Summary

This essay is a part of the Pandemics and Policy series.

Policymakers should

-

resist using trade restrictions or subsidies to re‐shore global supply chains in case of a public health emergency or to reduce American “dependence” on foreign countries for essential medical goods;

-

acknowledge that the nation’s overall productive capacity and its medical goods industries are generally healthy and that domestic industries and their supply chains have adapted during the pandemic to meet extraordinary demand;

-

understand that past government attempts to re‐shore “essential” supply chains have proven costly and unsuccessful;

-

recognize that global integration and economic openness, by contrast, can bolster U.S. resiliency by increasing economic growth, mitigating the impact of domestic shocks, and maximizing flexibility; and

-

adopt market‐oriented policies that would generally benefit the U.S. economy while also supporting the industrial base and national resiliency, such as liberalizing unilateral trade and investment; entering new trade and investment agreements with U.S. allies, particularly those that specialize in medical goods; eliminating nationalist restrictions on government stockpiles and opposing any new ones; expanding high‐skilled immigration; and eliminating “never needed” regulations that were suspended during the pandemic to boost domestic production, investment, and adjustment.

President Biden has proposed that the U.S. government “take steps in the aftermath of the [COVID-19] crisis to produce American-sourced and manufactured pharmaceutical and medical supply products in order to reduce our dependence on foreign sources that are unreliable in times of crisis,” adding that his “goal is to develop the next generation of biomedical research and manufacturing excellence, bring back U.S. manufacturing of medical products we depend on, and ensure we are not vulnerable to supply chain disruptions, whether from another pandemic, or because of political or trade disputes.” This view, according to the Biden administration, undergirded the president’s January 25, 2021, “Buy American” executive order further restricting U.S. government purchases to “American-made” goods. It also mirrors the views of the previous administration and others who claim that the pandemic revealed serious weaknesses in essential supply chains that justify protectionism and industrial policy (i.e., targeted and directed government efforts to plan for specific future industrial outputs and outcomes), often on “national security” grounds.

As Daniel Ikenson and Simon Lester acknowledge in a separate Pandemics and Policy piece, “international trade and cross‐border investment produce some degree of reliance and risk,” including with respect to pandemics and essential goods. However, the current COVID-19-related push to achieve supply chain “resiliency” through economic nationalism suffers from several flaws. In particular, it ignores that the U.S. manufacturing sector—including with respect to most medical goods—was relatively healthy and expanding before COVID-19 and that domestic companies and global supply chains quickly adapted in response to emergency demand; that most federal government attempts to re-shore supply chains on economic security grounds have proven costly and unsuccessful; and that global integration and economic openness can bolster U.S. resiliency by increasing economic growth, mitigating the impact of domestic shocks, and maximizing flexibility in times of severe economic uncertainty. These realities argue for a different approach to achieving real resiliency—an approach based on the open and flexible policies that America does best.

The Reality of American Manufacturing and Pandemic Resilience

Contrary to conventional wisdom, there is little evidence of systemic weaknesses in the United States’ “industrial capabilities” (i.e., the ability to produce the goods that the country needs in times of war or other national emergency)—the metric that, along with access to similar capabilities abroad, the Department of Defense considers critical for national security.

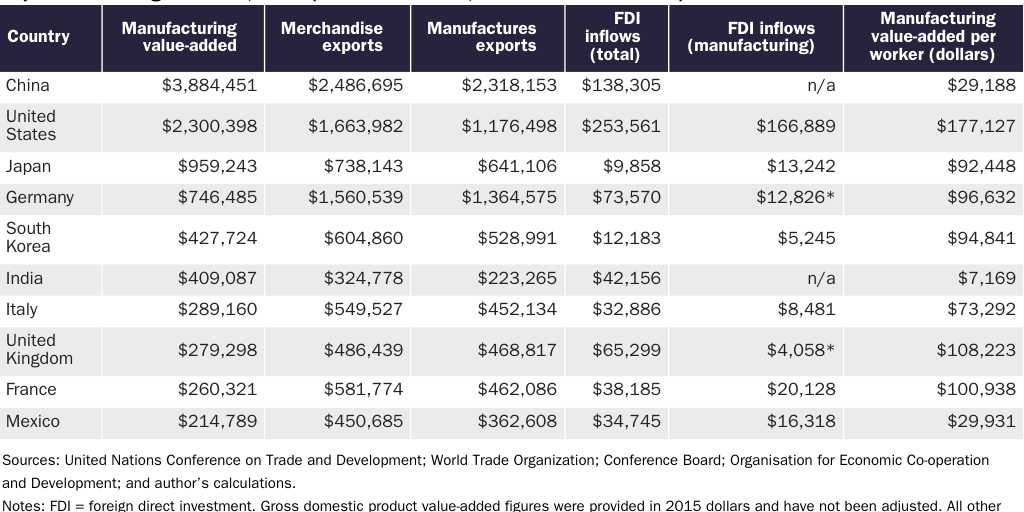

In fact, the U.S. manufacturing sector remains among the most productive in the world and is a global leader (see Table 1).

The sector’s health is perhaps most evident in its relative ability to attract investment. In 2018, for example, foreign direct investment (FDI) inflows into the U.S. manufacturing sector alone (almost $167 billion) were larger than total FDI inflows into China for the same year ($138 billion). The total value of foreign investor equity (FDI stocks) in the U.S. manufacturing sector reached $1.77 trillion that same year.

Manufacturing also performs well on a historical basis, continuing earlier trends of expansion. As I explained in a paper on the U.S. manufacturing sector overall, real (inflation-adjusted) value-added and gross output were up significantly between 1997 and 2018, while investment—capital expenditures, research and development (R&D), and FDI—also has been consistent and historically strong. Finally, the sector has experienced improved financial performance since 2001 (the first year of data available), with real gains in revenues, post-tax income, and assets.

These topline data also mask that U.S. durable goods production (real gross output and real value-added) has increased even more significantly—by 35.9 percent and 109 percent, respectively—since 1997. (Contrary to some popular claims, moreover, these gains are not solely attributable to changes in computing power; they are substantial even when removing the entire computers and electronics industry.) By contrast, small declines in nondurable goods production have been driven by basic, low-margin consumables such as textiles and apparel, tobacco, or “dematerialized” goods like paper—not other nondurables like chemicals (including pharmaceuticals) and energy that might have a legitimate national security nexus. Remove the decliners, and nondurable goods’ real value-added and gross output increased by 22.9 percent and 10.3 percent, respectively, between 1997 and 2018.

Second, the manufacturing industries most closely associated with pandemic resiliency have generally prospered in recent years. For example, a 2020 St. Louis Federal Reserve study of “essential medical equipment” (hand sanitizer, masks, personal protective equipment, ventilators, etc.) found that American producers supplied the vast majority (more than 70 percent) of these products in 2018. The World Trade Organization (WTO) further notes that the United States is not just a top global producer and importer of medical goods but also a top exporter (second overall, right behind Germany).

Featured Video

Government data on domestic production of medical equipment and supplies also show a healthy industry with expanding real output and value-added between 1997 and 2018. This includes the broader “medical equipment and supplies manufacturing” industry, which had $102 billion in gross output and $62 billion in value-added in 2018, and the two most important sub-categories, “surgical and medical instrument manufacturing” ($45.9 billion) and “surgical appliance and supplies manufacturing” ($37.4 billion). Indeed, real output in the latter category—which contains ventilators, masks, and many other medical goods—increased by almost 90 percent over the period examined. Other categories, such as “analytical laboratory instrument manufacturing” (121.8 percent), “irradiation apparatus manufacturing” (468 percent), and “electromedical and electrotherapeutic apparatus manufacturing” (418.1 percent) also experienced substantial gains in real output.

The only domestic medical goods industry that has contracted in recent years is basic personal protective equipment, or PPE (i.e., textiles, apparel, paper products, and rubber gloves), but even there, the concern is overblown. For example, the domestic textile industry in 2018 generated approximately $54 billion and $17.6 billion in real gross output and value-added, respectively, and has seen significant increases (4.7 percent and 5.4 percent) since the end of the Great Recession. Also, the apparel industry produced $9.6 billion in output in 2018.

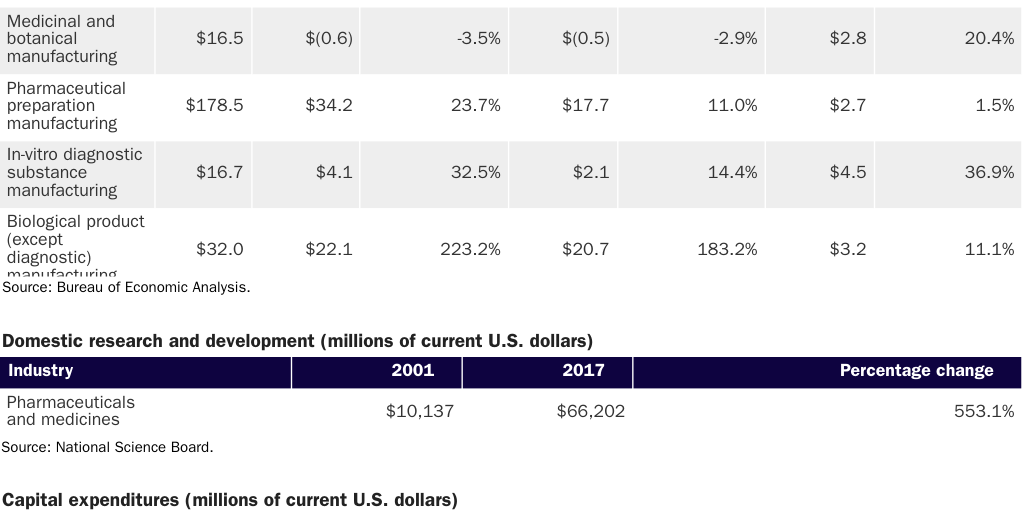

With respect to pharmaceuticals, government data on output, R&D, and capital expenditures show that American manufacturers have performed well in recent years (see Table 2).

A 2020 McKinsey report notes that the United States is home to more than 500 pharmaceutical manufacturing facilities—among the highest concentrations in the world. The WTO adds that the United States is both a major importer and exporter of pharmaceutical products, having shipped almost $41 billion in medicines (35 percent of total U.S. medical goods exports) in 2019.

Available public data on domestic and global production of pharmaceutical inputs (i.e., active pharmaceutical ingredients, or API) do not indicate a need for urgent government funding, such as that offered to Eastman Kodak Company. According to the Food and Drug Administration (FDA), of the roughly 2,000 global API manufacturing facilities, 13 percent are in China; 28 percent are in the United States; 26 percent are in the European Union; and 18 percent are in India. For the APIs on the World Health Organization’s “essential medicines” list for the U.S. market, 21 percent of manufacturing facilities are in the United States; 15 percent are in China; and the rest are in the EU, India, and Canada. The FDA further notes that the United States was home to 510 API facilities in 2019, 221 of which supply the aforementioned “essential medicines.” The development and production of the BioNTech/Pfizer and Moderna COVID-19 vaccines underscore the United States’ pharmaceutical capacity (and the need for international cooperation).

Third, there is substantial evidence that domestic producers and supply chains have thus far weathered the pandemic as well as could be expected, given 2020’s massive and unforeseen shocks to global medical goods supply and demand. In particular, an extensive December 2020 analysis of “U.S. industries producing COVID-19 related goods and the supply chain challenges and constraints that impacted the availability of such goods” from the nonpartisan U.S. International Trade Commission (USITC) drew the following conclusions:

-

The United States is a large global producer of pharmaceuticals, medical devices, soap and cleaning products, and N95 masks. Prior to the pandemic, the U.S. market for these goods was primarily satisfied by domestic manufacturers, with imports supplementing that production.

-

The United States was a smaller producer of low-value PPE products—surgical masks, medical gowns, and rubber gloves—that are primarily produced in developing countries with low labor costs or abundant supply of raw materials (especially in the case of rubber gloves).

-

Pharmaceutical and medical device production and supply chains proved resilient during the pandemic, and supply concerns remained limited throughout 2020. With respect to pharmaceuticals in particular, the USITC’s conclusions echoed a previous analysis showing China and India to be major suppliers of certain drug products but little evidence of U.S. “dependency.”

-

The most significant factor affecting the availability of other COVID-19-related goods was the unprecedented demand for such items in the United States and abroad. In response, U.S. producers significantly increased production but in most cases could still not keep up with demand. For example, U.S. N95 mask producers supplied 80 percent of the domestic market in 2019 (30 million units per month, with medical professionals needing only about 10 percent—or 3 million—of those) and increased production six-fold by the end of 2020 in response to the pandemic. However, domestic demand for N95 masks increased by as much as ten-fold during the summer of 2020, easily outpacing the U.S. expansions.

-

Imports of medical goods, especially PPE, helped fill the gap between domestic supply and demand, which in many cases exceeded historical volumes by several orders of magnitude. Import sources were widely varied overall, with China the dominant import source for only surgical masks and medical gowns. Although some shortages did exist in the first half of 2020, they were mostly alleviated in subsequent months (though PPE supply remains tight). Only rubber gloves continued to be a concern going into 2021, mainly due to the limited availability of natural rubber (sourced primarily from Malaysia) and artificial alternatives.

-

Beyond demand, the most common concerns raised by U.S. producers and importers were regulatory barriers (especially for surgical masks, medical gowns, and hand sanitizer), tariffs on finished goods and manufacturing inputs, and uncertainty regarding future demand once the pandemic ends.

Overall, the report shows a large and diverse U.S. medical goods market in which both domestic production and imports vary according to comparative advantages and work in tandem to satisfy consumer demand—demand that skyrocketed in response to a once-in-a-generation pandemic and was met (albeit imperfectly) by both imports and increased domestic production, most of which came without government support. In short, the system was stressed but ended up working pretty well.

Anecdotal evidence supports the USITC’s findings. Many U.S. companies shifted operations to produce high-demand PPE during the pandemic—an example of the U.S. manufacturing sector’s pre-existing industrial capacity and flexibility. Others were drawn into the market by sky-high demand: online crafts retailer Etsy, for example, sold more than $600 million in facemasks during the second and third quarters of 2020 (12 million units in April alone), and “more than 110,000 sellers sold at least one mask between April and June.” Although short-term gaps in U.S. PPE supply inevitably emerged during the pandemic (due to astronomical demand, pre-pandemic stockpiling mistakes, or other issues), they were filled in by foreign producers and the stockpiles. As of late summer 2020, for example, National Institute for Occupational Safety and Health–approved N95 masks were readily available (for individual or bulk purchase) on websites like Amazon. Several members of Congress even went so far as to write to President Biden complaining about a potential glut of U.S.-made PPE, because the “industry retooled production chains in the spring to respond to the crisis,” and as a result, “domestic production capabilities for essential products like isolation gowns, N95 masks, testing swabs and other critical products have grown exponentially.”

Related Read

Manufactured Crisis: “Deindustrialization,” Free Markets, and National Security

Expansive new security nationalism proposals warrant extreme skepticism, and market‐oriented policies should be prioritized.

Widescale repatriation and “self‐sufficiency” policies, by contrast, defy basic economic sense and would produce significant distortions. Most notably, there is the problem of maintaining pandemic‐level capacity in non‐pandemic times. The USITC calculated that in 2020, the United States used many times the number of N95 masks, medical gowns, surgical masks, and other essential goods that were used in 2019. Maintaining that much excess capacity in times of normal demand is extremely costly (for many industries, profitability kicks in at around 80 percent capacity utilization), and running at that level in non-pandemic times would produce a global glut—ironically, similar to the ones the U.S. government complains about when China subsidizes “global excess capacity” and certain to cause new trade tensions. Indeed, we could already have a glut of American-made PPE, and foreign governments are already speaking out about other nations’ pandemic-era subsidies.

Compounding this issue is policymakers’ inability to know which products to target both during and after the pandemic. Ventilators, for example, were on no one’s radar before COVID-19 hit. In March 2020, when they were suddenly considered essential for fighting the coronavirus, the U.S. government invoked the Defense Production Act (DPA) to force domestic manufacturers to make them. By the summer, however, medical professionals determined that ventilators were not as critical as once thought, but producers continued to churn them out under government orders, leading to reports of the goods “piling up” in a strategic reserve or being donated to “countries that don’t need or can’t use them.” According to the USITC’s December 2020 report, other DPA-funded medical goods production will only come online after mid-2021, when the pandemic may have subsided.

Given these interventions, as well as the numerous U.S. companies that independently expanded operations or entered the medical goods market in response to the pandemic, it is an open question as to whether additional government action is needed to boost domestic production of essential medical goods. Indeed, companies such as Mark Cuban’s new generic drug company, are in the process of adding domestic capacity without government subsidies. By the time U.S. policymakers decide to intervene in the U.S. market, it will look much different than the one on which they based their decision and will likely change again by the time any government-supported production comes online.

Finally, there is a serious risk that future government interventions will have political, rather than economic, motivations—similar to the ones that reportedly drove the Trump administration’s doomed subsidies to Eastman Kodak. According to a July 2020 Congressional Research Service report, for example, the Department of Defense invoked the DPA to give hundreds of millions of dollars, appropriated under the Coronavirus Aid, Relief, and Economic Security Act to fight COVID-19, to politically connected industries (shipbuilding, semiconductors, space-based defense, aviation, microelectronics, rare earth mining, etc.) that are at best tangentially related to the pandemic. The report adds that these and other COVID-19 actions lacked transparency and accountability, led to the reassignment of one official, and were opposed by several House committees because they were not, as Congress intended, “reserved for health and medical countermeasures.”

Supply Chain Nationalism Makes the United States Less Resilient

Protectionism often undermines resiliency by weakening a country’s economy and manufacturing sector—a conclusion supported by decades of research. For example, International Monetary Fund economists in 2018 examined data for 151 countries over 51 years (1963–2014) and found that “tariff increases lead, in the medium term, to economically and statistically significant declines in domestic output and productivity” as well as more unemployment and higher inequality. These harms were amplified for the U.S. manufacturing sector: increased tariffs on manufacturing inputs (e.g., steel) resulted in a statistically significant decline in manufacturing sector-wide output (6.4 percent) and productivity (3.9 percent) five years after the tariff hikes in question. Economists have come to similar conclusions in the context of COVID-19: a November 2020 analysis, for example, found that the economic costs of “localizing” global supply chains for medical goods would lower economic activity and incomes yet also prove unable to insulate countries from a pandemic-induced economic shock.

The United States’ implementation of nationalist policies on security grounds—for steel, ships, machine tools, semiconductors, and other “essential” goods—also reveals a long track record of high costs, high risks, failed objectives, and unintended consequences. In case after case, the protected industries did not emerge stronger or more resilient—in fact, just the opposite. This checkered history must be considered when evaluating new proposals to support certain industries on national security grounds.

By contrast, extensive literature ties trade openness to improved economic performance more broadly. A 2018 paper from Robert Feenstra summarized the studies on the long-run, overall gains from trade for the United States, calculating total average gross domestic product (GDP) gains of 1.1 percent per year due to increased product variety arising from imports, the productivity-enhancing effects of trade-induced creative destruction, and pro-competitive effects on domestic prices. Other studies have shown similar benefits for the U.S. economy.

Overall, the evidence and analysis refute current arguments that economic nationalism would bolster the U.S. industrial base (and thus national resiliency). Instead, American protectionism has been repeatedly found to weaken the U.S. manufacturing sector and the economy more broadly.

Free Markets Enhance U.S. Resilience

There is little to indicate that trade and investment openness has made the United States less economically resilient and thereby increased national security risk. In fact, openness in many cases can decrease a country’s vulnerability to demand or supply shocks, or it can help the economy recover.

Featured Video

This conclusion makes intuitive sense—greater trade and investment openness might make an economy more vulnerable to external supply or demand shocks, but it also helps reduce a nation’s vulnerability to (and improve its recovery from) domestic shocks—and is borne out in academic research. In fact, an August 2020 assessment of the pandemic’s initial impact on supply chains and national economic performance found that “renationalization” of supply chains would generally not improve a country’s overall economic performance, or the performance of specific sectors (including manufacturing industries such as textiles, chemicals and pharmaceuticals, and electrical equipment), after a global pandemic. A subsequent analysis came to similar conclusions, finding that manufacturers who used imported inputs fared worse when their supplier markets were hit by COVID-19 but fared better when their own home market was hit.

Finally, domestic policy likely outweighs trade openness in terms of mitigating the risk of economic shocks. For example, two of the most “trade-dependent” countries—Germany and South Korea—experienced COVID-19-induced quarterly GDP contractions in the first half of 2020 that were similar to or better than the relatively “closed” Japan or United States, while other “open” economies performed less favorably over the same period. Germany’s initial “V‑shaped” recovery is particularly noteworthy, given the country’s level of economic development and high dependence on trade. Cato’s Ryan Bourne adds that certain foreign suppliers rebounded quickly from COVID-19, but “it was the lack of demand from importing countries that took longer to contain the virus, such as the United States and the UK, which prolonged a depression of activity in those industries.” These situations indicate that domestic policies, in particular countries’ ability to control the virus or keep their economies open, drove their economic performance more than trade or investment liberalization. Subsequent research supports these conclusions.

Market-Oriented Reforms Can Further Support Manufacturing and Resiliency

While the “death” of the U.S. manufacturing sector and our economic “vulnerability” and dependency have been greatly exaggerated, several market-oriented policy reforms would support national resiliency by strengthening the U.S. economy generally and boosting the manufacturing sector’s performance in particular:

-

Unilateral liberalization of tariffs on industrial inputs and medical goods. President Trump’s tariffs have harmed the U.S. manufacturing sector, increased uncertainty, and antagonized allies while providing little long-term benefit to the protected domestic industries at issue. At the same time, imports of PPE and pharmaceuticals have proven vital in fighting COVID-19. Eliminating import restrictions would thus provide an immediate boost to the U.S. manufacturing sector and additional relief during and after the pandemic. Longer term, Congress should reform or eliminate the U.S. laws that provide the president with vast discretion to impose tariffs on “national security” or other grounds without any congressional input or oversight.

-

New trade and investment agreements with U.S. allies. The U.S. government should liberalize trade and investment with allies by expanding the National Technology and Industrial Base (NTIB) to include allies (and innovative manufacturing nations) such as Finland, Germany, Japan, the Netherlands, South Korea, Singapore, Switzerland, or Sweden. The government also should fully implement the NTIB and further liberalize trade, investment, and R&D collaboration among all NTIB members, for example by eliminating U.S. procurement restrictions (e.g., Buy American; the Berry Amendment; and the Byrnes-Tollefson Amendment). Over the longer term, the United States should consider new comprehensive free trade agreements with these and other countries.

-

Eliminating Buy American restrictions. As Cato scholars have argued for decades, Buy American procurement requirements are bad law, bad economics, bad trade policy, and bad politics—and can especially harm U.S. manufacturers. The federal government should eliminate these restrictions, particularly for the procurement of essential goods and services. For example, the government should terminate the Stock Piling Act’s “Buy American” rules for “strategic and critical materials” and should block attempts to implement similar rules for the Strategic National Stockpile (which covers medical goods).

-

Improving human capital. In order to address immediate concerns regarding the dearth of qualified U.S. manufacturing workers in science, technology, engineering, and mathematics fields, the federal government should significantly expand high-skilled immigration—restrictions on which have been shown to encourage multinational corporations to offshore jobs and R&D activities to their affiliates in more welcoming countries and to benefit potential U.S. adversaries, especially China, in terms of new jobs, new businesses, and new innovations. Over the longer term, private-sector training and apprenticeship programs, such as the employer-funded Federation for Advanced Manufacturing Education program, can equip native workers for the future needs of advanced manufacturing industries and supplement federal, state, and local government educational policies.

-

Eliminating “never needed” regulations. During the COVID-19 pandemic, state and federal governments temporarily suspended hundreds of regulations to boost domestic production, investment, and adjustment during the national emergency, revealing in the process that these “never needed” regulations discouraged economic growth and dynamism while providing little, if any, public benefit. Although many of these regulations affect nonmanufacturing issues and industries (e.g., physician licensing), many others—such as FDA testing and approval of medical goods—directly inhibit the domestic production of certain essential goods. The USITC cited these and other U.S. regulations as a major impediment to boosting domestic medical goods production during the pandemic. Other regulations, such as biofuels mandates, increase production costs for U.S. manufacturers. Repeal of these regulations would therefore boost not only economic growth generally but also American manufacturers directly—all to the benefit of economic resiliency.

Additional government action—for example, government stockpiles or private inventory mandates—need not be considered unless and until these and other market-oriented policies prove insufficient to satisfy legitimate security concerns. It is difficult to conceive, however, of scenarios in which new and expansive industrial policy programs would be warranted.

Conclusion

Economic openness and global interdependence undoubtedly risk the importation of economic shocks—including pandemics—into the United States that roil supply chains for essential goods and cause serious disruptions to our daily lives. However, both theory and practice show that this same openness can promote global stability and improve the nation’s resilience in times of national emergency and that nationalist policies present a far greater risk to our ability to withstand and respond to economic shocks—even when such policies are implemented on security, rather than purely economic, grounds.

The COVID-19 vaccine produced by Germany’s BioNTech and U.S. multinational pharmaceutical giant Pfizer provides a timely lesson in this regard. Immigrants founded and run both companies and are heavily represented on their vaccine research teams in both Germany and the United States. Each company relies on global capital markets to fund most business operations, and Pfizer famously passed on government funding for the coronavirus vaccine R&D, choosing instead to foot the $2 billion bill (and assume related risks) itself. The vaccine’s development, meanwhile, relied on “messenger RNA” technology first developed by Hungarian and American researchers, as well as initial COVID-19 gene mapping by Chinese and Australian scientists.

The German and American drug companies partnered in March 2020 (having previously collaborated on a flu vaccine), and Pfizer assigned production to its existing pharmaceutical manufacturing, supply, and distribution facilities in Belgium and the United States (in Missouri, Massachusetts, and Michigan), using raw materials from, among other places, Canada and a British-owned facility in Alabama. To deliver the vaccine, Pfizer piggybacked off its previous experience and capacity related to global refrigerated distribution, setting up cold storage systems in the United States and Germany. Pfizer also partnered with cargo companies (FedEx, UPS, and DHL) and United Airlines to deliver doses around the world using a global logistics and transportation infrastructure (warehouses, planes, computer systems, workers, etc.) that developed over decades. Some of the first doses injected into American arms were flown from Belgium.

BioNTech and Pfizer were able to go from concept to final delivery of millions of vaccine doses in only a matter of months—just as their management boldly predicted in April, more than a month before Operation Warp Speed was officially announced. This miraculous effort resulted not from the plan of any single person or government but by international teams of companies and individuals, complex global supply chains, and long-standing policies facilitating the organic, cross-border flow of labor, goods, services, and knowledge. Surely, some state funding (e.g., grants for basic research and vaccine purchase commitments) was involved, but attempts to “nationalize” and micromanage the vaccine’s development and delivery would have delayed—if not thwarted—those processes, costing numerous lives along the way.

If the goal is, as President Biden claims, to “develop the next generation of biomedical research and manufacturing excellence,” then we’ve already succeeded.

About the Author

This work is licensed under a Creative Commons Attribution-NonCommercial-ShareAlike 4.0 International License.