In the wake of the COVID-19 pandemic and rising U.S.-China tensions, American policymakers are again embracing industrial policy. Both President Biden and his predecessor, as well as legislators from both parties, have advocated a range of federal support for American manufacturers to fix perceived weaknesses in the U.S. economy and to counter China’s growing economic clout.

These and other industrial policy advocates, however, routinely leave unanswered important questions about U.S. industrial policy’s efficacy and necessity. First, what is industrial policy? Advocates of industrial policy often fail to define the term, thus permitting them to ignore past failures and embrace false successes while preventing a legitimate assessment of industrial policies’ costs and benefits. Yet U.S. industrial policy’s history of debate and implementation establishes several requisite elements—elements that reveal that most industrial policy successes are not industrial policy at all.

Second, what are the common obstacles to effective U.S. industrial policy? Several obstacles prevent U.S. industrial policies from generating better outcomes than the market. This includes legislators’ and bureaucrats’ inability to pick winners and efficiently allocate public resources (F. A. Hayek’s knowledge problem); factors inherent in the U.S. political system (public choice theory); lack of discipline regarding scope, duration, and budgetary costs; interaction with other government policies that distort the market at issue; and substantial unseen costs.

Third, what problems will industrial policy solve? The most common problems purportedly solved by industrial policy proposals are less serious than advocates claim or else are not fixable via industrial policy. This includes allegations of widespread U.S. deindustrialization and a broader decline in American innovation; the disappearance of good jobs; the erosion of middle-class living standards; and the destruction of American communities.

Fourth, do other countries’ industrial policies demand a U.S. industrial policy? The experiences of other countries generally cannot justify a U.S. industrial policy because countries have different economic and political systems. Regardless, industrial policy successes abroad—for example, in Japan, South Korea, and Taiwan—are exaggerated. Also, China’s economic growth and industrial policies do not justify similar U.S. policies, considering the market-based reasons for China’s rise, the Chinese policies’ immense costs, and the systemic challenges that could derail China’s future growth and geopolitical influence.

These answers to these questions argue strongly against a new embrace of industrial policy. The United States undoubtedly faces economic and geopolitical challenges, including ones related to China, but the solution does not lie in copying China’s top-down economic planning. Reality, in fact, argues the opposite.

Introduction

American policymakers on both the left and right are once again embracing industrial policy to fix alleged U.S. market failures and to counter China’s own economic interventions. Congress is currently poised to pass—with vocal White House support—several pieces of legislation that would deliver tens of billions of taxpayer dollars to “critical” domestic industries and technologies. Unfortunately, the public discourse has thus far elided several essential questions about what industrial policy actually is; how past U.S. attempts at industrial policy (properly defined) have fared; whether current proposed industrial policies can fix the economic problems they target; and whether the industrial policies of other countries—particularly China—demand that the U.S. government follow suit.

This paper will systematically answer each of these questions, addressing both economic theory and practice (as demonstrated through numerous historical and current examples of U.S. industrial policy in action). Overall, these answers reveal numerous problems that argue strongly against the adoption of new U.S. industrial policies, and they establish a high bar for future government action.

Featured Discussion

What Is Industrial Policy?

Assessing the necessity and efficacy of U.S. industrial policy requires first defining the term. Without this definition, industrial policy advocates can claim that past failures are not, in fact, industrial policy, while other policies tangentially related to government action are clear industrial policy successes. There also is the risk, as economist Herbert Stein notes in the 1986 book, The Politics of Industrial Policy, of “adopt[ing] so loose and sweeping a definition of industrial policy that it becomes virtually synonymous with overall economic policy,” thus precluding a legitimate assessment of industrial policy’s costs, benefits, and overall desirability.1 As fellow economist Mancur Olson writes in the same book, often industrial policy proposals “are so vague that they invite the reaction that industrial policy is neither a good idea nor a bad idea, but no idea at all; that it is the grin without the cat.”2 In short, if everything is industrial policy, then nothing is.

Industrial Policy’s Requisite Elements

Fortunately, industrial policy’s long history of academic debate and implementation in the United States establishes several requisite elements that, when combined, can identify whether past or proposed government initiatives are properly considered industrial policy. For example, when examining U.S. industrial policy efforts in the 1920s and 1930s, economic historian Ellis Hawley explained:

By industrial policy I mean a national policy aimed at developing or retrenching selected industries to achieve national economic goals. In this usage, I follow those who distinguish such a policy, both from policies aimed at making the macroeconomic environment more conducive to industrial development in general and from the totality of microeconomic interventions aimed at particular industries. To have an industrial policy, a nation must not only be intervening at the microeconomic level but also have a planning and coordinating mechanism through which the intervention is rationally related to national goals, a general pattern of microeconomic targets is decided upon, and particular industrial programs are worked out and implemented.3

As the Mercatus Center’s Adam Thierer wrote in a 2020 article, Hawley’s definition shows that “targeted and directed efforts to plan for specific future industrial outputs and outcomes is at the heart of a proper understanding of industrial policy.”4 Such outputs and outcomes must also occur within national borders: government procurement of foreign-made semiconductors, for example, cannot be industrial policy. Thus, industrial policy is inherently nationalist, with government support for domestic industry either indirect (e.g., tariffs, quotas, and “Buy American” mandates) or direct (e.g., subsidies for American companies, jobs, or investments).

Finally, industrial policy output and outcomes are commercial in nature, distinguishing them from both basic scientific research and defense procurement, such as fighter jets. The former has no targeted or strategic commercial application. The latter, as explained by Richard Nelson and Richard Langlois in the 1980s, is categorically different from commercial-oriented industrial policies for three reasons. First, as the sole consumer of such goods, the federal government has a unique and deep knowledge of the products or technology at issue and its own needs therefor, as well as a strong and direct interest in obtaining high-quality deliverables. Second, the public strongly believes in the legitimacy of the government’s primary mission (thus minimizing politicization and short-termism). And third, commercial spillovers are an unintended benefit, as opposed to the main purpose, of government action.5

Similar definitions and policies were offered by industrial policy advocates in the 1980s and 1990s, the last heyday of U.S. industrial policy. This includes former Clinton administration official Robert Reich in The Next American Frontier (1983); historian Otis L. Graham in Losing Time: The Industrial Policy Debate (1992); and former Commerce Department official Erik Pages in Responding to Defense Dependence (1996).6 More recently, the Carnegie Endowment’s Uri Dadush and the Hudson Institute’s Arthur Herman, citing a 2006 paper by economists Howard Pack and Kamal Saggi, have echoed these historical definitions.7

Thus, both advocates and critics coalesce around four essential features of industrial policy:

- a focus on manufacturing, to the exclusion of services and agriculture;

- targeted and directed microeconomic (firm or industry-specific) support (e.g., tariffs or subsidies), as opposed to horizontal, sector-wide, or economy-wide policies (e.g., corporate tax rate reductions or patents);

- a government plan to fix market failures, including negative externalities, and thereby achieve in targeted industries/companies clear, specific, and measurable commercial outcomes, such as jobs, investments (research and development, capital expenditures, etc.), output, or products that are better than what the market could provide in the absence of industrial policy; and

- a requirement that these market-beating commercial outcomes be generated within national borders.

As Duke University economist Michael Munger explains, industrial policy is not aimed at making the macroeconomic environment more conducive to industrial development in general. It does not target the levels of research, jobs, or even industrial activity that we generally have in the United States, nor does it even correct perceived or real shortcomings of markets by any means necessary.8 It aims at dictating the specific composition of commercial industrial activity within the nation to achieve a broader national goal.9 Thus, for example, industrial policy does not say “we need to lower carbon emissions” (via, for example, a carbon tax or a nondiscriminatory consumer subsidy paired with unilateral free trade in environmental goods); it says “we need to lower carbon emissions by subsidizing or protecting American solar panel companies and workers.”

What Industrial Policy Isn’t

Many of the industrial policies that advocates propose contain the four elements above, but often these same individuals add events or transactions that cannot be considered industrial policy without rendering the term inutile. A pro-industrial policy symposium hosted by the conservative think tank American Compass, for example, contains proposals for reshoring core digital technologies, offering subsidies for biopharmaceutical and semiconductor manufacturing, and putting local-content restrictions on electrical grid equipment and medical goods.10 All of these proposals seek to encourage domestic production of targeted commercial industries pursuant to a broader national strategy, and they therefore qualify as industrial policy rightly understood. On the other hand, the symposium adds active labor market policy, environmental regulatory reform, an infrastructure bank, World Trade Organization (WTO) reform, and vigorous antitrust action by a new Department of Economic Resilience. Yet while each might tangentially benefit domestic manufacturing, none directly supports a specific industry or targets specific market-beating commercial outputs.

This confusion permeates the current debate over industrial policy both here and abroad. In fact, many (if not most) of the industrial policy successes that proponents praise are not industrial policy at all, and they often border on the absurd. Examples include Apple and the smartphone (and almost every piece of essential hardware that it contains); Microsoft Windows; Google, Google Maps, and the entire internet; supercomputers; semiconductors and semiconductor lasers; digital optical networks; the graphical user interface; global positioning system (GPS); LED screens; plasma displays; artificial intelligence and speech recognition; videoconferencing; closed captioning; Linux and cloud computing; nanotechnology; renewable energy (lithium batteries, wind power, solar panels); nuclear energy; fracking; seismic imaging; LED lighting; airbags; the civilian aviation industry (and jet engines in particular); the pharmaceutical and biotech industries, as well as most innovative drugs, including HIV/AIDS treatments and mRNA technology; magnetic resonance imaging; advanced prosthetics; the human genome project; hybrid corn; and even lactose-free milk!11

Yet few of these modern marvels are the direct result of industrial policy in any legitimate sense. For example, industrial policy proponents routinely cite the Defense Advanced Research Projects Agency (DARPA) for its support for (or even invention of) the commercial internet as a poster child of industrial policy success. However, leaving aside the missing manufacturing nexus, DARPA did not have a plan for, or even anticipate, the internet—there was no “mission-oriented directionality” to the government support provided, nor was there any effort to make the Advanced Research Projects Agency Network (ARPANET) or early email a broader commercial success instead of simply “data links to connect computer facilities doing defense-related work.” Indeed, a decade earlier the Department of Defense had terminated research done by the Air Force into “a decentralized communications grid distinct from the traditional telephone,” and those people involved in ARPANET explained that DARPA “would never have funded a computer network in order to facilitate email.”12

Overall, ARPANET’s contributions to the commercial internet (packet switching and early email) were just that—contributions, as were private-sector efforts such as the early 20th century radio and television technologies, and during the 1970s, Xerox’s Ethernet and Randy Seuss’s Computerized Bulletin Board System.13 Just as surely, government funding has supported research that was later used by private companies to produce commercial information technology successes. But none of these scattershot government contributions to one part of an eventual commercial success can properly be considered a coherent, strategic industrial policy.

This conclusion may sound obvious, but the argument is common, especially in the tech sector.14 As noted, for example, it is routinely asserted that the federal government—via industrial policies that developed core components and financial support for Apple—invented the iPhone!15 However, as documented by researcher José Luis Ricón, such assertions equate as industrial policy any government support given at any point in the history of a product’s or company’s creation, and assign all credit for the innovation to the state.16 In particular, the industrial policy that led to the multi-touch screen was actually National Science Foundation and Central Intelligence Agency funding for basic research at the University of Delaware into an entirely different field (neuromorphic systems), and the researchers independently developed the multi-touch system to aid their state-funded research. Meanwhile, another private company, Bell Labs, was developing a similar technology without state support. The connection between the state and several other core smartphone technologies was similarly attenuated and unplanned, with foreign or private alternatives emerging in parallel. Furthermore, state funding for Apple was just a small government-secured loan issued by a private bank that supplemented substantial private startup capital that the company already had. In other words, “Apple was steaming ahead before the involvement of the [state-backed loan] and given what we know, it is most reasonable to assume that it would have continued to do so hadn’t there been government involvement.”17

Leaving aside even the wholly private innovation of packaging all of these technologies into the iPhone, crediting these technologies to industrial policy renders the term meaningless. Political scientist Alberto Mingardi finds that these sorts of misattributions routinely plague the much-heralded examples of American industrial policy success.18

The space program is also often cited as an industrial policy model, but, as economist John Kay explains, its lessons are limited at best:

Apollo was a success because the objective was specific and limited; the basic science was well understood, even if many subsidiary technological developments were needed to make the mission feasible; and the political commitment to the project was sufficiently strong to make budget overruns almost irrelevant. Centrally directed missions have sometimes succeeded when these conditions are in place; Apollo was a response to the Soviet Union’s pioneering launch of a human into space, and the greatest achievement of the USSR was the mobilisation of resources to defeat Nazi Germany.19

It’s unfathomable to think that the U.S. government—and American voters—will have the political will for another project such as the moonshot, especially for commercial objectives that, unlike space exploration, lack a traditional government nexus. Furthermore, products developed from space technologies arose not from a central industrial plan, but were instead the result of decentralized private actions utilizing directionless, government-funded research.

Finally, the COVID-19 vaccines developed under Operation Warp Speed have been heralded as a triumph of American industrial policy, but the first vaccine to reach the market, the Pfizer/BioNTech vaccine, disproves this assertion. BioNTech is a German company that had been working on mRNA vaccines for years and began its collaboration with Pfizer (based on an earlier working relationship) months before the U.S. government began Operation Warp Speed in May 2020 or contracted with the companies for a vaccine in July of that same year.20 (BioNTech management actually predicted in April 2020 that distribution of finished doses would occur in late 2020.) The companies famously refused government funds for research and development or for testing and production—efforts that instead leveraged Pfizer’s substantial preexisting U.S. manufacturing capacity, as well as multinational research teams, global capital markets and supply chains, and a logistics and transportation infrastructure that had been developed over decades. In fact, the Trump administration’s contract with Pfizer was for finished, FDA-approved vaccine doses only, and it expressly excluded from government reach essentially all stages of vaccine development (i.e., “activities that Pfizer and BioNTech have been performing and will continue to perform without use of Government funding”).21 There is even some evidence that Operation Warp Speeds’ allocation of vaccine materials to participating companies (some of which still have not produced an approved vaccine) may have impeded non-participant Pfizer’s ability to meet its initial production targets and expand production after the vaccine was approved.22

Related Read

Correcting the Record on Operation Warp Speed and Industrial Policy

The rapid development of COVID-19 vaccines is not the ‘triumph’ of government intervention that industrial-policy advocates claim.

Surely, some state support, such as funding for mRNA research and a large vaccine purchase commitment, was involved both before and during the pandemic, but it lacked the necessary commercial, strategic, or nationalist elements of industrial policy. In fact, Hungarian biochemist and mRNA visionary Katalin Karikó left her government-supported position at the University of Pennsylvania “because she was failing in the competition to win research grants” and thus “moved to the BioNTech company, where she not only created the Pfizer vaccine but also spurred Moderna to competitive imitation.”23 The National Institutes of Health grant supporting her early work actually came through her colleague, Drew Weissman, and was not directly connected to mRNA research.24 Other efforts, such as Moderna’s mRNA vaccine, had more state support, but the BioNTech/Pfizer vaccine shows that it was not a necessary condition for producing a wildly successful COVID-19 vaccine.

What Obstacles Must Industrial Policy Overcome in the United States?

American industrial policies face several obstacles that prevent their effective implementation. This section provides the most common of those obstacles, as well as real-world examples of how they have plagued past U.S. industrial policy efforts—and thus why new industrial policy proposals should, in general, be opposed.

The Knowledge Problem

Perhaps the most widespread industrial policy obstacle is the knowledge problem. In “The Use of Knowledge in Society,” Nobel laureate F. A. Hayek explained that the information needed to secure the best use of scarce national resources “never exists in concentrated or integrated form but solely as the dispersed bits of incomplete and frequently contradictory knowledge which all the separate individuals possess.” Because this information is unique and ever-changing, central planners cannot discern it via aggregate, retrospective statistics: “The continuous flow of goods and services is maintained by constant deliberate adjustments, by new dispositions made every day in the light of circumstances not known the day before, by B stepping in at once when A fails to deliver.”25

Thus, decentralized, market-based economic activity in general produces better outcomes than centrally planned activity (one authority for the whole economic system) because the former better mobilizes the diffuse knowledge—via price signals and millions of individual, real-time, dynamic transactions—that are needed for economic actors to make relevant decisions. Because no single person possesses all such knowledge in real time, economic planners must show how their “solution is produced by the interactions of people each of whom possesses only partial knowledge” and fixes “the unavoidable imperfection of man’s knowledge and the consequent need for a process by which knowledge is constantly communicated and acquired.”26 They rarely do.

A core part of industrial policy’s knowledge problem is timing: because markets and personal preferences are constantly evolving, the facts (products, investments, supply and demand, etc.) on which an industrial policy is designed will inevitably be different than the facts that exist at the time it is approved, and they will likely change again (and again) upon implementation. Discovery is endless. Thus, history repeatedly has shown that the “critical technologies” (and suppliers) of today are often not so critical tomorrow, and only markets are flexible and nimble enough to reveal the difference. Planners don’t stand a chance.

Past U.S. industrial policy efforts have often struggled to surmount the knowledge problem, particularly in high technology goods. As technology experts Patrick Windham, Christopher T. Hill, and David Cheney noted in 2020, for example, “US efforts in the 1990s to identify ‘critical technologies’ did not succeed, partly because it is hard to predict which technologies will be most valuable in the future.”27 James L. Schoff of the Carnegie Endowment for International Peace cites these efforts among the U.S. “technonationalism” failures in the 1980s and 1990s. He documents how past efforts to support critical technologies, (as defined by a National Critical Technologies Panel) through trade and investment restrictions, subsidies, and public-private consortia failed because the government—which was worried about Japan at the time—could not foresee how the marketplace would develop. The U.S. government therefore focused on current national champions such as Motorola and Toshiba, and missed how the internet would transform mobile and digital technologies and “stimulate the rise of internet titans” that today “possess some of the world’s most coveted technology, investing more than most governments do to push new boundaries and accelerate change through design and systems integration.”28 After noting another U.S. government miscue—seeing Japan as an unstoppable technological powerhouse—Schoff explains that American firms “prospered because of their ability to innovate and compete effectively, not because of such technonationalist or protectionist measures.”29

Even if policymakers pick the right industry to promote, moreover, they can struggle to identify and support the right product in that industry. For example, U.S. semiconductor policy in the 1980s saw dynamic random access memory (DRAM) chips as being central to national security and the future of U.S. global technology leadership and believed that trade restrictions would encourage new American entrants in the DRAM market. Yet no such investments occurred because U.S. firms were exiting the DRAM market after rightly determining that future success would be in advanced microprocessors, specialty chips, and design, rather than “high-volume, low-profit commodity” memory chips.30

Similar problems plagued contemporaneous U.S. supercomputer policy, which targeted older technology and vector supercomputers produced by the American firm Cray and Japan’s NEC, just as those products were losing out to non-vector supercomputers, and as the supercomputer industry was undergoing major structural changes that rendered trade protection obsolete.31 As the American Enterprise Institute’s Claude Barfield explains in his book High Tech Protectionism, “With supercomputers, as with semiconductors and flat panels, government officials either never understood or willfully ignored the structure of the industry and the nature of worldwide competition in the sector [and] seemed blissfully unaware of the technological trajectories of the industry.”32

Examples of knowledge problem failures are not limited to history books. For example, in March 2020 the Trump administration invoked the Defense Production Act to push domestic manufacturers to make more ventilators, which were deemed essential to fighting the novel coronavirus at that time. By the summer, however, medical professionals determined that ventilators were not as critical as they had once thought, but producers continued to churn them out under government orders, leading to reports of the goods piling up in a strategic reserve or being donated to “countries that don’t need or can’t use them.”33 According to a December 2020 report from the U.S. International Trade Commission, production for other medical goods funded by the Defense Production Act will only come online after mid‐2021 (with the virus more contained), even though there was evidence of a domestic medical goods glut in late January.34

Public Choice—Especially in the American System

Government industrial policy plans also face obstacles inherent in the political system that produces and implements those policies. As detailed in the work of public choice theory, political actors act not in the public interest, but in their own rational self-interest, and thus they use the political systems in which they operate to make themselves, not the general public, better off. Elected officials’ primary goal is therefore reelection, whereas bureaucrats strive to advance or protect their own careers.

Public choice distorts both the design and implementation of industrial policies. On the former, elected officials frequently advance legislative policies that confer concentrated benefits upon small, homogenous, often local interest groups and impose diffuse (but larger) costs upon the public, because only the former groups have sufficient motivation to follow the issues closely and apply political pressure through lobbying, campaign contributions, and votes. Because members of the general public are rationally ignorant about these policies (and thus do not tie their votes or contributions to them), elected officials act rationally in supporting the policies, even when they are known to produce net losses for the country. This collective action problem not only generates pork-barrel projects (often through “logrolling” bargains, in which legislators trade votes on each other’s pet projects), but it also makes reform or elimination of these programs exceedingly difficult, regardless of their efficacy.35

The same political pressures that distort elected officials’ support for an industrial policy can similarly distort the federal bureaucracy’s work to effectuate it. Research shows, for example, that government agencies’ agendas often mirror those of the members of the congressional committees that primarily oversee them—members that often actively seek out these committee assignments in order to affect the regulatory agencies beneath them. Similarly, studies show that agencies can become “captured” by motivated special interest groups or their elected benefactors, who use the agency to further their own narrow interests at the broader public’s expense.36 Even where political pressure is limited (often by design), capture can occur where bureaucrats lack the same level of specialized knowledge as the entities they regulate, and thus they grow to rely on those entities for both information and manpower.

All industrial policies face these political impediments, but two aspects of the American system amplify them. First, large segments of Congress may be replaced every two years and the president every four. This dynamic not only injects short-term thinking and uncertainty into the decisionmaking process, but also makes elected officials more risk-averse and focused on reelection instead of the long-term national interest. Thus, as Mancur Olson explained in 1986, “It is precisely in the areas of uncertainty like high technology and new industries that private venture capital has the greatest advantage” over government.37 This dynamic has likely worsened since the 1980s, owing partly to longer presidential campaigns that far exceed those in other countries.38 Representatives today essentially start campaigning for the next election shortly after winning the last one.

Second, the United States has a well-developed lobbying and interest group system, which would inevitably affect, and likely deteriorate, the design and implementation of any significant industrial policy. As Olson explained, because existing organized interests would greatly influence any industrial policy, advocates must explain how proposals to allocate capital on preferential terms to promising new firms in emerging technologies (who usually lack lobbying power) will be insulated from powerful, often declining, firms with a strong lobbying presence.39 The effect of interest group pressure on federal industrial policy formation and implementation has doubtless increased since Olson first opined on the issue 35 years ago.

Past U.S. industrial policy efforts show how public choice issues can thwart planners’ intentions. For example, Windham, Hill, and Cheney note that, along with knowledge problem issues, U.S. critical technologies efforts in the 1990s failed “because decisions about R&D funding priorities inevitably become political, as groups and leaders vie to have their favorites supported”—a process that “results in a broad list that pleases everyone but is largely useless as a guide to policy.”40

When policies are implemented, moreover, politics often intervenes—even in systems that are designed to be insulated from the political process. The supercomputer policy in the 1990s was essentially client-service for one American company, Cray, and its computer model, while ignoring other American market entrants, such as Hewlett-Packard, IBM, Intel, and Sun Microsystems, which offered different, and arguably better, products.41 To block a potential National Science Foundation purchase of a supercomputer made by Cray’s Japanese rival NEC, the House of Representatives passed legislation sponsored by Rep. David R. Obey (D‑WI), whose district included a Cray facility, that all but guaranteed that Cray would win the contract, and the Commerce Department imposed record-setting antidumping duties of 454 percent on Japanese supercomputer imports in 1997.42 The duties pressured NEC to agree to invest $25 million in Cray, in exchange for Cray dropping the case, and give Cray exclusive rights to sell NEC’s vector supercomputers in the United States.43 This legal extortion scheme was all the more brazen given that Cray did not even make a vector supercomputer at the time its case blocking NEC’s model was settled.

Today, the supposedly impartial Department of Commerce’s abuse of the U.S. antidumping law, which permits remedial duties on dumped imports found to injure U.S. manufacturers and workers, is common practice. The agency’s actions result in duties that go far beyond the levels needed to remedy injurious dumping, while also revealing that it is an agency captured by domestic interest groups (especially the steel industry); that it is unconcerned with the views of diffuse consumers (including other manufacturers); and that it is unburdened by congressional or judicial checks on its authority.44

More recent government efforts to support clean coal and carbon capture technology (CCT) have also fallen victim to politics. A 2018 review by George Mason University’s David Hart of 53 energy technology demonstration projects that were funded by the 2009 American Recovery and Reinvestment Act (ARRA) and administered by the Department of Energy (DOE) reveals that coal-related CCT projects “dominate[d] the portfolio from a fiscal perspective … accounting for about five out of every six dollars allocated to energy-demonstration projects during the Obama era.” They also were subject to more lenient private cost-sharing requirements and overoptimistic government expectations as to whether they would attract follow-on private investment, and were disconnected from “the benefits that each sector might reasonably expect to receive from a project.”45 Meanwhile, technologies with more potential, such as nuclear power, renewables, and gas-fired electricity plants, were ignored.

The government’s special treatment of CCT projects, Hart notes, was due at least in part to politics—especially when it came to the largest project in DOE’s portfolio (which received almost one-quarter of all government funding), FutureGen:

This megaproject, which dates back to 2003 and was terminated for the first time in 2008, was revived through ARRA funding earmarked for its Illinois site. President Obama, then a senator from Illinois, had vowed during his 2008 campaign to support clean coal technologies, and the state of Illinois (which had invested its own funds in the project) and its representatives in Congress (and those of surrounding states) pushed to include it among the “shovel-ready” projects eligible for the stimulus. Much like the Clinch River breeder reactor demonstration project … the local fiscal benefits of FutureGen apparently weighed heavily in its vampire-like rise from the dead.46

Another federally funded clean coal project—the demonstration plant in Kemper, Mississippi—was excluded from Hart’s analysis because it had a different funding source, the 2006 Clean Coal Power Initiative, but this “model of President Obama’s climate plan” also suffered public choice problems.47

Then, of course, there is the case of Solyndra and the Obama administration’s “Section 1705” loan program funded by the ARRA. As the Mercatus Center’s Veronique de Rugy explains, Solyndra spent almost $1.8 million on lobbyists, employing six firms with ties to Congress and the White House, while DOE reviewed its loan application. Overall, almost $4 billion in DOE grants and financing went to companies with connections to officials in the Obama administration. De Rugy adds that “nearly 90 percent of the 1705 loan guarantees went to subsidize projects backed by large, politically connected companies including NRG Energy Inc. and Goldman Sachs.”48

Related Read

The Pandemic Does Not Demand Government Micromanagement of Global Supply Chains

Evidence and analysis refute current arguments that economic nationalism would bolster the U.S. industrial base (and thus national resiliency). Instead, American protectionism has been repeatedly found to weaken the U.S. manufacturing sector and the economy more broadly.

Two separate analyses, one from the Reason Foundation and one from Georgetown University, found a significant connection between Section 1705 loan sizes and their recipients’ lobbying efforts.49 These results are consistent with recent research finding that politically connected firms (as measured by contributions to home state elections) are “64 percent more likely to secure an ARRA grant and receive 10 percent larger grants” than other, less-connected companies, yet “state-level employment creation associated with grants channeled through politically connected firms is nil.”50 Analyses have also found that the Section 1705 and other ARRA-funded loan guarantee programs administered by DOE suffered from other political problems, such as conflicting statutory mandates, time constraints, or uneconomic objectives such as job protection and Buy American rules.51

Most recently, a New York Times investigation into Maryland vaccine manufacturer and longtime government contractor Emergent BioSolutions found that the company invested heavily in lobbying while ignoring various safety and manufacturing best practices. It had effectively “captured” the Biomedical Advanced Research and Development Authority, which was authorized to disburse and monitor pandemic-related contracts, and yet, despite repeated contracting failures, Emergent was rewarded with a $628 million contract to manufacture COVID-19 vaccines. The company’s actions ultimately imperiled millions of doses of Johnson & Johnson vaccines and weakened the Strategic National Stockpile by monopolizing its $500 million annual budget and thus reducing the taxpayer dollars available for pandemic-related supplies.52

These examples not only show how public choice can undermine, if not actively work against, industrial policy objectives, but they also show that systems designed to be governed by neutral arbiters and to be insulated from political pressures have nevertheless become distorted by politics—just as public choice theory predicts.

Lack of Discipline

American industrial policies can also suffer from a lack of discipline regarding scope, duration, and budgetary costs—often due to public choice issues. Unlike private actions, the successes or failures of which are usually adjudicated (often ruthlessly) by the market, government policies often live or die based on political considerations rather than their actual efficacy. As the Brookings Institution’s Linda Cohen and colleagues explain in their 1991 book, The Technology Pork Barrel:

The second difference between public and private decisionmaking is the institutional structure in which decisionmakers are evaluated. Although retrospective evaluation of R&D is difficult and imperfect in the private sector, it is facilitated by the shared recognition that R&D is intended to provide financial returns to the company and by the presence of quantitative, quite easily observed, indexes of success, such as sales, unit costs, accounting profits, and evaluation of the firm in capital markets. In the public sector, the ultimate external test of an R&D program is its ability to generate more political support than opposition.53

The authors, who are sympathetic to U.S. industrial policy, examine six federal industrial policy programs that originated in the 1960s and 1970s and were intended to develop commercial technologies for the private sector: the supersonic transport, the Applications Technology Satellites Program, the Space Shuttle, the Clinch River Breeder Reactor Project, synthetic fuels from coal, and the Photovoltaics Commercialization Program. (They omit basic research and defense projects from their retrospective cost-benefit analysis.) They deem only one program—NASA’s satellite activities—as having been worthwhile, but it was killed before being completed. Four others were failures that cost billions of dollars, crowding out more meritorious R&D projects, yet these endured long after fiscal, technological, and commercial failure was established—a survival owed to political pressure (especially financial benefits accruing to numerous congressional districts) and captured regulators. The authors conclude that “the history of the federal R&D commercialization programs … is hardly a success story,” and that case studies overall “justify skepticism” about such programs. This is because “American political institutions introduce predictable, systematic biases into R&D programs so that, on balance, government projects will be susceptible to performance underruns and cost overruns.”54

David Hart summarizes the general problem identified by the Technology Pork Barrel examples in his 2018 paper:

Once a project’s spending spigot is turned on, its geographically concentrated fiscal benefits attract political support without regard to technological payoffs or commercial viability. Large projects are particularly attractive to legislators whether or not the technologies being demonstrated are ready to be scaled up, and even if cost, schedule, and performance targets are consistently missed. According to this view, white elephants are a virtually inevitable outcome of the U.S. political system.55

Numerous other industrial policy projects justify this conclusion, despite Hart’s personal optimism that these forces might be controlled. The Jones Act (Section 27 of the Merchant Marine Act of 1920), for example, restricts domestic shipping services to U.S.-built, ‑owned, ‑flagged, and ‑staffed vessels, in order to foment a strong domestic shipbuilding industry and a ready supply of merchant mariners during wartime, yet the act has presided over the long-term degradation of both the industry and the oceangoing merchant marine fleet.56 Despite these failures, the law has not only persisted for a century, but has actually been made more restrictive in recent decades—in large part due to the well-developed lobbying machine comprised of the U.S. shipbuilding industry, maritime unions, the Jones Act fleet, and other groups (including at least one foreign government) that benefit from the policy’s continued existence.57

The U.S. ethanol program has also lasted for decades despite numerous studies showing that corn-based ethanol imposes substantial economic and environmental damage, while raising food prices and undermining U.S. climate goals. Yet these mandates are championed by almost every presidential candidate visiting Iowa; even the pro-deregulation Trump White House expanded them in 2018, and both Republicans and Democrats—fully aware of the program’s flaws—work tirelessly to maintain it.58

The U.S. antidumping law has been subject to widespread and decades-long criticism from economists, legal scholars, and trading partners, and various aspects of its administration have been repeatedly ruled illegal by federal courts and adjudicatory panels under U.S. trade agreements (e.g., the World Trade Organization and the North American Free Trade Agreement).59 Yet the law not only remains in force—accounting for hundreds of special duties today—but has been repeatedly expanded by Congress to achieve desired protectionist results and to permit even greater abuse in the future.60 The government also routinely ignores WTO rulings against the Department of Commerce antidumping abuses—practices that are becoming increasingly common.61

The clean-coal megaprojects FutureGen and Kemper persisted in the face of repeated failures and numerous cost overruns because of their political value (and political problems in case of failure). As the New York Times wrote of Kemper, “The system of checks and balances that are supposed to keep such projects on track was outweighed by a shared and powerful incentive: The company and regulators were eager to qualify for hundreds of millions of dollars in federal subsidies for the plant, which was also aggressively promoted by Haley Barbour, who was Southern’s chief lobbyist before becoming the governor of Mississippi.”62 As noted above, FutureGen was actually revived because of its importance for former president Barack Obama and his home state of Illinois. That it and other DOE projects were ultimately canceled, Hart notes, likely resulted from a unique confluence of “temporary” events: the ARRA’s 2015 expiration date for fund disbursement, a bipartisan push for fiscal austerity, and partisan Republican opposition to Obama-era industrial policy projects.63 Only the first item might be replicable today. Even the success of the Petra Nova project “suffered chronic mechanical problems and routinely missed its targets before it was shut down” in 2020.64 According to energy experts, the project reveals the operational and financial impediments to carbon capture more broadly, yet DOE remains committed to funding it.65

Surely, not every U.S. industrial policy boondoggle lasts as long as the Jones Act, but the examples above—and many others—reveal that the risk is significant and the problems pervasive.

Featured Project

Cato Project on Jones Act Reform

The Cato Institute aims to shake up this status quo by shining a spotlight on the Jones Act’s myriad negative impacts and exposing its alleged benefits as entirely hollow. By systematically laying bare the truth about this nearly 100-year-old failed law, the Cato Institute Project on Jones Act Reform is meant to raise public awareness and lay the groundwork for its repeal or reform.

Interaction with Other Policies/Distortions

Industrial policy implementation is also often undermined by government policies that may have distorted the market at issue. As the Brookings Institution’s Shanta Devarajan explains:

The analytical case for industrial policies is based on the idea that there is a market failure that is preventing industrialization and so some form of government intervention, such as a subsidy, is necessary to correct that failure. The case is usually made in the form of elegant economic models that portray the market failure and show how intervention can lead the economy to higher growth. Most of these models assume that the relevant market failure is the only distortion in the economy. In the real world, however, these economies are full of distortions, such as labor market regulations, energy subsidies, and the like. In this setting, correcting the market failure associated with industrial policy may not promote industrialization; in fact, it may make matters worse.… Instead of relying on simple models that assume away all other distortions, governments would do better to identify the biggest distortions in the economy (such as energy subsidies) and work on correcting them. And if the biggest distortion cannot be moved, then governments need to take that into account in identifying the next biggest distortion to be addressed.66

Conflicting subsidies are a common problem in the United States. As discussed in the following section on industrial policies’ costs, for example, some DOE funding for CCT was allocated to subsidized, politically powerful ethanol producers, despite the product’s increasingly obvious shortcomings. Without government support for ethanol, other energy-demonstration projects might have been funded instead, perhaps with better results.

Then there are the laws and regulations that make industrial policy projects slower and more costly. DOE loan guarantee applicants, for example, must comply with the Davis-Bacon Act (mandating high wages and favoring labor unions) and Buy American laws (mandating domestic content and favoring U.S. manufacturers), both of which increase project costs and paperwork.67 Buy American restrictions also can limit companies’ access to needed materials or lead to project delays, and they confounded ARRA-funded infrastructure projects that were intended to boost the U.S. manufacturing sector.68 These same projects also had to comply with the National Environmental Policy Act (NEPA), as well as similar laws at the state level, which require government review and approval of federal actions that significantly affect the environment. A recent assessment of NEPA by Eli Dourado of the Center for Growth and Opportunity finds that publication of NEPA-required environmental impact statements takes an average of 4.5 years, and that ARRA projects have entailed approximately 193,000 NEPA reviews, 7,200 environmental assessments, and 850 impact statements. While these reviews are ongoing, no project funds may be disbursed or actual work begun.69

Bipartisan efforts to overhaul NEPA have thus far proven unsuccessful, and Democrats—who currently control the federal government—have expressed a desire to apply both Buy American and Davis-Bacon to future industrial policy initiatives.70 In fact, both are included in the bipartisan U.S. Innovation and Competition Act and Infrastructure Investment and Jobs Act, each of which passed the Senate in the summer of 2021 and seek to subsidize the domestic production of certain goods and technologies.71

These entrenched, policy-driven distortions, and others, can turn projected industrial policy successes into costly failures—exacerbating market failures rather than fixing them. Policymakers should therefore focus on correcting distortions caused by current policies before adding another layer of distortion via new industrial policy.

High Costs—Seen and Unseen

Finally, industrial policies impose substantial costs beyond the budgetary line item assigned to a specific project. This includes not only substantial cost overruns, but also numerous unseen costs imposed on other parts of the U.S. economy—costs that often undermine an industrial policy’s own objectives.

Seen Costs

Projects frequently fall victim to cost overruns well beyond initial budget projections. Borrowing costs, given the perpetual U.S. budget deficit, also magnify this expense. For example, in 2014 DOE claimed that its green energy lending programs were making money because the agency’s assessment ignored the interest costs that taxpayers paid to finance the loans at issue. As the Urban Institute’s Donald Marron explained at the time, DOE’s alleged $810 million profit became a $780 million loss when Treasury’s borrowing costs were included.72

Furthermore, it often takes years to determine whether a project merits its cost. For example, in 2014 DOE congratulated itself at the opening of the subsidized Abengoa cellulosic biorefinery in Hugoton, Kansas, but that plant was shut down in 2015 and sold off at a severely discounted price as part of a 2016 bankruptcy proceeding.73 By 2018, the entire U.S. cellulosic biofuel industry was on the ropes, and the Hugoton facility still sits idle today.74

Finally, cherry-picked industrial policy successes often obscure a wider portfolio of failures and thus, higher costs per success. For example, Hart’s review of DOE energy-demonstration projects found that 10 CCT projects accounted for 82 percent of all DOE funding ($3.49 billion of $4.24 billion) in 2009, but only three were still active in 2018, with the huge FutureGen project among the failures.75 Since Hart’s study, one of these three, the Petra Nova power project, was mothballed after suffering frequent outages and missing its carbon sequestration goals.76 Another, Archer Daniels Midland’s Illinois Industrial Carbon Capture and Storage Project (which captures carbon dioxide as a byproduct of ethanol production), is still operating, but it has reached only half of its annual emissions storage target.77 Only Air Products and Chemicals’ carbon capture facility in Texas (which received $284 million from DOE) can be considered successful.78 Was this one success worth the total CCT portfolio cost of $3.5 billion?

Other industrial policy portfolios raise similar issues. While Tesla famously paid back its $485 million loan under the Advanced Technology Vehicle Manufacturing program, Fisker Automotive went bankrupt without paying off its $529 million loan; Ford’s $5.937 billion loan and Nissan’s $1.448 billion loan also remain outstanding.79 Presumably, they will be paid back, but this story remains unwritten.

Unseen Costs

Beyond these seen costs are the many hidden ones that even government industrial policy successes impose on the economy, including indirect costs paid by private parties, deadweight costs to the economy, opportunity costs, misallocation of resources, unintended consequences, moral hazard and adverse selection, and uncertainty.

Indirect costs paid by others

Industrial policies that restrict access to goods and services from disfavored (usually foreign) suppliers raise prices for both the restricted items and their favored competitors, imposing significant costs on consuming companies and individuals. For example, tariffs that former president Donald Trump implemented to boost the U.S. steel and aluminum industries have been repeatedly found to raise foreign and domestic steel prices, thus harming downstream U.S. manufacturers and reducing GDP.80 Pervasive Buy American rules, which generally restrict government contracts to domestic producers, have similarly been found to act as a barrier to entering the U.S. market and to raise domestic prices in the same way that a tariff does.81

Deadweight costs

Trade restrictions or taxation to fund industrial subsidies also impose deadweight costs on the economy. For example, by raising domestic prices a tariff not only redistributes to producers money that consumers used to save when buying cheaper, non‐tariffed imports, but also reduces domestic consumption overall. This portion of the consumer surplus is simply destroyed—a deadweight loss that makes the United States, as a whole, worse off in the amount of wealth destroyed (money that consumers, pre‐tariff, could have saved, invested, or spent on other things). Economists have repeatedly found that import restrictions impose substantial deadweight costs on the economy—a key reason why so few economists support them.82 High tax rates have been found to impose similar costs.83

Opportunity costs

Industrial policy programs that entail government spending also entail opportunity costs, as explained by St. Louis Federal Reserve Economist Michelle Clark Neely:

Each subsidy given to an industry or firm generates an opportunity cost: the cost of foregone alternatives. In other words, to correctly evaluate a policy, you need to know not only what you’re getting, but also what you’re giving up. Based on industrial policy experiments in several countries, most economists have little confidence in the government’s ability to measure these benefits and costs properly.84

Given that both time and federal budgets are finite, government industrial policies replace efforts and money that could have been spent on other priorities, potentially imposing significant opportunity costs in the process. In The Technology Pork Barrel, for example, Cohen and Noll explain that the Clinch River breeder reactor “absorbed so much of the R&D budget for nuclear technology that it probably retarded overall technological progress.”85 Other nuclear projects, and the Space Shuttle, likely had similar net negative effects.86 As noted above, more recent government overspending on Emergent BioSolutions’ pricey anthrax vaccines left less money available to purchase other medical goods, such as N95 masks, for the Strategic National Stockpile, thus contributing to its shortages when COVID-19 arrived in 2020.87

These opportunity costs are sometimes mentioned when government industrial policies publicly fail, but they must also be considered when evaluating the alleged successes, too. As Duke professor Daniel Gross explains, for example, we celebrate that World War II shifted the scientific establishment from its previous projects to atomic fission, radar, and other war-related technologies, but we ignore the canceled projects’ potential benefits.88 Once these types of opportunity costs are considered, allegedly successful industrial policies can end up undermining the economy, as well as various strategic national objectives.

Misallocation of resources

Industrial policies also often distort private investment decisions, pushing resources away from productive transactions, businesses, or industries. When the Trump administration pushed automakers to produce ventilators that were never needed, their efforts occupied machinery, labor, and capital that could have been used to make cars that subsequently were in short domestic supply. The canceled $765 million loan to turn Eastman Kodak into a pharmaceutical ingredient company caused the company’s shares to surge 1900 percent, and its market capitalization at one point reached $2.2 billion (a twentyfold increase)—private capital that could not be invested elsewhere (for example, in actual U.S. pharmaceutical ingredient producer Fujifilm).89 Even after the government loan was stymied, and without any new plan for long-term financial viability (along with continued poor financial performance), the company’s shares still traded at three to four times their pre-loan announcement price, thus diverting for several months (if not longer) hundreds of millions of private investment dollars away from other companies.90

Industrial policies can also discourage private investment in industries that the government is actually trying to promote. As Harvard’s Josh Lerner explains, with respect to the Obama-era DOE’s green energy subsidies,

The enormous scale of the public investment appears to have crowded out and replaced most private spending in this area, as [venture capitalists] waited on the sideline to see where the public funds would go.… Rather than being stimulated, cleantech has fallen from 14.9 percent of venture investments in 2009 to 1.5 percent of capital deployed in the first nine months of 2019.91

With respect to the Advanced Technology Vehicle Manufacturing program in particular, Wired magazine found in 2009 that “this massive government intervention in private capital markets may have the unintended consequence of stifling innovation by reducing the flow of private capital into ventures that are not anointed by the DOE,” and then provided instances when this very risk had materialized.92

Finally, potential industrial policy beneficiaries can divert resources from their actual business to obtaining federal benefits (lobbying, grant writing, etc.), thus undermining the former. Wired notes, for example, that

Aptera Motors has struggled this year to raise money to fund production of the Aptera 2e, its innovative aerodynamic electric 3‑wheeler, recently laying off 25 percent of its staff to focus on pursuing a DOE loan. According to a source close to the company, “all of the engineers are working on documentation for the DOE loan. Not on the vehicle itself.”93

Kodak spent almost $800,000 on lobbying before it received its Defense Production Act loan, and Emergent BioSolutions has spent millions on lobbying and winning federal contracts. Overall, countless millions of dollars—dollars that could have been spent on producing better products—have instead been spent on political efforts by companies in the steel, shipbuilding, ethanol, and other industries that are common industrial policy targets.94

Unintended consequences

Industrial policies produce consequences that not only are unforeseen by government planners but also undermine the policies’ own objectives. As already noted, government subsidies intended to spur various energy innovations repeatedly discourage them. Steel protectionism has boosted less productive and innovative firms’ lobbying efforts and financial returns, thus discouraging overall innovation (R&D spending and creative destruction) in the industry.95

Numerous other examples abound. Semiconductor policy during the 1980s and 1990s sought to boost domestic producers’ global competitiveness (while diminishing their Japanese competitors), but instead it enriched Japanese chipmakers via quota “rents” and government-backed collusion and helped turn South Korean companies into global leaders.96 Jones Act shipping restrictions, intended to bolster national security, have pushed American energy consumers to buy from Russian producers and American shippers to use Chinese shipyards for repairs. Restrictions on imports of machine tools from major producer countries in the 1980s fueled the growth of China’s machine tools industry.97 Ethanol subsidies and mandates have reduced cropland, increased food prices, and harmed the environment. Buy American restrictions tied to federal transportation subsidies have raised the price of domestically produced transit buses and discouraged the purchase of more-efficient foreign-made buses, thus lowering the quality and use of public transit (fewer stops and less geographic coverage), increasing traffic congestion, and harming the environment.98 Outside of the United States, European innovation policy has stymied innovation, while Japanese industrial policy has slowed productivity growth.99 The list of countries and industries more harmed than helped by industrial policy goes on and on.

Moral hazard and adverse selection

Industrial policies also can generate moral hazard (i.e., encouraging actors to engage in overly risky behavior by protecting them from its consequences) and adverse selection (i.e., the tendency to attract the highest-risk or least-responsible actors). Research shows, for example, that government loan guarantees that insure lenders against incurring losses from default can encourage banks to take on risky borrowers, discourage them from undertaking standard due diligence to apply for credit guarantees, and attract a disproportionate share of risky borrowers, thus resulting in inefficient resource allocation overall.100 In the United States, the poster child for these problems was the Section 1705 loan guarantee program and the $535 million loan to solar panel manufacturer Solyndra that it supported.101 As explained by economist Ryan Yonk, the scandal with Solyndra was not that the company failed, but that its loan application—which a 2015 Inspector General report found was plagued with deficiencies and misrepresentations about a company with publicly known problems—was ever approved in the first place.102 In a comprehensive assessment of all DOE loans and loan programs implemented between 2009 and 2016, the Heritage Foundation’s Nick Loris found that projects routinely featured failed companies that “could not survive even with the federal government’s help,” and added that both the Government Accountability Office and DOE Office of Inspector General reports “identify that the loan programs were fraught with inefficiencies, lack of due diligence, and inadequate oversight and management.”103

Uncertainty

Industrial policies often produce uncertainties due to their inherently political nature (frequent elections, program lapses, etc.) and potential to engender trade disputes or retaliation from foreign trading partners. Numerous studies, for example, show that U.S. tariffs during the Trump administration increased trade policy uncertainty and thereby decreased investment and economic growth.104 These results are consistent with the general economics literature showing that policy uncertainty undermines investment, employment, and economic growth. As the University of Chicago’s Steven J. Davis explains,

a variety of studies find evidence that high (policy) uncertainty undermines economic performance by leading firms to delay or forego investments and hiring, by slowing productivity-enhancing factor reallocation, and by depressing consumption expenditures. This evidence points to a positive payoff in the form of stronger macroeconomic performance if policymakers can deliver greater predictability in the policy environment.105

Both theory and practice show why it is difficult, if not impossible, for industrial policies to achieve such predictability. These outcomes not only undermine the common argument that industrial policies fix market short-termism—they are similarly afflicted (if not more so)—but also show that such policies impose significant economic harms.

Almost all of these seen and unseen costs arose in the 2009 government bailouts of General Motors and Chrysler, which were deemed industrial policy successes by the Obama administration because they only cost taxpayers about $10 billion, which was the difference between the current-dollar value of funds the government invested and recouped.106 However, this total ignores the true, interest-adjusted cost to taxpayers, which the Congressional Budget Office estimates was 40 percent higher ($14 billion).107

Furthermore, as economist Daniel Ikenson has explained, even this larger dollar figure ignores all of the bailout’s hidden costs for the economy. For instance, the $61 billion allocated to these corporations could have been spent on more productive initiatives, such as retraining autoworkers. The long-term competitiveness of GM and Chrysler was diminished because they were not reorganized via standard bankruptcy proceedings. Ford and other U.S.-based automakers who did not receive special treatment lost business, thus harming not only their finances but also American consumers and the economy, because these companies’ better products and business models were not rewarded. Moral hazards arose from encouraging the continuation of the companies’ and the United Auto Workers’ irresponsible practices. Bond holders and other investors suffered because they did not receive the fair value of their holdings, potentially short-circuiting U.S. bankruptcy law along the way. Then there are the political costs of protecting well-connected favorites (here, unions), and the cost of uncertainty about whether and when political actors would again decide to intervene in the market and legal system, citing the bailout as precedent.108

If It Creates One Tesla?

Some industrial policy advocates argue that these seen and unseen costs are an expected and necessary part of backing ventures considered too risky for private capital and are worth the expense if the project ultimately supports one big winner, such as Tesla Motors. Even assuming that Tesla’s story is fully written, or that electric vehicle (EV) proliferation benefits average Americans, however, this argument must have limits: Would government backing of Tesla be worth one trillion dollars’ worth of waste, failure, and cronyism? Two trillion? Surely, some number of losers—individuals and the economy overall—would be too much, even if the government picked one winner in the process. Costly public failures might also undermine public confidence in the government and support for future federal policies, industrial or otherwise—jeopardizing the next Tesla (or more worthwhile targets) rather than nurturing it. Solyndra’s failure had this very result.109

These arguments, as well as other industrial policy defenses, also require quantifying the benefits that alleged successes confer, not merely upon the recipient companies and their workers, but on the U.S. economy more broadly. Positive externalities, market-beating R&D spillovers, and faster economic growth are often claimed, but these benefits are rarely supported by hard evidence or thorough empirical analysis. Indeed, a core theme of scholars Deirdre Nansen McCloskey and Alberto Mingardi’s book, The Myth of the Entrepreneurial State, is the lack of rigorous and systematic empirical analyses of the overall efficacy of nations’ industrial policies, as opposed to whether specific projects achieved certain deliverables.110 Pack and Saggi examined the issue in 2006 and explained a key hurdle to such analyses:

Although there are cases where government intervention coexists with success, there are many instances where industrial policy has failed to yield any gains. The most difficult issue is that relevant counterfactuals are not available. Consider the argument that Japan’s industrial policy was crucial for its success. Because we do not know how Japan would have fared under laissez-faire policies, it is difficult to attribute its success to its industrial policy. It might have done still better in the absence of industrial policy—or much worse. Given this basic difficulty, only indirect evidence can be obtained regarding the efficacy of industrial policy. Direct evidence that can “hold constant” all the required variables (as would be done in a well-specified econometric exercise) does not exist and likely never will.111

The authors nevertheless concluded that sectoral targeting has not been not effective.112 Since then, several literature reviews have come to essentially the same conclusion: the few empirical studies of industrial policy tend to focus on specific transactions and issues rather than the aggregate, economy-wide effects of industrial policy; they often suffer from methodological or data limitations; and they have produced mixed, country-specific results.113 The studies therefore cannot permit strong conclusions about the success or failure of industrial policy writ large.

Finally, one must also consider whether an industrial policy success would have occurred in a market without the supporting program. Often, subsidized successes perform no better than their unsubsidized competitors. The most recent example is the BioNTech/Pfizer COVID-19 vaccine achieving the same or better results than vaccines that received far more government support. Yonk’s 2020 assessment of DOE loan guarantee programs, for example, finds that few loans were extended that couldn’t have been obtained in the market.114 He adds:

Most Section 1705 funding has gone to large corporations who already have access to capital for investments in research, development, and deployment. Recipients of LPO [DOE Loan Program Office] guarantees include multiple Fortune 200 companies, utility companies, and multinationals. Many are wholly owned by yet larger companies. The application process itself all but ensures that only large, established companies will be capable of participating in the program. Applicants can expect to pay between $150,000 and $400,000 in fees before even being considered.115

As noted above, other analyses of the program have come to the same conclusion. Semiconductor consortium SEMATECH’s work has also been found to have produced deliverables that the market could have provided without government assistance.116 A 2020 analysis of 25 cleantech startups funded by the Advanced Research Projects Agency-Energy (ARPA‑E) in 2010 found “no clear evidence” that subsidy recipients performed better than similar cleantech startups in terms of being acquired, launching an initial public offering, or receiving venture capital funding within 10–15 years of their founding. The authors therefore conclude that the program did not achieve one of its primary goals, which was to generate “an increased likelihood of success (measured in different ways) for ARPA‑E startups compared to similar companies.”117 The authors find that awardees did obtain more patents than nonsubsidized competitors, but do not rule out that this success was due to ARPA‑E encouraging subsidy recipients to patent or choosing companies with a higher propensity to patent.118 Finally, the authors found that funding from DOE’s Office of Energy Efficiency and Renewable Energy did not affect awardees’ patenting or follow-on funding, while DOE’s Small Business Innovation Research awardees actually patented less than the average unsubsidized firm.119

The ARPA‑E program was therefore the best of the bunch. However, the bar is low, and success is still no better than what the market could produce. As one supporter of ARPA‑E put it, “one would hope to see stronger evidence of the impact of ARPA‑E support not only on follow-on funding, but also on product introductions, sales and other downstream commercialization variables over a longer time span.”120 Alas, no such evidence exists.

What Problem Will Industrial Policy Solve?

Industrial policy advocates also routinely fail to demonstrate the existence of the specific economic problem that their proposed policies will solve. The most common problems, without which new industrial policy would not be necessary, are either much less serious than advocates claim or else cannot be fixed with industrial policy. This includes allegations of widespread deindustrialization, declining manufacturing jobs and business investment, the erosion of middle-class living standards, and the destruction of American communities.

Deindustrialization

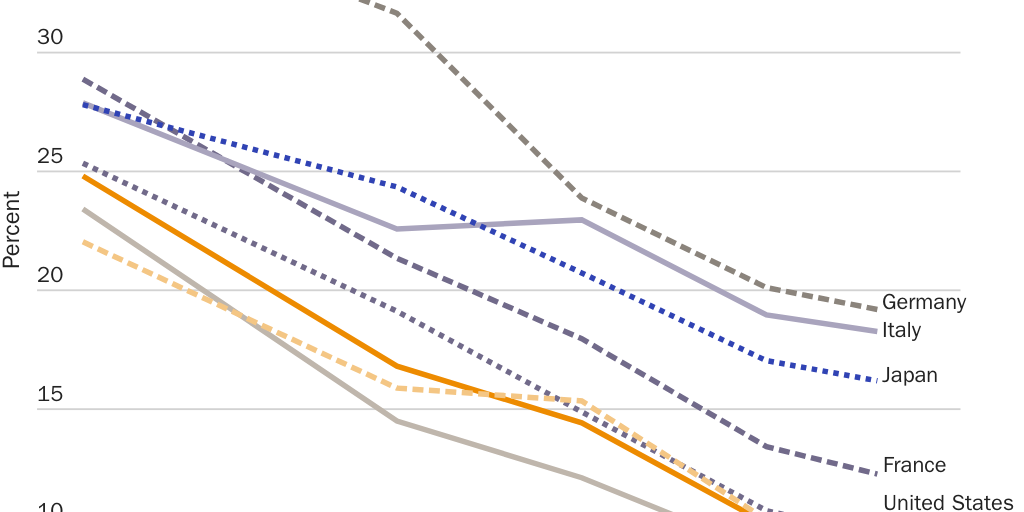

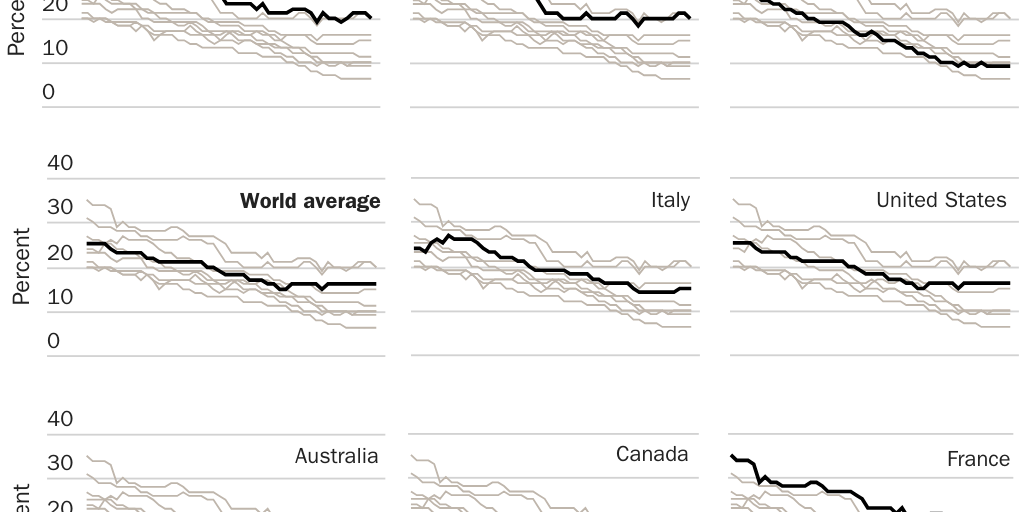

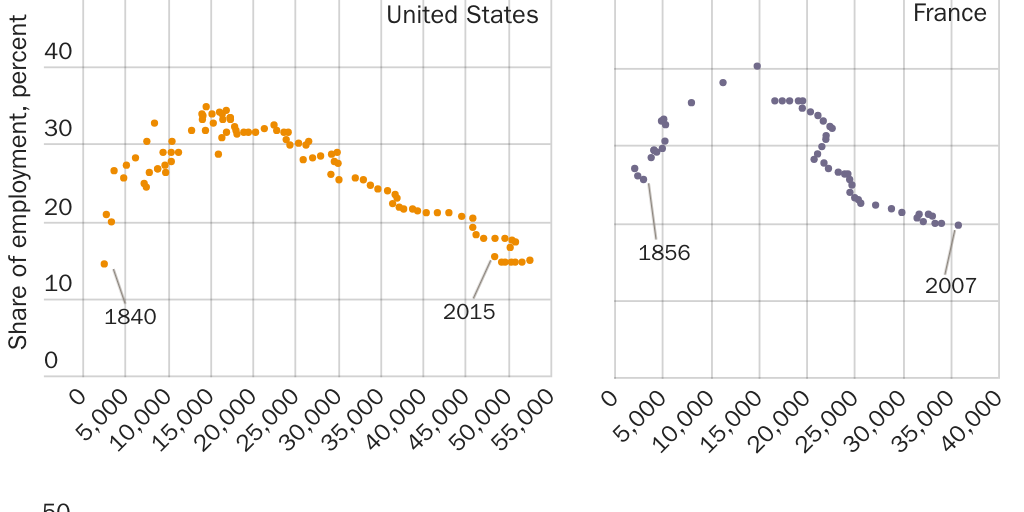

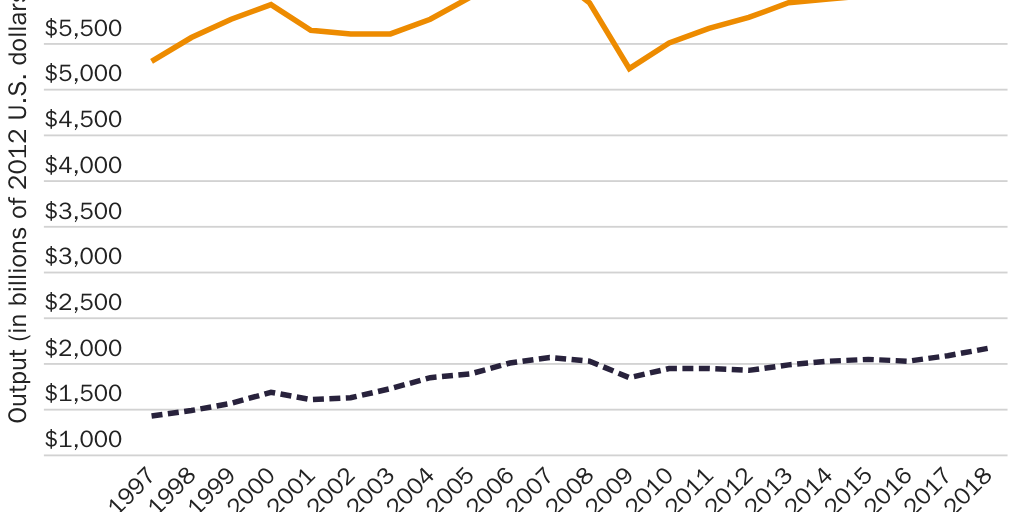

The supposed deindustrialization of the United States does not justify new industrial policies. There is little merit to the common argument that the U.S. industrial base has been dismantled by decades of free-market fundamentalism and a lack of industrial policy.121 Both the declining number of manufacturing jobs (Figure 1) and the manufacturing sector’s shrinking share of GDP (Figure 2) primarily reflect long‐term global trends that are shared by most industrialized nations and that are disconnected from specific federal economic policies, whether they are free market or interventionist.

Overall, as Figures 3 and 4 show, the historical trends in U.S. manufacturing jobs and the manufacturing sector’s GDP share are a standard story of economic development that all countries eventually experience as they get richer.

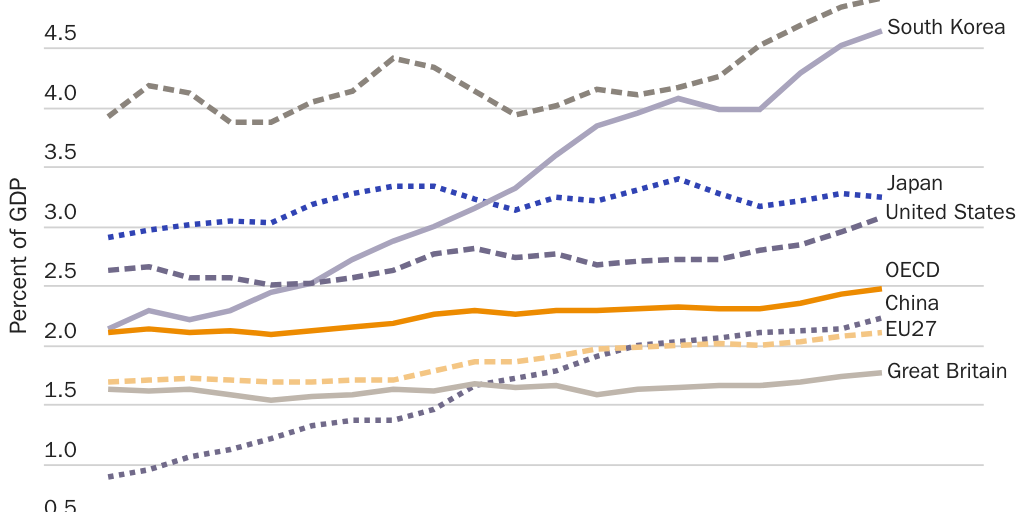

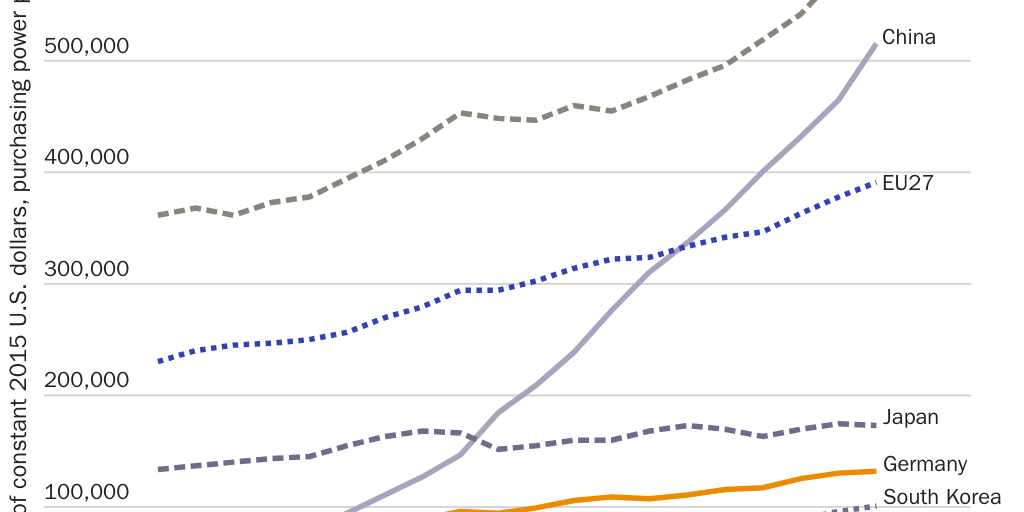

Given that these long-term, systemic trends were experienced in other countries, such as Germany and Japan, that had both trade surpluses and active, comprehensive industrial policies, there is little to suggest that new U.S. industrial policies would change the same trends in the United States.

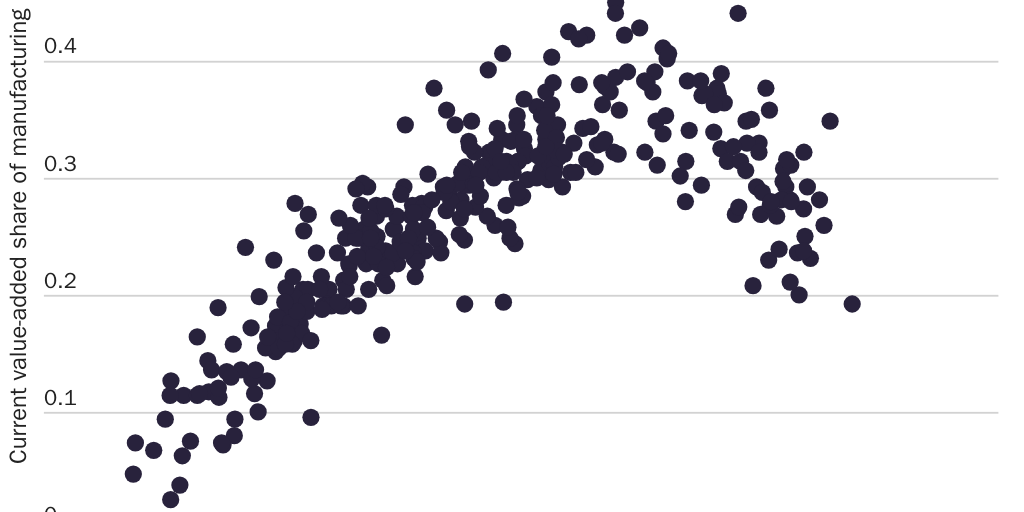

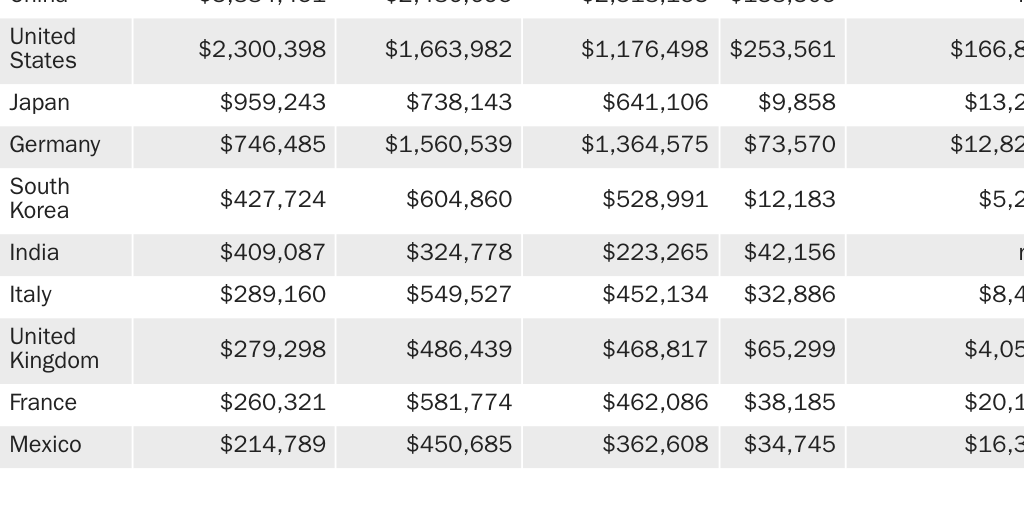

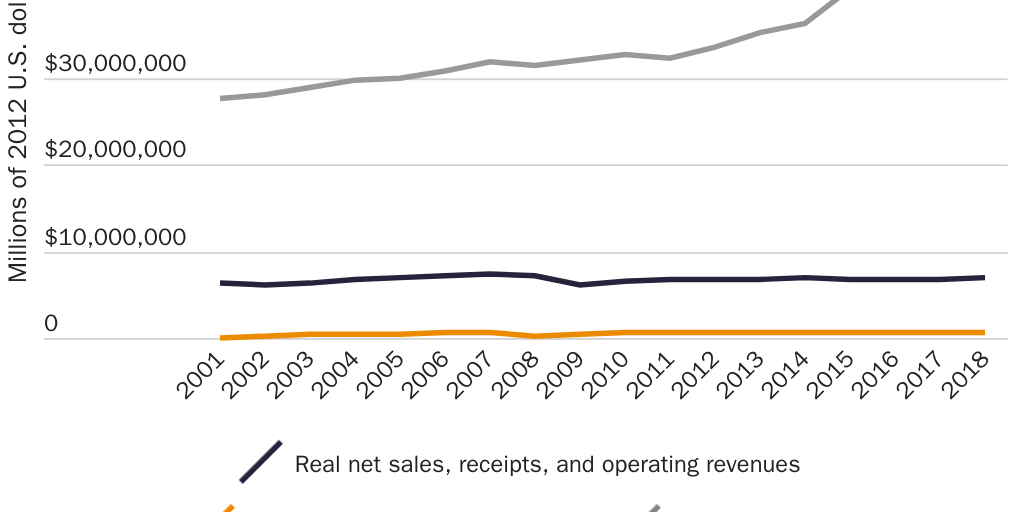

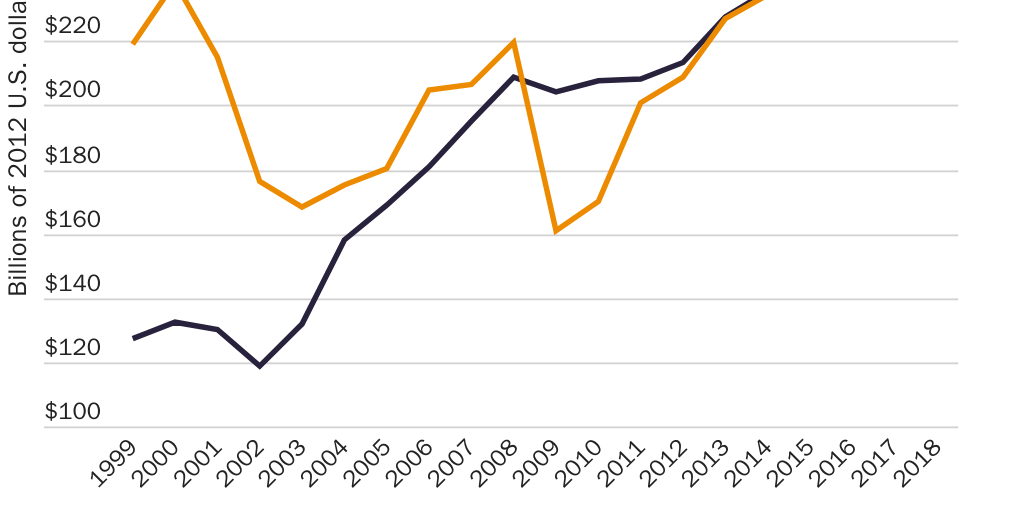

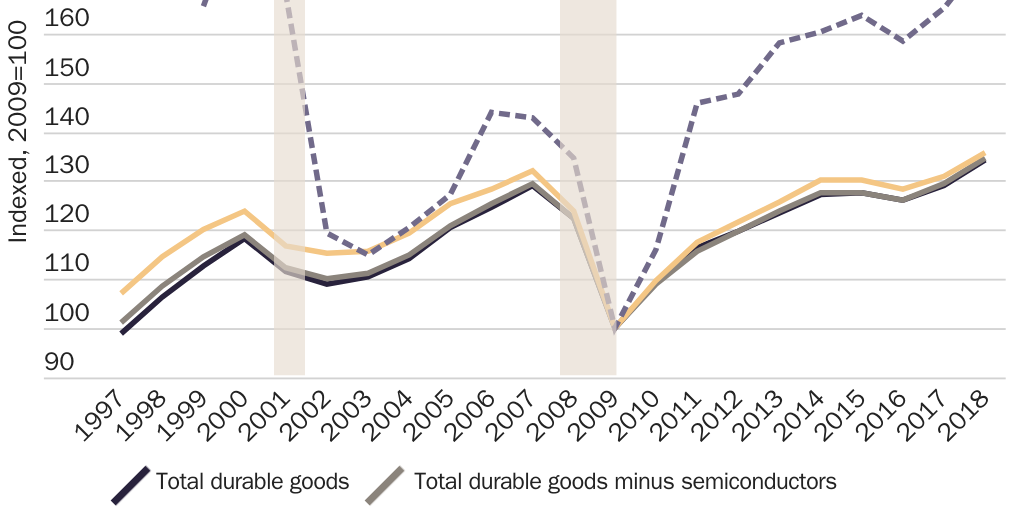

Furthermore, Table 1 and Figures 5 through 7 show that the U.S. manufacturing sector remains among the most productive in the world and has actually expanded since the 1990s—continuing earlier period trends in output, investment (both capital expenditures and R&D), and financial performance.

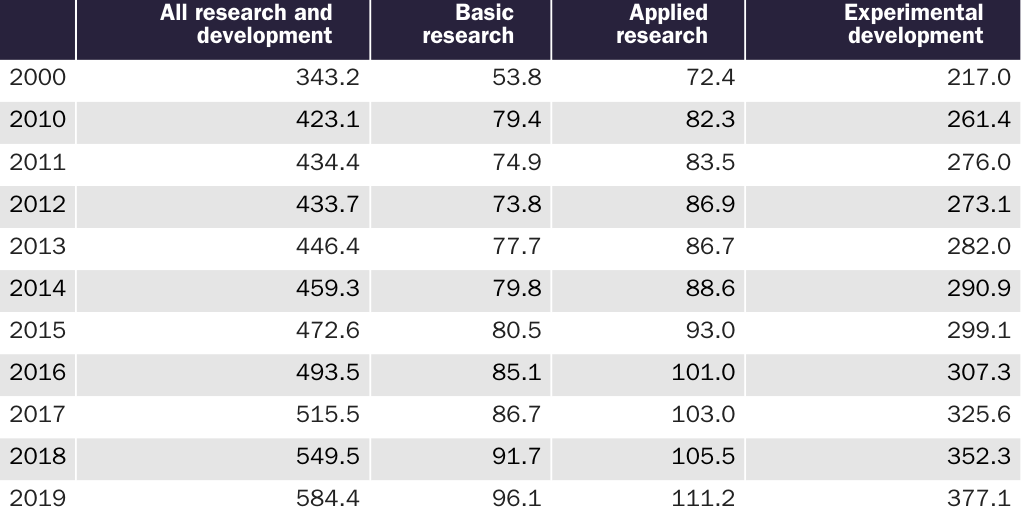

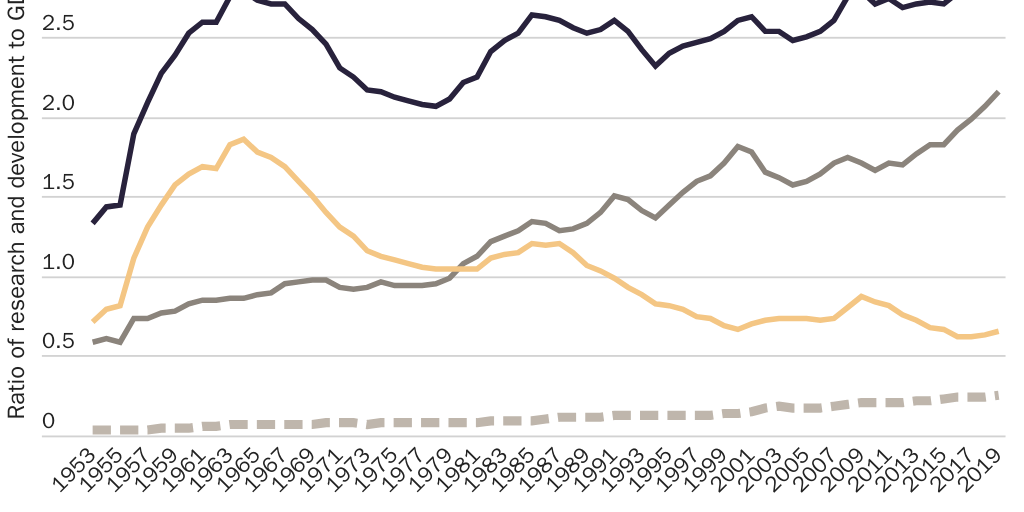

As shown in Table 2 and Figures 8 through 10, moreover, the R&D spending trends for the U.S. manufacturing sector generally track those of the nation overall, which hit all-time highs in R&D spending as a share of GDP and inflation-adjusted dollars spent.

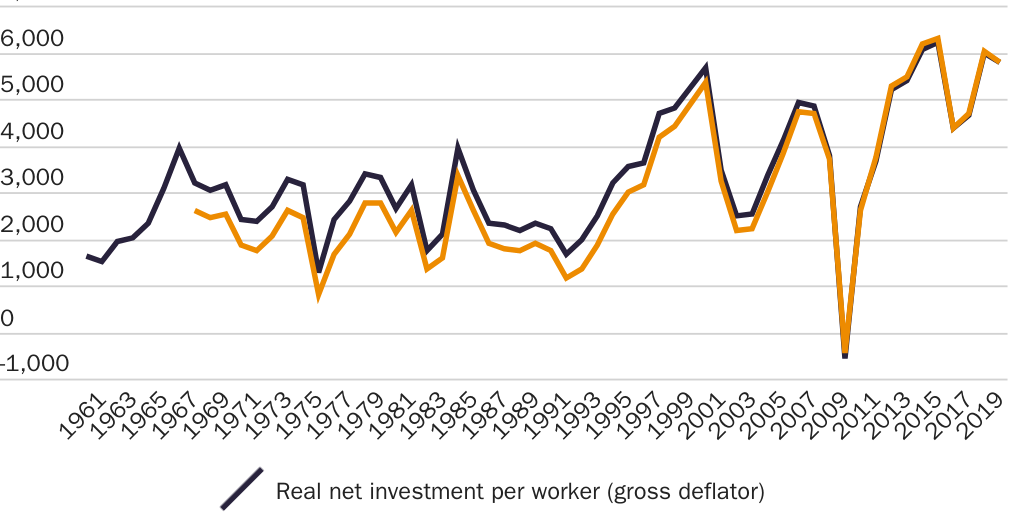

As documented by economist Donald Schneider, numerous experts have concluded that overall net investment in the nonfinancial corporate sector (i.e., new investment minus depreciation) has not declined in real terms. As shown in Figure 11, this reached an all-time high on a per worker basis during the mid-2010s and leveled off afterward.

Research from University of Houston economist Dietz Vollrath shows that a causal connection between total U.S. business investment and economic growth disappears after accounting for slowing population growth, which is not something that industrial policy can fix.122

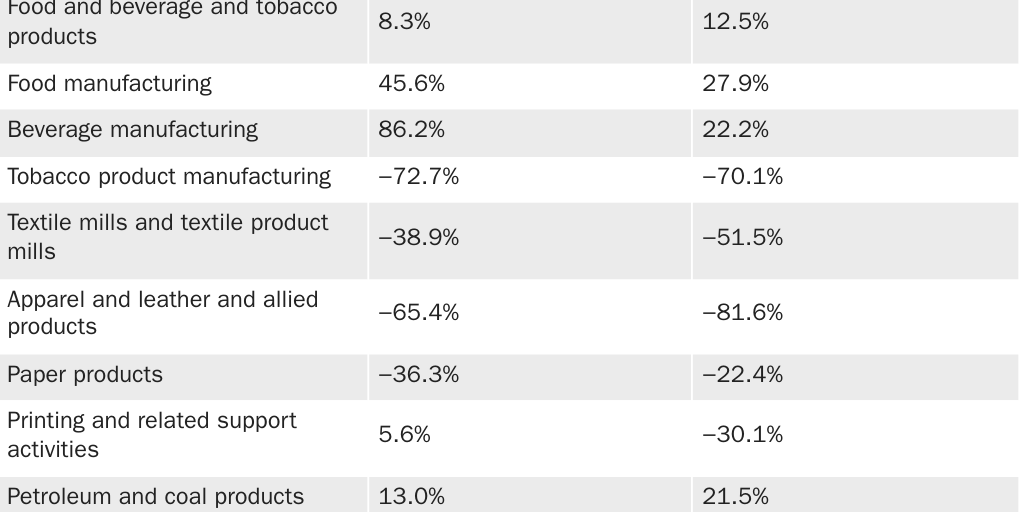

These topline data underscore that any new American industrial policy would require targeting specific industries to change the sector’s composition, not the horizontal tax or educational policies that some advocates claim to be industrial policy. And while some manufacturing industries have undoubtedly declined over the last several decades, these changes usually reflect fundamental shifts in U.S. and global markets that are driven by trade, technology, changing consumer habits, and other trends, as opposed to a weak manufacturing sector. The declines also have been offset by gains in other industries, particularly durable goods industries, such as transportation and aerospace, and high-value nondurable goods industries such as chemicals and energy (see Figure 12 and Table 3).

These and other U.S. manufacturing data reveal a flexible and dynamic sector that is generally responsive to free-market forces that are important for the health of the economy overall, not merely for the manufacturing sector. Furthermore, the offshoring or automating of low-wage, low-skill industries in the apparel, furniture, and other manufacturing industries, while undoubtedly difficult for the workers directly affected, is an important part of a healthy, dynamic economy and an essential part of economic development, moving resources from less- to more-productive domestic enterprises. This is true regardless of whether the enterprises are in manufacturing or other sectors.

Manufacturing Jobs

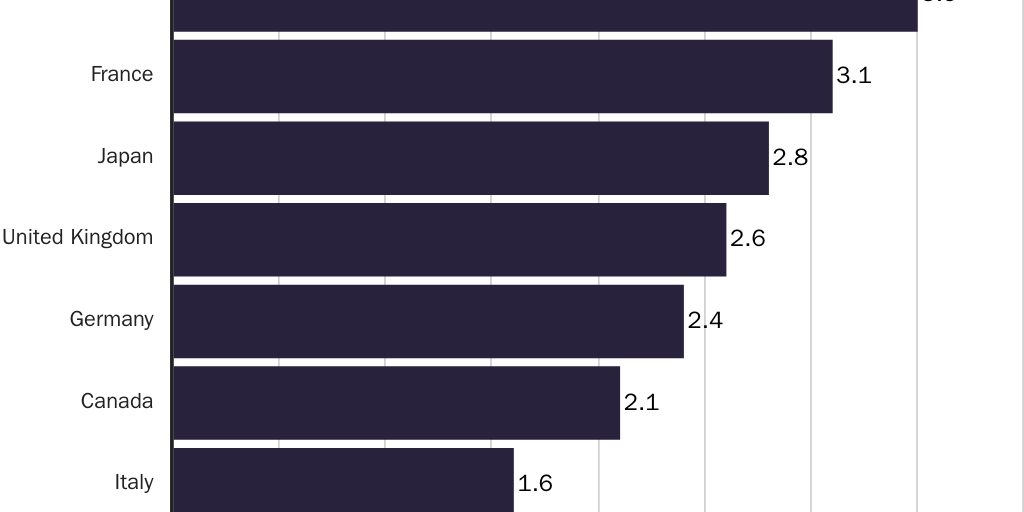

Manufacturing jobs cannot justify a new industrial policy push. It is highly questionable to assume that the significant decline in the number of factory jobs during the 1990s and 2000s could have been reversed via industrial policy because those same trends were happening in all industrialized nations, including those with robust industrial policies. American policy could, in theory, produce a one-time increase in overall manufacturing employment, but the long-term downward trend would continue. Furthermore, as shown in Table 1 and Figure 13, U.S. manufacturing workers continue to be among the most productive in the world, even accounting for a slowdown since the Great Recession.

However, altering the composition of the 165-million-person American workforce to include an additional one or two million manufacturing jobs would not necessarily be better for the workforce or for the U.S. economy overall, because manufacturing jobs are not sufficiently special or economically beneficial as to warrant government industrial policy interventions, even assuming that such interventions would be successful.

As the Cato Institute’s Ryan Bourne documented in 2019, manufacturing jobs are not significantly more stable or secure than jobs in other sectors, especially for low-skilled workers whose jobs have been disappearing for decades and who are most exposed to, and replaced by, automation and trade.123 As shown in Figure 14, annual job creation in manufacturing has been low since the 1960s, and there was net job destruction from the 1960s through 2010.

Although the number of manufacturing jobs has increased since the Great Recession, the Bureau of Labor Statistics projects that the sector will resume its long-term trend of shedding manufacturing jobs (444,800 of them, to be exact) over the next decade due to international competition and productivity-enhancing technologies.124 On the latter issue, for example, the number of man-hours required to produce a ton of steel in the United States dropped from 10 in 1980 to approximately 1.5 today. The newest steel plants, however, need even fewer workers—one Austrian mill needs only 14 employees to make 500,000 tons of steel wire per year.125 Because demand for steel is finite, steel industry employment will thus continue to decline while productivity continues to climb.