Federal spending is rising and the government’s debt is growing by a trillion dollars a year. President Trump came into office promising spending cuts and debt reduction, but he has delivered the opposite so far.

How fast has Trump raised spending compared to past presidents? Spending for Trump’s third year (fiscal 2020) was roughly set in the August budget deal with Congress, so we can look at the president’s spending over his first three years.

Presidents share budget power with Congress. They can either sign or veto spending bills, which gives them a lot of leverage. Presidents can dig in their heels against congressional profligacy, or they can go with the flow and let political pressures push spending ever higher.

The following charts show annual average real (inflation-adjusted) spending growth under presidents back to Eisenhower. The data comes from Table 6.1 here, except I updated 2020 based on August CBO. See further notes at the bottom.

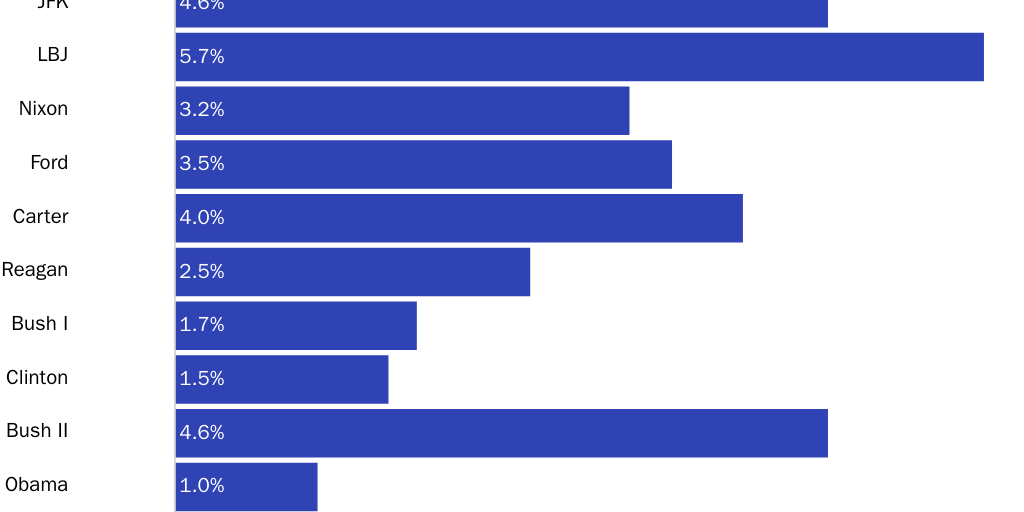

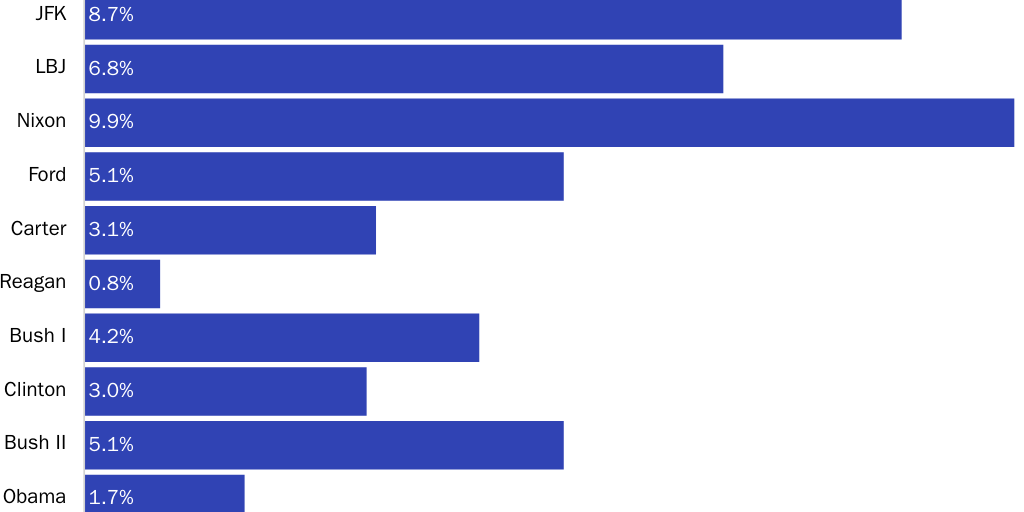

Figure 1 shows total federal outlays. Ike is negative because defense spending fell at the end of the Korean War. Obama is the most frugal president since Ike based on this metric.

LBJ is the big-spending champ, followed by George W. Bush. Both Texans pushed for large increases on both guns and butter. Trump also presides over increases in defense and nondefense spending.

By contrast, real defense spending fell under both Bush I and Clinton, which helped reduce their growth rates in Figure 1.

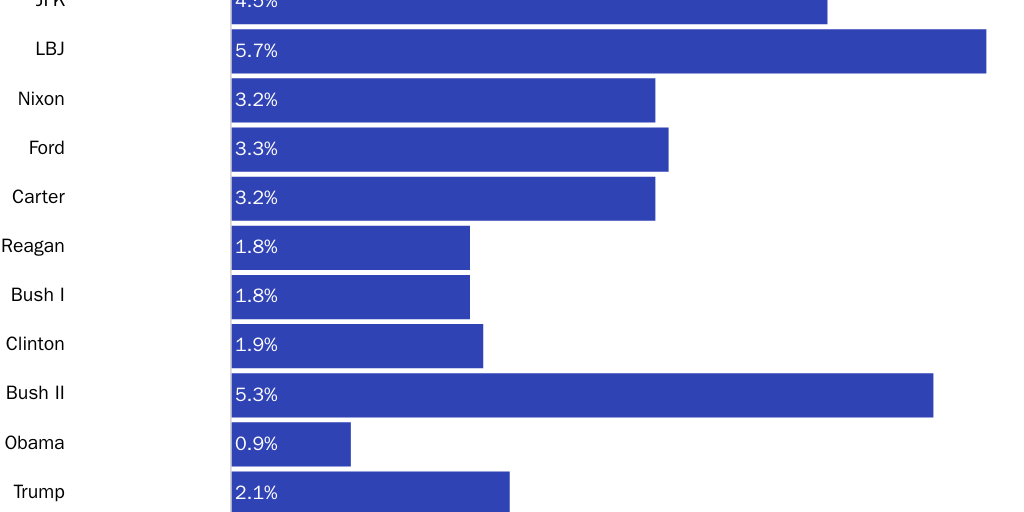

Figure 2 shows total outlays less interest. Carter, Reagan, and Trump perform better on this metric than the first one because they faced rising interest costs during their tenures.

Figure 3 shows total outlays less interest and less defense. Thus, it includes spending on nondefense discretionary and entitlement programs. Prior to Carter, the White House was a horror show of big spenders from both parties.

Figure 3 also shows that for frugality in nondefense spending, Reagan stands alone.

I measured spending growth by calculating the compound annual rate between the first and last years of a president’s term. For example, Bush II was 2001 to 2009. Trump was 2017 to 2020, with the latter year based on the current CBO baseline estimate.

I made two adjustments to the budget data, both for 2009. First, the official data includes an outlay of $151 billion for TARP in 2009. But TARP ended up costing taxpayers nothing, and official budget data reverses out the spending in later years. So I’ve subtracted $151 billion from the 2009 amount.

Second, 2009 is the last budget year for Bush II, but that year was extraordinary because Obama signed into law the giant stimulus bill, which included $114 billion in outlays for 2009. It is not fair to count that spending for Bush II, so I’ve subtracted it out.

Note also that spending in the stimulus bill was mainly temporary and had petered out by Obama’s last year in office. Obama thus added a trillion dollars or so to federal debt that is not reflected in my measure here, which uses the spending total in the last year to measure the growth.

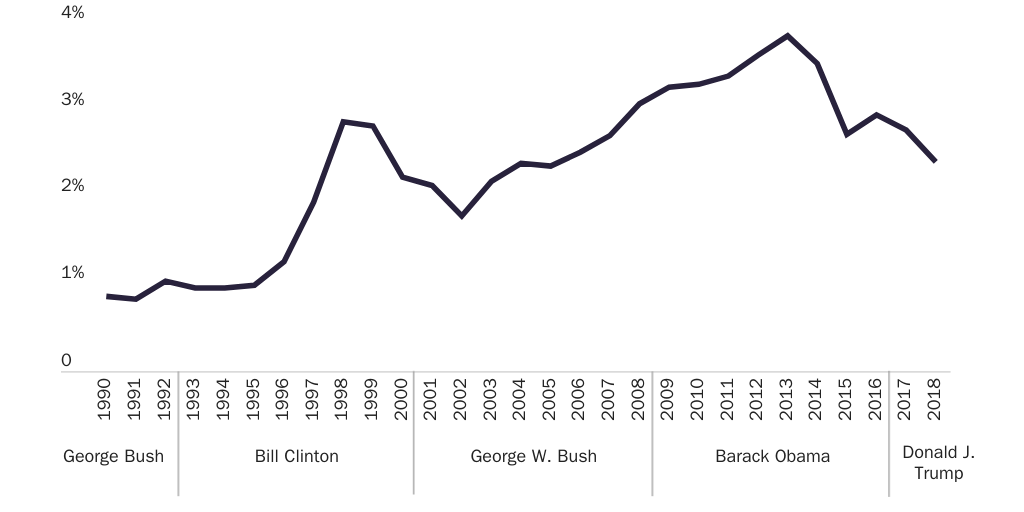

Finally, while spending growth rates are generally down from the pre-Reagan decades, economic growth is slower these days. As a result, the government’s share of the economy has crept upward since Clinton left office, and CBO projects that the share will continue to rise in coming years.