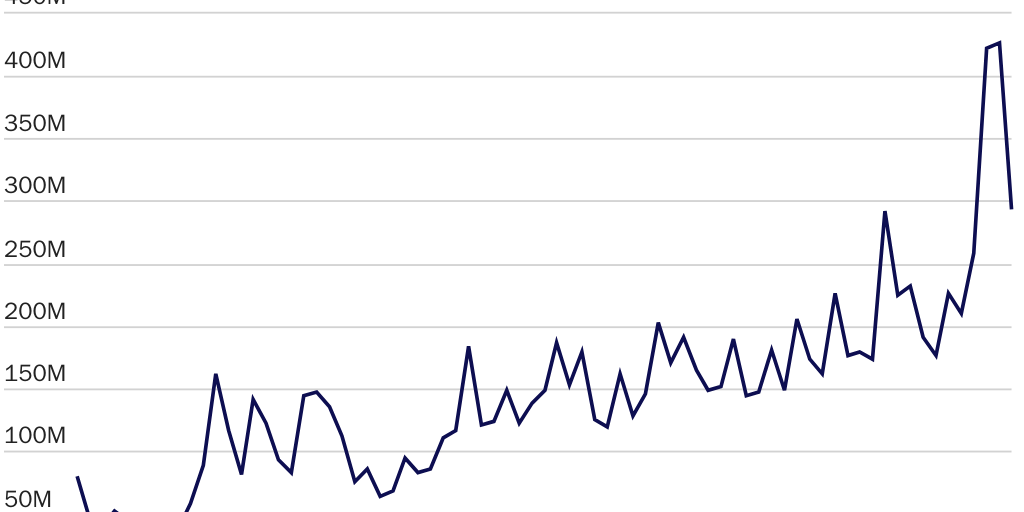

Cryptocurrency is here to stay, if the growing number of on-chain crypto transactions is any guide (see Figure 5).1 Yet the United States continues to lag other advanced economies by failing to provide clear rules for cryptocurrency and decentralized finance (DeFi). This lack of regulatory clarity should not be mistaken for a light-touch approach, which would be welcome. Rather, regulatory ambiguity has led to an untenable situation where crypto projects eager to comply with US law are offered no practical guidance, are rebuffed by their would-be regulators, and are undermined with high-stakes enforcement actions.

This status quo risks pushing entrepreneurs and developers with key skills (such as applied cryptography) out of the United States, as well as limiting Americans’ ability to take advantage of the capabilities of crypto and DeFi. These capabilities include mitigating the traditional risks of financial intermediaries (e.g., theft, fraud, and breach of duty) by replacing those middlemen with self-executing software programs. In addition, the technology underlying cryptocurrencies can be leveraged to build decentralized autonomous organizations (DAOs), as well as a new internet architecture (sometimes called Web3) that provides an alternative to more-centralized platforms. An inhospitable regulatory environment for cryptocurrencies, therefore, could have far‐reaching consequences for new technology pathways. Entrepreneurs, developers, and users should decide whether these pathways are explored, not policymakers and bureaucrats.

Importantly, cryptocurrencies hold promise for liberty, providing individuals with choice in their currency, the potential to protect their financial privacy and property rights, and the ability to engage in quick, cheap, and borderless transactions. Whether these promises are realized depends in part on providing a clear regulatory environment for cryptocurrencies that does not unduly burden their capacity to transform and grow.

The Problem

Regulatory uncertainty plagues the US crypto ecosystem on multiple fronts.

Crypto tokens. Because a crypto token may be seen as a commodity, a security, a currency, or perhaps something else entirely, the application of existing laws and regulations to crypto projects is not always clear. A legal landscape that is characterized by this uncertainty, or that prioritizes legacy regulatory formalities regardless of their practical relevance to cryptocurrencies, risks becoming inhospitable for both entrepreneurs and users and damaging to technological innovation, capital formation, and consumer welfare.

Resolving whether cryptocurrencies are regulated under securities laws or commodities laws is a prerequisite to addressing other questions about how to regulate the exchange of cryptocurrencies and their general interactions with the financial system, including questions about custody and accounting.

Securities laws evolved, in no small part, to address the risks posed by managerial bodies possessing information that investors do not and those bodies’ capacity to act at odds with investors’ interests. Cryptocurrency projects seek to transcend the traditional model of centralized enterprises with a corporate form, headquarters, and managerial hierarchy by eschewing, among other things, a managerial body exercising ongoing control over the project. Indeed, a core innovation of decentralized cryptocurrencies is that of mitigating managerial risks through technology.

When a cryptocurrency project does not involve centralized management or control, applying legacy securities laws is both legally inappropriate and practically ineffective at addressing potential harm. But applying securities-law safeguards designed to mitigate certain risks is appropriate when a cryptocurrency project involves managerial control (and when other criteria under securities case law are satisfied).

Crypto exchanges. Like crypto tokens themselves, the marketplaces over which they trade can be decentralized. These decentralized exchanges (or DEXs) replace centralized exchange services with self-executing software protocols that allow crypto users to transact peer-to-peer, thus mitigating traditional intermediary risks like those related to transaction execution and custody. DEXs are a core component of the broader DeFi ecosystem, allowing, for example, users to trade tokens that enable them to access Web3 services (such as decentralized social networks or file storage systems). Subjecting DEXs to regulations designed for traditional exchanges and broker-dealers does not suit the relevant risks or realities of DEXs and undermines their potential benefits. For example, applying registration requirements to open-source software protocols impedes their core benefits of open access and interoperability because licensing both inhibits the protocols’ ability to enter the market and third parties’ ability to integrate with them.

Centralized crypto exchanges present standard risks related to financial intermediation. Yet US regulators have not afforded centralized crypto exchanges practical registration pathways with clear and evenly applied rules. This de facto prohibition on lawful onshore crypto exchanges stymies innovation, competition, and entrepreneurship, and it provides little benefit to American crypto market participants.

Stablecoins, currency competition, and payment innovation. Cryptocurrencies can bring the benefits of competition to currencies, which have long been subject to government monopoly. Competition not only has the potential to provide currency that better suits an individual’s needs, but lessons learned from competition could also strengthen the dollar and help to preserve its status as the world’s reserve currency.

Although digital currency use is growing, to date it has not reached the level of traditional government fiat currencies. Stablecoins—cryptocurrencies designed to maintain a stable value—are one innovation that has seen increasing use and may provide opportunities for faster and more efficient methods of payment under a properly structured regulatory framework.2

Unfortunately, regulatory barriers, including uncertainty, stand in the way of such new tools and the competition they bring. For example, the Securities and Exchange Commission has made vague assertions that certain stablecoins are securities, leaving issuers unsure about their compliance obligations. In addition, proposals that would subject stablecoin issuers to tight gatekeeping by bank regulators, including frameworks that would prohibit any firm other than a federally insured depository institution from issuing stablecoins, would raise barriers to market entry.3

In addition, subjecting cryptocurrencies generally to capital gains taxes impedes their use as money. Because capital gains tax rates are structured to incentivize long‐term holding, these taxes penalize people for using cryptocurrencies as money for everyday purchases. They also impose a heavy—and at times impossible—administrative burden both on cryptocurrency users and on those required to report cryptocurrency transactions to the Internal Revenue Service.

Anti-Money Laundering laws and DeFi. The decentralized nature of certain crypto tools, such as DEX protocols and noncustodial crypto wallets (tools for individuals to personally safeguard their own crypto holdings) are a poor fit for the existing Anti-Money Laundering (AML) regime. The current AML regime leans on centralized financial intermediaries to, for example, identify customers and report supposedly suspicious activities. But applying rules designed for financial intermediaries to disintermediated financial technologies can effectively break them. For instance, requiring the operators of computing infrastructure that does not directly interface with customers to nonetheless identify those parties subjects the operators to unmanageable compliance obligations. Similarly, requiring providers of noncustodial crypto wallets to identify their customers is akin to treating manufacturers of physical wallets for cash as if they were banks; it creates both invasive and impractical regulatory burdens.

Taken together, these regulatory obstacles hinder the use of crypto technology as the foundation of new computing infrastructure and work against the use of cryptocurrencies as money.

Solutions

Congress can undertake several reforms to level the playing field for cryptocurrencies.

- Create a pro-competitive framework for stablecoin issuers. Congress should create a pro-competitive regulatory framework for stablecoin issuers. The framework should focus solely on basic reserve requirements and mandatory disclosure of relevant information about those holdings. The regulator overseeing this framework should not be one conflicted by involvement in providing other payment services. Moreover, regulators should not be granted discretionary authority to prevent certain stablecoin issuers from operating based on vague criteria. Additional anti-competitive restrictions that ought to be rejected are those prohibiting certain types of businesses (such as retailers or networked technology platforms) from issuing stablecoins, as well as mandates that stablecoin issuers be insured depository institutions.4

- Amend the definition of securities to exclude decentralized crypto token projects. Congress should amend securities statutes to clarify that securities laws do not apply to decentralized cryptocurrency projects by providing a clear, practical test for determining whether a crypto project is decentralized. The key question is whether the cryptocurrency purchaser is expecting profits solely from the efforts of others (i.e., relying on their essential managerial or entrepreneurial efforts). The criterion is whether, in selling a cryptocurrency, the seller, promoter, or developer promises performance necessary to bring the crypto project and its stated benefits to fruition. If so, the cryptocurrency project at issue is centralized. If not, it is decentralized.

- Establish tailored disclosure for crypto projects on the path to decentralization. Cryptocurrency projects can take time to achieve decentralization. Some projects may seek to sell their cryptocurrencies to finance their development or place governance tokens in the hands of users as a way to achieve decentralization. Congress should legislate a tailored registration model that prioritizes disclosures related to the specific risks of cryptocurrencies (e.g., fraud, deception, and manipulation by managers) and protections against fraud and misleading statements.

- Tailor policy to differences between centralized and decentralized crypto exchanges. Congress should ensure a framework for crypto marketplaces that is sensitive to the key differences between centralized and decentralized crypto exchanges. When exchanges are truly decentralized (i.e., where there is no single party or unified group promising performance or maintaining unilateral discretionary control, but rather an open-source and self-executing software protocol effecting transactions), they do not present the same intermediary risks as centralized exchanges. Bona fide DEXs should not be subjected to inapt regulatory requirements. In addition to averting asset custody risks, DEXs’ public transaction histories allow regulators to observe and address market manipulation. DEXs that wish to demonstrate that they comply with standards equivalent to those of centralized exchanges, including through automated controls, should have an option to do so via strictly voluntary registration.

- Provide clear and practical registration paths for centralized crypto exchanges. Centralized exchanges should be afforded a clear and practical registration pathway that is focused on intermediary risks. Specifically, crypto commodity exchanges should be offered a tailored, disclosure-based registration pathway. Crypto securities exchanges should be subject to a new crypto-specific alternative trading system rule made possible by Congress through amendments to the Securities Exchange Act.

- Answer key questions before devising Anti-Money Laundering legislation. Policymakers seeking to apply AML rules to DeFi applications should answer five key questions.5 First, does the legislative proposal distinguish centralized actors and decentralized systems? Poorly tailored rules encourage recentralization, reintroducing intermediary risks. Second, does the proposal require reporting information that applications do not have access to? If so, it acts as a de facto prohibition on DeFi infrastructure. Third, does the proposal preserve cash-like treatment for cash-like transactions done digitally? Genuinely peer-to-peer transactions should not be subject to greater surveillance than cash. Fourth, does the solution accommodate technological change? If not, innovations that are useful to users preserving their privacy, as well as the interdiction of bad actors, could be counterproductively left by the wayside. Fifth, is the solution evidence-based? Any proposed solution should have a clear and compelling evidence-backed rationale regarding its efficacy.

- Do not apply punitive tax rules to the crypto ecosystem. Congress should remove capital gains taxes, at the very least, where cryptocurrencies are used to purchase goods and services. Tax‐reporting standards should not undermine crypto miners and developers by, for example, subjecting them to inapt rules that encompass them within overbroad definitions of covered entities.

Suggested Readings

Regulatory Clarity for Crypto Marketplaces Part I: Decentralized Exchanges by Jack Solowey and Jennifer J. Schulp, Cato Institute Briefing Paper no. 154 (May 10, 2023)

Regulatory Clarity for Crypto Marketplaces Part II: Centralized Exchanges by Jack Solowey and Jennifer J. Schulp, Cato Institute Briefing Paper no. 155 (May 10, 2023)

Don’t Push Crypto Offshore, Don’t Outlaw Disruptive Innovation by Jack Solowey, Cato at Liberty (blog), Cato Institute (February 24, 2023)

Practical Legislation to Support Cryptocurrency Innovation by Jack Solowey and Jennifer J. Schulp, Cato Institute Briefing Paper no. 140 (August 2, 2022)

Congress Should Welcome Cryptocurrency Competition by Nicholas Anthony, Cato Institute Briefing Paper no. 138 (May 2, 2022)

A Simple Proposal for Regulating Stablecoins by Norbert J. Michel and Jennifer J. Schulp, Cato Institute Briefing Paper no. 128 (November 5, 2021)

This work is licensed under a Creative Commons Attribution-NonCommercial-ShareAlike 4.0 International License.