create what is now popularly known as “cryptocurrency.”

At its core, cryptocurrencies have offered a way to digitally store and transfer value in a manner secured by cryptography rather than governments and other third parties. In doing so, Bitcoin, and the cryptocurrencies that followed, opened new opportunities for people across the world. Part of those opportunities have been cryptocurrency’s ability to move money across borders in an increasingly global economy.

The Rise of Cryptocurrency in a Global Economy

Over the last 15 years, cryptocurrency has become a global phenomenon. For better and worse, cryptocurrencies have made headline news, become legal tender in El Salvador, and been the subject of several congressional hearings. Although Bitcoin and a few others have maintained consistent dominance, there is an estimated 26,355 cryptocurrencies currently in existence with a total market cap of over $1 trillion. To be clear, many of these projects have failed or never made it off the launch pad, but that is not necessarily bad. As Mark Cuban, American entrepreneur and investor, has noted, “99 percent of tokens will go broke. Just like 99 percent of early internet companies did.… But the winners will be game changers. That’s the way tech works.” And like the internet, cryptocurrency is an innovation that is already opening up new opportunities worldwide.

One area that cryptocurrencies have already made waves is in the mining industry. Not to be confused with the industry dedicated to extracting resources from the Earth, cryptocurrency mining is the process of validating a public ledger that records cryptocurrency transactions. Notably, the public nature of these ledgers means that people are free to contribute regardless of their location, experience, or status. So long as someone has the computers necessary, they are free to enter this market. Over the last two years, Bitcoin mining has, on its own, created average revenue streams of $30 million per day. From Kenya to the United States, entrepreneurs around the world have tapped into this industry.

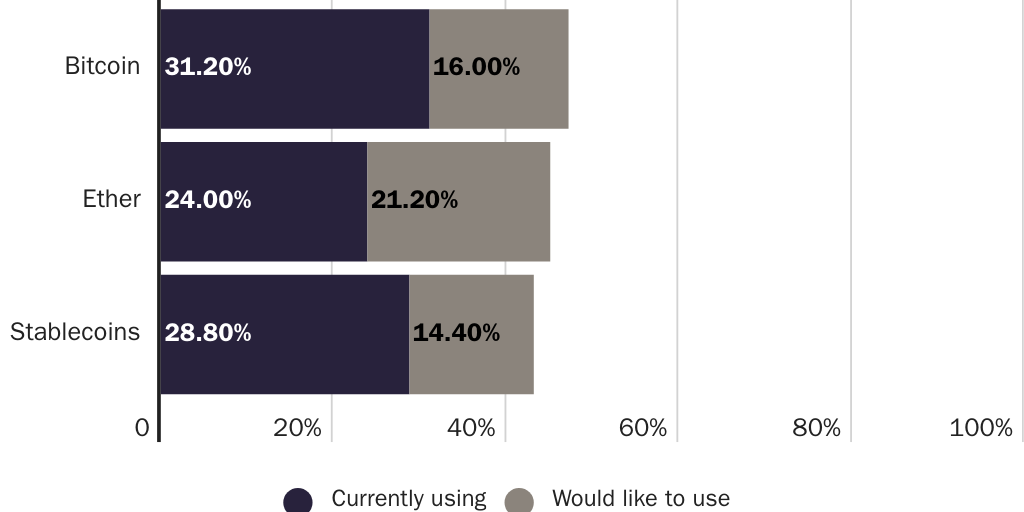

Outside of this niche industry, multinational firms have also taken notice and begun to incorporate cryptocurrencies into their businesses (Figure 1). In a 2021 survey, 58 percent of multinational businesses responded that they had used at least one form of cryptocurrency. This interest is likely due in part to the growing use of cryptocurrencies for ecommerce payments. CoinGate, a cryptocurrency payment processor, published a report noting that the company facilitated 927,294 payments in 2022—a 63 percent increase from 2021. Although this activity is a small fraction of the total global economy, it is remarkable to consider that the novel technology was being used for payments once every 34 seconds.

People may still be divided by geographical constraints and political borders in the physical world, but the digital world has created opportunities for connecting people. And within this digital world, cryptocurrencies have offered a new way for people to transfer value across borders—unhindered by the problems plaguing payments.

A Primer on Problems Plaguing Payments

Many people are probably unfamiliar with the barriers that prevent money from moving across borders. One of the many successes of globalization is that most cities offer foods from the farthest reaches of the globe—a luxury that was once only available to the elite, if anyone at all. However, the entrepreneurs seeking to import those foods and make them available are likely all too familiar with the challenges posed by the costs of tariffs and other trade restrictions. Likewise, people seeking to merely send money to distant family and friends are likely all too familiar with the costs of today’s financial barriers. Worst of all, those fleeing war-torn nations, authoritarian regimes, or similarly dire circumstances are likely all too familiar with just how quickly money can become frozen and trapped within national borders. Whether it be with remittances, carrying wealth, or choosing a better currency, the laws around national borders have long restricted the movement of money.

Restricted Remittances

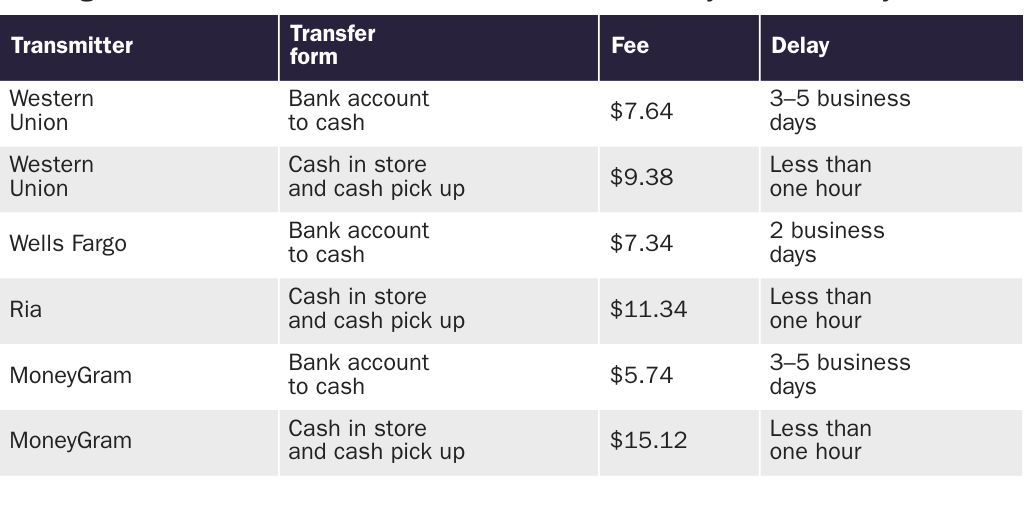

Being the first generation to plant roots in a new country or even just staying connected with distant relatives can quickly result in getting up to speed with the costs of international transfers. The average remittance is around $200, but the fees can stack up when it comes to something as simple as sending money to loved ones across borders. On average, remittances cost 6.01 percent of each transaction, or $12.02 to send $200. Monetary costs aren’t the only thing that plague payments: it can also take days for payments to arrive (Table 1).

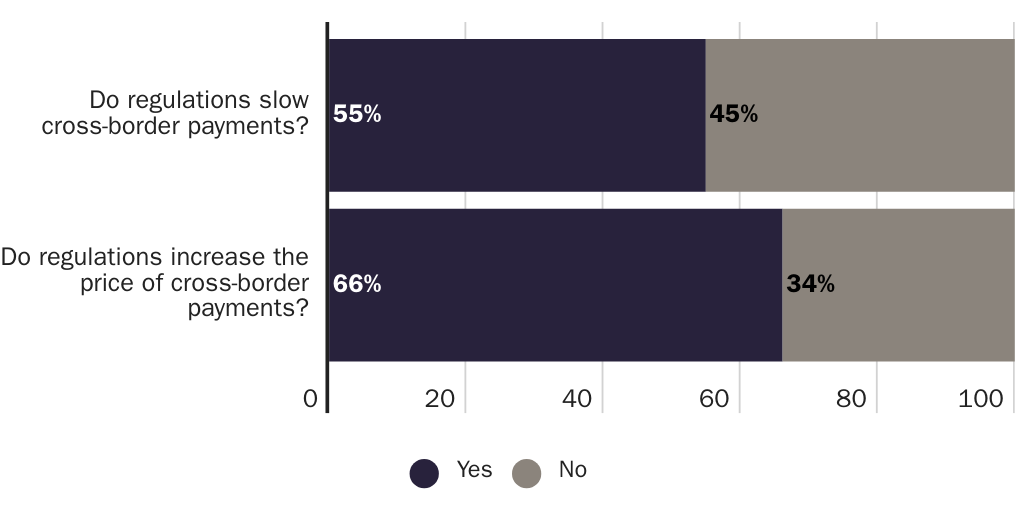

This critique, however, is not one that companies should suffer in a vacuum considering that both the fees and the delays are partially a result of the laws and regulations that govern the financial system. While sending money to friends and family should be a simple endeavor as people should be free to exchange with one another, governments around the world have created a labyrinth of requirements and obstacles as part of their efforts in the never-ending wars on drugs and terror. These requirements force financial institutions to check and recheck for the possibility of fraud, money laundering, or any other potentially suspicious activity. To make matters worse, the institutions that offer international transfers must comply with the requirements in both the country of origin and the country set as the destination—in effect doubling the regulatory burden. In late 2021, 55 percent of the banks surveyed by the Financial Action Task Force said that complying with multiple regulatory requirements significantly slowed their settlement times. To make matters worse, 66 percent of those banks said multiple regulatory requirements also raised the cost of cross‐border payments (Figure 2).

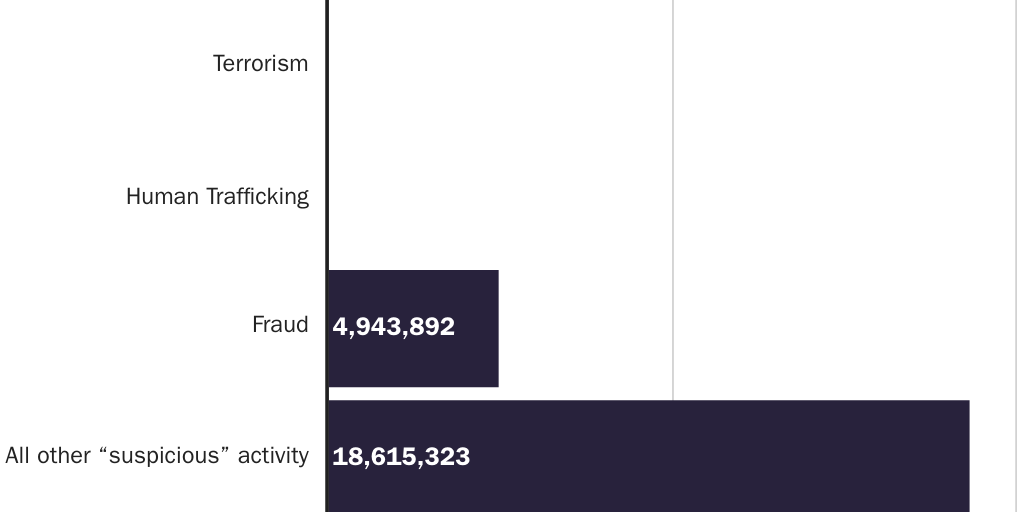

To put these costs into perspective, it is estimated that the U.S. financial system spent $46 billion in 2022 on complying with the Bank Secrecy Act regime. Supporters of this regime may be tempted to point out that the laws are there to catch criminals and that therefore the costs are justified. However, the evidence that is available suggests otherwise (Figure 3). Out of the over 23 million suspicious activity reports that depository institutions filed between 2014 and 2021, less than a quarter of the reports were for the suspicion of terrorism (0.01 percent), human trafficking (0.03 percent), or fraud (20.97 percent). The vast majority of the reports were filed because financial institutions were not sure where a customer’s funds came from, they suspected that the transactions were out of the norm for the customer, or they saw that the customer used multiple accounts. Yet even though those reports are less likely to be thwarting actual criminals, the cost of compliance is incurred just the same, and in effect, payments across borders are slower and costlier than they should be.

Trapped under Illiberalism

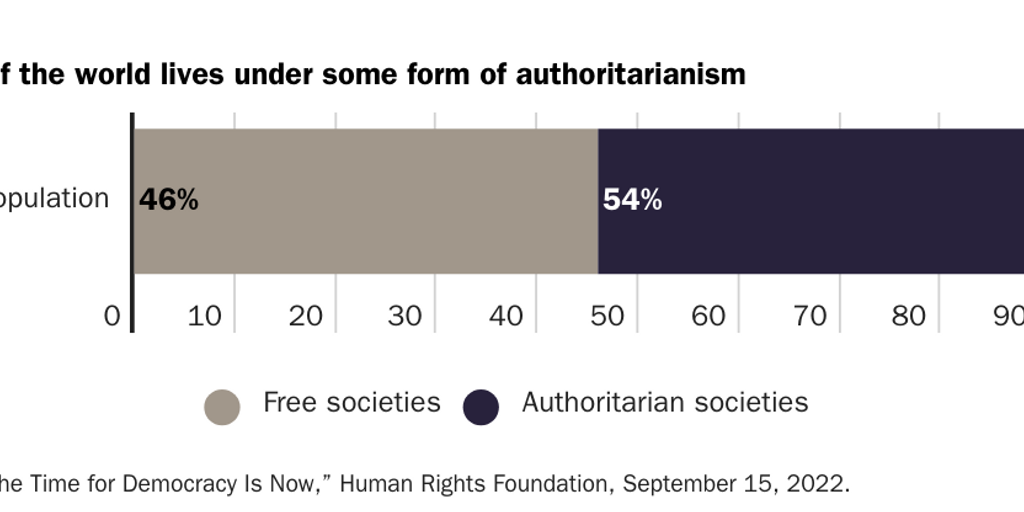

The Human Rights Foundation estimates that approximately 54 percent of the world’s population lives under some form of authoritarianism (Figure 4). While people should be free to exchange with one another regardless of political borders, authoritarians regularly turn to the financial system to freeze accounts and seize assets—simultaneously trapping citizens and cutting them off from society.

In China, for example, Jimmy Lai, entrepreneur and recipient of the 2023 Milton Friedman Prize for Advancing Liberty, became the target of government intimidation due to his long-held commitment to liberty and support for the freedom protests in Hong Kong. Less than a year after arresting Lai, the Hong Kong police froze both his personal finances and the finances of three companies linked to his newspaper, Apple Daily. In Russia, Alexei Navalny, activist and founder of the Anti-Corruption Foundation, had a similar experience when Russian authorities froze his bank accounts. The freeze began just days ahead of demonstrations that were planned to protest the exclusion of opposition candidates in a local election in Moscow.

Government use of financial controls to enforce illiberal public policy is not, however, limited to overtly oppressive regimes like China or Russia. In 2022 in Canada, for example, Prime Minister Justin Trudeau resorted to invoking the Emergencies Act for the first time in Canadian history to choke off protests over COVID-19 restrictions. As donations began to flow in from around the world (many coming from the United States), Trudeau chose to freeze the bank accounts of protestors to restrict access to funding and cut the protestors off from society. The United States has also been unable to resist the temptation to use the financial system as a means for social control. Perhaps in the most infamous example, Operation Choke Point was a Department of Justice initiative to go after politically disfavored businesses (e.g., state‐licensed cannabis dispensaries, payday lenders, pawn shops, or gun shops). Coordinating with other federal agencies, the Department of Justice pressured financial institutions to deny services to these lawful businesses to, as one official described it, “chok[e] them off from the very air they need to survive.”

Governments of all types thus recognize that the traditional financial system is an effective tool for social control. More so, in a time when social media can be used to rally support from around the globe, governments recognize that using the financial system does not generate significant backlash given its relatively hidden nature. Unlike when riot police are used, there are no photos of an official striking a devastating blow to a protestor or tear gas filling the streets. Instead, the moment of impact is when victims receive a call from the bank or an error message in an app to notify them that they no longer have access to their finances. And yet, it can halt people in their tracks all the same—effectively cutting them off from their local community and the world at large. For the billions of people living under overt authoritarianism or simply subject to ill-considered laws, the potential for abuse of the traditional financial system is all too recognizable.

A Lack of Competition

Failure to secure a stable national currency has been a long-standing issue for governments worldwide (Figure 5). Pictures of streets littered with cash or citizens carrying baskets of money have become hallmarks of hyperinflation. Yet one of the reasons that this mismanagement has been allowed to persist is because governments rarely face competition in the realm of money. Until the emergence of cryptocurrency, the most common form of monetary competition was that of people abroad choosing to use the dollar—a process known as dollarization.

Yet, there are still pitfalls given how highly limited this competition is. For instance, shortly after the Taliban took control of Kabul in August 2021, the U.S. government stopped all shipments of U.S. dollars headed to Afghanistan and froze the accounts of the Afghani government at the Federal Reserve and U.S. banks. In practice, this decision meant that despite having no control over the actions of the Taliban, the dollarized economy in Afghanistan was brought to a halt and citizens were suddenly faced with a cash shortage.

With that said, the U.S. government is not alone in undermining the reach of the dollar. Foreign governments have also turned to prohibitions to prevent alternative currencies (i.e., the dollar or euro) from gaining use. In 2019, Zimbabwe’s government banned foreign currencies in an attempt to spur citizens into using the Zimbabwe dollar. Moments like these showcase why broader competition in the realm of money is necessary. Although globalization has helped get better money into the hands of people around the world, governments have persisted in their efforts to restrict that access.

Every day that people are not free to choose a sounder currency is a day that trade is slowed, investments are foregone, and economies regress. And while competition could put pressure on governments to provide better money, most governments have responded by preventing that competition from taking place in a bid to solidify their monopolies on money issuance within their borders.

A Unique Solution in a New Form of Money

Cryptocurrency has offered a unique solution to some of the problems experienced with traditional payments. While still novel and limited in adoption, cryptocurrencies offer new avenues for remittances, new safe houses for wealth, and new opportunities for monetary freedom.

Remittances Done Differently

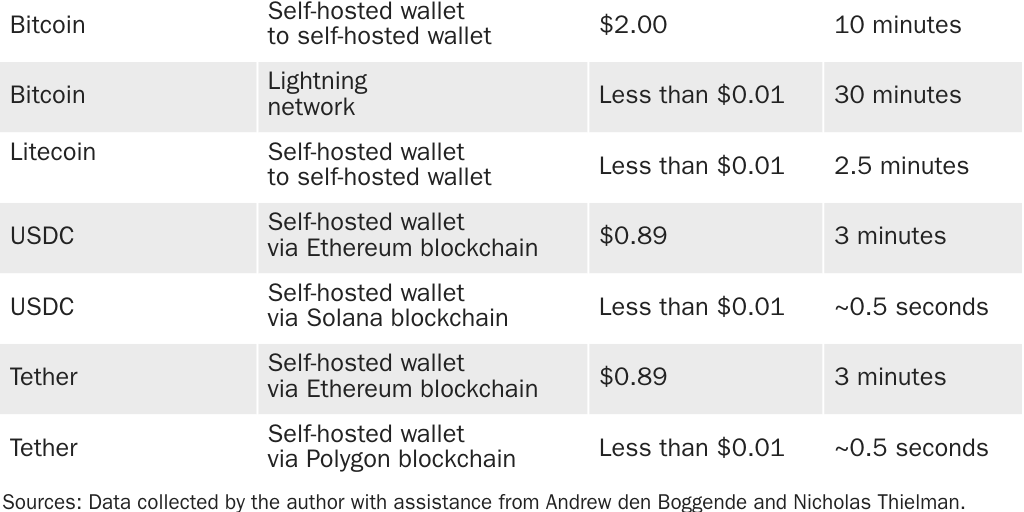

In stark contrast to the traditional financial system, a unique advantage of cryptocurrencies is that they do not discriminate based on someone’s physical location. The technology opens the door for people to freely do business with one another regardless of political borders. Whether you are in New York City or New Delhi, cryptocurrencies work the same. In fact, recent advancements have meant that one does not even need an internet connection. Now, value can be transferred as simply as sending a text. By harnessing innovation to remove these geographical and political constraints, the fees and delays associated with sending remittances can be reduced significantly (Table 2). The lack of multiday delays and dependence on a third-party transmitter is especially important when considering times of crisis—either during a natural disaster or political upheaval. The difference between waiting a few minutes and waiting a few days can drastically impact a situation.

These benefits are not without challenges. For instance, additional fees can be incurred when exchanging, for example, dollars for bitcoins and then bitcoins for pesos. In a somewhat ironic fashion, by removing traditional intermediaries (e.g., banks or payment transmitters), using cryptocurrencies for remittances introduces another step to the process as users seek access to on and off ramps. With that said, this challenge does come with a silver lining: it only matters to the extent that someone does not want to use cryptocurrency as a medium of exchange. With everything from corner stores to mortgage lenders embracing cryptocurrency, it is likely that many people may be perfectly happy to receive and keep cryptocurrency as adoption increases. In fact, this condition is especially true in countries where inflation (or hyperinflation) have destroyed the value of national currencies.

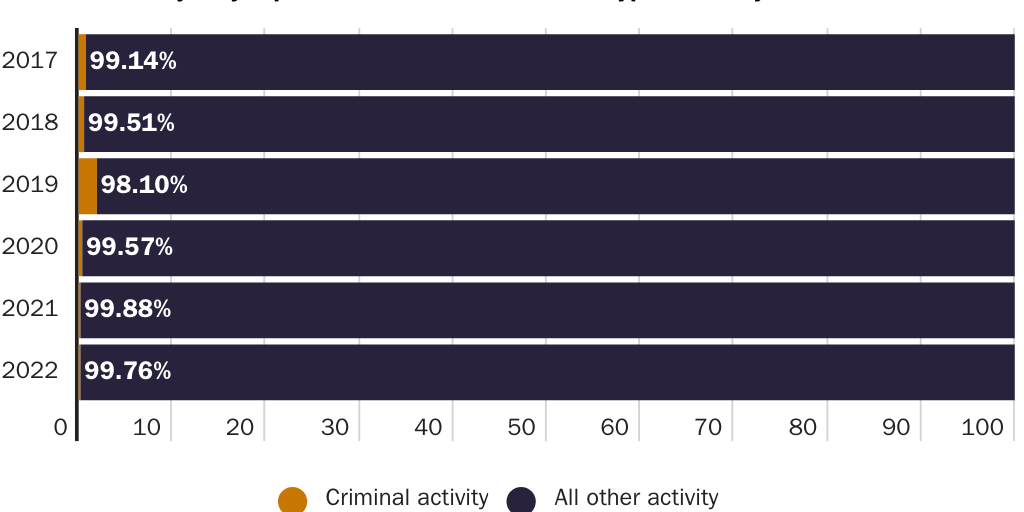

The idea of sending money outside the traditional financial system could create cause for concern. Politicians have missed no opportunity to claim that the only use of cryptocurrency is to facilitate crime. Yet, setting aside the questionable nature of financial surveillance in the traditional financial system (Figure 2), it’s important to recognize that the use of cryptocurrency is—contrary to the claims of politicians—to the benefit of law enforcement in some cases. The key condition to note is that transactions are preserved on the blockchain—enhancing the ability of governments and citizens alike to find those who engage in criminal behavior. In fact, it’s partly due to this transparency that criminal activity only represents an estimated 0.24 percent of cryptocurrency activity (Figure 6).

Resisting Illiberalism

Whether it is when a financial account is frozen during a protest in China or Canada, governments regularly turn to traditional financial institutions to choke off the opposition—and those institutions often have no choice but to comply. However, cryptocurrencies—to the extent that they are decentralized (e.g., Bitcoin)—do not involve a third party for governments to pressure. More so, the miners that do maintain the systems are so diffuse that if the government were to stop one, there are countless others across the world that would continue to ensure that the ledgers are kept up-to-date. This resilience is known as “censorship resistance.”

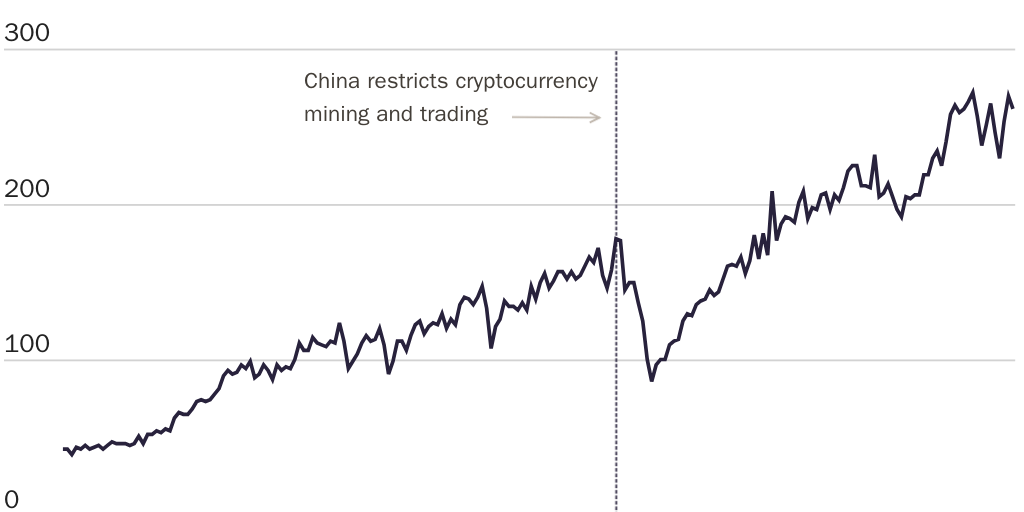

Censorship resistance is not just a theoretical possibility. Due to the restrictive policies abroad, censorship resistance can be observed in practice. For instance, consider when the Chinese government chose to ban both the trading and mining of cryptocurrency in June 2021. As the country with the largest percentage of cryptocurrency mining taking place, the prohibition would have been a death blow for any other nascent industry. In practice, however, Bitcoin mining was able to fully recover just as the year came to a close (Figure 7).

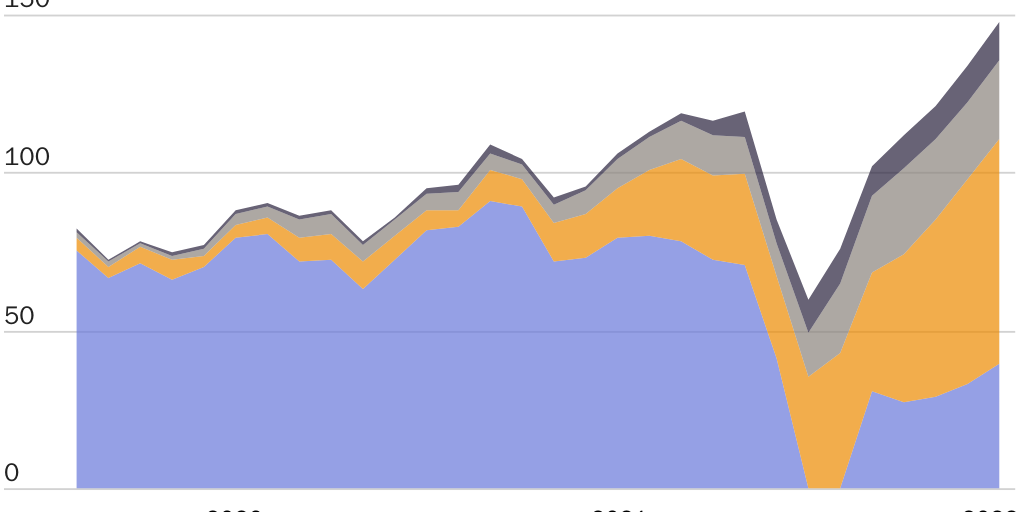

How was this recovery possible? Well, cryptocurrency mining is an industry that is particularly adept at voting with its feet. Production came to a halt in the initial wake of the ban as miners tried to close up shop (Figure 7), but the story didn’t end there. Rather, miners quickly packed up and moved across borders to the United States, Kazakhstan, Canada, and many other countries (Figure 8). Unlike the challenges other industries face (e.g., establishing new transportation routes, finding new employees, scouting new prospects, etc.), moving an industrial mining setup is just a matter of loading hundreds, or perhaps thousands, of computers into a shipping container. And that was exactly what happened shortly after the Chinese government’s crackdown. Some operations still remain in China illegally operating underground, but the vast majority were able to move across borders—showcasing that, on the world stage, cryptocurrency can survive even some of the strictest acts of government censorship.

A Lifeline for Choice

There is no shortage of examples of people around the world suffering because there is either too little money leading to cash shortages or too much money leading to hyperinflation. In either case, alternative currencies in the form of both foreign currency and cryptocurrency have provided a lifeline for those suffering under failing domestic currencies and have provided a source of motivation for those managing domestic currencies.

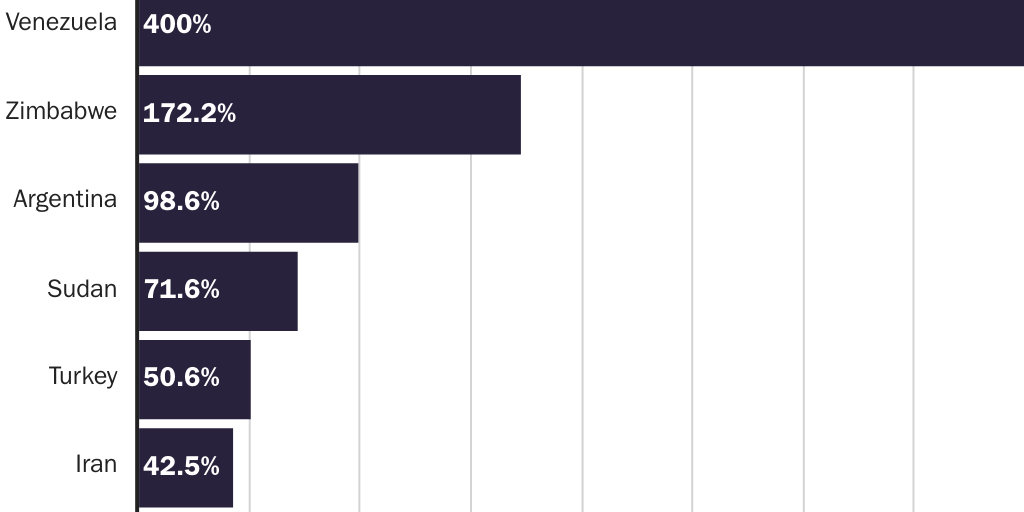

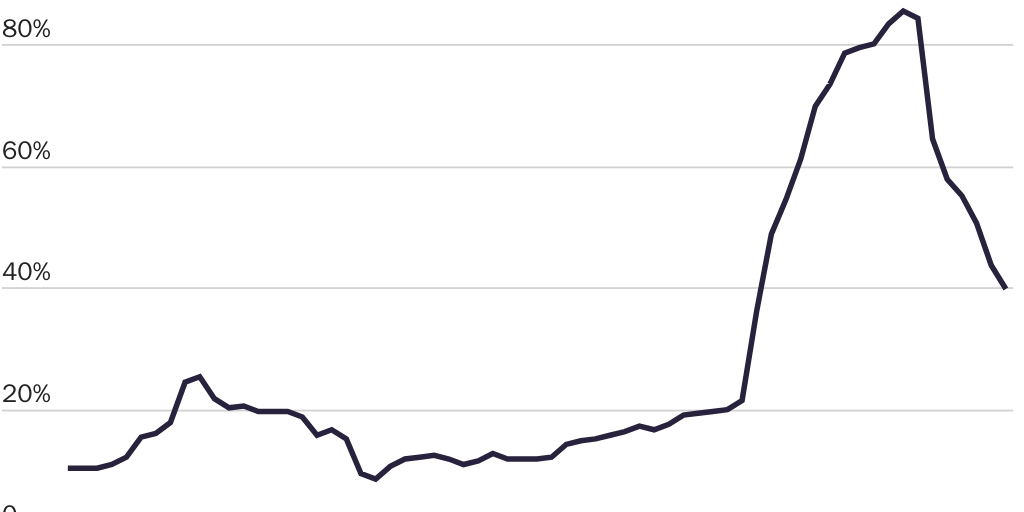

Where both legal and even logistical barriers have made it difficult for cash, or physical banknotes, to make it across borders, cryptocurrencies have offered a new opportunity due to their inherently borderless and digital nature. Several reports have shown that Turkish citizens exchanged liras for bitcoin and tether to escape the lira as inflation nearly hit 90 percent in late 2022 (Figure 9). Similar stories have also emerged in inflation-plagued Argentina. Furthermore, across all of Latin America, more than a third of consumers have said that they have made everyday purchases with cryptocurrency.

Limited as these examples may be, they showcase that there is an important role for alternative currencies in times of crisis. Where competition is allowed, alternatives can serve as a source for both motivation and inspiration. By welcoming market forces into the realm of money, issuers cannot sit idly by as inflation skyrockets into the triple digits and the economy is brought to a halt. People would simply recognize a failing money and leave for an alternative. However, maybe more importantly, allowing alternatives also allows new and innovative ideas to be tested without jeopardizing the larger system. It’s for this reason that Representative Byron Donalds (RFL) is correct in his description of currency competition when he said, “World economies work best when you have a highly interactive … marketplace where people can exchange goods, products, and currencies. It’s actually to the betterment of all currencies when there are multiple options.”

Lessons for Governments across the World

One of the great successes out of the emergence of cryptocurrency has been the reminder that the issuance of money is not a role exclusive to governments alone. Throughout much of history, the private sector has had a part to play in the issuance and handling of money. In fact, the current status quo of state monopolies and central banks is a relatively recent historical development. For example, the Federal Reserve has only been around for 110 years. With that said, policymakers worried about losing their standing should not turn to increasing restrictions, prohibitions, and other controls to close off this new chapter of monetary competition. Rather, policymakers should welcome cryptocurrency competition as both a source of motivation and inspiration for improving national currencies.

Instead of doubling down on the legal and regulatory regime that has made moving money across borders slow and costly, policymakers should welcome the innovation taking place with cryptocurrency. For example, the laws on legal tender, private coinage, and capital gains taxes should all be amended to permit greater monetary freedom with cryptocurrencies and foreign currencies. For too long, the statutes surrounding these issues have acted as both explicit and implicit barriers to currency competition.

The innovations taking place with cryptocurrency should also be a wake-up call that the existing regime built upon the Bank Secrecy Act is long overdue for reform. Without any evidence to suggest that this regime is effectively combating crime, the current approach to financial surveillance should be repealed or significantly reformed. While cryptocurrencies have opened a new path for innovation, legacy systems should not be left behind due to red tape alone.

Conclusion

From the most mundane to the most extreme of circumstances, the emergence of cryptocurrency has introduced new pathways for people around the world looking to connect in an ever-increasingly globalized economy. With that said, there are still challenges on the road ahead for this novel innovation. The learning curve, volatility, fees, and other costs all pose challenges for the adoption of the nascent technology. However, where governments—authoritarian and democratic alike—have chosen to close off borders and restrict the movement of money, cryptocurrency offers the chance for people to choose an alternative. In turn, cryptocurrency has offered the opportunity to open global exchange and move money across borders.

About the Author

This work is licensed under a Creative Commons Attribution-NonCommercial-ShareAlike 4.0 International License.