| The Daily Show With Jon Stewart | Mon — Thurs 11p / 10c | |||

| Tim Kaine | ||||

| www.thedailyshow.com | ||||

|

||||

(The health care discussion occurs between 2:00 and 3:15.)

| The Daily Show With Jon Stewart | Mon — Thurs 11p / 10c | |||

| Tim Kaine | ||||

| www.thedailyshow.com | ||||

|

||||

(The health care discussion occurs between 2:00 and 3:15.)

I was a bit critical of Laura Tyson’s New York Times article on “Why We Need a Second Stimulus.” Apparently I wasn’t nearly critical enough.

The Nation and National Public Radio are advising President Obama to “stop listening to infrastructure-phobic advisers like Larry Summers and start taking counsel from Laura Tyson, a member of his Economic Recovery Advisory Board who argues that $1 trillion in infrastructure investment is needed over the next five years.”

At The Atlantic, senior editor (and Boston Globe columnist) Joshua Green thinks Laura Tyson’s article “underscored what a loss it is for the Obama administration that it couldn’t manage to find a place for her on its economic team.” Mr. Green can’t imagine why a Berkeley professor who wants to add an extra trillion to federal spending wouldn’t be the ideal budget director.

In the article that so impressed Mr. Green, Tyson wrote, “The primary cause of the [current] labor market crisis is a collapse in private demand… By late 2009, in response to unprecedented fiscal and monetary stimulus, household and business spending began to recover. But by the second quarter of this year, economic growth had slowed to 1.6 percent.”

Combining “fiscal and monetary stimulus” in a single phrase is a clumsy way to conceal the irrelevance of “fiscal stimulus” (debt-financed federal spending) to GDP growth in 2009. Fiscal stimulus means the Treasury sells more bonds. Monetary stimulus means the Fed buys more bonds. To discuss those transactions as if they had the same effect is just another mysterious Keynesian incantation.

Tyson claims there is “too little appreciation for how stimulus spending has helped stabilize the economy and how more of the right kind of government spending could boost job creation and economic growth.” She wants much more spending on unemployment benefits (a paradoxical definition of a jobs program) and on aid to state and local governments (where unemployment rates are relatively low).

To argue for more borrowing and spending, however, Tyson cannot credit monetary policy for helping the recovery. Because she explicitly advocates much more spending on “unemployment benefits and aid to state governments” (not just “infrastructure”), Tyson has to demonstrate that changes in federal spending (not Fed policy) explain why the economy appeared to be recovering in late 2009 but faltering by the second quarter of 2010. It is not enough to allude to simulations from Mark Zandi’s famously incorrect forecasting model, as the CEA and CBO have done. Tyson needs to show us a fact or two. She didn’t even try. She even got the size of Obama’s stimulus bill wrong, citing last year’s antiquated $787 billion figure that the Congressional Budget Office (CBO) has revised twice since January.

In reality, the 2009 stimulus bill was mostly about extending unemployment benefits, expanding Medicaid, dispensing small checks (refundable tax credits) and other schemes to rob Peter and pay Paul. Such transfer payments add nothing to GDP; they just discourage work. The increase in federal nondefense purchases (such as “shovel-ready” projects) contributed only two-tenths of one percent (0.2) to the change in GDP in 2009. That was no larger than in 2008 when the Recovery Act did not exist. And even that trivial sum is merely an accounting gain rather than a net economic gain, because federal borrowing is no free lunch. The reason Keynesian accounting is no substitute for economics is that governments can only spend what Danny DeVito called “OPM” (other peoples’ money). To claim that such spending is a net addition to “aggregate demand” is to ignore those other people — namely, current and future taxpayers.

The timing of Obama’s so-called stimulus spending has been totally inconsistent with Tyson’s description of how the economy supposedly responded in the past and present, and why she expects growth to slow by a percentage point or two next year unless the feds spend more on multi-year jobless benefits and deficit-sharing with the states. In its latest whitewash, the CBO “now estimates that the total impact over the 2009–2019 period will amount to $814 billion. Close to half of that impact is estimated to occur in fiscal year 2010, and about 70 percent of ARRA’s budgetary impact will have been realized by the close of that fiscal year.” With half of the spending in fiscal 2010 and 30 percent in 2011 and beyond, that means just 20 percent of the $814 billion ($163 billion) had been spent by the end of October 2009. Yet it was in late 2009 when Tyson claims the stimulus had the most impact.

Tyson worries that “by next year, the [fiscal] stimulus will end.” That’s wrong too. The CBO estimates that 30 percent of the spending ($244 billion) will occur in fiscal 2011 (January to October) and beyond to 2019.

Unfortunately, Ms. Tyson’s reference to the second quarter’s GDP is entirely unrelated to her diagnosis of the problem as being “a collapse in private demand.” GDP does not measure private demand because it subtracts imports. Yet spending on imports is just as much a part of “demand” as is spending on domestic goods and services. Real gross domestic purchases increased at a 4.9 percent annual rate in the second quarter, up from 3.9 percent in the first. Neither figure suggests any paucity of private spending.

The second quarter surge in imports (which largely accounts for the wide gap between domestic purchases and GDP) looks like a statistical fluke. “Real” imports appeared to rise so much mainly because import prices supposedly fell at a 9.5 percent annual rate (which means a 2.38 percent rise in the quarter, multiplied by four to get the annual rate). By contrast, import prices rose at a 14.6 percent annual rate in the first quarter and at a 24.8 percent rate in the fourth quarter of 2009. Those figures say more about the folly of converting smallish price changes into annual rates than they do about the real economy. Besides, imports fell 2.1 percent in July and exports rose 1.8%, so the questionable second quarter trade figures did not indicate a lasting trend.

Tyson did not bother to figure out how large the first stimulus bill was, or when the borrowed loot was spent. She did not bother to look up the negligible contribution of federal spending to recent changes in GDP, and she confused GDP with domestic demand.

The press kept telling us that Tyson was almost certain to replace Peter Orszag as OMB director, and then to replace Christina Romer as head of the Council of Economic Advisers. Yet such plums keep slipping from her fingers, to the dismay of her fans at The Nation, NPR and The Atlantic. This is rare evidence of good judgment from the Obama White House.

As I blogged earlier, yesterday the Kaiser Family Foundation and the Health Research & Educational Trust released their survey of employer-sponsored health benefits in 2010.

For most of this survey’s history, it included a very useful graph of the average growth rate of employer-sponsored insurance premiums. Here’s the graph from their 2007 survey:

(The grey and light-green lines represent year-to-year growth in overall inflation and wages, respectively.)

Unfortunately, 2007 was the last year that KFF/HRET included that graph in their annual survey. Had they included that graph this year, it would have shown an even more heartening moderation of premium growth:

A lot of things can drive premium growth. I discussed a couple of them in my last post. Some factors that could cause premium growth to moderate might not be all that welcome; if insurers dumped all their sick enrollees, for example. But absent dramatic evidence of that, isn’t this good news? And isn’t good news worth highlighting?

Every year, the Kaiser Family Foundation and the Health Research & Educational Trust produce the leading survey of employee health benefits. Yesterday, KFF and HRET issued their survey of health benefits in 2010 with a news release that begins:

Family Health Premiums Rise 3 Percent to $13,770 in 2010…

Premiums rose by just 3 percent? Great news! Last year, KFF/HRET guesstimated that the average cost of family coverage could hit $14,539 in 2010. Working families saved hundreds of dollars!

Not so fast, says KFF/HRET. The main reason premiums rose less than expected is that “businesses have been shifting more of the costs of health insurance to workers through … deductibles and other cost-sharing,” said KFF president and CEO Drew Altman. Actually, deductibles and other cost-sharing do not shift health insurance costs; they reduce the amount of insurance. What they shift is the cost of health care, from the insurance pool to individual members of the pool.

Nevertheless, greater cost-sharing does appear to be a significant factor behind the minimal growth in premiums:

Many employers are … raising the annual deductibles workers must pay before their health plans begin to share most health care costs. A total of 27 percent of covered workers now face annual deductibles of at least $1,000, up from 22 percent in 2009, the survey finds. Among small firms (3–199 workers), 46 percent face such deductibles…

Among other plan types, only consumer-driven plans (which are high-deductible plans that also include a tax-preferred savings options such as a Health Savings Account or Health Reimbursement Arrangement) saw growth in their market share. Such plans now enroll 13 percent of covered workers, up from 8 percent last year…

“Consumer-driven plans have clearly established a foothold in the employer market, tripling their market share from 4 percent in 2006 to 13 percent today,” said study lead author Gary Claxton, a Kaiser vice president and director of the Healthcare Marketplace Project.

“This may be helping to stem the rapid rise in premiums that we saw in the early 2000s, but it also means employer coverage is less comprehensive,” says Altman.

Yes, and that’s generally good news too. Federal tax law encourages workers to increase their consumption of employer-sponsored insurance at the expense of other stuff they value more. In a 2004 study for the Cato Institute, Christopher Conover estimated the tax preference for employer-sponsored insurance leaves Americans more than $100 billion worse off each year. That same tax preference also fuels the “relentless” rise in health insurance premiums. The trend toward greater cost-sharing shows that private markets are responding to rising prices the way they should: by limiting consumption of low-value items.

Maulik Joshi, who is “president of HRET and senior vice president for research at the American Hospital Association,” worries, “High out-of-pocket expenses … affect health care decisions for patients… [H]ouseholds will face difficult choices, like forgoing needed care, or reexamining how they can best care for their families.” Exactly. Someone needs to choose between health care and other uses of money. Avoiding those difficult choices is not an option. The best available evidence suggests that consumers do a remarkably good job with those decisions. The only lamentable part is that employers are deciding how to make health insurance less comprehensive (greater cost-sharing vs. managed-care controls), instead of workers making those decisions for themselves.

But isn’t this generally good news? Apparently not to the folks at KFF and HRET. In a subsequent post, I’ll explore the negative spin they put on what their survey found.

A week ago today, I questioned both the premises and purpose of an upcoming National Journal forum on ObamaCare and job creation. The forum’s promotional materials touted the new health care jobs that the law will create as a Good Thing, even though we already have too many health care jobs. All in all, it looked to be a very dignified pro-Obama(Care) rally, funded by one of ObamaCare’s biggest beneficiaries, the drugmaker Eli Lilly. The Washington Examiner’s Tim Carney picked up on the story. Then Instapundit added his own pithy interpretation: “Hey, the Atlantic media empire needs money. Eli Lilly has it. Plus, it boosts Obama. Win-win!” (Actually, I believe that would be win-win-win.)

To its credit, National Journal has since added balance to the forum and its panel. I received a promotional email today that reframes the event by asking, “are the right jobs being created?” (Emphasis mine.) They’ve also added AEI’s Tom Miller to the panel, who I’m guessing will cast a skeptical eye on the value added by these new health care jobs. Now the event looks to be a dignified and balanced discussion of ObamaCare.

National Journal still describes ObamaCare as “reform,” which I submit compromises objectivity. But this is progress. Kudos to them.

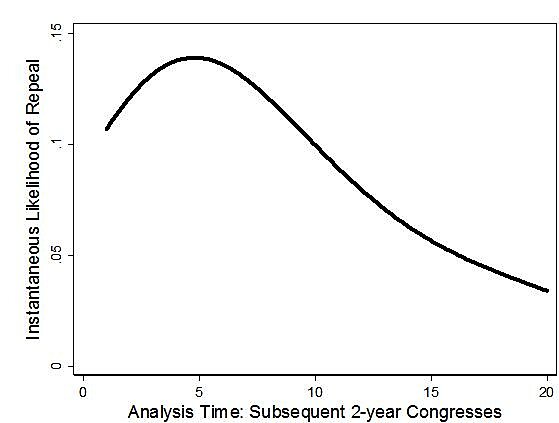

The political science blog Rule 22 has a post discussing the likelihood of repealing at least some part of ObamaCare. Author Jordan Ragusa finds:

Ragusa is predicting only that the odds are better than 50–50 that Congress will repeal some part of the law, such as the expanded 1099 reporting, which House Democrats have already moved to eliminate because small businesses find it so onerous. He is not laying odds on whether Congress will repeal the entire law or its most important and unpopular provisions (i.e., ObamaCare’s individual mandate).

His post does shed light on the likelihood of repealing the individual mandate, however. As the below graph shows, the probability of repealing any provision of major legislation rises in each of the next five Congresses (i.e., over the subsequent 10 years). After that point, the probability of repeal begins to fall.

Note that this graph shows the instantaneous probability of repeal. The cumulative probability is the area under the curve, and increases monotonically over time. Thus the probability that Congress will repeal some part of ObamaCare by 2020 is more than 13 percent.

Ragusa therefore concludes:

the newly enacted law will be most “at risk” not in the next Congress, but a decade from now. So sit tight.

Also noteworthy is that Ragusa presents only the probability of legislative repeal. The prospect that the courts may invalidate all or part of the law increases the probability that some day, ObamaCare will no longer be on the books.

H.R. 3421, the “Medical Debt Relief Act of 2009,” has nothing to do with relieving people of medical debts. It adds to the list of information credit reporting agencies may not communicate to their clients.

Current law bars credit bureaus from sharing truthful information about bankruptcies occuring more than ten years in the past, and lawsuits, judgments, tax liens, accounts placed in collection, or other adverse information more than seven years old, except in certain high-dollar credit transactions. This bill would add a new item to the list of officially banned information: medical debts that have been paid more than thirty days before a credit report is issued.

There are many cases, of course, where people who incur medical debts deserve our sympathy. But do they deserve our money?

If this bill becomes law, it will relieve people of one burden of medical debt. Lightening the obligation to save for a medically rainy day or carry health insurance, the bill will produce more people who fall on hard times due to illness or injury. These spendthrifts are worse credit risks than others, and their ability to obfuscate this will drive up the cost of credit.

The result? More expensive credit for everyone to cover the risk of medical debtors. A transfer of wealth from people responsible enough to save and buy health insurance to those who are not.

Not to worry, defenders of the law may say, Congress has findings in the bill saying that “medical debt collections are more likely to be in dispute, inconsistently reported, and of questionable value in predicting future payment performance because it is atypical and nonpredictive.”

The credit industry has a highly sophisticated cadre of analysts working to determine what facts and circumstances are, and are not, predictive of financial acuity. Congress does not. ‘Nuff said.