(This is the last of a three-part series.)

In my first and second posts addressing a recent Bank of Canada Working Paper by Ben Fung, Scott Hendry, and Warren E. Weber, I argued that the paper exaggerates the shortcomings of Canada’s 19th-century currency system, with its reliance upon the notes of numerous commercial banks, and also that it wrongly credits “government intervention” for various improvements to the system that were in fact instigated by Canada’s commercial bankers themselves.

With this third and final post, I come to the brass tacks of Fung et al.‘s paper: its conclusion, supposedly informed by shortcomings of Canada’s 19th-century currency system, that even if governments supply their own, official digital monies, so long as private digital currencies aren’t altogether outlawed, it will take government regulation to render them safe and uniform.

The validity of this conclusion depends, first, on that of Fung et al.‘s understanding of the shortcomings of Canada’s private banknote currency; second, on whether they are correct in arguing that government interference played an essential part in perfecting that currency; and, lastly, on whether they are justified in treating today’s digital currencies as analogous to yesterday’s banknotes. Having addressed the shortcomings of Fung et al.‘s assessment of Canada’s banknote currency in my previous posts, I now turn to consider whether they are justified in claiming that whatever was true of private banknotes is likely to be true for private digital currencies as well.

Redeemable Digital Currencies

At one point Fung et al. declare (p. 3) that “the only difference” between the commercial banknotes of long ago and today’s digital currencies is that in the one instance “monetary value was ‘stored’ on a piece of paper” whereas in the other value exists “electronically.” But the declaration doesn’t hold water. Indeed, it’s so leaky that Fung et al. themselves quickly contradict it.

The contradiction occurs as soon as Fung et al. acknowledge the existence of two quite distinct sorts of digital currency. There are, first of all, “fractionally backed digital currencies that are redeemable on demand” (p. 28), mentioned examples of which include “Octopus cards in Hong Kong, M‑pesa in Kenya, PayPal Prepaid card balances and Visa/Mastercard prepaid cards,” all of which are “denominated in a country’s monetary unit” (p. 32). Then there are private digital currencies “that have their own unique monetary unit that differs from any national currency unit,” the best-known example of which is Bitcoin.

It should be obvious that only redeemable digital currencies have much in common with Canada’s 19th-century commercial banknotes, which were also “fractionally backed,” “redeemable on demand,” and “denominated in [Canada’s] official monetary unit,” and that these digital currencies alone could possibly possess the same flaws as banknotes sometimes did.

Redeemable Digital Currencies: Riskiness and Vulnerability to Counterfeiting

It’s conceivable, for example, that PayPal might default, leaving holders of its prepaid card balances to collect what they may from its receiver or liquidator. So those prepaid balances aren’t perfectly safe, just as commercial banknotes were never perfectly safe. It’s even possible that PayPal balances might someday command less than their par value, though (for reasons I’ll get to) it isn’t so easy to imagine why they’d ever be discounted so long as PayPal stays solvent. Finally, prepaid cards can be, and sometimes are, counterfeited, by compromising the data in a genuine card and using it to create fake copies. Though chip-based cards are much harder to clone, even those aren’t entirely safe.[1]

But while redeemable digital currencies may possess all these imperfections, that hardly means that they possess them to the degree that banknotes sometimes did, or to one warranting government intervention. To repeat a point I insisted on in my first installment in this series, imperfection doesn’t imply inefficiency, which is to say that the costs of regulatory interference aimed at correcting the imperfections may exceed those of the imperfections themselves.

In fact, neither the imperfect safety nor the vulnerability to counterfeiting of today’s redeemable digital currencies appear significant enough to justify any sort of government interference. Regarding the risk of counterfeiting, for example, although stored value cards are sometimes counterfeited, the problem is far less serious than it is for ordinary credit card counterfeits. For that reason few stored value card issuers have so far found it worthwhile to add chips to their cards. Should the counterfeiting problem become more severe, more will presumably take that step, just as many credit card issuers have done.

Redeemable Digital Currencies: Likelihood of Discounts

When we come to consider the likelihood that redeemable digital currencies will routinely command less than their par or face value, as banknotes sometimes did, it becomes apparent that even these superficially similar types of currency are in some respects as different as night and day. Discounts applied to the notes of solvent banks mostly reflected the costs brokers stood to incur in getting them redeemed, including the costs of receiving, sorting, and storing the notes and, once enough were accumulated, those of bundling and sending them on their way back to their places of origin via mail stage, railway mail car, or St. Lawrence steamer. There were besides this the costs of having their redemption proceeds sent back to them, whether by the same costly means, in the shape of gold or Dominion notes, or by bank draft.

Redemption of banknotes’ modern digital counterparts is, in contrast, accomplished by means of a few keyboard strokes, by which light pulses are sent hurtling through glass-fiber cables, at speeds lately approaching that of unimpeded light itself. It all happens, moreover, at trifling cost. For this reason alone, even if it had taken government intervention to do away with discounts on Canada’s commercial banknotes, it wouldn’t follow that such intervention will be needed keep today’s redeemable digital currencies current.[2]

Am I saying that the market for redeemable digital currencies is efficient? Not quite. Because the digital currency industry is still in its swaddling clothes, there are ample opportunities for successful providers to assess fees exceeding their costs, and to secure corresponding surpluses. Still the presumption ought to be that, as the industry matures, competition will prove no less effective in hammering-down the surpluses than it is in rewarding relatively efficient firms in the first place.

Indeed, one need only look to see this very process taking place before one’s eyes. Consider Safaricom, one of the two Kenyon mobile network operators (the other is Vidacom) that launched M‑pesa back in 2007. Safaricom charges fees typically ranging between one and two percent for various M‑pesa transactions, and has made handsome profits by so doing. Yet it recently chose to dispense with charges for smaller transfers; and it’s bound to make similar decisions in the future as competition among rival digital currency suppliers stiffens.

All this, I realize, is the stuff of any principles text. Yet it’s worth pointing out lest anyone should lose sight of it. I also think it prudent to observe that, generally speaking, if one wishes to avoid inefficiency, the last thing one ought to do, except perhaps in those uncommon instances in which an industry qualifies as a “natural monopoly,” is to let an outfit already gifted with a statutory monopoly of some product — whether it be paper currency, soap bars, or salt — compete with private sector suppliers of other products, including substitutes for the monopolized good. Letting it enter these other markets is, after all, a recipe for having it resort to cross-subsidies to defeat its more efficient private sector rivals — an alternative to outright prohibition that Fung et al. (p. 32) don’t appear to consider.

Non-Standard Digital Currencies

Turning to private digital currencies that are neither denominated nor redeemable in some official money — and that aren’t, for that matter, redeemable claims to anything at all — it should be perfectly obvious that these have about as much in common with old-fashioned banknotes as a $50 gold Maple Leaf has with a $50 deposit credit at the RBC or Scotiabank. While both a banknote and a bank deposit credit are IOUs, bitcoins and Maple Leafs aren’t.

It should therefore be equally obvious that non-standard digital currencies are necessarily both free of default risk and incapable of having a market “value” distinct from their nominal or face value. The value of a bitcoin can and does fluctuate in terms of other currencies; but a bitcoin is always worth precisely one bitcoin. It follows that, whatever experience may tell us concerning losses suffered by banknote holders owing to either bank failures or discounts applied to the notes of solvent banks, that experience tells us even less about today’s non-standard digital currencies than the precious little it tells us about their standardized and redeemable counterparts.

That leaves counterfeiting. Fung et al. think it “likely that digital currencies would be subject to criminal attempts to counterfeit them,” and it is hard to disagree with them. But here again, the statement is more true of redeemable digital currencies than of non-standard ones, including bitcoin and other cryptocurrencies which, as Fung et al. recognize (p. 27), appear to have solved the counterfeiting problem “by requiring ‘proof of work’ or ‘proof of stake’ before a block of transactions can be added to the blockchain.” The concession is important, for, so far at least, no other actual or would-be currencies, whether official or private, can claim to be counterfeit-proof. That point ought surely to be seen as a decisive one in at least some digital currencies’ favor.

Yet instead of emphasizing the point, Fung et al. devote but a single, fleeting sentence to it. They also surround that sentence with others concerning problems other than outright counterfeiting to which decentralized digital currencies are supposed to be uniquely vulnerable, namely, the so-called “double spending” problem, and the risk of “fraud and cyber attacks.” But “proof of work” schemes are just as effective in preventing double spending, where a legitimate owner of digital currency units makes and spends copies of those units, as they are in ruling-out outright counterfeiting. The outright theft of stored bitcoin through successful hacking of security systems has, in contrast, been a very real problem. But despite what Fung et al. claim, and as Willie Sutton (or any garden-variety mugger or purse-snatcher) might tell you, currencies that “rely on a trusted third party,” including the paper currencies that central banks supply, can be stolen no less easily.

The Question of Scarcity

Thus far, both here and in my previous posts in this series, I’ve referred to only three items in Fung et al.‘s list of “five desirable characteristics of a medium of exchange”: minimal exposure to counterfeiting, a high degree of safety (taken to mean safety from loss owing to a providers’ insolvency), and uniformity with respect to the prevailing standard monetary unit. I’ve overlooked the other two, ease of transacting and scarcity, because Fung et al. themselves allow that with respect to these characteristics Canada’s private banknotes were no worse than available alternatives, including Dominion notes.

Fung et al. say nothing about the relative ease of transacting with private digital versus government-supplied currency. They do, however, compare the capacity of digital currencies to remain scarce to that of government fiat currencies, to the disadvantage of the former. While at least some central banks, including those of Canada, the U.S., England, Europe, and Japan, are, in their words, “committed to keeping inflation low and stable,” they believe that

Private digital currencies are likely to be scarce only when subject to strong government regulation or when their are rules for issuance hard coded from the beginning and not subject to any change (p. 28).

It’s hard to see just how Fung et al. arrive at this conclusion. With regard to redeemable digital currencies, the mere fact that their issuers (like most private issuers of redeemable IOUs but unlike modern central banks) face the penalty of failure in the event of nonpayment has been by far the most powerful constraint against excessive issues. It sufficed, at any rate, to keep the supply of banknotes in check in Canada when its banks were able to issue notes subject to no practical limit save the requirement that banks pay their notes on demand.[3] If there is some reason for supposing that a similar obligation won’t suffice to contain the growth of today’s redeemable digital currencies, Fung et al. should spell it out.

Concerning non-standard digital monies, it’s of course true, as Fung et al. say, that these may not be sufficiently scarce, and may therefore fail to “ever enjoy wide spread acceptance,” unless rules limiting their multiplication are “hard coded from the beginning.” But whoever thought otherwise? And is this not something we can safely let private digital currency suppliers discover for themselves, as at least some have already done? What’s the point, in short, of insisting on the necessity of government regulation in the event that private firms attempt to do what they can’t possibly get away with doing? One might as well observe that government regulation “may” be called for to keep privately-manufactured airplanes from dropping out of the sky, or never getting off the ground, unless their manufacturers happen to take the trouble to equip them with wings and other such aerodynamically-appropriate devices.

Fung et al. insist nonetheless that even those non-standard private digital currencies that manage to get off the ground are more likely to end up becoming worthless than their government-supplied counterparts. In defense of this view they note that several non-standard digital currencies have already come and gone, whereas they are unaware of “evidence of any government issued fiat currency having become valueless” (p. 29). Reading that last statement, I couldn’t help thinking of an old bank building in Madison, GA, not far from where I used to live, that still contained the former bank’s vault. When I saw it the vault’s interior was literally lined with Confederate States’ notes. Were they not smothered with glue and varnish, those notes would be worth something to collectors today. But they sure couldn’t have been worth much to whoever glued them on the vault walls in the first place!

To be fair, Confederate money only became worthless after Lee surrendered at Appomattox, so perhaps the example shouldn’t count. But there are numerous other examples one might point to — enough, at least, to have inspired Irving Fisher to remark, in 1910, that “Irredeemable paper money has almost invariably proved a curse to the country employing it” (Introduction to Economic Science, p. 219, my emphasis). Consider those famous pictures, taken in Weimar Germany, of a man papering a wall with Reichsmarks while the Reichsbank was still a going concern, or of a woman lighting her stove with them? And how about those $100 trillion Zimbabwean notes that ended up being worth less than a penny — and that mainly because their very worthlessness made them popular with souvenir hunters?[4] Last and, in this case, also least, let’s not forget those notorious Hungarian pengős, 3.8 of which were worth a gram of gold when they were first introduced in 1927. By August, 1946, when the forint was introduced, a gram of gold cost 5300 octillion pengős! Admittedly a unit of currency worth 1/5300 octillion grams of gold is, mathematically speaking, worth more than zero. But who’s counting?

Admittedly Fung et al.‘s claim that government fiat currencies are less likely to become worthless than their private digital counterparts rests on something other than the difference between 1/5300 octillion and zero. It depends as well on the authors’ belief that official currency issuers enjoy the ability “to declare their currencies legal tender and require that they be accepted in certain transactions.” But while legal tender laws may suffice to render fiat currencies valuable in the settlement of certain preexisting debts, they have no bearing at all on such currencies’ value in spot transactions.

As for such currencies’ acceptability in payment of taxes and other government dues sufficing to keep them from becoming worthless, the claim begs the question: acceptable at what rate? Imagine, if you will, a poll tax payable in old Zimbabwean dollars. Unless Zimbabwe’s tax authorities suffer from money illusion, that tax would tend to increase no less rapidly than other prices. The public receivability of official fiat monies tends, in other words, to contribute little more to their value than their receivability among other sellers of goods and services. As a bulwark against hyperinflation, a paper currency’s legal tender status is in itself far less reassuring than an absolute quantity limit like the one that will forever keep the quantity of bitcoins below 21 million.

Overlooked Advantages of Banknote Currency

I come now to what I regard as the most serious shortcoming of Fung et al.‘s paper, namely, it’s failure to consider the ways in which private currency may be better than government-supplied alternatives. That in assessing Canada’s 19th century experience, Fung et al. never take this possibility seriously is evidenced by their asking, “Did Dominion Notes Improve the System?” without ever asking whether Dominion Notes may actually have been worse than Canada’s commercial banknotes.

Yet to judge either by the opinion of contemporary experts, or by the preferences of Canada’s citizens, Dominion notes were inferior to commercial banknotes. Regarding the public’s verdict, it’s notorious that the notes of Canada’s commercial banks were its currency of choice, which it preferred, not only to government currency, but to gold itself. Consequently to create a demand for Dominion notes the Canadian government had, not only to make them full legal tender, and require that the chartered banks hold them in amounts equal to no less than 40 percent of their legal tender reserves, but to outlaw banknote denominations below $4 and (after 1880), below $5. Were it not for the last of these provisions, it’s highly doubtful that Dominion notes would have circulated at all, for the chartered banks would naturally have been inclined to “push” their own notes, and there’s no evidence that Canada’s citizens would have hesitated to take them.

And while the verdict of Canada’s citizens might be set aside by some readers as proof of nothing save those citizens’ lack of discernment, that of contemporary experts can’t be so readily dismissed. And that verdict was also unanimous in holding banknotes to be superior to redeemable government paper currency.

Banknotes were considered superior to government paper money in three important respects. First, banks stood to lose more by dishonoring their promises, bankers were less likely to break those promises than government authorities were. Second, bankers were more likely to employ the scarce savings represented by the public’s currency holdings productively. Finally, banknote currency was “elastic,” meaning that its quantity tended to adapt automatically to secular, cyclical, and (especially) seasonal changes in demand, whereas government-supplied currency was not. Because there’s no place for these advantageous qualities of banknote currency among the “desirable characteristics of a medium of exchange” Fung et al. consider relevant “for determining how well private bank notes and government notes performed” (p. 3n. 2), their appraisal severely underrates banknotes in comparison to their government counterparts.

Banknotes Contributed to the Efficient Employment of Savings

I have already, in the first part of this series, referred to the superior efficiency and elasticity of Canada’s banknote currency in arguing that these advantages more than compensated for the somewhat lower security of such currency (judged solely in terms of its specie backing) compared to Dominion notes. So it remains for me only to elaborate a bit more on these traits.

As Joseph Johnson pointed out in 1910 (p. 129), thanks to the Canadian public’s “unquestioning confidence” in Canadian banks’ notes and other credit instruments, they “never demand that they be converted into gold,” which is “used only between banks and in the foreign exchanges.” The banks, in other words, had succeeded in developing “an almost perfect credit system” — the very embodiment of Adam Smith’s ideal highway “suspended upon Daedalian wings.” The savings represented by the Canadian public’s currency holdings, or that part of it which the government did not acquire by monopolizing the supply of currency of denominations below $5, was almost entirely backed by productive bank loans, rather than by either specie or loans to the Dominion government. Had the government succeeded in any of its several attempts to completely substitute Dominion notes for banknotes, those savings would instead have been either locked-up in so much gold coin and bullion, or commandeered by the Canadian government.

In summary, Canada’s banknotes were, in contrast to either Dominion notes or the notes of U.S. national banks, genuine commercial credit instruments, as opposed to fiscal devices whose real purpose was to secure forced loans to the government from the public, either directly or via bank reserve or note-collateral requirements. It’s possible, of course, that Fung et al. don’t consider the difference important. Perhaps they don’t believe it matters much how scarce savings are employed. Or perhaps they deny that Canada’s private banks were any more capable of employing such savings productively than Canadian government authorities were. But if they believe either of these things, they ought to say so. And since in holding either view they’d be bucking centuries of received opinion, they also ought to say why.

Banknotes Provided an “Elastic” Currency

However impressive it may have been, the efficiency of Canada’s banknote currency was not nearly as widely appreciated as its elasticity was. For while Canadians themselves may have been inclined to take their elastic currency system for granted, U.S. observers were keenly aware of it, and of the stark contrast between it and their own nation’s notoriously inelastic paper currency, consisting of greenbacks and national bank notes. During the final decades of the 19th century, and the first decades of the 20th, the inelasticity of the U.S. currency stock was an important cause, if not the main cause, of recurring financial crises. Just how currency inelasticity contributed to U.S. crises is a subject too involved to go into here (though readers can find a quick summary in this Cato Policy Analysis). But that it did so ought to be evident enough from the fact that the Federal Reserve System was established “to furnish an elastic currency.”

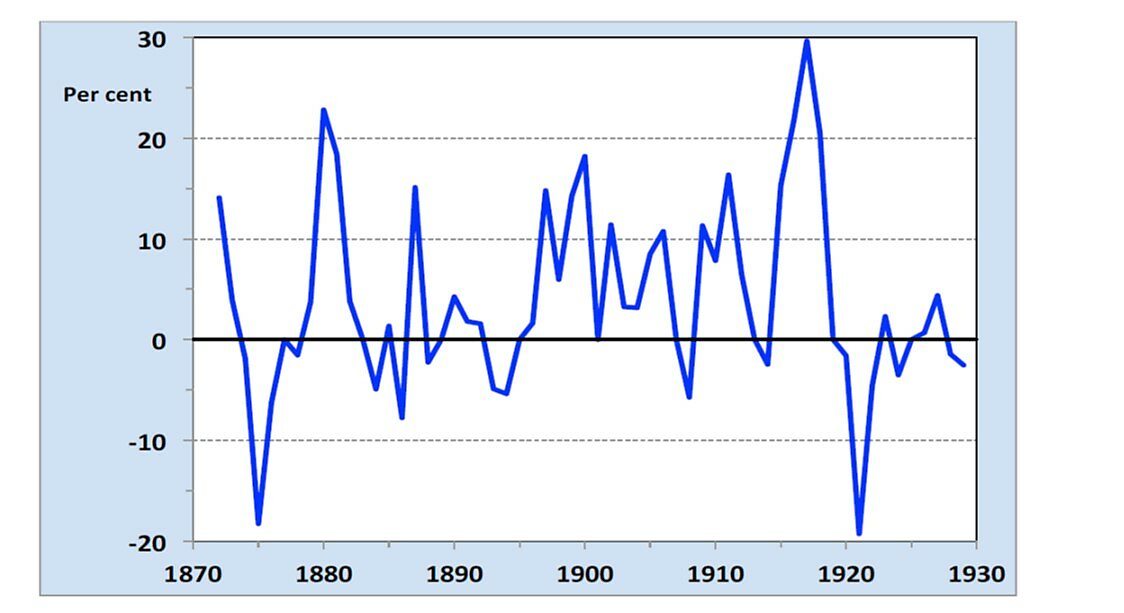

That Canada’s elastic banknote currency allowed it to avoid the crises that afflicted the U.S. economy is no minor detail. Yet Fung et al. never so much as hint at this advantage of Canada’s banknotes — or at the fact that the supply of Dominion notes were even less elastic than national bank notes in the U.S. The only reference Fung et al. make to variations in the stock of Canadian banknotes consists of some remarks concerning year-to-year growth rate changes (p. 19), which they illustrate with the following chart:

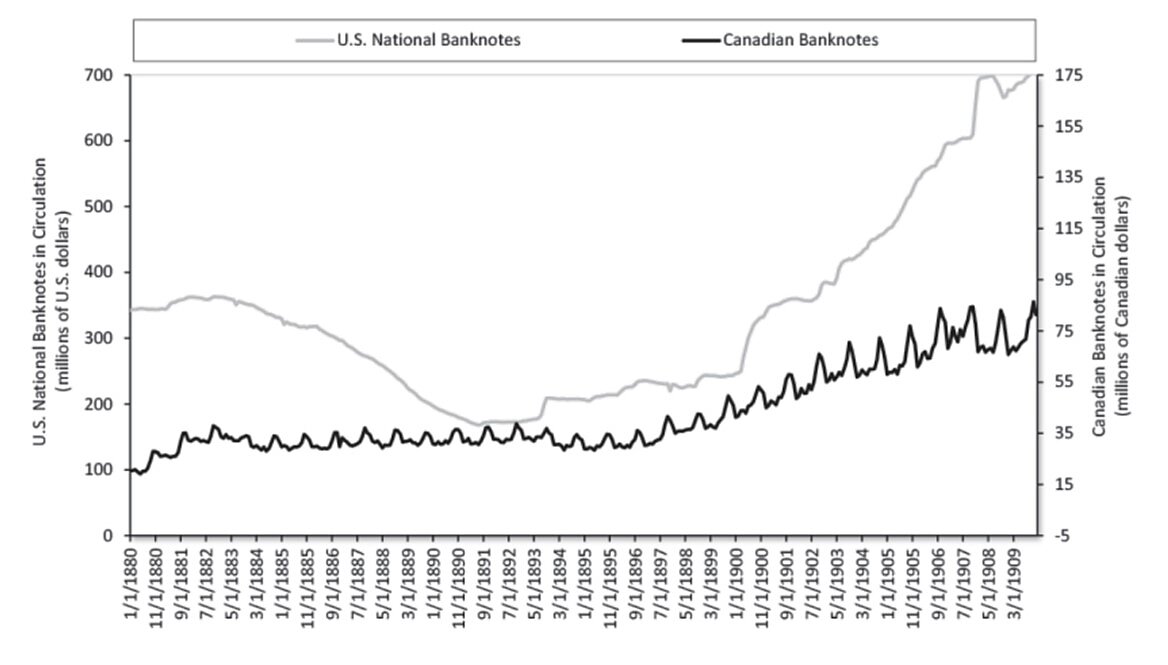

Someone knowing nothing more about the behavior of the Canadian banknote supply than what this chart reveals might be forgiven for supposing that the vaunted “elasticity” of Canada’s banknote supply was but a euphemism referring to its volatility. But here is a different picture, showing levels rather than growth rates, and using monthly rather than annual data, for both U.S. national bank notes (left scale) and Canadian banknotes (right scale) :

Alas, Fung et al.‘s paper supplies neither such chart, nor any other indication of the lovely saw-tooth pattern of Canada’s currency stock, perfectly reflecting both the comings and goings of the harvest season, and the secular growth of Canada’s economy.[5]

Canada’s banknote currency had yet another important advantage that not only Fung et al. but most other modern authorities overlook: its role in fostering branch banking. Branch banking itself was, of course, a highly advantageous feature of the Canadian system that the U.S. banking system long lacked. Besides contributing to Canadian banks’ safety by making it relatively easy for them to diversify their assets and their liabilities, it also made it much easier for bank-intermediated credit to flow where it was most needed, equalizing interest rates in the process.

But it was only because they were free to issue their own notes that Canada’s chartered banks found it profitable to establish far-reaching branch networks. For had Canada’s banks been obliged to stock their branches’ tills and safes entirely with specie and Dominion notes, instead of having them serve only as small change, the cost would have been prohibitive. By equipping those branches with their own notes instead, they saved a corresponding amount of resources, for until those notes were actually placed into circulation, they were, as one Canadian banker put it (p. 834), “merely so much paper.”

The Real Lesson

I come now at last to what I consider to be the most disappointing thing about Fung et al.‘s working paper. It isn’t that it exaggerates the flaws of Canada’s private banknote currency, or that it understates the bankers own part in correcting those flaws. And it isn’t that it overlooks Canadian banknotes distinct advantages over government paper currency. Nor is it that Fung et al. employ their misleading appraisal of Canada’s 19th-century system to arrive at still less reliable conclusions regarding the inherent defects of digital currencies. What’s most disappointing about the paper is that one might read every word of it, and carefully, without ever realizing that, even before the reforms of the 1880 and 1890, Canada’s private currency system was widely considered, by experts and non-experts alike, to be one of the world’s best currency systems ever, and a darn good one at that.

For testimony on this point, one might turn to the any of the same authorities upon whom Fung et al. rely in cataloguing the Canadian system’s flaws, as well as to many other authorities. For our purposes, the two sources upon which Fung et al. rely upon most heavily should suffice. Toward the end of his history Breckenridge (p. 355) says that “The efficiency of the banks … their services to the country, have received about all the positive description that the subject permits.” He then devotes his book’s final chapter (p. 360ff) to a detailed description of the Canadian banking system’s many advantages, ending with a flurry of rhetorical questions that, read in context, amount to a summary:

How the Canadian banks economize capital; how they utilize and distribute it; what is the security, convertibility and elasticity of the circulating medium they supply; how thoroughly are their creditors protected against loss; how low and how nearly equal are the rates of interest in different parts of the country; how cheaply are other banking services sold; how easy of access are banking facilities; what support have worthy customers in critical times; and how far does the system promote the stability of commercial confidence: these are questions to which, perhaps, this chapter forms an answer. According to the true response, the merits of the Canadian Banking System must be judged. If the present answer be sufficient, the reader may draw his own conclusions.

According to Joseph French Johnson (p. 128), Canada’s banknote-based currency system

possesses features of extraordinary merit, adapting it admirably to the needs of the country which it serves. It performs most efficiently the service for which banks are created, gathering up the country’s idle capital and placing it in channels of useful employment. … The law leaves the banks such freedom that business is never brought to a halt through lack of instruments of exchange; whether the need be for checks and drafts or for bank notes, the supply is always adequate. The redemption system insures perfect elasticity for both the note and deposit currency. …Finally…the system possesses a solidarity that makes possible united action in the face of a common peril.

Similar words of praise can be found in works not mentioned by Fung et al. Thus George Hague, in his “Historical Sketch of Canadian Banking” (p. 476), observes that “No person acquainted with Canada can doubt that its banking system has been conducive to its material interests in a very high degree, and it is the opinion of many who are conversant with the matter, that no other system would have been equally beneficial.” Elsewhere (p. 452) Hague remarks that Canada’s system is “perfectly adapted to the wants of the country, and has proved itself so during the most trying periods of commercial depression, no matter how long protracted.”

Nor, as I’ve shown previously on Alt‑M , was such praise voiced only by bankers and economists.

Yet for Fung et al., the sole merit of Canada’s 19th-century currency arrangement lies in its supposed ability to adumbrate the likely flaws of today’s private digital currencies, and the consequent need for regulators (including, presumably, the Bank of Canada) to stick their mitts in it. Honing-in as it were on every knot and toadstool they can discover disfiguring trunks within the forest of Canada’s chartered banks, they overlook the tremendous merits of the forest itself, and thus manage to arrive at precisely the wrong answer to the question their paper poses.

That question, to paraphrase it, is, “In light of Canada’s experience with commercial banknotes, what must regulators do to perfect today’s private digital currencies?” Stand back a ways, ignore those toadstools and knots, and behold that glorious old forest. The right response, surely, is not unlike the one French businessmen famously gave to Jean-Baptiste Colbert, France’s Comptroller-General of Finances, back in 1681: leave them be.

____________________________

[1] PayPal Prepaid card balances are, on the other hand, safer than cash itself in at least one respect, for if you lose cash you’re out of luck, while according to PayPal “If your card is lost or stolen, we will, upon your request, send you a new card. Your funds will be transferred to the new card account.” In this as well as in other respects, including the fees involved, prepaid card balances resemble travelers’ checks rather than banknotes, raising the question whether Fung et al. should be drawing conclusions regarding the need to regulate them from past experience with such checks, rather than with circulating banknotes.

[2] If Canada’s experience with banknote discounts supplies only dubious grounds for regulating digital currencies, antebellum U.S. experience, to which Fung et al. also appeal (p. 30), is still less pertinent, for the relatively extensive note discounts of that episode were peculiar byproducts of unit banking, which is now defunct.

[3] Fung et al. wrongly attribute the scarcity of Canada’s commercial banknotes to official “restrictions on the quantity that could be issued,” and particularly to the post-1871 stipulation limiting banks’ circulation to their paid-in capital. “Since banks did not increase their capital very often,” they write, “this [capital limitation] controlled the supply of banknotes” (p. 18). But the capital limit didn’t actually become binding until 1906. Something else must have kept banknotes scarce until then. That something was, surely, the fact that banknotes were routinely presented for payment in gold or Dominion notes, which were themselves scarce, with failure as the penalty for non-payment. That Fung et al. don’t recognize this most basic mechanism for limiting the expansion of redeemable bank money is more than a little disconcerting.

[4] Regarding that Zimbabwean $100 trillion note, Fung et al. observe (p. 29n32) that instead of being valueless it was still worth a loaf of bread in 2009. But the story of the Zimbabwean dollar didn’t end in 2009, for that currency wasn’t officially abandoned until the summer of 2015, when a new Zimbabwean dollar was introduced, with a starting value once again equal to one U.S. dollar. At the then official exchange rate, one old $100 trillion note was worth just 40 cents of the new currency, while in Harare a loaf of plain white bread cost $1.3, which is to say more than three old $100 trillion notes.

[5] For an excellent discussion of how Canada’s banks furnished the extra paper currency needed for its harvest season — and automatically took it back once the season had passed — see A. St. L Trigge, “How Canada Provides Currency for Moving the Crops,” The Bankers’ Magazine 72 (1906), pp. 834–41.