The interest on a typical 30-year mortgage costs $500 more per month than it did in 2019. Credit card rates have climbed to record highs. From auto loans to business financing, borrowing costs have surged across the board since the pandemic. Understandably, many Americans are frustrated by rising borrowing costs and sticker shock, even as wage gains have outpaced inflation since early 2023. Today, affordability, inflation, and deficits consistently rank among the top priorities for voters. If politicians want to make life more affordable and bring down interest rates, they should focus on reducing spending and government intervention, not increasing it.

Federal Borrowing Raises Interest Costs for Consumers and Business Owners

When the federal government runs a deficit, it must borrow to cover the gap between spending and tax revenue. This deficit spending and the borrowing needed to finance it impact the overall economy.

In the short run, federal deficit spending increases aggregate demand. In a supply-constrained environment, like the pandemic, this spike in demand can contribute significantly to inflation. Simultaneously, federal borrowing competes for available private capital. This “crowding out” effect means less money is directed to productive private enterprises, and more is directed to Treasury bonds, resulting in slower economic growth.

Taken together, higher deficits and debt can alter consumers’ and businesses’ expectations about inflation and interest rates. Over the longer run, bondholders tend to demand a greater return on investment—called term premia—to compensate for volatility and inflationary pressures. That means higher interest rates on government debt, which, in turn, influence interest rates for everyone else.

The pandemic offers a clear example of how large deficits combined with supply constraints can trigger a chain reaction of inflation and higher interest rates. Between 2020 and 2021, the pandemic disrupted labor markets and supply chains, and Congress approved more than $6 trillion in fiscal stimulus in a supply-constrained environment. Inflation skyrocketed after, hitting 40-year highs. The central bank then raised interest rates to tamp down inflation, while bond yields rallied to 4 percent—more than double what they were 10 years earlier.

Interest rates for many types of consumer debt have similarly risen relative to a decade ago, spiking especially after the pandemic spending surge (see the graph below). For the median American, this means spending hundreds of dollars more in annual interest costs on a typical car, home, and/or business loan. For example, a $328,000 30-year mortgage would entail a roughly $2,000 monthly interest payment at today’s rates, $500 more per month than an identically priced mortgage at 2019 or 2016 interest rates. This spike in borrowing costs is exactly what conventional economic modeling would predict following a significant increase in the federal deficit.

When banks set interest rates, they are responding to market conditions shaped significantly by government policy. In the post-pandemic environment, expansive government fiscal policy with deficits exceeding 6 percent of GDP since 2023 has put upward pressure on interest rates.

One key takeaway here should be that deficit spending can have painful economic consequences that reverberate long after the initial spending episode. Another is that many dominant “affordability” narratives and their respective policies do not address this underlying fiscal driver of today’s inflation and cost frustrations.

Many of the Populist Alternatives to Cutting Spending Are Anti-Affordability

Some politicians’ (and voters’) instincts on affordability are to increase subsidies or to pressure the Federal Reserve to lower interest rates. Pumping more capital into a supply-constrained market, such as the housing markets of San Francisco or New York, will not magically create an abundance of new housing supply. It’ll just bid up the price and shift costs to taxpayers, leaving the root of the problem unaddressed. Such is the case with health care and education, which together receive trillions of dollars in taxpayer subsidies every year. Have prices fallen for either of these sectors in aggregate? No.

In the same vein, the president or Congress compelling the Federal Reserve to lower interest rates risks fueling inflation. Over the pandemic, Congress authorized trillions in stimulus deficit spending. To finance this new spending, the Treasury Department issued a huge wave of new debt, which needed to be purchased by someone. At the time, the Federal Reserve faced a choice:

- Do nothing and watch as yields—the rate of return investors earn on debt—naturally rise as bondholders demand greater compensation to purchase this wave of new debt. Or…

- Accommodate fiscal profligacy by purchasing securities itself, soaking up some of the new supply that Congress created.

The Federal Reserve chose option B, pursuing a more accommodative monetary policy as they sometimes have in the past, rather than letting markets sort out the underlying risk and price of US debt.

What followed was a bout of record-breaking inflation not seen since the 80s. Incumbent Democrats lost elections following this inflation episode, driven out in part by anger over high sticker prices. Incumbent Republicans would be wise, both for the health of the economy and for their self-interested political survival, to pursue sound monetary and fiscal policy and avoid repeating such a mistake.

Yet last week, the Department of Justice served the Federal Reserve with subpoenas and threatened a criminal indictment over the Fed’s building renovations. It’s difficult not to view this in the broader context of the president’s prior demands to lower interest rates.

At the same time, President Trump recently announced his desire to cap credit card interest rates at 10 percent, under the guise of “affordability.” Price controls do not work and have an abysmal track record. Capping credit card interest rates will reduce both the availability of credit and the quality of credit products offered to consumers. The poorest, lowest credit rating individuals are likely to be hit hardest and may be forced to turn to more risky credit alternatives, such as short-term, high-cost “fast cash” loans.

There Is No Free Lunch

Affordability will not be brought about by price controls, nor will it be brought about by further deficit spending on new subsidies. Instead, the only sustainable path to reduced costs and higher incomes for Americans is deregulation and sound monetary and fiscal policy.

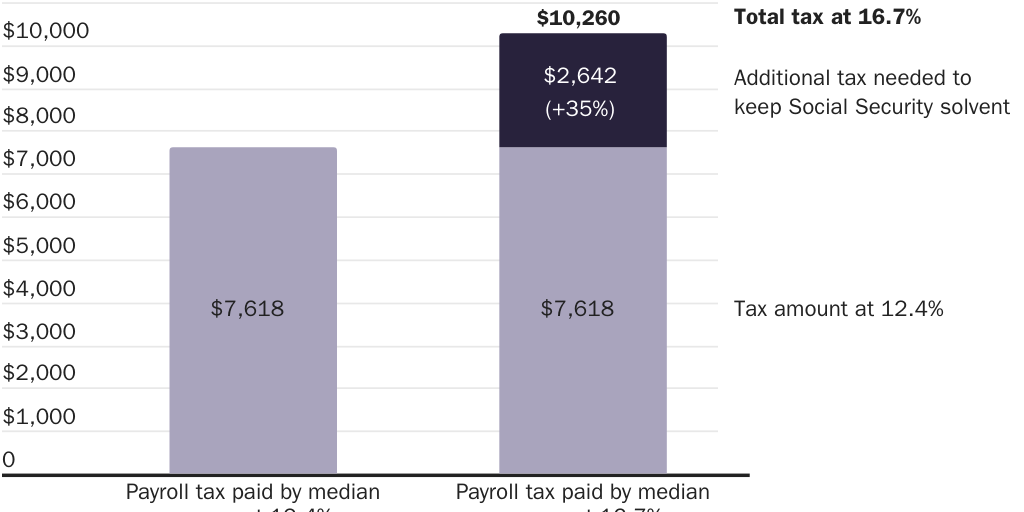

For fiscal policy, the Bipartisan Fiscal Forum’s proposed deficit target of no more than 3 percent of GDP would be a meaningful benchmark that would begin to reverse the upward pressure high debt places on interest rates. Pairing such a target with a powerful fiscal commission modeled on the Base Realignment and Closure (BRAC) process could provide Congress with the political cover and procedural framework needed to implement difficult but necessary spending reforms. At a minimum, that must include Congress reforming Social Security, Medicare, and Medicaid, which together are driving the US towards a debt crisis. Unless and until that happens, affordability will remain out of reach.