Executive Summary

Both the American left and right often use “national security” to justify sweeping proposals for new U.S. protectionism and industrial policy. “Free markets” and a lack of government support for the manufacturing sector are alleged to have crippled the U.S. defense industrial base’s ability to supply “essential” goods during war or other emergencies, thus imperiling national security and demanding a fundamental rethink of U.S. trade and manufacturing policy. The COVID-19 crisis and U.S.-China tensions have amplified these claims.

This resurgent “security nationalism,” however, extends far beyond the limited theoretical scenarios in which national security might justify government action, and it suffers from several flaws.

First, reports of the demise of the U.S. manufacturing sector are exaggerated. Although U.S. manufacturing sector employment and share of national economic output (gross domestic product) have declined, these data are mostly irrelevant to national security and reflect macroeconomic trends affecting many other countries. By contrast, the most relevant data—on the U.S. manufacturing sector’s output, exports, financial performance, and investment—show that the nation’s total productive capacity and most of the industries typically associated with “national security” are still expanding.

Second, “security nationalism” assumes a need for broad and novel U.S. government interventions while ignoring the targeted federal policies intended to support the defense industrial base. In fact, many U.S. laws already authorize the federal government to support or protect discrete U.S. industries on national security grounds.

Third, several of these laws and policies provide a cautionary tale regarding the inefficacy of certain core “security nationalist” priorities. Case studies of past government support for steel, shipbuilding, semiconductors, and machine tools show that security-related protectionism and industrial policy in the United States often undermines national security.

Fourth, although the United States is not nearly as open (and thus allegedly “vulnerable”) to external shocks as claimed, global integration and trade openness often bolster U.S. national security by encouraging peace among trading nations or mitigating the impact of domestic shocks.

Together, these points rebut the most common claims in support of “security nationalism” and show why skepticism of such initiatives is necessary when national security is involved. They also reveal market-oriented trade, immigration, tax, and regulatory policies that would generally benefit the U.S. economy while also supporting the defense industrial base and national security.

Theoretical Justifications for National Security Protectionism and Industrial Policy

“National security” has long been invoked to justify government policies intended to support manufacturing in case of war or another emergency. The justification has been offered not only by trade skeptics and supporters of industrial policy (i.e., targeted and directed government efforts to plan for specific future industrial outputs and outcomes1) from Alexander Hamilton to Donald Trump but also by advocates of free markets.2

The general argument of each side is similar: open markets may be good in most cases, but ensuring the productive capacity of essential manufacturing sectors can warrant the imposition of tariffs, subsidies, or other types of industrial planning. Trade skeptics and industrial policy advocates go further, however, by arguing that American “deindustrialization” (and, by extension, “dependency” on foreign production) justifies interventionist U.S. trade and economic policy. Indeed, the absence of such policies is often alleged to have caused the manufacturing sector’s demise. Related to the first point, the skeptics and industrial policy advocates are also trusting of the efficacy of protectionism and industrial policy to achieve national security objectives. These same individuals further assume that open trade is incompatible with national security and economic “resiliency.”

An April 2020 op-ed from Sen. Marco Rubio (R‑FL) is indicative of the interventionist case:

Any prudent policymaker should recognize that both efficiency and resiliency are values we should prioritize and seek to balance. But that’s not what we have done in recent decades. [U.S. economic policy] choices, from offshoring to building an economy based on finance and service, have produced one of the most efficient economic engines of all time. But a pendulum can swing too far in one direction. And when an economy lacks resiliency, it can be devastating in a crisis.…

Today, the result of these failed policy choices is that our manufacturing base is severely diminished, and millions of productive jobs that relied on it are gone. The American domestic supply chain devoted to producing vital medical supplies like generic pharmaceuticals and respirators has withered.3

Rubio goes on to claim that these problems require “a new vision to create a more resilient economy” and proposes a “sweeping pro-American industrial policy” that involves “re-shoring of supply chains integral to our national interest—everything from basic medicines and equipment to vital rare-earth minerals and technologies of the future.” And he is certainly not alone: prominent politicians and pundits on the right and left routinely lament the harms that “deindustrialization” has imposed on U.S. national and economic security and propose “sweeping” programs (protectionism, domestic procurement mandates, subsidies, etc.) to fix this alleged problem.

Free marketers largely reject the interventionist critique but do acknowledge the potential need for security-related protectionism and industrial policy. Adam Smith explained in The Wealth of Nations that one of the “two cases in which it will generally be advantageous to lay some burden upon foreign for the encouragement of domestic industry” is “when some particular sort of industry is necessary for the defence of the country.“4 Smith noted that Great Britain’s military, for example, needed to maintain “the number of its sailors and shipping” and therefore supported measures to promote the domestic shipping industry at the expense of domestic consumers or other countries. Two centuries later, Milton and Rose Friedman noted that while “the argument that a thriving domestic steel industry, for example, is needed for defense … is more often a rationalization for particular tariffs than a valid reason for them, it cannot be denied that on occasion it might justify the maintenance of otherwise uneconomical productive facilities.“5 To this day, stalwart defenders of open trade and free markets permit a “national security” exception to those policies.6

However, these same scholars are quick to limit the national security exception. After granting the “defence” basis for Britain’s Navigation Acts, for example, Smith explained that it arose during a time of “violent animosity” between Britain and Holland—not merely in expectation of such hostilities—and was specifically needed to reduce “the naval power of Holland, the only naval power which could endanger the security of England.” He added that it would “very seldom” be “reasonable” to pursue such protectionism (“to tax the industry of the great body of the people” so as not “to depend upon our neighbors for the supply”).7

The Friedmans were more direct (and skeptical): “To go beyond this statement of possibility and establish in a specific case that a tariff or other trade restriction is justified in order to promote national security, it would be necessary to compare the cost of achieving the specific security objective in alternative ways and establish at least a prima facie case that a tariff is the least costly way. Such cost comparisons are seldom made in practice.“8 Contemporary economists and free marketers have reiterated such concerns: “Given the negative impact of tariffs on wealth, when they are proposed, even under the national defense justification, they should be carefully examined to see if there is a true national defense issue or if domestic firms are merely justifying tariffs for protection from competition.“9

This skepticism—mostly absent from Washington—is indeed warranted: analyses of the U.S. manufacturing sector and the relationship between trade and national security, as well as the United States’ long and checkered history of security-related protectionism, undermine the theoretical justifications for imposing protectionism and industrial policy in the name of national defense. Instead, open trade, freer markets, and global interdependence will in almost all cases produce better outcomes in terms of national security and, most importantly, preventing wars and other forms of armed conflict.

The Reality of American Manufacturing and National Security

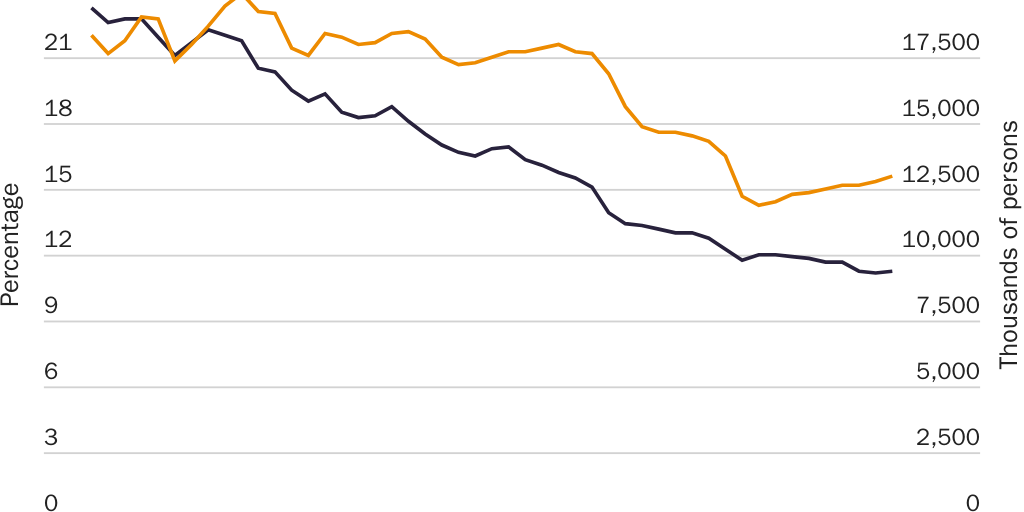

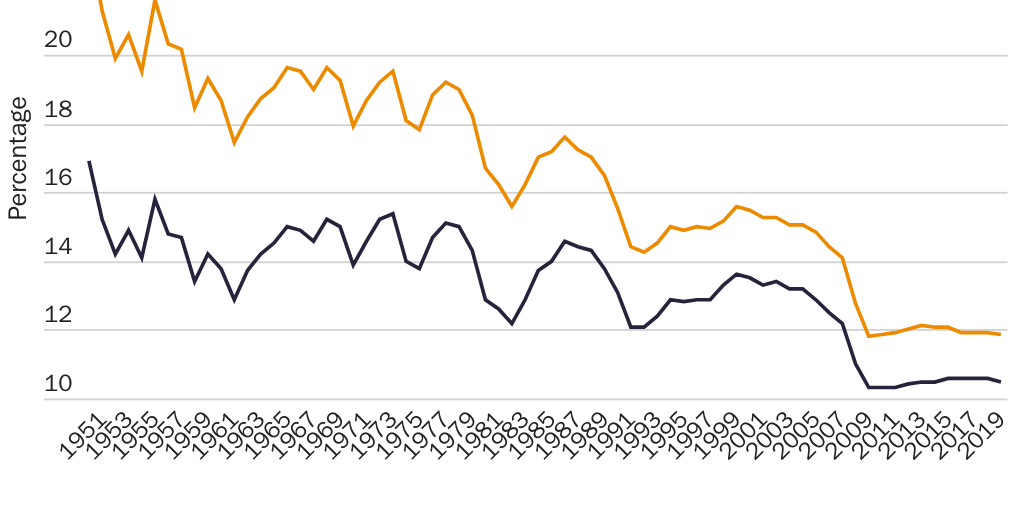

Today’s security nationalists often emphasize two trends—declining U.S. manufacturing employment and the sector’s declining share of U.S. economic output (as measured by gross domestic product [GDP])—when lamenting American industrial decline and proposing new policies to support domestic manufacturing and national security. Figure 1 shows that both trends have occurred.

However, these trends provide little insight into the state of the U.S. defense industrial base or government policies affecting it, because they primarily reflect secular, global macroeconomic forces mostly unaffected by domestic policy and say little about the productive capacity of the United States overall or of the industries that are most essential to U.S. national security.

Secular Trends Driving Changes to U.S. (and Global) Manufacturing

Both declining manufacturing jobs and the sector’s declining share of GDP primarily reflect long-term global trends disconnected from specific economic policies, whether “free market” or “interventionist.”

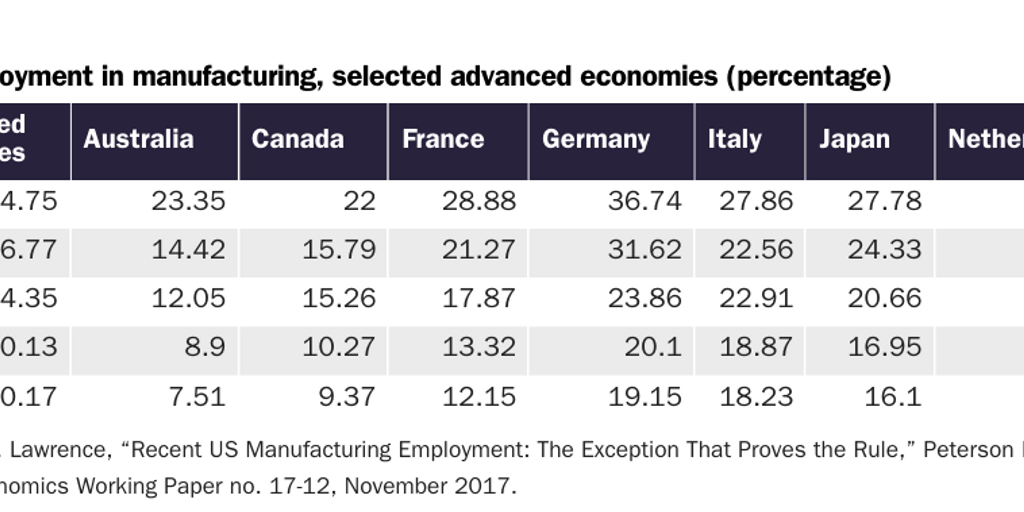

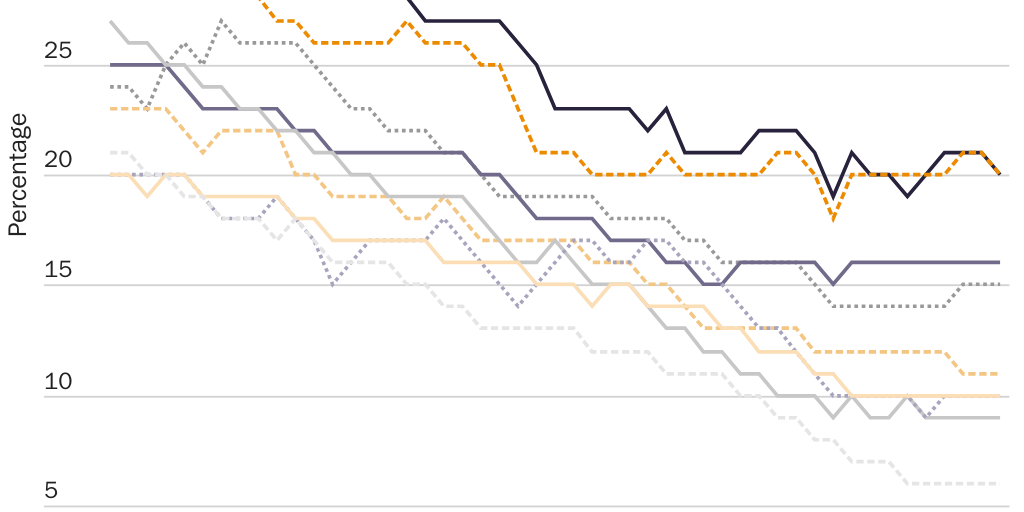

Jobs. The long-term decline in U.S. manufacturing jobs coincided with rising sector output and was mirrored in developed countries around the world—including those with economies more centered on manufacturing, with long-standing trade surpluses in goods, or with more aggressive industrial policies.10 (See Table 1 and Figure 2.) In fact, Robert Lawrence’s 2020 examination of 60 countries between 1995 and 2011 found that nations with manufacturing trade surpluses experienced slightly larger declines in manufacturing employment than those with manufacturing trade deficits and that manufacturing job losses were as large in countries with “improving” manufacturing trade balances over this period as those with “worsening” ones.11

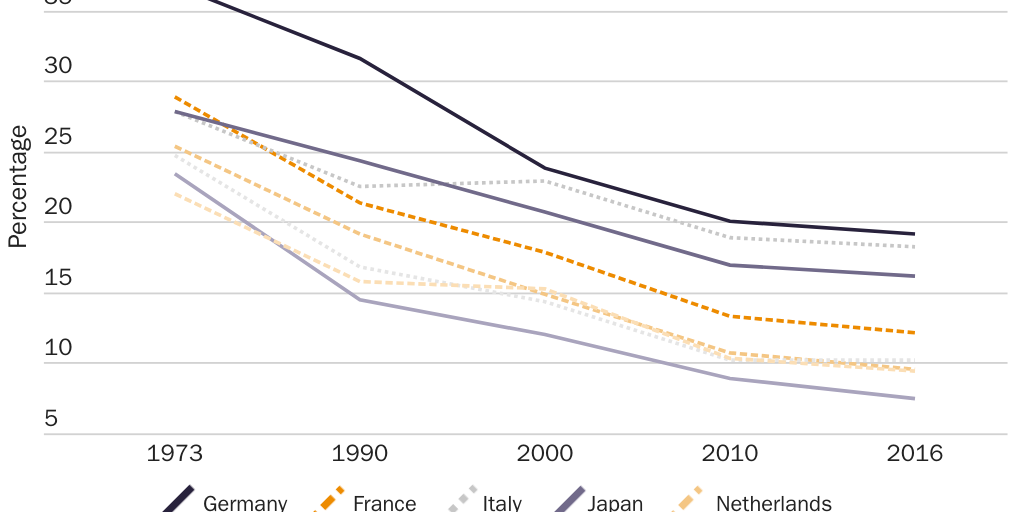

As shown in Figure 3, countries generally follow the same inverted‑U pattern of economic development, first adding and then losing manufacturing jobs as they develop.

Figures 1–3 establish that, though manufacturing in some countries represents a larger total share of a country’s domestic workforce than in the United States, the loss of manufacturing jobs—and thus the basis for any “deindustrialization” claim—is happening around the world. (Despite recent U.S. industrial job gains, the U.S. Bureau of Labor Statistics expects the longer-term downward trend to continue in the next decade, projecting a loss of almost 445,000 U.S. manufacturing jobs from 2019 to 2029.12) Thus, for example, U.S. policy might have been able to increase overall manufacturing employment at some point, but the trends—including the significant decline in jobs from the late 1990s to the late 2000s—would have remained essentially unchanged.13 Therefore, the changes in manufacturing jobs alone provide little insight into the state of American manufacturing or related U.S. policies.

Aggregate employment trends also say little about the ability of U.S. workers to produce essential goods during a national emergency. For example, U.S. manufacturing employment increased by almost 1 million jobs between 2010 and 2018, “outperforming” Germany, Japan, and China in the process. However, over the same period, real manufacturing value-added per worker and per hour worked in the United States increased by only 0.3 percent per year and 0.1 percent per year, respectively, as compared to 5.6 percent and 5.7 percent per year between 2000 and 2008—a time of significant manufacturing job loss in the United States.14 In other words, American workers were improving their ability to produce manufactured goods (and thus to supply the economy in times of war or other emergency) at a much more rapid pace during the height of “deindustrialization” than during the subsequent period of “reindustrialization.” In reality, neither job gains nor job losses demonstrate a vibrant (or lagging) American industrial sector. There also is little to indicate that U.S. manufacturing jobs deserve special government support.15

GDP Share. Manufacturing’s declining share of total U.S. GDP also reflects secular trends largely disconnected from U.S. government policy. First, the change in the industrial sector’s GDP share reflects the relative strength of the U.S. services sector instead of the weakness of American manufacturing. Indeed, between 1997 and 2019, real gross output and real value-added of private services–producing industries increased by 87 percent and 77.4 percent, respectively, while the same metrics for U.S. manufacturing increased by a slower-but-still-respectable 18.7 percent and 52.8 percent—continuing long-term trends in these U.S. sectors dating back to the 1940s.16

Second, the relative growth of services versus manufacturing reflects fundamental shifts in consumption patterns in the United States and other countries away from goods and toward services.17 In the United States, “consumers, government, and investors have been devoting declining shares of nominal spending to goods relative to services” since the 1960s, and “the overall impact, inclusive of investment expenditure on equipment and software, was a decline in nominal US spending on goods relative to services by 1.47 log points (percent) per year over the entire period.“18 Thus, U.S. consumers were allocating half of all their spending on consumption to goods—50.3 percent—in 1960 but only 33 percent by 2010. Over the same period, U.S. government consumption and investment expenditure on goods dropped from 61 percent to 42 percent.19 As shown in Figure 4, Americans’ consumption of durable goods as a share of total consumption has similarly declined since the 1950s.

These relative consumption trends coincide with the U.S. manufacturing sector’s declining share of U.S. GDP (see Figure 1), and these factors have coincided over time: documenting trends in U.S. consumption and manufacturing value-added between 1900 and 2000, for example, economists Francisco Buera and Joseph Kaboski found a “strong connection” between the two.20 The onset of COVID-19 in the United States again showed the link between consumer spending and manufacturing sector performance: U.S. manufacturers during the summer of 2020 outperformed domestic service providers because several factors—including “catch-up” purchases that were delayed in the spring; continued restrictions on many services; consumer unease about public exposure; and stimulus payments—had pushed homebound Americans to increase their relative consumption of goods over this period.21

Nor are the consumption and output trends limited to the United States or even other developed countries.22 Lawrence Edwards and Robert Lawrence found that the share of national spending on goods between 1970 and 2010 declined at a similar rate in Australia, Canada, Denmark, France, Italy, South Korea, the Netherlands, the United Kingdom, and the United States (though the United States had the lowest total share [34 percent] by 2010).23 As shown in Figure 5, advanced economies’ manufacturing-GDP shares followed suit.

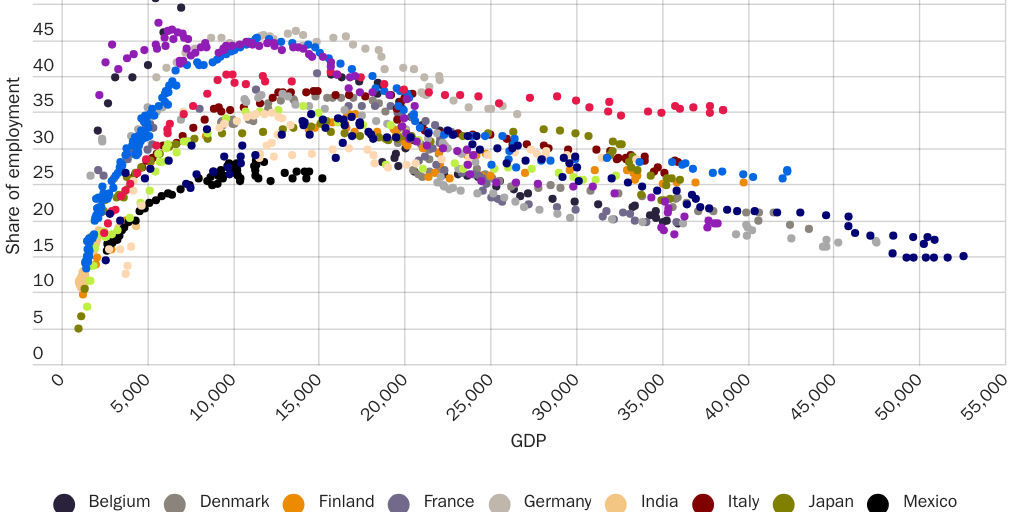

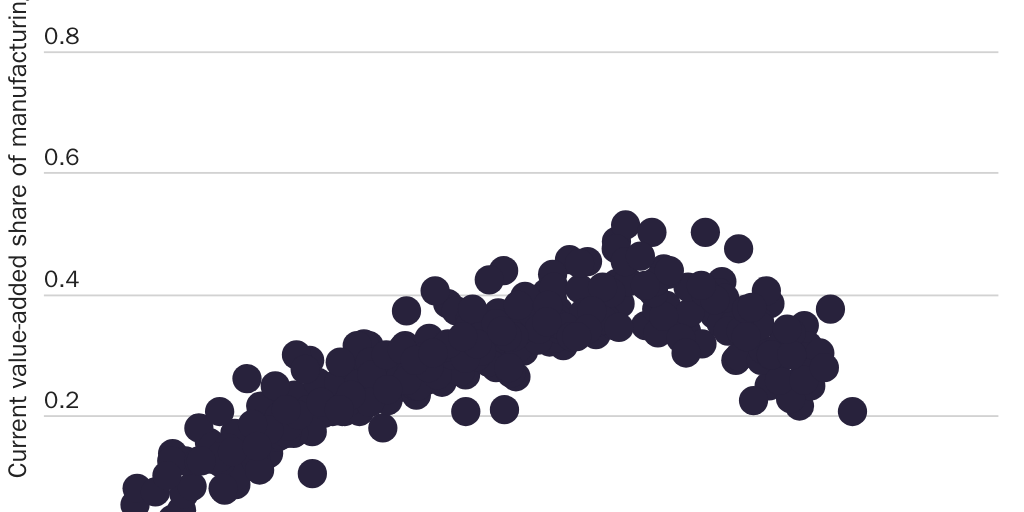

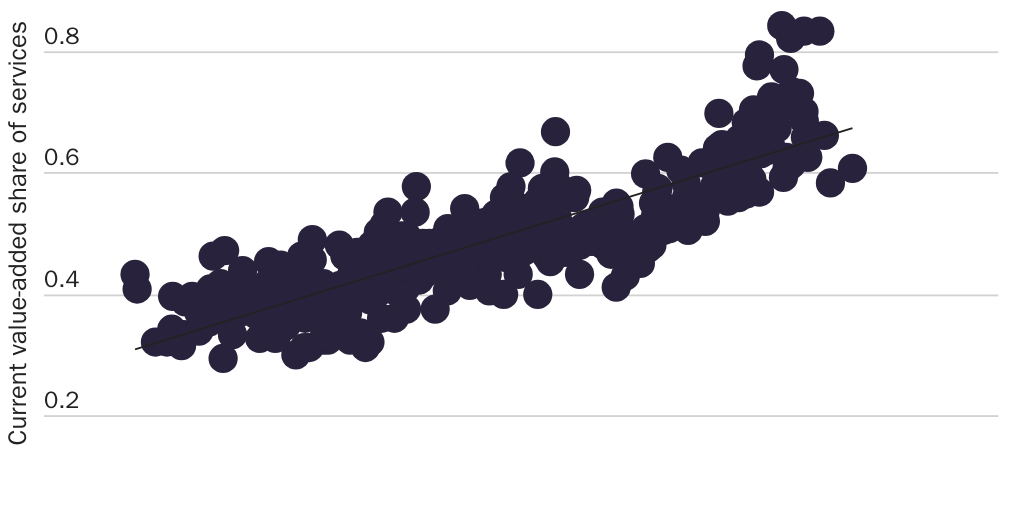

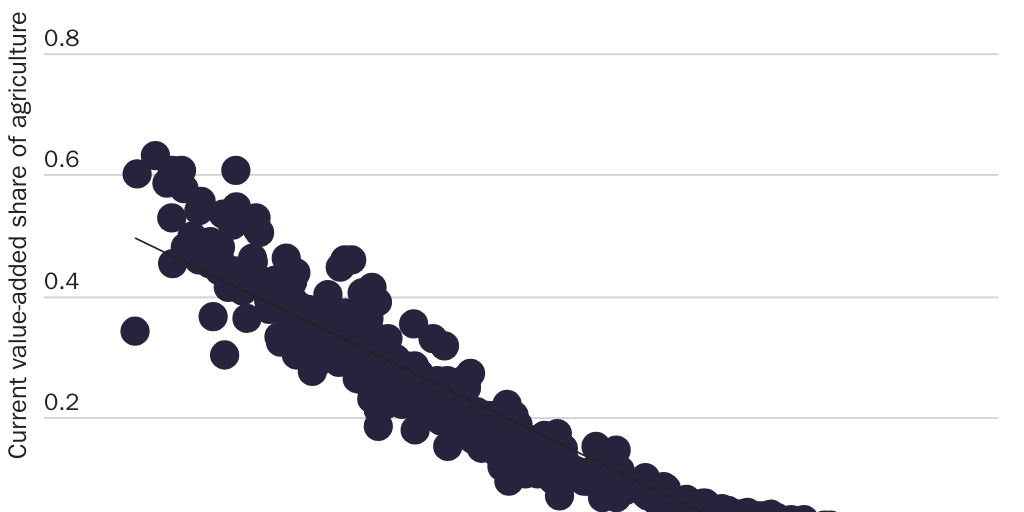

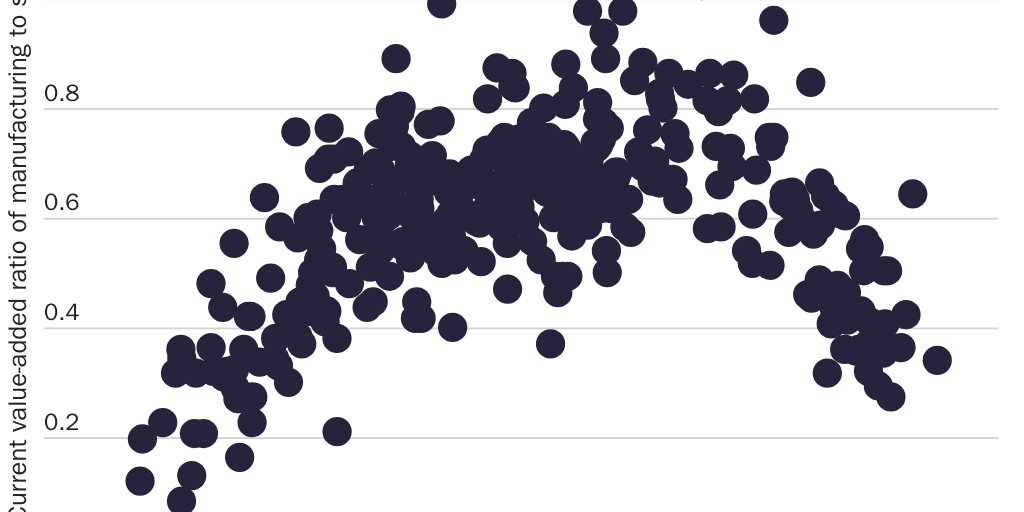

The declining role of manufacturing in a nation’s economy is a standard story of economic development, not cause for alarm or criticism of national economic policy. As shown in Buera and Kaboski’s 2012 examination of 31 countries representing 68 percent of world population and 80 percent of 2000 GDP (reproduced in Figures 6a, 6b, 6c, and 7), both the manufacturing sector’s share of total value-added (Figure 6a) and its relationship to services value-added (see Figure 7) follow the same inverted‑U pattern (increasing then decreasing) as every nation develops.24 Each country’s experience with services (see Figure 6b) and agriculture (see Figure 6c) is also similar to those of other countries.

In sum, both the manufacturing employment and GDP-share trends occurring in the United States reflect macroeconomic forces affecting most industrialized countries around the world in the same way and thus cannot be a proxy for the state of the U.S. manufacturing sector or an indicator of the success or failure of previous U.S. policy.

U.S. Productive Capacity Remains High Both Overall and in Security-Related Industries

Furthermore, employment and GDP share trends say little about the nation’s “industrial capabilities” (i.e., its ability to produce the goods that the country needs in times of war or other national emergencies), which along with access to similar capabilities abroad is what the U.S. Department of Defense (DOD) considers critical for national security.25 By this metric, the United States shows little weakness. Despite popular claims that the United States has suffered a broad decline in productive capacity, the U.S. manufacturing sector actually remains among the most productive in the world and has expanded since the 1990s—continuing earlier period trends in output, investment, and profitability that the Cato Institute’s Daniel Ikenson documented in 2007.26 Also, the manufacturing industries most closely associated with “national security” (e.g., metals, transportation, defense, computers and electronics, pharmaceuticals, and medical goods) have prospered.

The United States Remains a Global Manufacturing Leader. Comparisons of U.S. manufacturing with other countries’ sectors (see Table 2) show that the United States continues to be at or near the top of most categories, including output, exports, and investment.

As shown in Table 2, the United States in 2018 ranked second in the world in total real manufacturing value-added and merchandise exports. The United States ranked third globally for exports of “manufactures”; however, this category excludes important U.S. manufactured goods such as fuels and certain foods, and European Union (EU) bloc and country numbers are inflated because they include intra-EU trade (e.g., German exports to France).27 The U.S. manufacturing sector’s performance is also strong on a per capita or per manufacturing worker basis, outperforming China and several other top manufacturing countries. Among Organisation for Economic Co-operation and Development nations, moreover, the United States is the top recipient of manufacturing foreign direct investment (FDI)—more than doubling the second-place nation. In 2018, FDI inflows into the U.S. manufacturing sector alone (almost $167 billion) were larger than total FDI inflows into China for the same year ($138 billion). Inward FDI stocks in the U.S. manufacturing sector reached $1.77 trillion that same year.28

In short, the United States remains a major global manufacturer and a top destination for manufacturing investment.

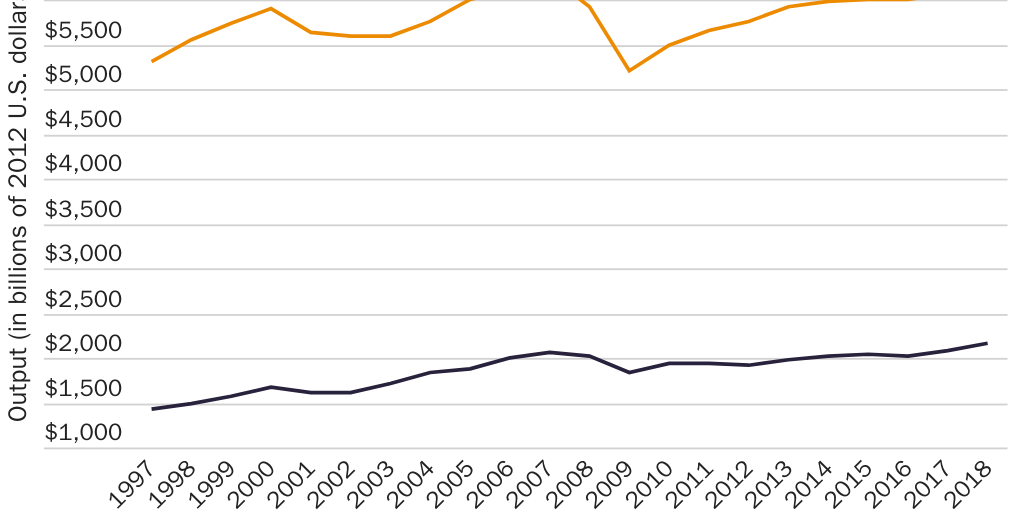

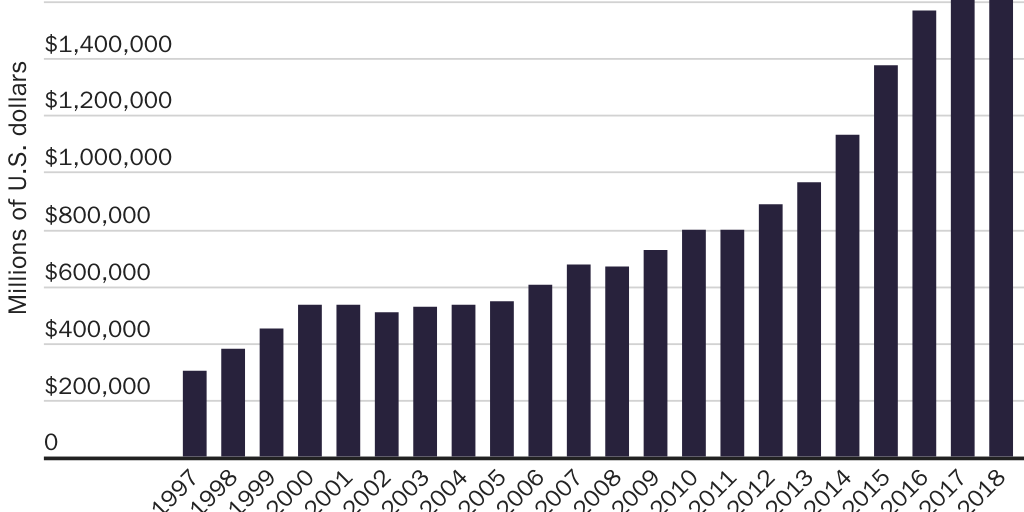

The United States’ Industrial Capabilities Keep Expanding. Second, historical data on the U.S. manufacturing sector show it to be growing. As shown in Figure 8, real (inflation-adjusted) U.S. manufacturing value-added and gross output were up significantly between 1997 and 2018.

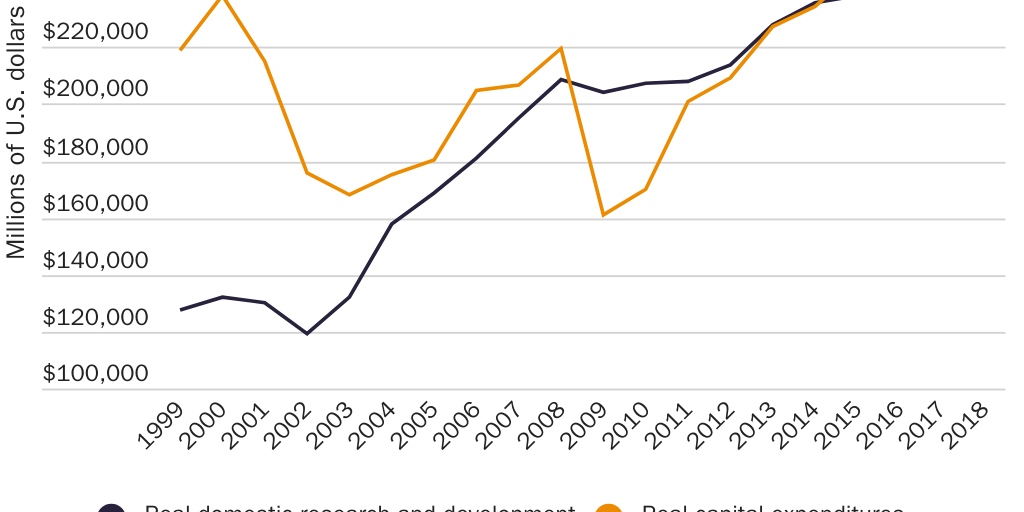

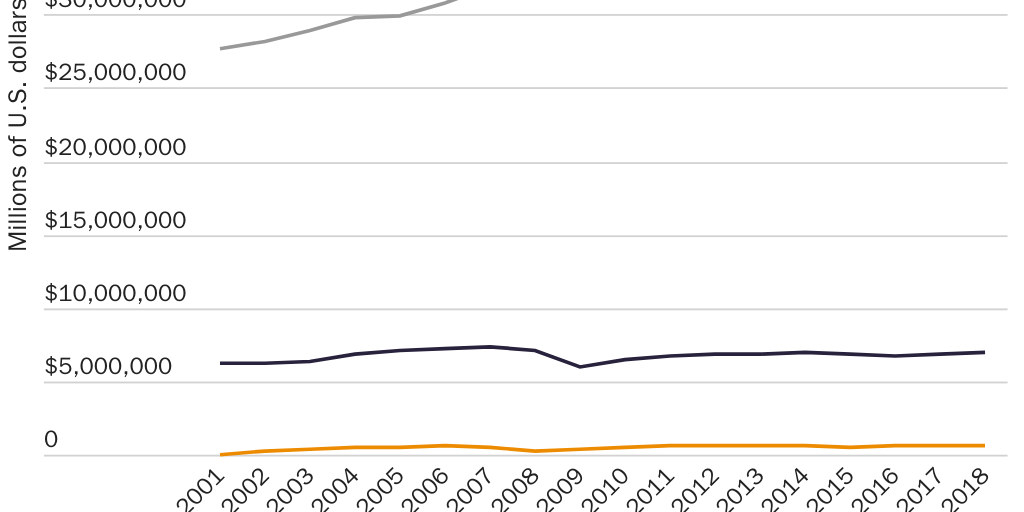

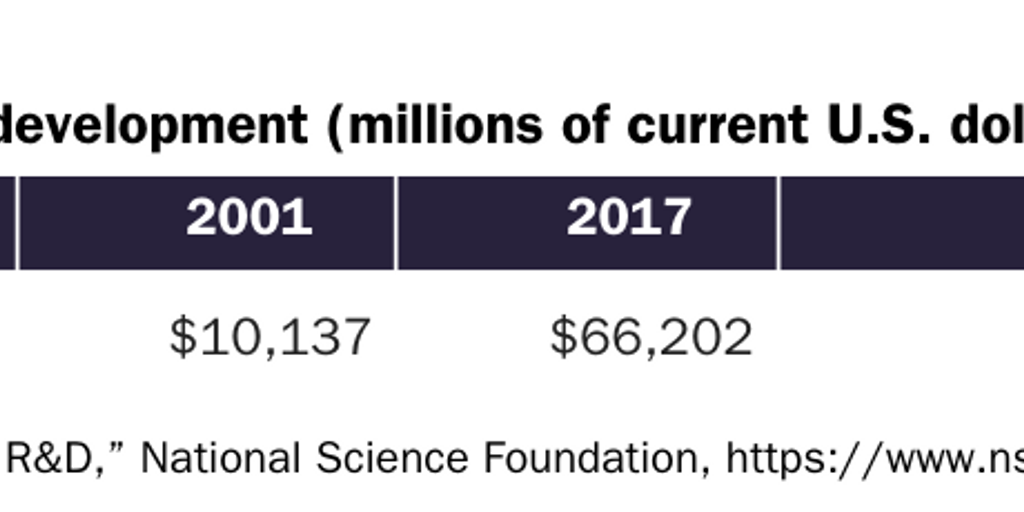

Furthermore, investment in the manufacturing sector—capital expenditures, research and development (R&D), and FDI—has been consistent and strong. (See Figures 9 and 10.) Finally, as shown in Figure 11, the sector has also experienced improved financial performance since 2001 (the first year of data available), with inflation-adjusted gains in revenues, post-tax income, and assets.

Based on these and other data, the last two DOD reports on the U.S. defense industrial base concluded that it is “profitable and expanding” overall. In fact, the latest report for fiscal year 2019 (issued June 23, 2020) states that the largest six prime defense suppliers (Lockheed Martin, Boeing, Northrop Grumman, Raytheon, General Dynamics, and BAE Systems) “are financially healthy and continue to expand in market share” and that their “investments hit a six year high in 2018 at $33.9 billion with firms investing largely in acquisition of subsidiaries, R&D, and capital expenditures.“29

A longer-term view of these data is essential to evaluating the sector’s performance. Some of the more negative analyses of U.S. manufacturing provide an incomplete view because they fail to account for either the Great Recession, which collapsed global output and employment, or the manufacturing “mini-recession” in 2015–16, caused by an unexpected collapse in global oil prices—issues clarified by updating the data through 2018 (when U.S. trade conflicts halted the sector’s improvement).30 Indeed, the problems with taking a narrow snapshot are revealed by examining employment trends in the United States and other top manufacturing countries between 2010 and 2018. These data show that the United States (1.1 percent annual growth; 956,000 jobs gained) has had stronger employment growth than Germany (1.0 percent; 440,000 jobs), Japan (–0.4 percent; –229,000 jobs), and China (–0.5 percent; –9.5 million jobs).31 Just as it would be inappropriate to claim that this single datapoint captures the true state of these diverse, multitrillion dollar manufacturing sectors (or the national policies affecting them), so does using other short-term snapshots to argue the same.32

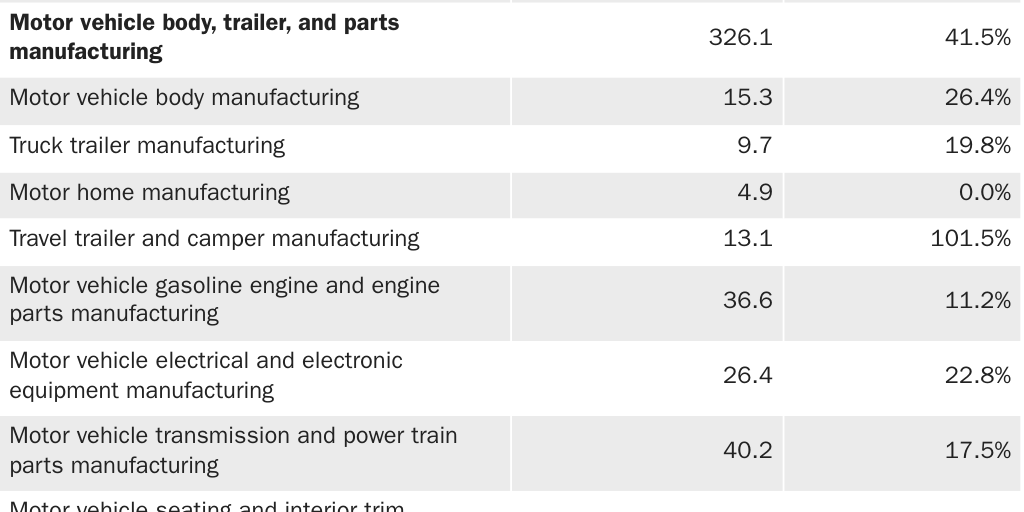

The topline data do, however, hide significant changes in the manufacturing sector over the past two decades in response to various economic forces. Some industries have indeed contracted since the 1990s, but often these changes reflect fundamental shifts in U.S. and global markets as opposed to a weak manufacturing sector. They are also often offset by gains in other, related industries. For example, as shown in Table 3, automobile manufacturing output dropped by almost 60 percent between 1997 and 2018, but light truck and SUV production grew by 175 percent over the same period.

This shift speaks to evolving U.S. consumer tastes (away from cars to SUVs) instead of American “deindustrialization” (though offshoring of some car production, especially to Mexico, has occurred). Furthermore, the high U.S. tariff on light trucks cannot explain increased U.S. SUV production, as only two-door SUVs are covered by the tariff. (The tariff also does not apply to imports from certain U.S. trade agreement partners.)33

These and other U.S. manufacturing data (see the Annex) also reveal a flexible and dynamic sector that is generally responsive to market forces—a flexibility that can prove critical in times of unexpected national emergency. For example, high demand for hand sanitizer, cleaning products, and face masks in the wake of COVID-19 caused small and large manufacturers across the country to retool their operations and thereby meet Americans’ essential material needs.34 This rapid transition is a testament to not only the hard work and ingenuity of U.S. retailers and manufacturers but also the United States’ economic dynamism and industrial capabilities more broadly.

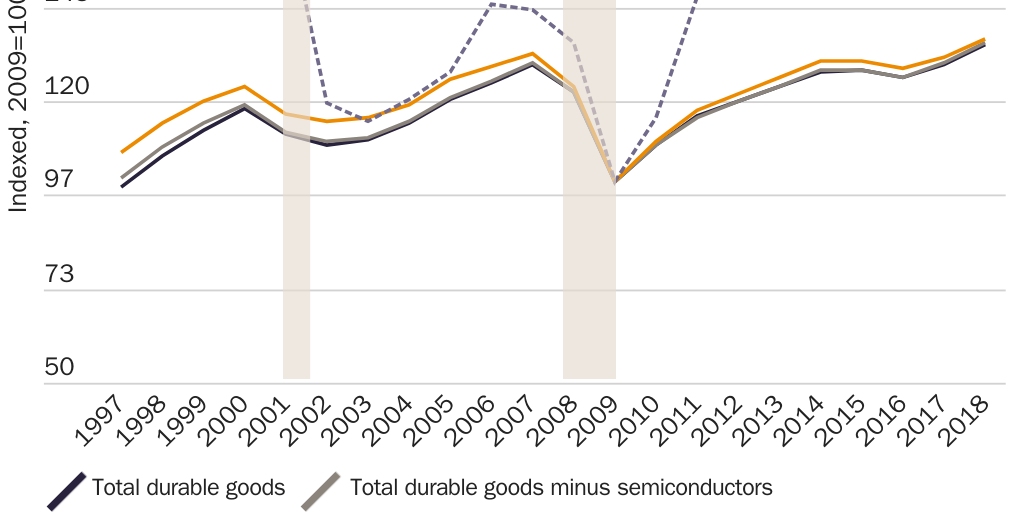

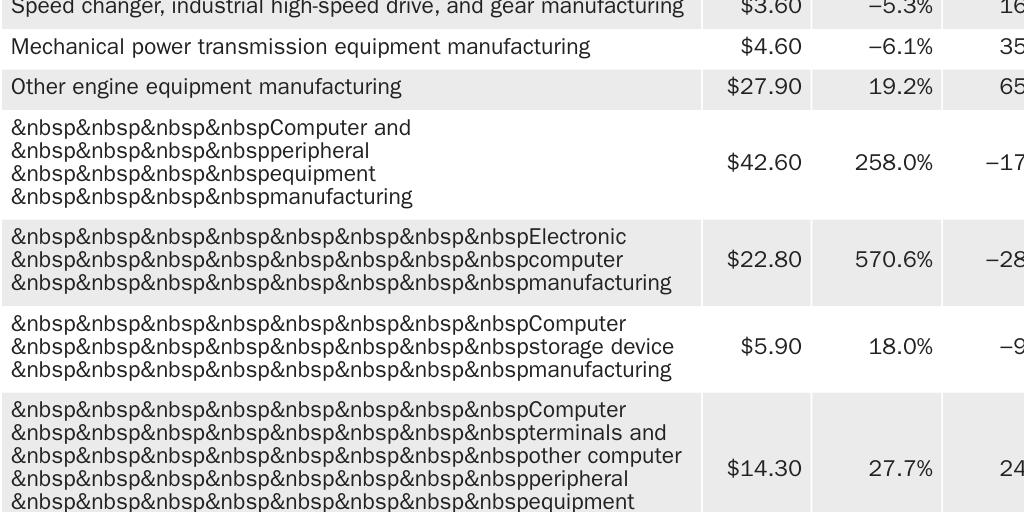

Industry-Specific Data Reveal Strength Where It Counts. Detailed breakdowns of U.S. manufacturing data also show a stark divide between durable goods (i.e., the goods such as metals, planes, and machinery that we most commonly associate with “national security”) and nondurable goods (e.g., food and textiles). In particular, U.S. durable goods production (real gross output and real value-added) has increased significantly—by 35.9 percent and 109 percent, respectively—since 1997 (see Figure 12), while nondurable goods output has sagged (see Table 4). The durable-goods gains are not, as some have claimed, merely the result of adjustments for increases in computing power.35 Excluding the entire computers and electronics industry (including semiconductors), U.S. durable goods’ real gross output and real value-added still increased by more than 26 percent and 60 percent, respectively, since 1997 and, excluding only semiconductors, 109.1 percent and 35 percent.

Eliminating these thriving sectors, of course, overcompensates for any technical adjustment issues, as U.S. computer, electronics, and semiconductor firms undoubtedly produce important and globally competitive products and employ hundreds of thousands of American workers. Doing so also raises questions about what other sectors may need to be discounted or excluded when evaluating the “true” state of the nation’s overall productive capacity. For example, should we also exclude the data for the paper and printing, tobacco, and magnetic and optical media (e.g., cassette tapes and CDs) industries—which have declined due to fundamental market changes and are thus unrelated to any “deindustrialization” concerns? Eliminating these industries would reveal even more impressive manufacturing sector gains since the late 1990s.

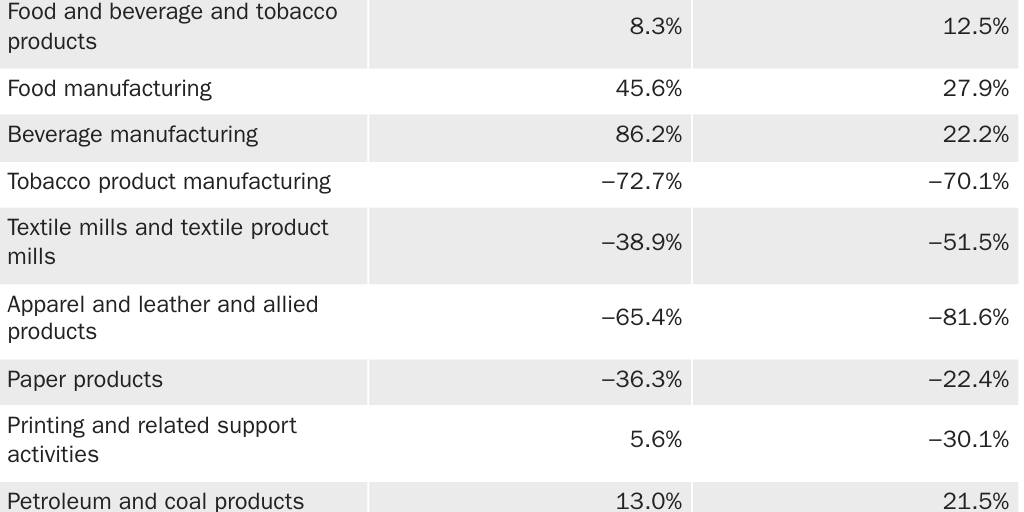

As shown in Table 4, moreover, declines in nondurable goods production have been driven by basic, low-margin consumables such as textiles and apparel; by tobacco; or by “dematerialized” goods such as paper—not other nondurables such as chemicals (including pharmaceuticals) and energy that might have a national security nexus.36 Remove the aforementioned decliners, and nondurable goods’ real value-added and gross output increase by 22.9 percent and 10.3 percent, respectively, between 1997 and 2018.

By contrast, the industries that are most closely tied to national security—including those now prioritized due to COVID-19—have not experienced significant historical declines and in most cases have expanded. (See Table 5.) This category includes the goods directly involved in national defense (e.g., tanks, missiles, and munitions), as well as those indirectly related, including metals, computer and electronic products (including or excluding semiconductors), motor vehicles, aerospace products, ships medical equipment, energy, chemicals, and pharmaceuticals. Although certain sub-industries’ output has risen and fallen over different periods (to be expected given business cycles, changing U.S. military operations, and other factors), the overall picture is one of stability and health, not decline.

These data also refute a common myth that industries unrelated to national security have driven gains in U.S. manufacturing output—the well-worn “we make potato chips, not microchips” argument. They also underscore why tying U.S. national security to trends in manufacturing employment or GDP share is so misguided.

Industry-level analyses corroborate these data in the two industries—semiconductors and medical goods—that Washington policymakers are now targeting for security-related support.

Semiconductors. Shortly before the end of the 116th Congress, both chambers approved by wide margins the National Defense Authorization Act for Fiscal Year 2021 (NDAA), which includes billions of dollars in federal support for the construction of domestic semiconductor manufacturing facilities and an R&D consortium. According to the Bureau of Economic Analysis (BEA), however, U.S. “semiconductor and other electronic compo-

nent manufacturing” production reached $113.4 billion in real gross output and $88 billion in real value-added in 2018.37 Real gross output for “semiconductor and related device manufacturing” alone reached $64.9 billion (more detailed value-added data are not available). The Semiconductor Industry of America (SIA) further notes that there are commercial semiconductor manufacturing facilities in 18 states, employing more than 240,000 Americans, and that the United States has 12.5 percent of global semiconductor manufacturing capacity.38 Furthermore, the largest share (44.3 percent) of U.S. companies’ production occurs in the United States (while only 5.6 percent is in China, whose alleged dominance was the stated justification for the subsidies).

The United States is also a top-five global exporter of semiconductors and related equipment, shipping almost $47 billion of those goods in 2019.39 These and other data led the SIA to conclude in its 2020 State of the U.S. Semiconductor Industry report that “the semiconductor manufacturing base in the United States remains on solid footing.“40

The SIA also reports that the U.S. industry has “nearly half” of all global semiconductor sales—a market share that has been steady (ranging from the mid-40s to low 50s) since the late 1990s—and is the top seller in every major regional market, including China. Sales by U.S. semiconductor firms also grew from $76.7 billion in 1999 to $192.8 billion in 2019—a compound annual growth rate of almost 5 percent.

Beyond output and sales, the U.S. semiconductor industry has been a global leader in capital spending (capex) and R&D. The SIA notes that total R&D and capex by U.S. semiconductor firms, including “fabless” companies that specialize in R&D but outsource actual chip manufacturing, was $71.7 billion in 2019, growing steadily between 1999 and 2019 at a 6.2 percent annual rate. R&D expenditures hit $39.8 billion last year, constituting 16.4 percent of the industry’s total sales last year—an “R&D intensity” second only to pharmaceuticals in the United States and the highest of any semiconductor industry in the world. Capex has been similarly world-class: SIA reports that 2018 capital expenditures reached “an all-time high of $32.7 billion” and constituted 12.5 percent of sales in 2019, with only South Korea having a larger global share of semiconductor capex that year.

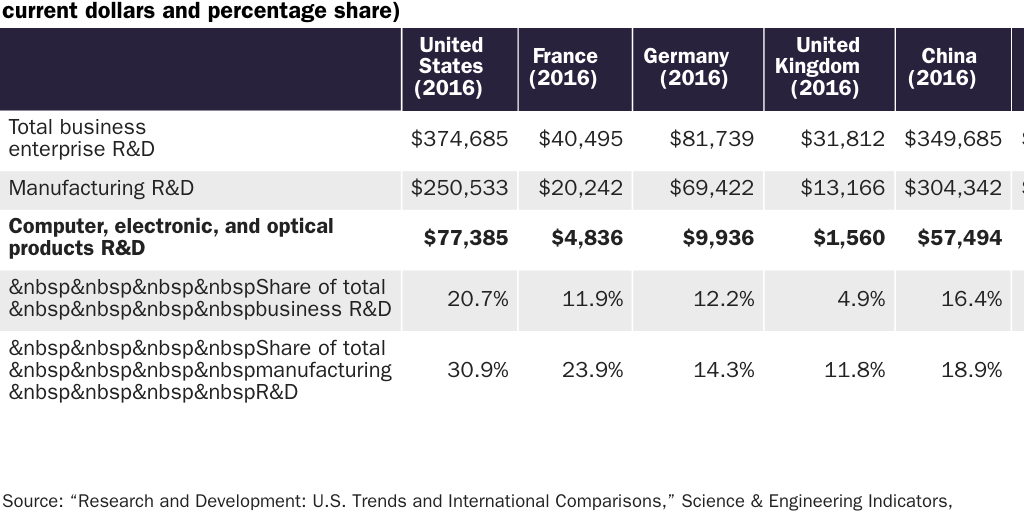

Other data corroborate these findings. (See Table 6.) According to the U.S. National Science Board’s 2020 report on R&D trends, U.S. computer and electronic (including semiconductor) companies spent more on R&D in 2016 (the last year available) than any other country surveyed—often many times more—with only South Korea’s sector having a greater share of total or manufacturing R&D than the United States.41

The BEA further calculates that foreign multinational corporations in 2017 spent $7.3 billion and $2.2 billion on R&D and capex, respectively, for their U.S. affiliates in the “semiconductors and other electronic components” sector, up from $4.4 billion and $1.9 billion in 2007.42 U.S. semiconductor companies’ stock prices also have climbed steadily over the past decade.43

As a result of this investment, the SIA notes that in 2019 the United States remained at or near the “leading edge” of current semiconductor technology. Although U.S.-based Intel announced delays to its 7 nm chip production (reportedly competitive with the 5 nm chips from Taiwan’s TSMC), Intel also remained financially healthy as of July 2020: “Even with $15 billion projected for capital expenditures this year, on a non-GAAP basis, Intel is looking at free cash flow of $17.5 billion.“44

In short, the U.S. semiconductor industry is profitable and expanding—in many ways still globally dominant—and is investing billions of its own dollars to stay that way. None of this indicates a significant long-term “national security” threat—particularly not one that could be solved via subsidies for commercial fab construction (which takes years to complete).

Medical Goods (Non-Pharmaceutical). The U.S. medical goods industry is also large and productive.45 For example, a 2020 study from the St. Louis Federal Reserve of “essential medical equipment” (hand sanitizer, masks, personal protective equipment, ventilators, etc.) found that American producers supplied the vast majority (more than 70 percent) of these products in 2018.46 The World Trade Organization (WTO) further notes that the United States not only is a top global producer and importer of medical goods but also is a top exporter (second overall, right behind Germany).47

Data from the BEA on domestic production of medical equipment and supplies also show a healthy industry with expanding real output and value-added between 1997 and 2018. This includes the broader “medical equipment and supplies manufacturing” industry, which had $102 billion in gross output and $62 billion in value-added in 2018, and the two most important subcategories, “surgical and medical instrument manufacturing” ($45.9 billion) and “surgical appliance and supplies manufacturing” ($37.4 billion). Indeed, real output in the latter category—which contains ventilators, masks, and many other “essential” medical goods—increased by almost 90 percent over the period examined.48 Other categories, such as “analytical laboratory instrument manufacturing” (121.8 percent), “irradiation apparatus manufacturing” (468.0 percent), and “electromedical and electrotherapeutic apparatus manufacturing” (418.1 percent) also experienced substantial gains in real output.

The only domestic medical goods industry that has contracted is basic personal protective equipment (i.e., textiles, apparel, or paper products), but even there, the concern is overblown. For example, BEA data show that the domestic textile industry in 2018 generated approximately $54 billion and $17.6 billion in real gross output and value-added, respectively—significant increases (4.7 percent and 5.4 percent) since the end of the Great Recession. Also, the apparel and sanitary paper industries produced more than $10 billion in output in 2018. Many of these companies shifted operations to produce high-demand personal protective equipment (PPE) during the pandemic—another example of the U.S. manufacturing sector’s flexibility.49 Finally, foreign producers and domestic stockpiles can fill in remaining gaps in PPE supply, as they have done throughout the pandemic. These facts belie the need for costly new government policies to subsidize or protect new and inefficient PPE capacity in the United States.

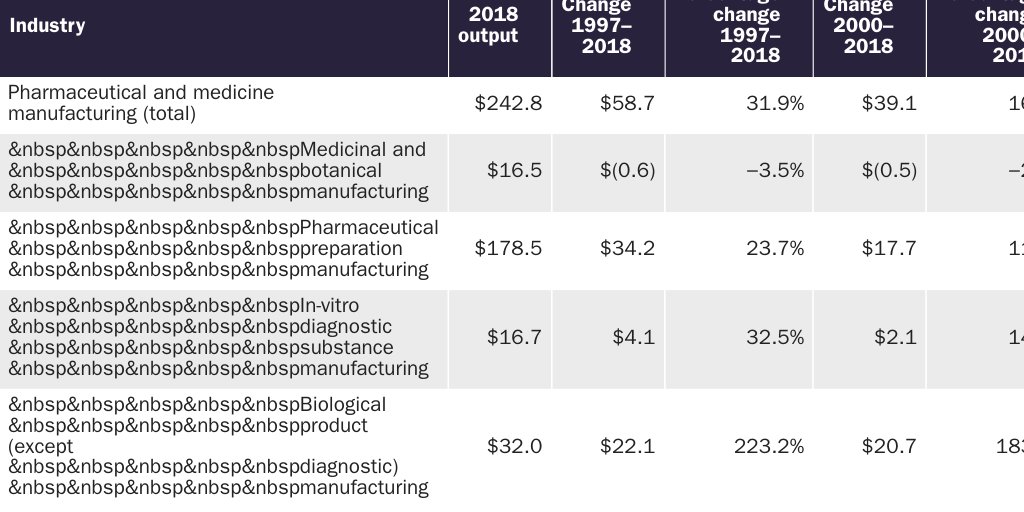

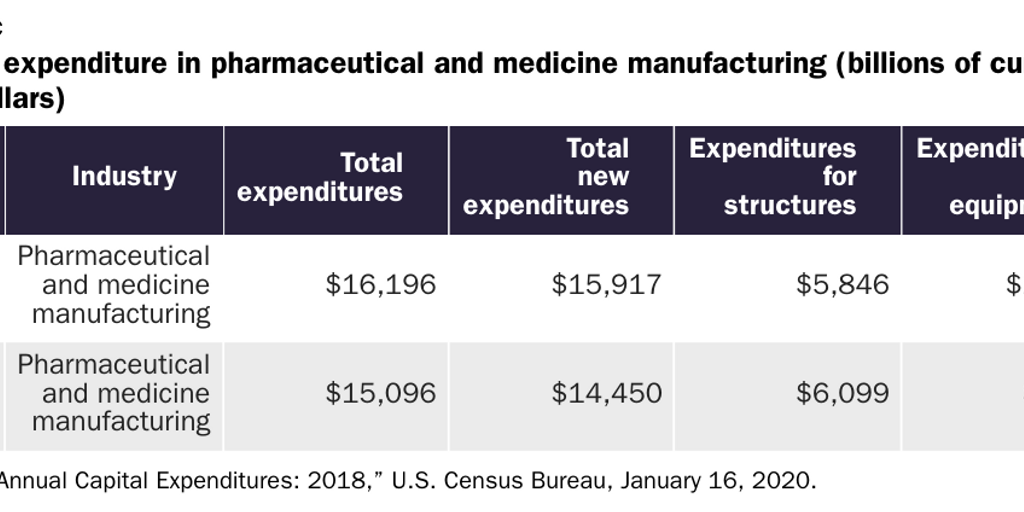

Pharmaceuticals. As shown in Tables 7a, 7b, and 7c, U.S. government data on output, R&D, and capital expenditures show that American pharmaceutical manufacturers have performed well in recent years.

A 2020 report from the McKinsey Global Institute notes that the United States is home to more than 500 pharmaceutical manufacturing facilities—among the highest concentrations in the world.50 The WTO adds that the United States is both a major importer and exporter of pharmaceutical products, having shipped almost $41 billion in medicines (35 percent of total U.S. medical goods exports) in 2019.51

With respect to pharmaceutical inputs (i.e., active pharmaceutical ingredients, or APIs), available public data on domestic and global API production do not indicate a need for urgent government funding (such as that proposed for Eastman Kodak Company). According to the Food and Drug Administration (FDA), of the roughly 2,000 global API manufacturing facilities, 13 percent are in China; 28 percent are in the United States; 26 percent are in the EU; and 18 percent are in India. For the APIs of World Health Organization “essential medicines” on the U.S. market, 21 percent of manufacturing facilities are located in the United States; 15 percent are in China; and the rest are in the EU, India, and Canada.52 The FDA further notes that the United States was home to 510 API facilities in 2019, 221 of which supply the aforementioned “essential medicines.“53

The “Defense Industrial Base” Already Enjoys Targeted Policy Support

“Security nationalism” also assumes a need for broad and novel U.S. government interventions while ignoring the current, targeted federal policies intended to support the defense industrial base. As documented in the Appendix, this includes policies intended to diversify potential sources of essential supplies beyond U.S. borders; to subsidize, procure, and stockpile domestically produced items deemed essential for national defense; or to protect domestic companies from import competition.

These laws, central to past DOD recommendations and actions to support the U.S. defense industrial base, are summarized as follows:

- International policies intended to support the defense industrial base: the “National Technology and Industrial Base” (NTIB), which includes Canada, the UK, and Australia and is intended to enhance national security by eliminating restrictions on trade and R&D collaboration among NTIB partner countries, thereby expanding the United States’ industrial capacity beyond U.S. borders; reciprocal defense procurement agreements between the DOD and its counterparts in 27 foreign governments, under which each country agrees to remove barriers to national security–related purchases of supplies and services of the other country;54 and “security of supply” arrangements with eight countries that “allow the DOD to request priority delivery for DOD contracts, subcontracts, or orders from companies in these countries.“55

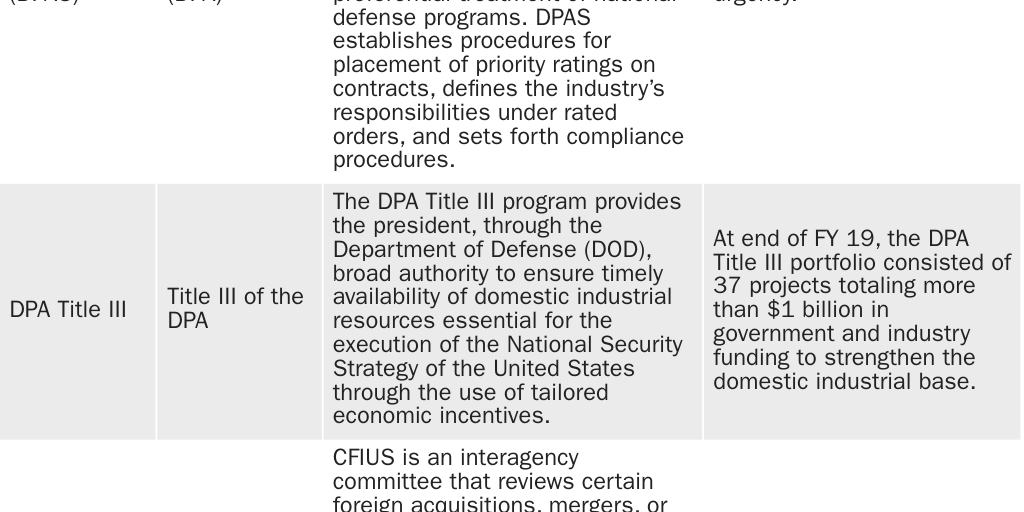

- Domestic laws intended to support the defense industrial base on express national security grounds, including: NTIB provisions that require the DOD to assess annually the defense industrial base (published in an annual industrial capabilities report) and to work to mitigate any potential concerns; the Defense Production Act of 1950, which allows the DOD to identify priority sectors for government contracting and enter into those contracts (Title I), and to support, through purchases or loans/loan guarantees, “essential” domestic industrial base capabilities that are found to be nonexistent, at risk of loss, or insufficient to meet government needs (Title III); numerous other programs (see the Appendix) providing the DOD with the authority and funding to support other parts of the industrial base; and the National Defense Stockpile Transaction Fund and Strategic and Critical Materials Stock Piling Act of 1939, which authorize the National Defense Stockpile Manager to fund R&D projects to develop new materials for the stockpile and require the president to encourage the development and conservation of domestic sources of “strategic and critical materials” through procurement.

- Laws intended to protect U.S. manufacturers via the imposition of restrictions on foreign imports, including: Section 232 of the Trade Expansion Act of 1962, which authorizes the executive branch to take action (e.g., through tariffs or quotas) against imports found to have been “imported into the United States in such quantities or under such circumstances as to threaten to impair the national security”;56 U.S. “trade remedy” laws, which allow for the imposition of antidumping or anti-subsidy duties on imports from specific countries that are found to have injured or threatened to injure the U.S. industry making a directly competitive product; and various “Buy American” laws, which require the federal government to purchase or contract for domestically produced industrial goods.

As explained in the Appendix and the following sections, many of these policies have proven to be ineffective, unused, or even counterproductive, and several reforms are proposed. Regardless, these measures’ mere existence rebuts the current caricature of a U.S. defense industrial base ravaged by free markets and government inattention. These policies also show that the federal government, particularly the DOD, has legal tools to address discrete and legitimate weaknesses in essential supply chains (e.g., for weapons). Also, the government’s implementation of some of these laws shows the weaknesses of security nationalism in practice.

“Security Nationalism” Makes the United States Less Secure

Because economic nationalist policies weaken the U.S. economy and manufacturing sector, the government should not pursue “security nationalism” to bolster national security.

Closed Markets Make Economies Less Secure

Protectionism often undermines national security by weakening a country’s economy and manufacturing sector, thus making it less resilient in the face of war or other shocks. Restrictions on international trade and investment not only reduce economic growth (and thus tax revenue) and output but also can distort the economy and divert resources from sectors (e.g., high-tech, high-productivity industries such as information technology) that are also essential to national security.

Decades of research bear this out. For example, International Monetary Fund (IMF) economists in 2018 examined data for 151 countries over 51 years (1963–2014) and found that “tariff increases lead, in the medium term, to economically and statistically significant declines in domestic output and productivity” as well as more unemployment and higher inequality.57 Numerous analyses of U.S. protectionism reveal that these policies impose economic harms that far outweigh possible short-term benefits, fail to protect American firms and workers over the longer term, and breed political dysfunction.58

Furthermore, protectionism’s harms are typically amplified for the U.S. manufacturing sector—the target of current security nationalist demands. The IMF paper, for example, found that increased tariffs on manufacturing inputs (e.g., steel) resulted in a statistically significant decline in manufacturing sector-wide output (6.4 percent) and productivity (3.9 percent) five years after the tariff hikes in question. These findings are particularly relevant for the United States, given the diversity and complexity of the domestic manufacturing sector; the consistently high percentage of manufacturing inputs as a share of total imports; the concentration of “trade remedy” (antidumping, countervailing duty, safeguard) duties on manufacturing inputs; and relatively new “national security” tariffs on almost all primary steel and aluminum imports into the United States.

Other papers have confirmed these harms. For example, a 2020 paper from Alessandro Barattieri and Matteo Cacciatore found that U.S. “trade remedy” duties were concentrated in a few upstream industries (base metals and metal products, chemicals, plastics, and rubber products) and therefore resulted in substantial employment losses for downstream manufacturing industries, along with modest and short-lived employment gains in the industries that won protection. The authors further determined that these downstream industries suffered because they lost competitiveness (and therefore jobs) after raising prices to cover higher input costs.59 Examinations of President Trump’s “national security” tariffs on steel and aluminum found that the measures’ costs were mostly borne by domestic manufacturers that consume these metals—including in industries most closely associated with national security (e.g., transportation and weapons)—and resulted in foreign retaliation against U.S. goods exports. As a result, the import protection harmed these firms in terms of increased costs and reduced output, jobs, exports, and investment.60

Finally, extensive literature ties trade openness to improved economic performance more broadly. A 2018 paper from Robert Feenstra summarized the studies on the long-run, overall gains from trade for the United States, calculating total average GDP gains of 1.1 percent per year due to increased product variety arising from imports, the productivity-enhancing effects of trade-induced creative destruction, and pro-competitive effects on domestic prices.61 A 2017 Peterson Institute for International Economics paper calculated the payoff to the United States from expanded trade between 1950 and 2016 to be $2.1 trillion, increasing U.S. GDP per capita and per household by $7,000 and $18,000, respectively.62 The U.S. International Trade Commission (ITC) found in 2016 that U.S. trade agreements produced small but significant gains in U.S. exports, real GDP, employment, and wages and saved American consumers $13.4 billion in 2014.63 Several other papers have found similar gains.64

Overall, the evidence and analysis refute current arguments that economic nationalism would bolster the U.S. defense industrial base (and thus national security). Instead, American protectionism has been repeatedly found to weaken the U.S. manufacturing sector and the economy more broadly.

“Security Nationalism” Fails in Practice

Regardless of the theory supporting “security nationalism,” the United States’ implementation of these policies—for steel, ships, machine tools, semiconductors, and other “essential” goods—reveals a long track record of costs, risks, failed objectives, and unintended consequences. This checkered history must be considered when evaluating new proposals to support certain industries on national security grounds.

Section 232 Tariffs on Steel. President Trump’s tariffs on steel imports under Section 232 is a powerful example of the perils of American security nationalism. Prior to the tariffs’ imposition, the U.S. steel industry had already won billions of dollars in government subsidies and import protection through dozens of U.S. trade remedy measures covering almost 61 percent of all steel product imports in 2017, the year before the Section 232 tariffs took effect.65 Public data for that same year also showed that the industry was at no risk of collapse: according to the Commerce Department’s Section 232 report, for example, annual U.S. steel output (around 80 million metric tons) and production capacity (around 115 million metric tons) were steady between 1998 and 2016, and the domestic industry’s U.S. market share remained dominant at around 70 percent between 2011 and 2016.66 Furthermore, in the months leading up to the Section 232 investigation, domestic crude steel output and shipments of steel mill products also remained stable;67 five of the six largest domestic steelmakers were profitable, posting a combined net income of $491 million in the first quarter of 2017; and Standard and Poor’s credit ratings showed eight major U.S. producers to be financially viable.68 This was not an industry in crisis.

Nor did imports pose an immediate threat to the United States’ ability to procure steel (and aluminum) for national defense needs, as judged by the same standards that the Commerce Department applied in a 2001 Section 232 investigation that concluded that imports of iron and steel did not pose a national security threat.69 As previously noted, imports constituted less than one-third of all domestic steel consumption, and the majority of those steel imports came from “reliable” (in Commerce Department parlance) U.S. allies, such as Canada (the largest source country), Brazil (2), South Korea (3), Mexico (4), Japan (7), and various EU countries, including Germany (8), the Netherlands (13), Italy (14), Spain (16), and the UK (17). As the Commerce Department noted in 2001, none of these countries—most of which were U.S. treaty, free trade agreement, and/or defense procurement agreement partners and home to companies with major U.S. investments—would realistically deny the United States steel in a time of war or other emergency:

The Department found that iron ore and semi-finished steel are imported from reliable foreign sources. Accordingly, even if the United States were dependent on imports of iron ore and semi-finished steel, imports would not threaten to impair national security.…

Imports of iron ore and semi-finished steel come from diverse and reliable trading partners. More than a dozen countries exported iron ore to the United States in 2000; many of these countries are in the Western Hemisphere. Over the past ten years, Canada—with which the United States shares a 3,987-mile border—has been the source of more than 50 percent of U.S. iron ore imports. Canada is a North Atlantic Treaty Organization (“NATO”) ally, the United States’ largest trading partner, and also a party to NAFTA.70

Meanwhile, China—the repeated excuse for the Section 232 tariffs—was only the 11th largest U.S. supplier of steel in 2017, suffering a 31 percent drop since 2011 (due in part to the dozens of U.S. trade remedy measures).71

The absence of a national security threat in 2017 was established in a statutorily required assessment from then-Secretary of Defense James Mattis that agreed with the Commerce Department that the “systematic use of unfair trade practices … poses a risk to our national security” but explained that because “the U.S. military requirements for steel and aluminum each only represent about three percent of U.S. production … DoD does not believe that the findings in the [Commerce Section 232] reports impact the ability of DoD programs to acquire the steel … necessary to meet national defense requirements.” For this reason, Mattis recommended only “targeted tariffs” focused on “correcting Chinese overproduction and countering their attempts to circumvent existing antidumping tariffs” instead of “a global quota or global tariff,” as well as a dialogue with “key allies” to emphasize the United States’ commitment to these countries’ “bilateral U.S. relationship.“72

Mattis’ recommendations—as well as the Commerce Department’s findings and standards in the 2001 Section 232 investigation—were ignored. Instead, President Trump, surrounded by U.S. steel company chief executive officers and union leaders at a March 2018 White House press event, announced blanket 25 percent tariffs—inexplicably 1 percentage point higher than what the Commerce Department recommended—on all types of steel.73 This included commodity products (e.g., rebar) with little national security nexus and semifinished products (e.g., slab) that American steel companies needed to maintain their domestic operations. It also included steel from close U.S. allies such as Canada, Japan, and the EU (including the UK).74

Numerous studies have documented the tariffs’ high economic costs for U.S. consumers (particularly manufacturing firms). In particular, the tariffs caused higher steel prices that in turn hurt other U.S. manufacturers in terms of higher input costs, lower exports, and lost competitiveness at home and abroad; created an opaque, costly, and uncertain “exclusion” bureaucracy, under which more than 100,000 requests have been filed by U.S. manufacturers seeking relief; resulted in approximately 75,000 fewer manufacturing jobs than would have otherwise existed in the absence of the tariffs; depressed global demand for steel (thereby dampening prices); bred global market uncertainty, which hurt investment in manufacturing; and caused numerous U.S. trading partners to retaliate against American exporters.75

At the same time, the steel tariffs were found to have a minimal impact on U.S. steelworker jobs and to do nothing to address global steel overcapacity—the primary long-term driver of the U.S. steel industry’s weakened financial position in 2018.76 Given these and other market dynamics (e.g., steelmakers bringing back inefficient capacity to capture rents and subsequently flooding the U.S. market), industry stocks tanked in late 2018 and early 2019, and steel companies were actually laying off workers and curtailing investments by the end of 2019.77 In extending the tariffs to downstream “derivative” products in early 2020, the Trump administration tacitly admitted that the steel tariffs had not achieved their primary goal of increasing and stabilizing the industry’s capacity utilization.78 As one Los Angeles Times story put it, “Trump’s steel tariffs were supposed to save the industry. They made things worse.“79

Finally, the president’s baseless invocation of “national security” in this (and other) Section 232 cases has likely harmed U.S. national security in other important ways, including by antagonizing allies and thereby undermining U.S. credibility and complicating efforts to build international coalitions on other, more legitimate security threats (e.g., China); eroding the rule of law in the United States via the clear abuse of constitutional trade powers delegated to the executive branch by Congress; and undermining U.S. leadership at the WTO by exploiting the body’s rarely invoked exceptions for the protection of “essential security interests.”

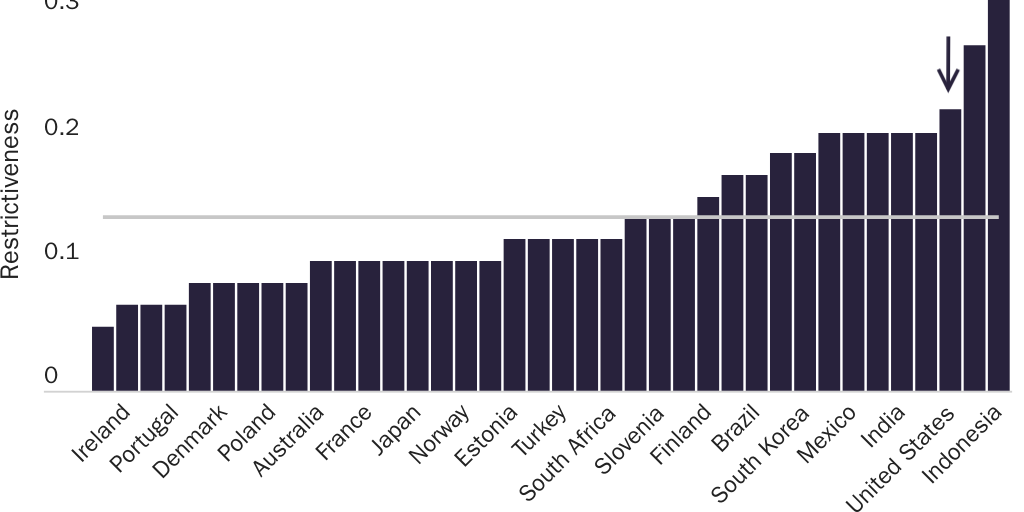

The Jones Act. The Merchant Marine Act of 1920 was presented as a plan to ensure adequate domestic shipbuilding capacity and a ready supply of merchant mariners in times of war or other national emergencies. Section 27 of the law—the “Jones Act”—purportedly supports those objectives by restricting domestic shipping services to vessels that are U.S.-built, U.S.-owned, U.S.-flagged, and U.S.-staffed. As a result, the United States has one of the most (if not the most80) restrictive shipping systems in the world, as shown in Figure 13.

A century of evidence—summarized in a 2018 Cato Institute policy analysis81—reveals that the Jones Act has failed in its main national security objectives while imposing substantial economic costs. First, Jones Act restrictions inflated U.S. shipping costs because the transport of cargo between U.S. ports and on inland waterways is off-limits to foreign competition. Higher shipping rates for waterborne transportation reduced demand for shipping services, thereby leading U.S. companies to purchase fewer vessels. Producers, in turn, build fewer ships, thus retarding both output (ships) and production facilities (shipyards).

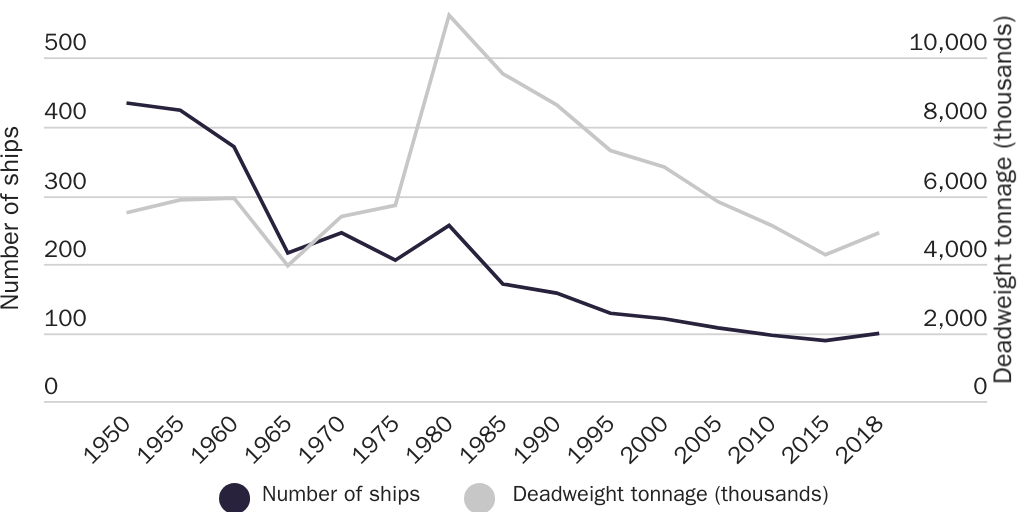

The trends shown in Figure 14 are especially bleak for oceangoing vessels (i.e., the ships that the U.S. military would need in wartime):

Nearly 9 of every 10 commercial vessels produced in U.S. shipyards since 2010 have been barges or tugboats. Among oceangoing ships of at least 1,000 gross tons that transport cargo and meet Jones Act requirements, their numbers have declined from 193 to 99 since 2000, and only 78 of those 99 can be deemed militarily useful. Even in their expressions of support for the Jones Act, government officials concede that the U.S. shipping industry and its associated ecosystem have been depleted.82

The Jones Act fleet is not only shrinking but also increasingly decrepit because of artificially high replacement costs. Of the mere 98 ships in service, more than a third (34.7 percent) are past the age of 20, and a quarter of them (24.5 percent) are past 30. Studies also show that these old vessels are not only inefficient but dangerous.

With fewer (and older) ships, fewer shipyards, and fewer workers in the industry, the Jones Act has undoubtedly failed to achieve its national security objectives—a conclusion evident by the fact that the U.S. military during the Gulf War and thereafter rarely turned to the Jones Act fleet (and overwhelmingly relied on foreign-built ships) to meet its sealift needs.83

Second, higher shipping costs caused by the Jones Act increase demand for alternative forms of transportation, including trucking, rail, and pipeline services, raising those modes’ rates and inflating business costs throughout the supply chain—thus affecting the operations and finances of nearly every business in nearly every U.S. industry, especially manufacturing. The Jones Act therefore disadvantages U.S. companies relative to their foreign competitors and consumes funds that U.S. households could spend or invest elsewhere in the economy (on more productive ventures). Indeed, some of those competitors, such as Russian gas producers that service Northeastern U.S. communities due to the artificially high cost of shipping liquified natural gas from Texas and Louisiana, are in hostile territories—another unintended consequence that undermines national security.

At the same time, heightened use of trucks and freight trains increases infrastructure and maintenance costs, as well as environmental costs (surface transportation emits more carbon than ships). It also raises safety issues (e.g., transporting toxic materials on U.S. highways) and increases traffic congestion—especially on highways running parallel to U.S. sea lanes—thereby generating opportunity costs from lost wages and lost output for American commuters. Finally, the Jones Act has been a persistent irritant to important U.S. trade partners, thus discouraging U.S. exports in those markets. These economic harms further undermine, rather than support, U.S. national security.

Machine Tool “Voluntary” Restraint Agreements, Subsidies, and Buy American Restrictions. Following a 1983 petition from the domestic machine tool industry under Section 232 and an affirmative “national security” determination by the Commerce Department in 1984, the Reagan administration concluded in 1986 five-year “voluntary restraint agreements” (VRAs) with Japan and Taiwan to limit their exports of certain machine tools and requested that nine other countries limit their U.S. machine tool market shares to certain levels. The federal government—led by the Commerce Department and the DOD—simultaneously implemented a “Domestic Action Plan” to “assist, encourage, and fund a variety of research and development activities to help modernize machine tool and manufacturing technology.“84 This included the creation of the National Center for Manufacturing Sciences (NCMS), a public-private consortium intended to “revitalize” the machine tool industry. Finally, Congress in 1986 and 1988 imposed Buy American restrictions on the DOD’s procurement of foreign-made machine tools.85 The VRAs were modified in 1991 and extended through December 1993, when they expired. The NCMS still exists, though it has been expanded to cover all manufacturing operations in North America (as opposed to just U.S. machine tools producers).

These trade restrictions and subsidies proved unsuccessful. First, the VRAs cost U.S. machine tool consumers (i.e., other U.S. manufacturers) hundreds of millions of dollars per year but provided much smaller benefits to U.S. producers, resulting in an estimated annual net loss of $647,892 (in 2017 dollars) per job protected.86 Among the measures’ victims was one of the United States’ largest machine tool producers, Hurco, which sourced certain hardware from Taiwan and survived because it won an exemption from the government through 1990.87 The trade measures also failed to reverse import growth (which expanded by 2.51 percent per year between 1986 and 1990) or domestic job losses (which declined by 2.09 percent per year), while delivering substantial “quota rents” to foreign producers.88 Import growth was attributable to the exemptions, lax government enforcement, and the growth of unconstrained foreign suppliers—most notably Austria and China.89

Second, neither the trade restrictions nor the subsidies revitalized the domestic industry. A 1990 Government Accountability Office report found, for example, that American companies had thus far failed to meet the Reagan administration’s domestic market share targets in four of the six machine tool categories at issue.90 The ITC in 1993 found that domestic machine tools shipments actually declined by 11.7 percent between 1989 and 1991, while employment dropped by 9.8 percent.91 According to a 1995 article for the Philadelphia Inquirer, after years of subsidies and import protection, the U.S. machine tool industry still remained a “distant third” in global production—essentially tied with Italy but well behind both Germany and Japan; had only half the volume of sales (measured in constant dollars) in 1995 that it had 30 years earlier; and saw its workforce shrink from 108,000 in 1980 to 58,300 in 1995 (as well as experience stagnant wages).92

Finally, the programs were plagued with dysfunction. The Government Accountability Office report found that the Commerce Department’s methods for monitoring quota compliance and related import volumes suffered from a lack of documented procedures and data, inaccurate calculation methodologies, and reporting delays of five months or more. It also found problems with compliance and enforcement. Moreover, U.S. restrictions on supplies from major foreign producers likely fueled the growth of new market entrants, including China, which has since become a global leader.

In 1993, the George H. W. Bush administration quietly allowed the machine tools VRAs to fade away.93 Furthermore, neither the Buy American restrictions nor the NCMS’s continued operation ever revitalized the domestic machine tools industry, which remains a DOD concern.

Semiconductor Tariffs and Subsidies. National security also undergirded U.S. support for the semiconductor industry in the 1980s and ’90s, but it also proved costly and unsuccessful.94 Government support was primarily implemented through two measures: the 1986 Semiconductor Trade Agreement (STA) between the United States and Japan and contemporaneous subsidies to support domestic semiconductor research and production. Each measure, however, generated meager benefits for specific U.S. firms while imposing substantial and unforeseen economic costs, leaving long-term national security objectives unmet or even undermined.

The STA. Under the STA, the Japanese government agreed to stop its producers from “dumping” dynamic random-access memory (DRAM) and erasable programmable read-only memory chips—enforced through production limits and export restraints that kept prices above U.S.-determined levels—and to guarantee foreign producers 20 percent of the Japanese market. In exchange, the United States suspended ongoing antidumping and Section 301 (a U.S. law intended to police foreign trading practices that allegedly harm U.S. commerce) investigations of Japanese memory chips.95

The STA’s economic harms were significant. A 1994 Peterson Institute analysis found that in 1989, the STA generated a net national welfare loss of $974 million ($2.04 billion in 2020 dollars) and cost U.S. consumers over $525,000 ($1.10 million in 2020 dollars) per manufacturing job potentially saved. After the STA took effect, domestic semiconductor prices “skyrocketed,” and a “full-fledged shortage of DRAMs was widely felt in the United States and Europe by early 1998.“96 As a result, U.S. semiconductor users, particularly up-and-coming computer manufacturers such as Apple that were dependent on DRAMs, were hobbled and less able to compete with Asian and European producers that could obtain cheaper DRAMs.97 As a result, the computer manufacturing industry shed one job for every U.S. semiconductor job supposedly gained from the STA.98 Increased DRAM prices also added almost $100 to the price of a personal computer selling for $600 or $700 in 1988.99

The STA also ended up helping Japanese semiconductor producers more than their U.S. competitors because the STA allowed the Japanese to charge higher prices in the United States and elsewhere. According to one Brookings Institution study, Japan’s manufacturers earned $1.2 billion in extra DRAM profits in 1988 alone and another $3–4 billion on all products in 1989—most of which was paid by U.S. consumers and computer manufacturers.100 Other studies found similar gains for Japanese producers, in part due to collusive behavior.101

U.S. producers, on the other hand, did not increase production capacity, despite artificially high domestic prices and U.S. government subsidies.102 All but one U.S. chip maker left the DRAM market within a decade, and the STA prevented neither industry recessions nor declining U.S. market share (which shrunk from 83 percent to 70 percent between 1986 and 1992).103 One reason is that U.S. firms found ways to circumvent the STA by importing not individual chips but rather assembled circuit boards that weren’t subject to the agreement.104 The benefits of the Japanese market share targets also proved illusory: although foreign semiconductor exports to Japan in 1992 hit the STA’s 20 percent market share targets, economist Craig Parsons found that this “achievement” was caused by broader macroeconomic trends, not the agreement itself.105 Other reports at the time noted that Japanese firms dumped the semiconductors that they were forced to buy into Tokyo Bay.106 Overall, “there is little consensus on whether the STA was effective in increasing the foreign market share.“107

As a result, “for most U.S. chip makers, the main impact of the price hikes was vastly greater profits strengthening their Japanese competitors.“108 Longer term, the STA actually helped “accelerate the entrance of Korean companies onto the world DRAM scene—as with Japanese companies, the supernormal profits that were obtainable in the years immediately after the [STA] allowed Korean firms such as Hyundai, Samsung, and LG to reap unexpected returns and gain a foothold at the lower end of the semiconductor technology ladder.“109 They are now market leaders.

Finally, the STA had significant political ramifications in the United States and abroad. It encouraged collusion among Japanese producers and restored the Japanese government’s control over the sector, with U.S. help. It led to the creation of a new and powerful lobbying group in the United States—composed of injured downstream user industries—that would go on to mold U.S. trade policy for decades.110 And it demonstrated the folly of U.S. security nationalism: just as the DOD was recommending action, American companies were exiting the DRAM market, having already discerned that their future was not in the “high-volume, low-profit commodity” but in advanced microprocessors, specialty chips, and design.111 As a result, U.S. Memories, a private consortium to expand domestic DRAM production, was “stillborn and collapsed in January 1990 owing to insufficient financial support and an unwillingness of other major buyers … to commit to future purchases.“112 Government planners foresaw none of this.

Sematech. Sematech (short for “semiconductor manufacturing technology”) was not a DRAMs project but instead a semiconductor R&D consortium funded jointly by private industry and the federal government—very similar to the consortium now proposed in the NDAA. As chronicled by Brink Lindsey in a 1992 piece for Reason, the primary impetus for Sematech was national security: only a month before the entity’s formation, a Pentagon-sponsored study on “defense semiconductor dependency”—prepared by the Defense Science Board, whose advisory panel conveniently included Sematech member companies—concluded that “it is simply no longer possible for individual U.S. semiconductor firms to compete independently against world-class combinations of foreign industrial, governmental and academic institutions.” The DOD therefore recommended $1 billion in government funding for a “Semiconductor Manufacturing Technology Institute.” Congress authorized $100 million a year for five years via the Defense Advanced Research Projects Agency.113

Lindsey showed how Sematech “confirm[ed] all the darkest suspicions of industrial-policy critics.” In its first phase, “Sematech was able to borrow technology from private companies and reproduce manufacturing results that other private companies had achieved years before—and do it with taxpayers’ money”; and in its second phase, Sematech did some “useful work, both in evaluating new equipment and improving working relations between chipmakers and suppliers”—but it was work that, while it may have helped a few favored U.S. equipment suppliers, added “very little to what private industry is already capable of doing for itself.“114

Meanwhile, U.S. semiconductor firms were staging a major turnaround but did so by “ignor[ing] just about everything Sematech’s supporters have ever said about semiconductor competitiveness.” Instead, “American companies have been thriving in those supposedly marginal ‘specialty’ markets derided by the Defense Science Board.” Even worse, Lindsey explained how Sematech actually hindered the industry’s revitalization by “favoring older, more-established companies [i.e., Sematech’s member companies] over innovative newcomers.” He finally debunked Sematech’s national security basis, noting that the U.S. military had ample domestic and foreign supplies of both commodity DRAMs and the chips most essential to U.S. weapons systems.115

Subsequent studies have confirmed Lindsey’s contemporaneous reporting. In a 1996 paper, for example, Douglas A. Irwin and Peter J. Klenow concluded that the “U.S. government’s contributions to Sematech do not induce more semiconductor research than would otherwise occur.“116 Even Sematech proponents Kenneth Flamm and Qifei Wang concluded that the consortium’s impact on member companies’ R&D expenditures was inconclusive and could in fact have been negative on net.117 That is hardly a ringing endorsement, given Lindsey’s account of other, noneconomic harms. In 2020, the Carnegie Endowment’s James L. Schoff included Sematech among the cautionary tales of American “technonationalism” in the 1980s:

The U.S. and Japanese bureaucrats promoting industrial policy and technonationalism at that time could not foresee the growth of the internet and how it would evolve in tandem with the smartphone and other new digital technologies. They could not conceive of AI-enabled cyber hacks of cloud-based data centers or stimulate the rise of internet titans like Google, Amazon, or the modern version of Apple. These companies flourished in the technoglobalist era and avoided single-firm product models by incorporating the best components of various leading technologies into their own product lines. Now these firms possess some of the world’s most coveted technology, investing more than most governments do to push new boundaries and accelerate change through design and systems integration.

Another lesson is that governments generally overreact to perceived technonationalist threats. Many U.S. policymakers and scholars during the 1980s viewed competition with Japan over technology as a form of economic warfare and regularly assumed the worst about the Japanese government’s intentions. American fears that Japan would come to dominate technological fields like semiconductors, supercomputers, satellites, and aerospace in the same way they pushed U.S. manufacturers out of the production of radios and televisions simply never happened, and U.S. initiatives such as SEMATECH or Super 301 trade dispute cases had only a marginal effect. After all, Japanese firms became members of SEMATECH within ten years, and many market-opening Super 301 cases against Japan involved products (like dynamic random access memory chips) that were soon overtaken by new technology or—in the case of satellites—were eventually subject to U.S. export controls. U.S. firms prospered because of their ability to innovate and compete effectively, not because of such technonationalist or protectionist measures.118

Given the NDAA’s plans to subsidize the U.S. semiconductor industry and to establish another R&D consortium, it appears that U.S. policymakers have not learned these lessons.

Other “Security Nationalist” Failures

These four case studies are a representative sample of the U.S. government’s long-standing inability to achieve national security objectives through protectionism and industrial policy, as well as the frequent abuse of “national security” for political purposes. Other examples of security nationalist failures include: Trump administration Section 232 tariffs on aluminum and Section 301 tariffs on Chinese imports;119 previous episodes of steel protectionism, including President Bush’s broad “safeguard” measures in 2001;120 the Sugar Program;121 crude oil import quotas from the 1950s to early 1970s;122 textiles and apparel protection;123 wool/mohair subsidies;124 Japanese automobile quotas; and antidumping duties on supercomputers and flat panel displays (which also received generous U.S. government R&D subsidies).125 In each case, along with many others, the outcome was essentially the same: high economic costs, the continued demise of the favored industry, political dysfunction, and U.S. government advocates who, as the American Enterprise Institute’s Claude Barfield explained in his book High Tech Protectionism, “either never understood or willfully ignored the structure of the industry and the nature of worldwide competition in the sector.“126

In short, any past successes of U.S. security nationalism are the exception, not the rule.

Free Markets Enhance U.S. National Security and “Resilience”

Freer markets—including openness to international trade and investment—can bolster national security and enhance the country’s resilience to economic “shocks,” such as a pandemic. The relationship between trade and national security has played a central role in U.S. economic and foreign policy since Secretary of State Cordell Hull helped create the World Trade Organization’s predecessor, the General Agreement on Tariffs and Trade, in the late 1940s and usher in the modern era of globalization.127 Since that time, numerous academic studies have supported Hull’s instincts, in terms of both geopolitics and economics, that trade and economic interdependence can prevent armed conflict and make countries more resilient to shocks.

Open Markets Help Achieve Geopolitical Objectives

A wide body of research across a range of countries and time periods reveals a strong, positive relationship between trade and national security.128

- One of the most influential analyses of trade and peace is that of John R. Oneal, Bruce Russett, and Michael L. Berbaum, who examined almost 10,000 country pairs between 1885 and 1992 and found that increasing two nations’ economic interdependence (as measured by bilateral trade-to-GDP ratio) from the 10th to the 90th percentile lowers the probability of a fatal dispute between them by 32 percent. They estimated that the growth in U.S.-China trade between the 1960s and 2002 reduced the probability of a fatal militarized dispute between the two nations by 27 percent, as compared with what it would have been without the increase in commercial relations (and assuming China’s authoritarianism remained unchanged). They further found that militarized disputes between nations significantly decreased their bilateral trade in the following year, thus indicating that “the relationship between trade and conflict is reciprocal.… Peace and commerce promote each other.“129

- Solomon W. Polachek and Carlos Seiglie similarly found in a 2006 study that as two countries’ gains from trade increase, their level of armed conflict decreases and their level of cooperation increases. In particular, a doubling of bilateral trade volumes leads to a 20 percent decrease in conflict.130

- In a 2016 Review of Development Economics paper, Jong-Wha Lee and Ju Hyun Pyun examined 243,225 country pairs from 1950 to 2000 and found that “an increase in bilateral trade interdependence significantly promotes peace,” with this effect strongest for contiguous countries (e.g., the United States and Canada). They also showed that peace is separately promoted by a nation’s openness to global trade and that “an increase in global trade openness reduces the probability of interstate conflict more for countries far apart from each other than it does for countries sharing borders.” Finally, they found that “states more dependent on the world economy tend to have fewer conflicts than those less dependent,” thus providing a strong “security motive” for nations’ efforts to increase other countries’ global economic integration.131

- Patrick J. McDonald in a 2004 article for the Journal of Conflict Resolution found that “free trade, and not just trade, promotes peace by removing an important foundation of domestic privilege—protective barriers to international commerce—that enhances the domestic power of societal groups likely to support war, reduces the capacity of free-trading interests to limit aggression in foreign policy, and simultaneously generates political support for the state often used to build its war machine.” Testing the link between individual countries’ trade barriers (measured in terms of both tariff levels and deviation from an ideal “free trade” state) and their propensity to engage in military conflicts, McDonald found that “the tendency of protective trade policies to increase military conflict is both statistically and substantively significant” and that “the level of free trade exerts a larger effect than aggregate trade flows on the outbreak of peace” between countries. He concluded that “these results strongly support the claim that free trade enhances the prospects for peace.“132

- Matthew O. Jackson and Stephen Nei in a 2015 paper examining alliances and interstate wars found that international trade induces peaceful and stable alliances: “Trade increases the density of alliances so that countries are less vulnerable to attack and also reduces countries’ incentives to attack an ally.” Examining detailed historical data on wars and trade, they showed that “the dramatic drop in interstate wars since 1950 is paralleled by a densification and stabilization of trading relationships and alliances”; that “countries with high levels of trade with their allies are less likely to be involved in wars with any other countries (including allies and nonallies)”; and that “an increase in trade between two countries correlates with a lower chance that they will go to war with each other.” They found that a country having more allies and more trade with those allies leads the country to be less prone to attack and less prone to being attacked. Importantly, they also noted that “in the absence of international trade, no network of alliances is peaceful and stable”—thus indicating the centrality of trade to peace, especially after 1950.133

- A 2020 analysis of 140 countries from 1970–2012, by Benny Kleinman, Ernest Liu, and Stephen J. Redding, found that as countries become greater economic “friends” (as measured by welfare exposure/gains due to the other countries’ productivity growth), they become greater political “friends” in terms of having more similar United Nations voting records, being less likely to be strategic rivals (i.e., “whether two countries regard each other as competitors, a source of actual or latent threats that pose some possibility of becoming militarized, or enemies”) and being closer to the “U.S.-led liberal order.” They concluded that these results, taken together, “are consistent with the view that increased conflict of economic interests between countries leads to heightened political tension between them.“134

- Finally, in a 2012 issue of the British Journal of Political Science, Timothy Peterson and Cameron Thies found that the post-World War II decline in armed conflict is driven by an “unprecedented” increase in intra-industry trade (i.e., trade in similar—in many cases, branded—commodities, caused by economies of scale and consumer demands for variety) during this period.135