Congratulations to the wave of Republicans who successfully ran on promises to tackle rising government debt and cut the hugely bloated federal budget. On the campaign trail, most candidates were not very specific about how they would cut the budget, but when they come to Washington they will be looking for good reform targets.

Newcomers to Congress can find a wealth of budget-cutting ideas in recent plans by various D.C. think tanks:

- At the Heritage Foundation, Brian Riedl has come up with $343 billion in proposed annual cuts.

- At the Committee for a Responsible Federal Budget, Bill Galston and Maya MacGuineas have proposed $400 billion in annual cuts.

- Esquire magazine assembled four former senators who came up with $476 billion in annual cuts.

- The National Taxpayers Union teamed up with the U.S. Public Interest Research Group to propose $600 billion of cuts over five years.

- Michael Ettlinger and Michael Linden of the Center for American Progress offer one plan that would cut annual spending by $255 billion.

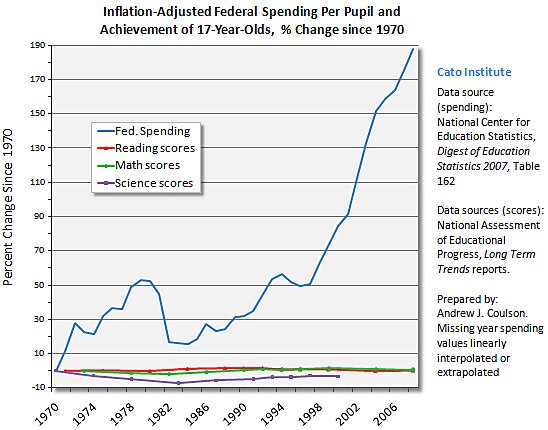

Cato’s website, www.downsizinggovernment.org, also provides a treasure trove of spending cuts, and I will be publishing a detailed budget-reform plan in coming days.

Some of the above budget plans include tax increases, but voters gave a resounding message yesterday that they want Congress to focus on cutting spending, not raising taxes.

Out of the starting gate next year, fiscal reformers in Congress should push for an across-the-board cut to discretionary spending for the rest of the current fiscal year. One approach would be for House leaders to propose a continuing resolution that extends spending at last year’s levels, less some substantial percentage cut applied to every program.

For the upcoming fiscal year of 2012, reformers need to carefully target some major program cuts and eliminations. The president and the Democrats in the Senate will likely resist proposed cuts, but the point is to further the national debate that has begun about the proper size and scope of the federal government.

Some initial targets for GOP reformers, with rough annual savings, could include: community development subsidies ($15 billion), public housing subsidies ($9 billion), urban transit subsidies ($9 billion), and foreign development aid ($18 billion). On the entitlement side, initial cuts could include raising the retirement age for Social Security and introducing progressive price indexing to reduce the growth rate of future benefits.

We will not get federal spending under control unless we begin a national discussion about specific cuts. And we won’t get that discussion unless enough members of Congress start pushing for specific cuts. Ronald Reagan was able to make substantial cuts to state grants in the early 1980s because policymakers had discussed such reforms throughout the 1970s. Republicans in the mid-1990s were able to reform welfare because of the extended debate on the issue that preceded it.

The electorate wants spending cuts, and they will support the policymakers who take the lead on cuts if they are pursued in a forthright and serious-minded manner.