A warm winter in 2022–2023, a purposive decline in consumption that caused the economy to cool, and frantic efforts to attract supplies of liquefied natural gas (LNG) obscured Europe’s enduring reliance on cheap Russian gas for economic growth. European winters will not always be warm, and there is not enough LNG to replace Russian gas in the short term. Efforts to wean Europe from Russian gas permanently defy economic logic. Should policymakers choose to do so, it would carry costs not only for Europe but also for the United States and the rest of the world.

The model for much of European economic growth—especially Germany’s—would be destroyed, without a clear vision of what could replace it. European inflation, economic stagnation, and even political instability loom. Meanwhile, higher gas prices could ripple through the global economy, stoking inflation and food shortages that in turn would impact quality of life in the developed world and could produce much worse effects in the developing world.

If contract gas prices are elevated, Europe would search for alternative suppliers. U.S. producers of natural gas are liquefying as much gas as possible to capitalize on higher prices in Europe, but there is no hope that LNG could replace Russian gas supplies. Moreover, as U.S. producers liquefy and export more gas, domestic prices will rise, erasing a U.S. advantage.

This paper focuses on the economic realities in Europe in the context of the war in Ukraine and calls for policy to engage with those realities. The costs of the war, and the Western policy responses to it, should create a sense of urgency for U.S. and European policymakers to find a political path out of the conflict. Otherwise, those underlying economic realities as well as the horrible consequences of the war are likely to impact Europe—and the world—for a long time.

Introduction

The high quality of life in the modern, developed world is in no small part due to our ability to control and utilize our surroundings. Mastery over energy has been a driving force of innovation and advancement for centuries. Flows from rich sources of energy to productive uses of it have yielded large economic benefits. Disruption of these flows makes all parties worse off economically. Leaders and policymakers who disturb these flows in pursuit of political aims face a harsh choice: either explain to their people why they should be willing to bear such suffering or else change their costly policies. If the economic suffering becomes significant enough, voters are likely to defend their own well-being at the ballot box if leaders cannot persuade them that these policies are worth the high costs and likely to achieve their stated aims. This paper shines a light on the economic damage wrought by limiting Russian gas and suggests that policymakers should urgently pursue a political solution to the war in Ukraine.

The winter of 2022–2023 was not as economically disastrous as it could have been, thanks largely to unusually warm weather in Europe. The severity of winter is variable, likely indicating problems for the continent in the future. Also, deindustrialization—that is, the shuttering of energy-intense industries—has helped decrease demand for gas but presages a poorer Europe. Less heating and lower economic production helped avert a crisis last winter but in the long run could lead to popular discontent.

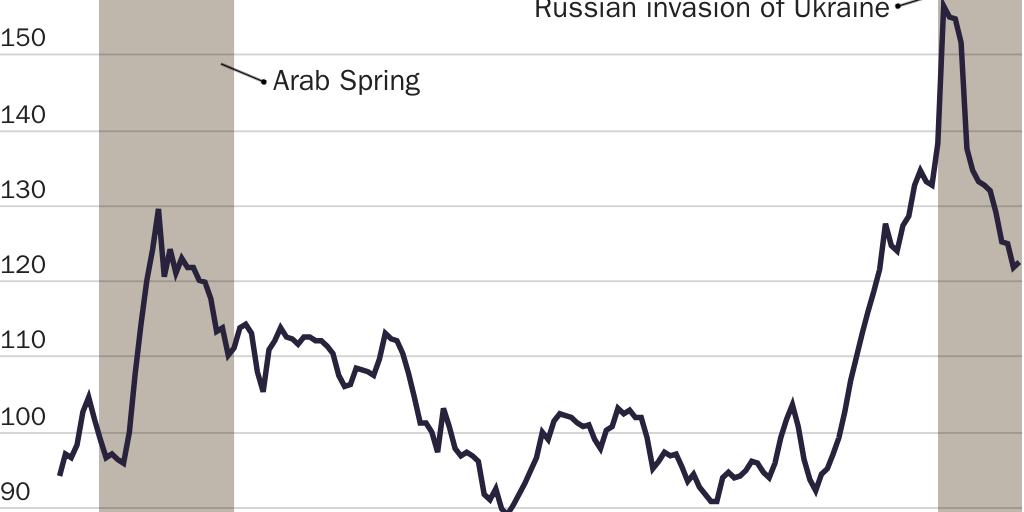

Over the last 50 years, importing inexpensive Russian gas has helped solidify Germany’s position as a world leader in industry and commerce, greatly enhancing the well-being of its people. The Russian standard of living has been improved by export earnings, a mutually beneficial arrangement. Beginning in 2022, there have been calls to reduce or boycott Russian gas to punish Russia for the war in Ukraine and to pressure it to accept a settlement favorable to Ukraine.1 Decisions by Poland and Ukraine to block or limit pipeline gas flow, to say nothing of the Nord Stream sabotage, disrupt this energy flow, adversely affecting the well-being of people worldwide as gas prices rise and lead to higher costs for everything from heating and electricity to plastics and fertilizer, resulting in material declines in average living standards, with more severe outcomes in poorer countries. Figure 1 shows the effects the war—and the policy responses to it—have had on world food prices.

Economic damage to Russia from interrupting the flow of gas is unlikely to be painful enough to produce policy change in Moscow. In 2021, gas exports to the European Union (EU) represented 0.8 percent of Russian gross domestic product (GDP), jumping to 2 percent of GDP in 2022 due to spiking prices.2 Going forward, the sharply decreased volume of pipeline gas to the EU may shrink its share to a more usual level, such as in 2021, if gas prices do not spike again.

Although pipeline gas flows cannot be redirected in the short run, long-term capital expenditure adjustment will change the geography of exports, increasing the relative share of Asia in the mix and diverting more gas bound for Europe to Russia’s ambitious LNG development program.3 Furthermore, the majority of the planet, namely the Global South, China, and India, do not support sanctions and continue to buy Russian fertilizer and other natural gas products. Threatening these countries with secondary sanctions would hurt the West’s relationship with them and would result in unintended negative consequences.

In the United States, fracking and the shale revolution have been a major boon to consumers and industry alike. Those opposed to Nord Stream 2 have sought to prevent Russia from gaining economic leverage over Europe but also have touted the benefits of exporting U.S. LNG to Europe.4 Already, increased U.S. LNG exports to replace Russian gas have resulted in higher domestic prices, increasing the cost of electricity, heat, and all manner of goods and services. This reduction in Americans’ standard of living is likely to accelerate. The costs would be diffuse, but the benefits would be concentrated.

Featured Event

EU policymakers, who either are not elected or do not face direct elections, have stated that this pain and suffering are worth it to save democracy and Ukraine.5 Politicians who must answer to voters will be forced to explain more as the costs, both direct (financial and military aid to Ukraine) and indirect (inflation and damage to the economy), increasingly hurt the electorate. A better alternative would be to consider what kind of political decisions could help end the war, avoiding the horrible consequences for all parties that could continue for a long time.

To reach an acceptable political solution, policymakers must take into account Russian interests, even if they do not consider them legitimate. Any solution is likely to include defense-related concerns, economics, and territorial questions. A peaceful solution is in the interest of all parties, but establishing what a feasible agreement looks like will be difficult and require reanimating the long dormant art of diplomacy.

This paper proceeds in three sections. First, it explains how Europe grew dependent on cheap Russian gas and shows the economic and political realities that relationship created. Second, in the context of calls for Europe to end its reliance on Russian gas, it demonstrates that it is impossible to replace Russian gas in the short or even long term, explaining why Europe’s better-than-predicted navigation of the winter of 2022–2023 is no indication that the problem has been solved. Third, it examines the costs of trying to replace Russian gas—for Europe, the United States, the Global South, and the environment. It concludes by arguing that since these economic realities are not amenable to policy changes, policymakers should demonstrate a sense of urgency in looking for political ways to end the war in Ukraine.

Fueling Europe

Today, flows of Russian gas through land-based pipelines are far short of full capacity (see Figure 2). Gas piped to Turkey under the Black Sea and onward to Europe continues, but the September 2022 sabotage of the Nord Stream pipelines eliminated a major source of gas, especially for Germany, which saw gas consumption in October–December 2022 fall 23 percent for industry and 21 percent for private consumers and customers compared to the average of the four prior years, despite massive imports of LNG.6 The dearth of cheap Russian gas is one reason that the German economy slipped into recession (i.e., GDP declined the last two quarters in a row).7

This stands in stark contrast to the relationship between the USSR/Russia and Europe over the last 60 years. Political turmoil—including the Cuban Missile Crisis, Prague Spring, the Soviet invasion of Afghanistan, and the U.S. bombing of Serbia—did not affect the flow of energy resources. The history of this successful economic relationship over energy, the most important of commodities, sheds light on the consequences of divorce now.

After the defeat of Nazi Germany, Soviet oil deliveries to Central and Eastern Europe increased steadily through the 1950s, as did export of components and steel pipes to the USSR, making this economically viable and beneficial to both sides.8

To increase these flows, in 1958 the USSR and its Eastern Bloc allies proposed the Druzhba pipeline, to be built largely using West German pipes. In an eerie foreshadow of today’s events, the John F. Kennedy administration opposed the pipeline, arguing that it would enhance the economy and thus the power of the USSR. It sought to block West German exports through the Coordinating Committee for Multilateral Export Controls (COCOM), a body created to control exports to the Eastern Bloc, specifically placing embargoes on advanced industrial goods and technologies.9 When some COCOM members refused to vote for it, Kennedy pushed the embargo through NATO, which unanimously approved a secret resolution banning export of large-diameter steel pipes.10 (The United States used NATO in a similar way to bypass organizations such as the United Nations when it attacked Serbia, Iraq, and Libya.) However, non-NATO countries and even some NATO countries did not comply with U.S. efforts, and the first oil flowed in 1962, with completion of the pipeline in 1964.

Similar politicking surrounded the first major USSR–Central and Eastern Europe gas pipeline. The Ronald Reagan administration’s opposition to the project was “an essential part of the effort to impede the growth of Soviet political and military power and economic leverage” and called for a ban on exports to the USSR for the pipeline, instead offering “access on favorable terms to U.S. coal and uranium resources,” similar to today’s promises of U.S. LNG for Europe.11 The USSR did not manufacture large enough pipes or compressors but planned to purchase them from Italy, a move seen as mutually beneficial and increasing trust in Europe.12 The U.S.-led diplomatic charge to stop the pipeline, ostensibly because of Soviet backing of the imposition of martial law in Poland in December 1981, fell short in the face of European solidarity in support of the project, and in 1983, the first gas flowed.

Featured Media

In 2011, Nord Stream AG, 51 percent owned by Russia’s Gazprom and 49 percent by German, French, and Dutch utilities, launched a pipeline under the Baltic Sea with annual capacity of 55 billion cubic meters (bcm), enough to satisfy over 26 million European households.13 As with previous projects, Western partners provided certain key components and pipes, as well as expertise required to lay the world’s longest undersea pipeline. Figure 3 shows the major gas delivery routes into Europe.

The direct Russia–Germany route of the pipeline and added expense of going under the Baltic Sea was intended to avoid disputes over transit tariffs and pricing with Ukraine and Poland and eliminate their leverage over Russian gas flows as well as interference from other Baltic states.14 Such disputes became an issue in the 1990s and early 21st century, particularly with the pipeline system sending gas from the Yamal Peninsula in the Arctic Ocean through Poland to Europe.15

The new route created political tension between Germany and some other EU members, with Polish and Baltic ministers even comparing it to the 1939 Molotov-Ribbentrop pact between Nazi Germany and the USSR.16 Opponents of the pipeline raised two main arguments. The first was the hypothetical threat of Russia cutting off gas supplies to exert political pressure, although this had never happened. The second was the idea that these countries had a right to transit fees, implying that buyers should pay more or sellers receive less to support transit countries. Such arguments have been repeated in relation to Ukraine.17 In the end, these arguments failed, and the pipeline was built.

While opposed in principle, the George W. Bush and Barack Obama administrations’ responses were muted. This was not the case with the proposed Nord Stream 2, which ran alongside the first project. President Donald Trump was vocal in his opposition, famously stating, “So we’re supposed to protect you against Russia, and you pay billions of dollars to Russia, and I think that’s very inappropriate.”18 In other words, this was a new twist on the old argument that such projects would enhance the power of Russia at the expense of the EU, ignoring the mutually beneficial aspects of it. Additionally, many, including Trump, argued that increased Russian gas sales would hurt potential U.S. LNG sales to Europe and thus the U.S. economy.19

Ultimately, in December 2019, the Trump administration did sanction firms involved in pipeline construction. In a rare defense of European sovereignty in the face of U.S. power, German Chancellor Angela Merkel said she was “opposed to extraterritorial sanctions” and together with Austria declared that the EU should decide its own energy policies without U.S. interference.20 As sanctions led to Russian contractors and materials replacing Western ones, work slowed but was eventually completed, aided by the Joe Biden administration lifting sanctions in May 2021. The completed 55 bcm annual capacity Nord Stream 2 never transported gas after Germany declined to commence operations following the Russian invasion of Ukraine.

Pipeline Politics in the Wake of the Russian Invasion of Ukraine

Ironically, on May 23, 2022, it was Poland, not Russia, that unilaterally terminated the Inter-Governmental Agreement (IGA) for natural gas delivered via the Yamal pipeline.21 This was due to Russia’s aggression against Ukraine, according to Polish Minister Anna Moskwa. The early termination smacked of politics since the agreement was scheduled to expire at the end of 2022 anyway. In terminating the agreement, Poland may have validated the efforts and added expense of Germany and Russia in laying Nord Stream under the Baltic Sea (i.e., to remove the leverage of transit countries on buyers and sellers).

On September 27, 2022, Poland and Denmark launched the Baltic Pipe to bring 10 bcm, the volume of gas Poland had been purchasing from Russia under the IGA, from Norway.22 Poland’s ability to reverse the Yamal flow and import gas from Germany, some of which had been received from Russia via Nord Stream, made the decision to terminate the IGA easier and was key for four months until the Baltic Pipe launch. It would prove fortuitous when the Nord Stream flow abruptly ended.

For 60 years, the USSR/Russia sold cheap energy to Europe, fueling its economic boom. Gas was not used as an “economic weapon” against other countries, as we have been repeatedly warned over the past six decades. However, there have been interruptions stemming from other kinds of disputes (see Box 1), and Russia not using gas as an economic weapon may have changed in mid-2022.

The Nord Stream 1 pipeline is pressured by the Portovaya Station, with compressors driven by five 20-ton turbines, originally manufactured by Rolls-Royce, plus a few spare turbines to ensure continuous operation.23 These complex, expensive machines require maintenance, onsite and at a factory, that is necessary to avoid violating the warranty.24 The imposition of sanctions on Russia threw a wrench into the works when the turbines were sent to Canada for maintenance.

On June 14, 2022, Siemens Energy, which acquired Rolls-Royce’s gas turbine business, stated that “due to the sanctions imposed by Canada, it is currently impossible for Siemens Energy to deliver overhauled gas turbines to the customer.”25 As a result of the equipment not being returned in time, and expiration of the allowed 25,000 hours between service on the other turbines, Gazprom reduced the number of turbines in operation at Portovaya from five to three, lowering gas flow capacity to only 60 percent.26 On July 16, Gazprom shut down another turbine (to 40 percent of capacity), and on July 27, a fourth was taken offline (to 20 percent).27

Initially at least, sanctions prevented the return of the turbines from Canada, raising the question of why they were sent there in the first place.28 After Gazprom was granted a waiver from sanctions, the first turbine was sent from Canada to Germany. However, Gazprom refused to take delivery, which Siemens and Western politicians characterized as a Russian political move.29

According to Gazprom, Siemens did not provide documentation that return of the turbines would not violate Canadian, EU, or UK sanctions, despite multiple requests, indicating significant risks for the Russian side.30 Furthermore, Gazprom declared that the turbine was sent to Germany, not returned to Russia as per the contract, which was signed with Siemens Energy subsidiary Industrial Turbine Co. (UK) Ltd., not Siemens Energy Canada Ltd., which received the Canadian export documentation.31 Thus far, Siemens Energy and Western governments have not commented on these specific issues noted by Gazprom.

Additionally, Gazprom stated that it sent damage reports about the turbines in operation that Siemens Energy denies receiving.32 On September 2, 2022, the Russian regulator ordered Gazprom to halt the last remaining turbine because of an oil leak that could lead to fire or explosion.33 Western turbine experts, including Siemens, stated: “Such leakages do not usually affect the operation of a turbine and can be sealed on site. It is a routine procedure during maintenance work.”34 This echoes sentiments expressed by Western politicians that Russia was deliberately cutting the gas supply to exert pressure on Europe.

Dmitry Peskov, spokesman for President Vladimir Putin, also stated that Russia would need to be sure that “the British subsidiary of Siemens would not remotely shut down the turbine.”35 While this might seem paranoid, it harkens back to an alleged Reagan-era transfer to the USSR of technology containing viruses that blew up a Siberian pipeline.36 Some have cast doubt on the veracity of that incident because of the lack of independent corroboration.37 However, from the Russian point of view, it is reasonable to assume that it is true; any operator of Russian critical infrastructure likely assumes Western-supplied tech contains elements that can be used to gather intelligence or sabotage critical Russian infrastructure, much in the way the United States views Chinese tech.

This author is not an engineer and thus not qualified to comment about the technical questions involved in turbine operation and maintenance. Also, the contracts between Siemens Energy and Gazprom and the customs and sanctions waiver documentation are not public. Thus, it is difficult to judge the merits of the specific contractual violations alleged by Gazprom, although it is interesting that Gazprom has not received a response to these issues, and it is difficult to see why Siemens would reroute the delivery and swap contractual counterparties. Similarly, the exposure of the contractual parties to differing sanctions in multiple jurisdictions clouds analysis.

Hopefully, with time, more information will become available, especially as a result of court proceedings and/or arbitration that is all but certain to result from this situation. This would help determine whether the stoppage resulted from Russia using gas as a weapon for the first time or from mechanical and legal problems. Either explanation is plausible.

It is also possible that both versions are partly true: Siemens was returning the turbines this way so that it could claim fulfillment of its obligations without the turbines actually reentering service while Russia could claim that it wanted to resume pipeline operation but was prevented from doing so.

For the foreseeable future, the Nord Stream pipelines will not be used as a weapon, as three of the four pipes were ruptured by explosions on September 26, 2022.38 Whether the one undamaged Nord Stream 2 pipe will be put into operation or the other three repaired is more a question of politics than engineering.39

The politics surrounding these pipeline systems and trade deals complicate an economic truth: Russia/USSR has a surplus of gas, and Europe has a deficit. In the absence of trade, Europe—Germany in particular—would face higher energy input costs leading to smaller and less competitive industry, while Russia would enjoy cheap gas at home but with lower output/economic activity. The gas trade leaves both parties better off economically, as basic economic logic suggests. In other words, low energy input costs have helped German industry to become a world leader despite high labor costs. This has greatly increased the well-being of Germans. Greater revenue from gas sales has in turn increased Russian investment in infrastructure and disposable income, benefiting the Russian people.

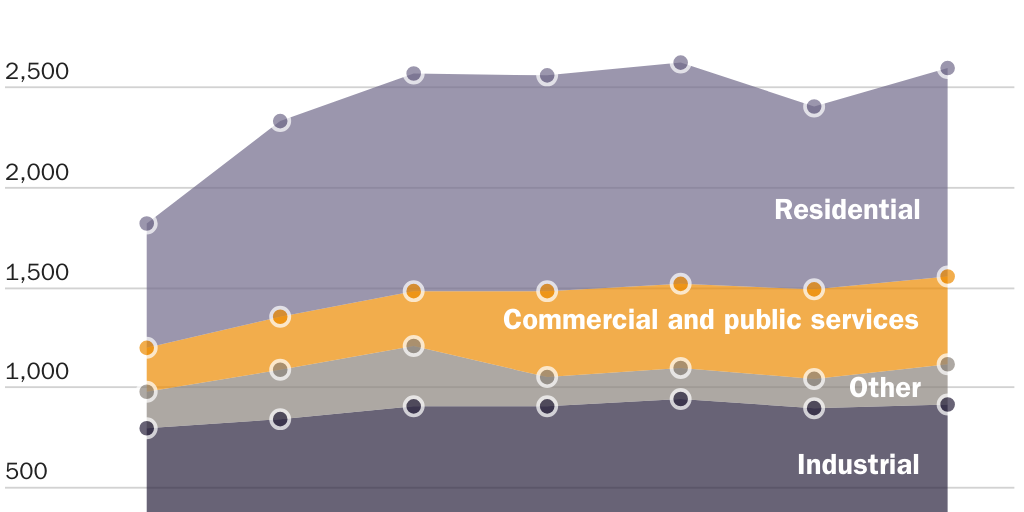

The pain in Europe resulting from higher gas prices will affect not only industry but also the population through higher home heating and electricity bills, on top of elevated prices for nearly all goods and services. “Demand destruction,” the current buzzword for using less energy in Europe, will damage not only the industrial sector but also residential heat and nonindustrial commerce, as Figure 4 shows.

Prior to the Russian invasion of Ukraine in February 2022, the positive-sum economic aspects of this relationship were widely acknowledged. It is important to note that even during the height of the Cold War, during periods of conflict and tension, flows of gas continued. The hypothetical that Russia would cut off the gas flow as an economic weapon was often trotted out during the Cold War and is being reprised today to justify actions to prevent economic trade that benefits both Russia and its neighbors. Even during the steadily worsening sanctions regime beginning in 2014, Russia delivered all the energy that Europeans bought under fixed contracts, a point often made by Russian business and political leaders.40

The argument that European dependence on Russian gas gives the latter an economic weapon is often exaggerated, since by the same token Russian dependence on European gas sales gives the latter an economic weapon. At the same time, it should be noted that there is an asymmetry: the lack of Russian gas has a very bad effect on the European economy, while the effect on Russia is less severe—although its gas producers and pipeline operators suffer significant losses.

Moreover, there is always the threat of a buyer’s strike. The 1,213 kilometer Blue Stream pipeline, which runs under the Black Sea from Russia to Turkey, commenced operation in February 2003 with annual capacity of 16 bcm. The offshore portion of the pipe is a 50/50 joint venture between Italy’s Eni and Gazprom. A month later, Turkey unilaterally stopped taking gas, in clear violation of a take-or-pay contract it had with the operators, and demanded lower prices and volumes because of weak demand.41 Although Turkey had no legal basis to do this, ultimately Russia agreed to these humiliating terms so that its $3.2 billion investment would not be wasted.42 This incident illustrates the oft-espoused fallacy that suppliers in pipeline systems have tremendous power whereas buyers have none.

In fact, political decisions by the EU have given Turkey more leverage over European energy supplies. In 2012, Russia began construction of the South Stream pipeline to deliver gas directly to EU member Bulgaria, without any transit countries. However, the EU implemented numerous roadblocks after construction had begun, despite objections from some of its members, resulting in Russia rerouting the pipe to Turkey, renaming it Turk Stream.43 The EU now buys the same gas but only after paying a Turkish transit fee.44 Also, Turkey can now shut off the gas flow for political reasons, such as EU criticism of its policies vis-à-vis Azerbaijan/Armenia, Syria, or the Kurds, to say nothing of Turkey’s application for EU membership that has languished for over two decades.

In sum, the USSR/Russia–Europe gas relationship has been profitable for all involved. USSR gas exports to Europe increased from basically zero in 1950 to 110 bcm per year in 1990.45 In 2021, Russia exported 185 bcm of gas to Europe.46 This in no small measure has fueled phenomenal growth in Europe, with real GDP per capita rising 281 percent since 1980.47 Opponents of the Europe-Russia energy relationship have provided no answer for how to replace Russian gas as an engine of European economic growth.

Disruptions to the Flow of Gas since the Invasion of Ukraine

Today, Europe is in a very different situation. Through a combination of sanctions, political decisions to shut energy flows, and the outright destruction of pipelines, a significant portion of ex ante energy supplies will not reach Europe.

The economic logic of the Russian-European energy relationship has not changed, but rather the politics of that relationship have in the wake of Russia’s invasion of Ukraine. The intervention of politics in the absence of options for adjustment clearly leaves all parties worse off economically.

Europeans have been making lifestyle sacrifices, such as wearing sweaters and turning down thermostats, to support political aims. In pursuit of sufficient punishment to reverse Russia’s Ukraine policy, European politicians are inflicting damage on their own people. Continuing down this path may lead to a bleak future. Early in 2022, calls to gather firewood rather than burn Russian fuel seemed fanciful.48 Later in the year, the news was full of stories of a run on wood stoves, people waiting in line for days to buy coal, and anticipated blackouts.49 As the situation stabilized and the warm winter eased fears, panic subsided—but could return.

The question is whether there are alternatives to Russian gas for the European economy and alternatives to European purchasers for Russian gas.

Why Europe Will Struggle to Replace Russian Gas

When it comes to natural gas, for Europe there is no near-term alternative to Russia. Europe endured the winter of 2022–2023 much better than some observers imagined, in large part due to exceptionally warm weather. However, the severity of winter varies and is unpredictable, so sunny assumptions should not form the basis of policy. Also, the idling of capacity helped reduce demand as did less heating in businesses, homes, and schools. (Gas demand for heating is more elastic than gas demand for electricity or industry. Due to greater elasticity, demand reduction is easier in winter [see Figure 4]). These factors resulted in EU consumption of natural gas from August 2022 to January 2023 falling 19.3 percent year on year.50

If such demand restrictions can be maintained or strengthened going forward, Europe’s economy and standard of living will suffer. In other words, Europe has not solved the problem of reliance on cheap Russian gas. At best, Europe has bought some more time unless it wants the process of deindustrialization and decline in well-being to continue.

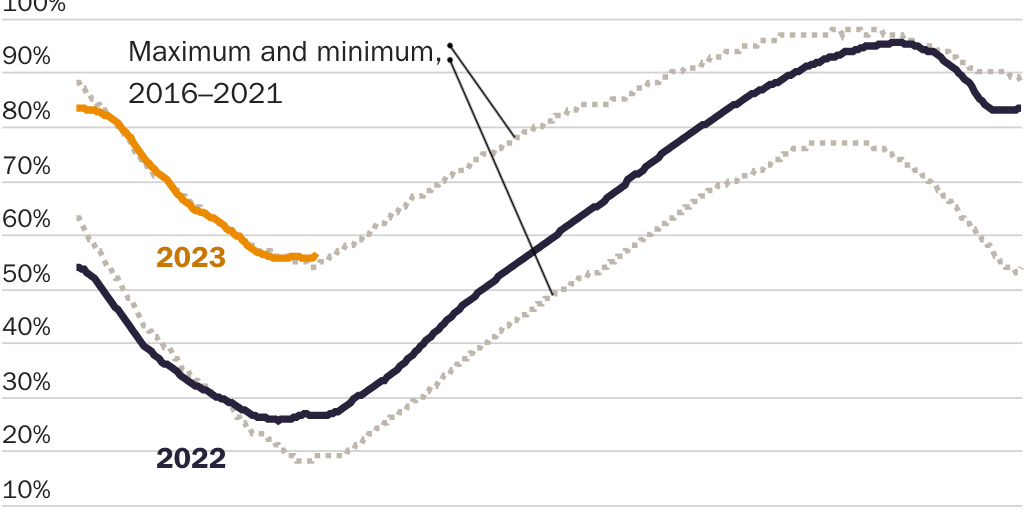

Figure 5 illustrates that EU gas storage at the beginning of 2022 was at or below the historical minimum of the range. As conservation measures kicked in during the year, and the mild winter eased demand, the storage level approached the maximum of the normal range. In 2023, storage levels remained near the top of the range, as the first three months of the year were warmer than usual. Whether nature continues to cooperate remains to be seen.

Not only did Europe benefit from reduced demand, but more supply was available. Nord Stream 1 was operating normally during the first half of 2022 and then at declining rates for another three months before being sabotaged at the end of September. Gas flow capacity through Ukraine was 100 percent before dropping to some 67 percent when Kyiv closed the Sokhranovka pipe on May 11, 2022.51 In the first 26 weeks of 2023, the EU imported only 25 percent of the Russian pipeline gas it imported during the same period the previous year; if this reduced rate persists for the rest of 2023, the EU will import 115 bcm less pipeline gas than in 2021.52 (See Figure 2 for a graphic representation of the decline in pipeline gas flows.)

Thus, Europe would have to replace even more natural gas in 2023 than in 2022. The shortfall in natural gas supplies in 2022 was partially compensated by LNG imports increasing by 60 percent, or 50 bcm year on year, and demand declining by 55 bcm, or 13 percent, its steepest drop in history.53 Even if these levels of LNG imports and demand destruction are maintained, available gas will be insufficient. If LNG cargoes cannot be attracted because of increased Chinese demand or if Russian imports fall further or if next winter is colder, the gas deficit will be even greater, necessitating further shuttering of industrial capacity and lowering of Europeans’ standard of living.

In theory, fracking could help ease Europe’s gas deficit. However, fracking is a political hot potato, with nearly every European country banning it and with very low popular and political support, due to environmental concerns as well as regulatory and infrastructure problems.54 In some EU countries where gas fracking was attempted, such as Poland, the costs were too high, making commercial exploitation not economically viable.55 Fracking in Europe could be revisited if gas prices settle at a much higher level, causing significant economic pain, sufficient to overcome environmental concerns. This, however, would likely take considerable time and thus not help with the energy shortfall for the foreseeable future.

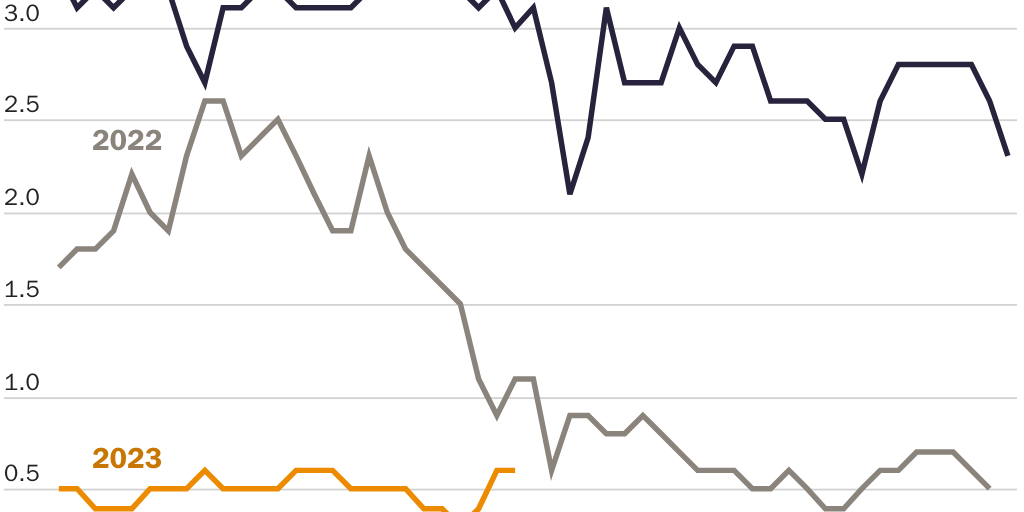

The market also expects higher prices for natural gas in Europe. Although the entire futures curve has shifted down as supply fears have abated somewhat, the December 2023 and May 2024 contracts are trading 53 percent and 39 percent above the May 2023 contract.56 It is worth noting that futures’ prices are not future prices; they are affected by many factors. Still, expectations of higher future prices play a significant role in these premiums.

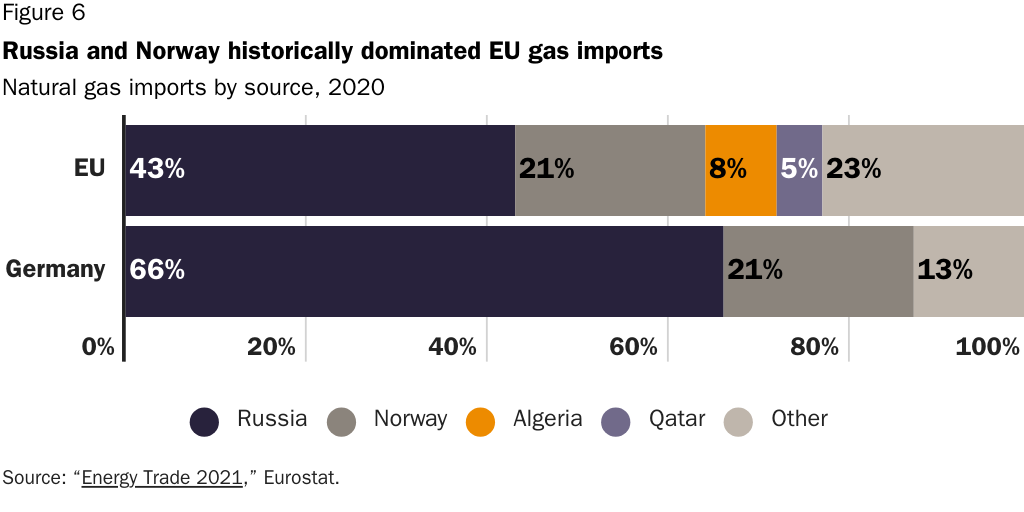

Figure 6 shows Europe’s reliance on Russia. Norway, the second-largest supplier of gas to Europe after Russia, exported 113 bcm in 2021, near capacity. An additional 10 bcm of supply is optimistically anticipated, but this cannot replace Russia’s 185 bcm per year.57 Bringing additional capacity online is difficult because of strong opposition from environmentalist and socialist parties. Also, expanding drilling and infrastructure would take years, during which time depletion of current fields will continue.

The third-largest supplier to Europe is Algeria, which may be able to increase supply by some 7 bcm, about 5 percent of what Russia supplies, through pipelines to Italy and Spain. However, the lack of spare capacity in pipelines from Spain to the rest of Europe may be a bottleneck: the Spain–France pipeline has annual capacity of only 5.5 bcm with utilization averaging 71 percent.58 Other North African suppliers are unable to increase deliveries because of supply constraints and political unrest.

Gas exports to Europe from Azerbaijan’s Shak Denis field in the Caspian Sea via the Southern Gas Corridor and the Trans-Anatolian Natural Gas Pipeline, or TANAP, are set to increase, but the amount and time frame are not certain. Current exports of 16.2 bcm (10.5 bcm to Europe and 5.7 bcm to Turkey) are expected to increase to 31 bcm per year in 2026.59 It is unclear what portion of the increase will be consumed by Turkey and Georgia. Also, there is high geopolitical risk in the Caucasus. The latest phase of the Armenia–Azerbaijan war is still simmering, and Georgia’s disputes over South Ossetia and Abkhazia remain unresolved.

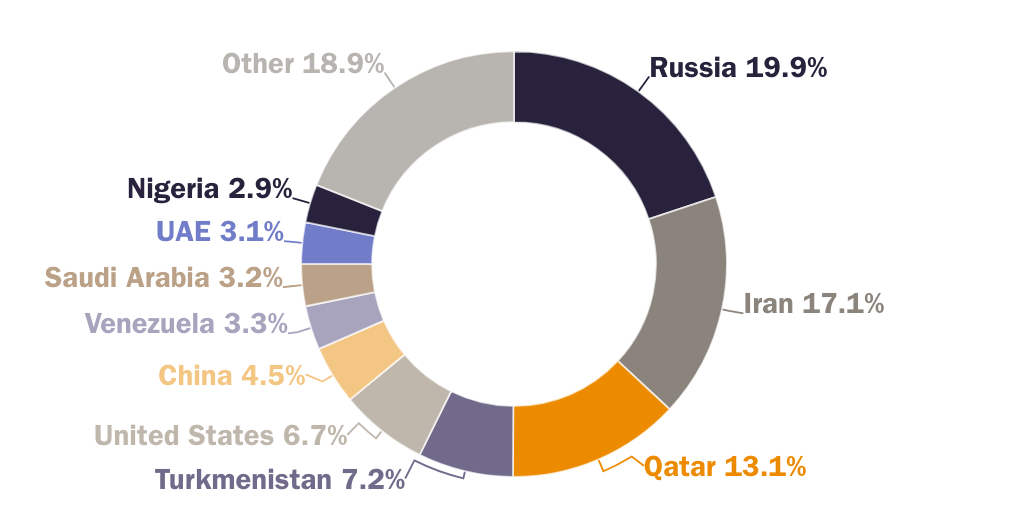

Another possible source of gas for Europe is Azerbaijan’s neighbor, Iran, which sits atop the world’s second-largest gas reserves and could theoretically build a pipeline to deliver cheap gas. However, current Western policies make that country a political and economic pariah. Farther east, Kazakhstan and Turkmenistan could increase gas production, but transport infrastructure is limited and passes through Russia and, therefore, is not a viable alternative to Russian gas. Figure 7 makes clear that natural gas exists in a variety of countries that are politically sensitive, far from Europe, or in many cases, both.

As Europe searches for alternate suppliers, Russia has begun to search for alternate purchasers. Russia launched the Power of Siberia pipeline in 2019 to increase sales to China. A recent Sino-Russia agreement will see an additional 10 bcm flowing to China annually, rising to 38 bcm upon completion of the system, including links to the existing pipeline from Sakhalin Island.60 Besides the usual consternation in Washington, DC, this has raised concerns that U.S. leverage over China will decrease, especially given the importance of LNG sales to China.61

These gas fields are in East Siberia and the Far East and are not connected to the European pipeline system. Still, as these pipelines will be used to increase sales not only to China but also to deliver LNG to Japan and elsewhere in Asia, it decreases the relative importance of European sales. Over time, Russian gas companies, first and foremost Gazprom, are likely to shift capital expenditures to eastern fields. It should be noted that sales to Japan are significant and continue, despite Western sanctions and the unresolved status of the Kuril Islands since World War II. Any Russian–Japanese political breakthrough could open a floodgate of gas sales, given Japan’s close proximity and very severe lack of energy.

It is impossible for existing suppliers of natural gas via pipelines to make up for the shortfall resulting from decreasing or cutting off Russian gas in the policy-relevant future. However, some analysts have suggested that LNG could hold the answer.

Is LNG the Answer?

The ability to transport LNG via special tankers from gas fields in the United States and other countries has been touted as the savior of Europe, but there are several issues that may limit the amount of relief it actually delivers. LNG is much more expensive than pipeline gas as it must be liquefied at a very low temperature (−265º F) and then transported over long distances, consuming a considerable amount of energy, both to power the ship and to keep the LNG cold. Further, modern shipbuilding notwithstanding, some LNG (0.1–1 percent per day) would be lost to evaporation. At the destination port, LNG must be regasified and injected into the pipeline system.

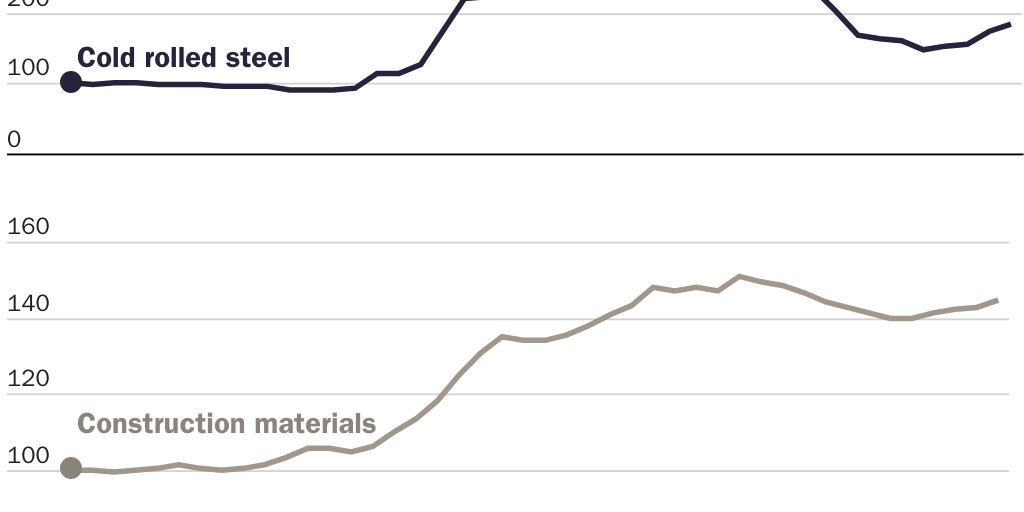

Construction of liquefaction and regasification facilities requires many years to complete and massive, multibillion-dollar capital expenditures. Given recent dramatic price increases in steel and other materials partly because of sanctions on Russia (see Figure 8), construction costs are likely to be much higher and put more upward pressure on LNG facilities’ cost, which in turn would be passed on to consumers.

Also, historically these facilities have been plagued by sizable cost overruns. For instance, Chevron’s massive Gorgon project in Australia was originally budgeted at $34 billion but ultimately cost over $54 billion upon completion in 2016.62 Rising costs, particularly of metals, many of which Russia is a large supplier, have stalled several LNG export projects in the United States, limiting further capacity growth.63 Higher LNG prices may be necessary to make further capacity expansion economically viable.

Given the massive capital expenditures and long payback periods, LNG suppliers have wanted buyers to make multidecade commitments to shield them from exposure to fluctuations in feeder natural gas prices. Because of a shortage of energy resources, North Asian buyers have been willing to do so, such as the recent 18-year commitment of Korea Gas to buy 1.58 million tons of U.S. LNG annually from BP.64 Europeans have been reluctant to enter such commitments, in large part due to a cheap, reliable gas supply from Russia. As a result, as much as 70 percent of world LNG production is locked up in long-term contracts.65 This means that the cost of replacing pipeline gas with LNG would be even higher, since supply not under contract is very limited.

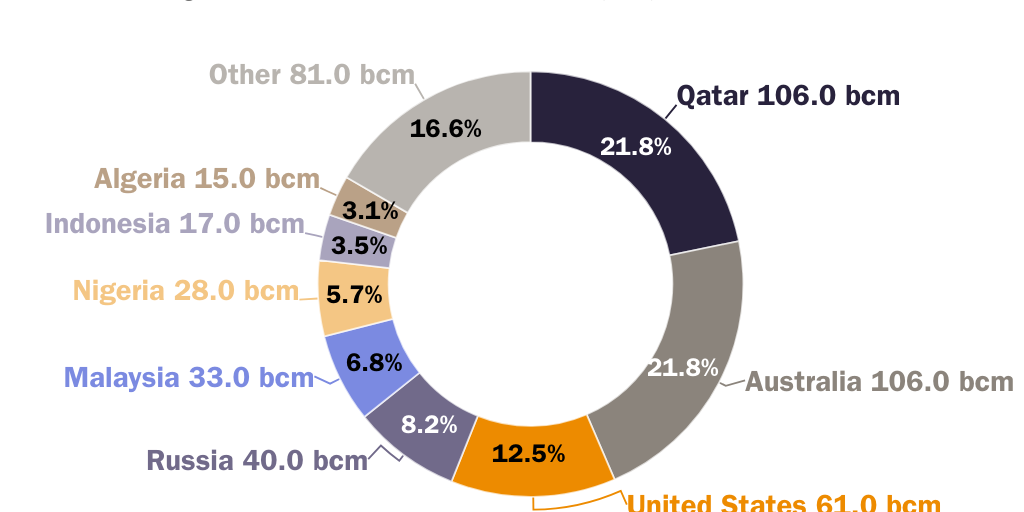

However, even without such supply arrangements, there simply is not enough LNG in the world. As shown in Figure 9, in 2020, global liquefaction capacity was 488 bcm, or 447 bcm ex-Russia, meaning that to replace Russian gas, Europe would need to import 41 percent of all exported LNG. Given the portion of LNG that is under long-term contracts, this would not be possible. Global capacity in 2022 certainly rose somewhat, perhaps to 517 bcm, but this does not change the fundamental calculus.66

Additionally, LNG transport vessels are expensive (more than $200 million) double-hulled vessels that must maintain very low temperatures and prevent gas ignition.67 Many vessels are on order, but currently, there are an estimated 681 vessels with total capacity of 103 bcm.68 In other words, the entire global LNG fleet would have to visit Europe nearly twice a year to compensate for the total loss of Russian gas.

Can More U.S. Liquefaction Make Up the Slack?

Last winter, Europe attracted LNG cargoes, albeit at very high prices, further increasing inflation and economic damage. These cargoes otherwise would have gone to countries that are poorer and cannot afford to pay the new, much higher prices, such as Bangladesh and Pakistan.69 This pain is intensified by weak emerging market currencies since oil and gas are priced in dollars.

There is another unintended victim of the chaos in natural gas markets: New England. Because of state and local regulations and the efforts of environmentalists and “not-in-my-backyard” activists, the region is largely not connected to huge gas fields in Appalachia.70 As such, it is forced to buy and regasify LNG for heating and electricity. This situation is made even worse by the Jones Act, which requires cargoes between U.S. ports to be transported in U.S. vessels.71 This law, intended to protect the U.S. merchant fleet, forces New England to compete with foreign buyers of non‑U.S. LNG. Prices last winter spiked above $30 per million British thermal units (MMBtu) from the already high-for-the-United States $7–$8 per MMBtu.72 The winter of 2023–2024 is likely to be worse, as in 2022, Russian gas was still flowing to Europe, albeit in lower amounts.

Despite aggressive expansion of export facilities in Qatar and the United States, as shown in Figure 10, LNG exports cannot make up the shortfall of Russian pipeline gas. To the extent that they help, the cost is very high to buyers, and many are simply priced out of the market. LNG exports are constrained by flat natural gas production in the United States or political pressure resulting from rising gas prices. The number of tankers and regasification facilities also limits the amount LNG can contribute to the European energy balance.

Thus, it is unlikely that Europe can attract significantly more LNG cargoes because of supply constraints and increasing demand from China as well as political and migratory repercussions from bidding cargoes away from poorer countries. There is little reason to believe politicians’ anger at U.S. companies profiting from high LNG prices in Europe will lead to any meaningful relief.73

The Costs of Denying Economic Realities

Keeping Russian gas out of the market would have serious effects. Europe would be hit the hardest, as it is the direct buyer of this gas, but the effects would be felt worldwide. Exporting LNG would cause natural gas prices in producing countries to rise along with those of Europe, and diverting LNG cargoes from poorer to richer countries, like those in Europe, would hurt the economies and peoples of the former.

In the United States

There is little indication that U.S. producers can replace Russian gas in Europe in the policy-relevant future. However, significant increases in U.S. LNG exports, if they happened, would put upward pressure on U.S. domestic prices given level gas production.

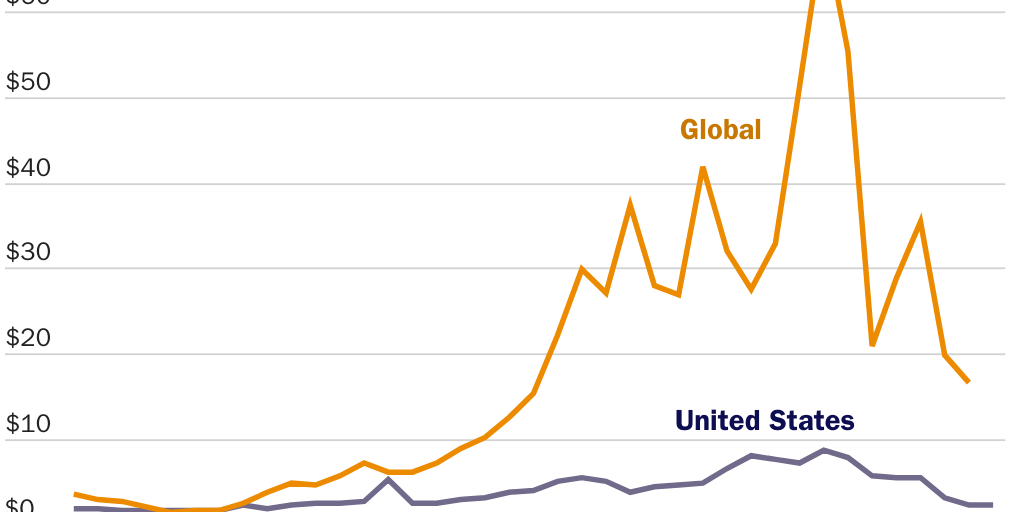

Because of widespread use of fracking and horizontal drilling, there has been an excess of gas supply over demand in the United States. Since natural gas markets are regional (in the absence of LNG, there are no arbitrage opportunities), in the decade following the 2007–2008 global financial crisis, U.S. natural gas averaged $3.37 per MMBtu with low volatility, compared to $8.37 per MMBtu with much higher volatility in Europe.74 This has been a tremendous tailwind for the U.S. economy: Some 43 percent of U.S. electricity capacity is gas-fired. Nearly half of U.S. homes are gas-heated, to say nothing of the other uses of natural gas from nitrogen fertilizer to feedstock for countless plastics, resins, and other materials.

It has also been a tremendous incentive for U.S. producers to invest in liquefaction. The export of LNG changes the situation by linking far-flung markets and opening gas price arbitrage. Whereas the pipeline natural gas market is geographically constrained, the LNG market is more like the market for oil: a fungible commodity sold on global markets. For exporting U.S. LNG to make economic sense, higher gas prices in Europe are needed. This could be achieved if Russian gas does not supply Europe. Taking that much supply off the market has driven prices much higher. Since U.S. gas production is currently flattish, as the proportion of U.S. production converted to LNG increases, less gas would be available for U.S. consumers, causing domestic gas prices to also rise. This increase in input costs for the rest of the economy would reduce U.S. competitiveness.

U.S. natural gas prices already have moved higher as more U.S. gas is converted to LNG and exported. PJM, North America’s largest regional electricity transmission organization, serving 13 states and the District of Columbia, noted that LNG exports to the EU and UK in the first half of 2022 “increased 66% over the 2021 annual average, primarily from U.S. exporters with operational flexibility. This international natural gas demand is a new competitor for domestic spot-market consumers, resulting in significantly higher fuel costs for PJM’s natural gas fleet.”75

Additionally, expectations of even more U.S. gas being diverted to Asia and Europe have driven prices higher. In March, President Biden promised together with international partners to “strive” to deliver at least 15 bcm in additional LNG to the EU in 2022 and 50 bcm of U.S. LNG annually by 2030.76 U.S. LNG exports increased at a rapid clip in 2022 and may have reached 118 bcm for the year, depending on the effect of downtime for maintenance or capacity going offline for other reasons.77 Exporting such a large portion of domestic gas would have a significant effect on prices. This has been one of the drivers of the increase in gas prices we saw, particularly in the first half of 2022.

Further evidence of the effect of LNG exports on domestic gas prices is the Freeport LNG facility, which represents some 15 percent of total U.S. LNG capacity.78 In June 2022, an explosion took the facility offline, reducing upward pressure on U.S. gas prices (i.e., total effective domestic supply rose, pushing the market clearing price down). Restarting the facility has had the opposite effect.

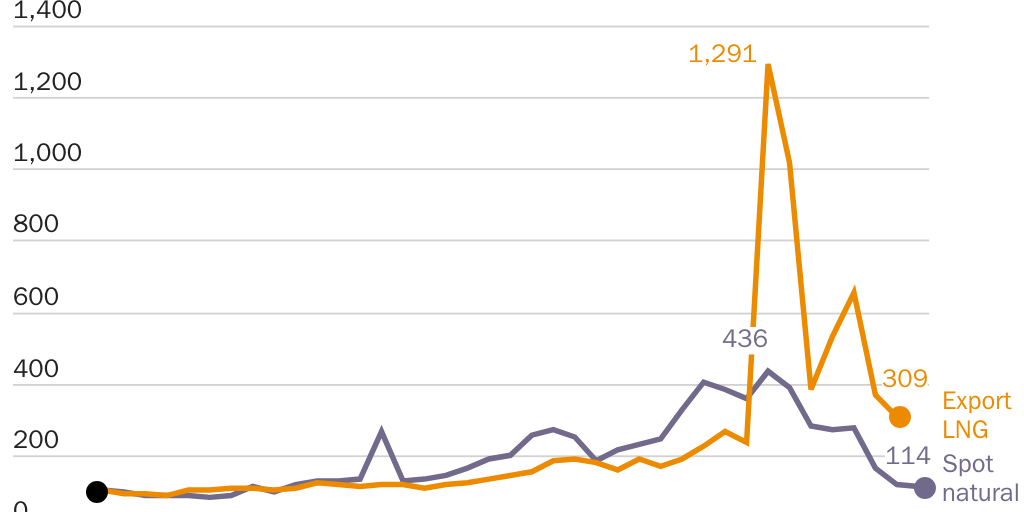

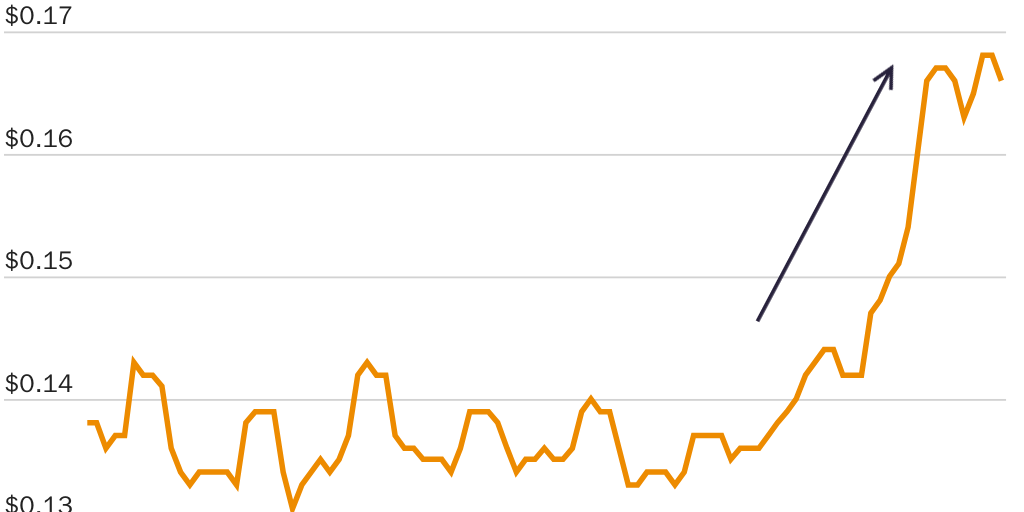

It is noteworthy that spot gas prices are very volatile. In 2023, the winter in the lower 48 states was warm, reflected in above average natural gas inventories, driving spot prices down (see Figure 11).79 Also, high oil prices have led to more fracking, especially in the Permian Basin, leading to increased output of associated natural gas. However, spot prices do not reflect the overall contract price trend (which is higher) cited by PJM.

The growth rate of gas production has slowed over the past few years. In part, this was due to the COVID-19 pandemic, which caused lower economic activity and thus decreased demand and reduced the number of working crews. Several fields could expand, but there is little spare pipeline capacity in part because of political factors: recent changes in federal permitting and regulatory frameworks and opposition from local governments, environmentalists, and not-in-my-backyard activists have stymied pipeline capacity expansion.80

Another factor contributing to flattish gas output is the Biden administration’s reluctance to grant drilling permits as part of its strategy to combat climate change. Approval of new oil and gas drilling leases by the Bureau of Land Management has plummeted.81 Moreover, companies are reluctant to launch new, expensive production projects when current government policy calls for oil and gas to be phased out in a few years.82

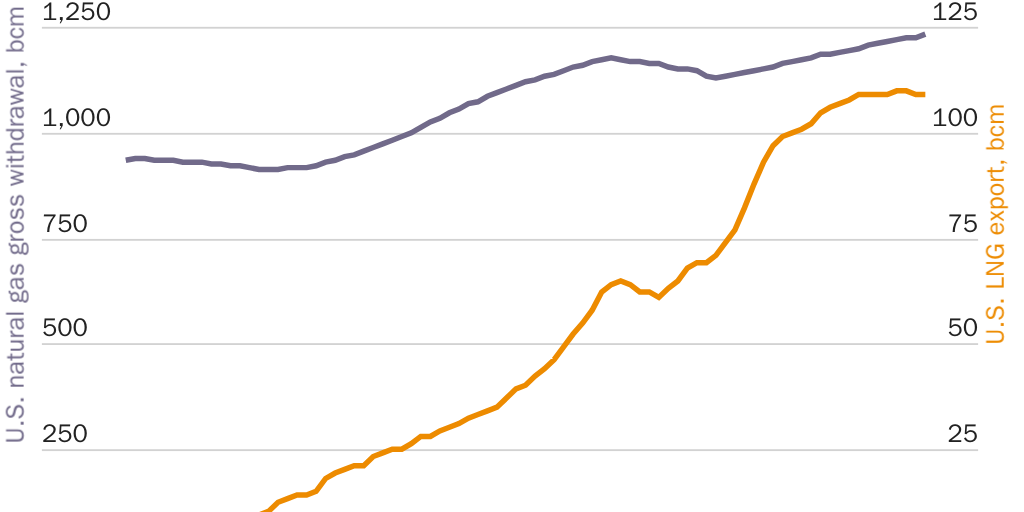

At the same time, growth of LNG exports has been exponential from practically zero six years ago (see Figure 12), although they still represent only 10 percent of gas production. Nevertheless, the trend is striking and confirms that rapidly rising LNG exports will put upward pressure on U.S. domestic gas prices.

Still, companies and governments continue to spend billions building new and expanding existing liquefaction facilities. In the United States, five facilities are under construction in Louisiana and Texas that are to bring export capacity from 111 bcm per year to 156 by the end of 2024.83 While these capacity additions are impressive, they are insufficient to replace the lost Russian gas, especially considering that global demand for gas will continue to rise.

United States: Secondary Effects

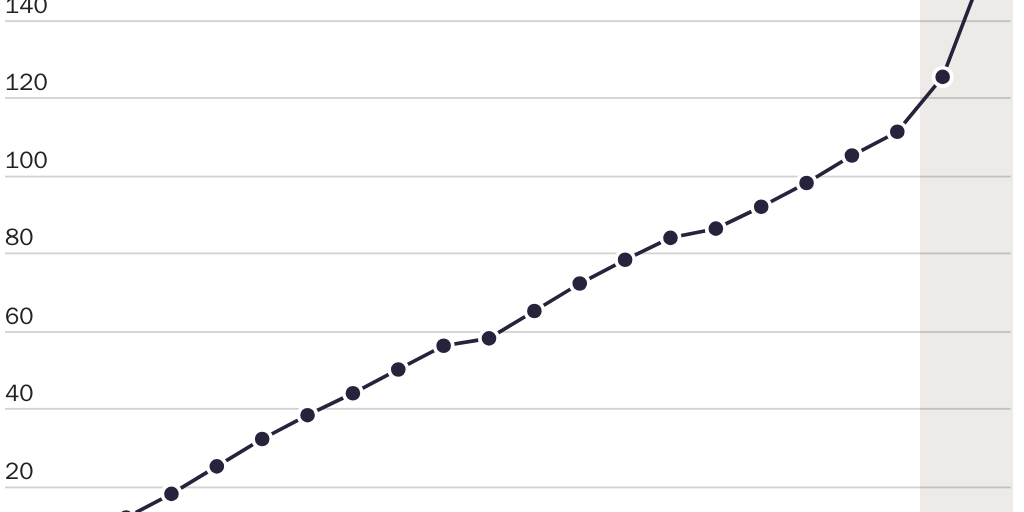

Any policies that divert U.S. natural gas to LNG for export would adversely affect the U.S. economy. For example, three-fourths of the production cost of ammonia is natural gas.84 As European spot gas prices began to jump in 2021, so did ammonia prices, rising from $250 per ton to over $1,300 per ton, even before the escalation in Ukraine, as regional ammonia markets have been linked by tankers for many years.

Featured Video

Similar price hikes can be expected for products where natural gas is the feedstock, such as fabrics (nylon, polyester), medicines, plastics, paints, and resins as well as intermediate feedstocks (methanol, ethane, formaldehyde, acetic acid, etc.). All these products would rise in price. Since many of these products are intermediate goods used in production of final goods, the inflationary effect is likely to span across the economy in dramatic fashion.

Electricity

Since gas fires around 38 percent of U.S. electricity output, electricity prices are sensitive to gas prices. In recent years, gas prices have been low and stable, because of fracking and horizontal drilling (see Figure 13). However, in early 2021, as gas prices began to rise, so did electricity prices. Besides LNG exports driving up prices, a major cold snap in the South Central United States resulted in more demand for gas and electricity and restricted gas flow.85 (It was during this time that kerosene-burning helicopters famously deiced “green” windmills.) Electricity and natural gas prices spiked to unprecedented levels.

Although electricity prices have a very pronounced seasonality, with hot summer temperatures driving up prices in counterphase to gas prices, the trend is clear: electricity prices have been rising and look set to rise further as the price of gas increases (see Figure 13). The U.S. Energy Information Administration (EIA) expected the average winter 2022–2023 electricity price to rise 10 percent year on year to $0.148 per kilowatt-hour (kWh). According to the U.S. Bureau of Labor Statistics, the average urban electricity price from October 2022 through March 2023 was $0.166 per kWh, an increase of 24 percent year on year, as shown in Figure 14. (These are very moderate increases considering the movement in gas prices, but to be fair, increases take time to filter through to long-term contracts. Also, since nearly all U.S. electric utilities are monopolies, public service commissions set rates and meet infrequently.) This masks considerable regional variation in tariffs, from Washington State ($0.101 per kWh) to Hawaii ($0.335 per kWh) as well in average monthly consumption, from 1,192 kWh in Louisiana to 531 kWh in Hawaii.86

According to the May 2023 EIA monthly report, in 2022 the average residential tariff rose 10.7 percent to $0.151 per kWh, costing consumers an additional $29.3 billion, or $240 per household.87 (The Bureau of Labor Statistics reported the average at $0.159 per kWh indicating an additional $30.9 billion, or $252 per household.)

For the first four months of 2023, residential electricity tariffs averaged $0.167 per kWh. If the average tariff for the full year remains at this level and consumption rises a modest 2 percent, then the added cost for 2023 would be $24.5 billion, or $200 per household. In total, residential customers could pay an additional $53.8 billion, or $452 per household for 2022–2023. Consumers who use more expensive, less efficient electrical heating would suffer more while those with gas would see less of an impact.

While these numbers may not seem catastrophic in isolation, in total they represent a sizable impact, especially for low- and middle-income households, more so given the higher inflation the United States has experienced lately.

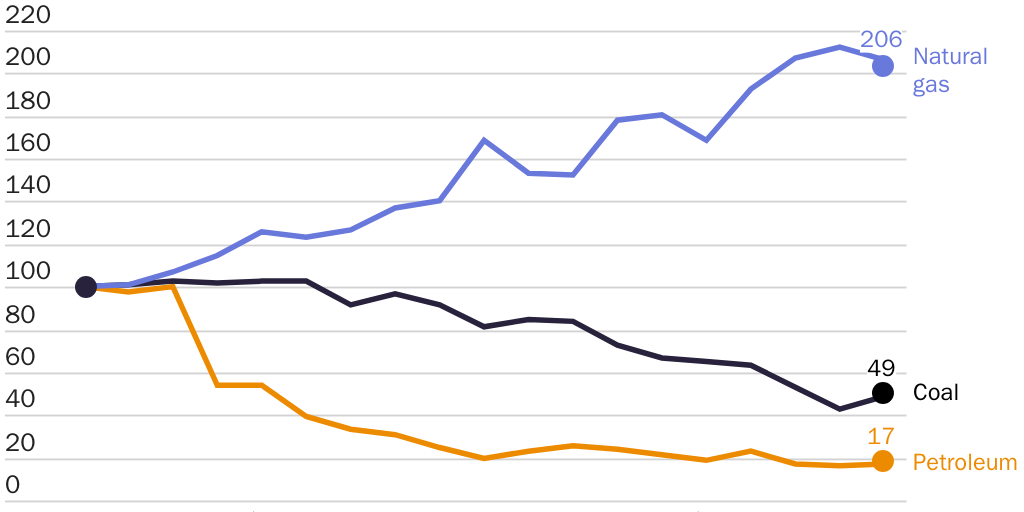

Similar to Europe, to produce electricity the United States has been using more clean burning gas and phasing out dirtier coal and petroleum (see Figure 15). As a result of soaring gas prices, more coal- and petroleum-fired electric capacity is being brought back online. Since there is an imperfect energy arbitrage among fuel sources, prices have soared, with Central Appalachia coal tripling from $59.50 per short ton in 2021 to $200.88 Not only will this put additional pressure on electricity prices, but there also is a strong negative externality: burning coal and petroleum puts more particulate pollutants into the atmosphere, adversely affecting our health and well-being.

Commercial electricity consumption (35 percent of the total) and industrial (26 percent) combined are more than residential (39 percent). Therefore, electricity prices driven up by rising fuel costs could potentially do even more damage to the U.S. economy even though commercial and industrial clients pay less (using EIA data, $0.126 and $0.085 per kWh, respectively, in 2022—up 11.8 and 17.7 percent—compared to $0.151 per kWh paid by residential customers).

According to the EIA, total electricity consumption in the United States was about 4.05 trillion kWh in 2022, the highest amount ever recorded and an increase of 6.4 percent year on year.89 Excluding direct electricity sales (e.g., generated and consumed on site by industrial users), sales rose 2.7 percent to 3.91 trillion kWh, surpassing pre-COVID-19 levels and also a record. The cost of this electricity rose 15.6 percent year on year, or $66.0 billion. There are many factors that contributed to the increase, including reckless fiscal policy that drove up the price of inputs across the board, but much of it can be attributed to rising natural gas prices stoked by pipeline closures and sabotage, and the accompanying rise in the prices of other fuels due to arbitrage. Thus, American consumers would pay an additional $66.0 billion in direct purchases of electricity and costs passed on to them by the industrial and commercial sectors. Electricity tariffs for the first four months of 2023 do not suggest relief for consumers for the year.

Heating and Gas

According to the EIA’s Winter Fuels Outlook, the nearly half of U.S. households that heat primarily with natural gas were to predicted to have spent 28 percent more than they spent in the winter of 2021–2022 in case of an average winter and the 41 percent of households that heat primarily with electricity were predicted to have spent 10 percent more, albeit from a higher base.90 Although spot prices take time to filter through to tariffs, the writing is on the wall: Consumers have paid more to heat their homes or have lived in colder homes, or both. Similar effects can be expected in other sectors of the economy.

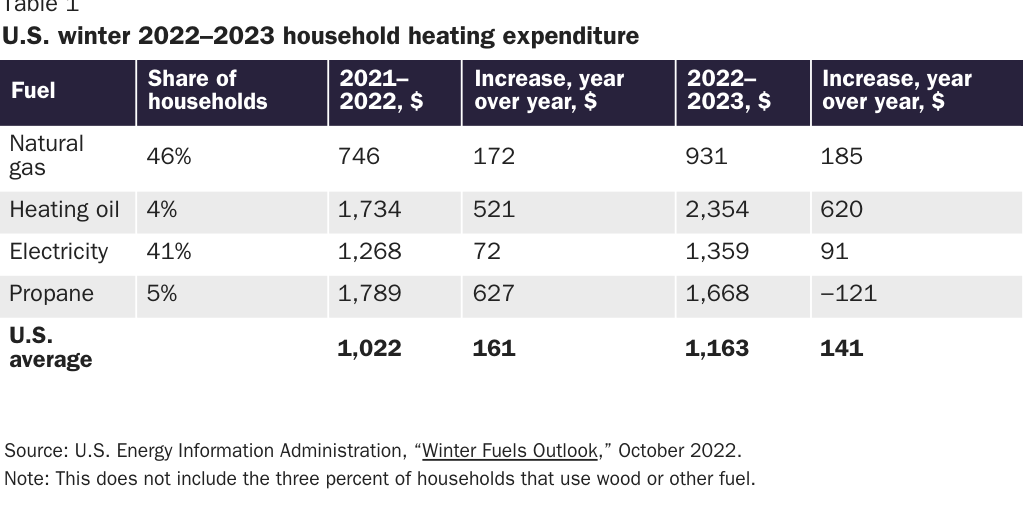

Cost increases for households heating with oil were expected to be even greater, as shown in Table 1.

This $17.3 billion, or $141 per household, represents funds that might not have been spent on other consumption and thus likely could have a material adverse effect on well-being, particularly of lower- and middle-income households, and could come on top of the $161 increase in the 2021–2022 winter. In total, for the two winters since the Russian invasion, the average household may have spent an additional $302 on heating.

Official information about households that heat with gas and electricity, 87 percent of the total in the United States, has not been released. However, electricity prices from October 2022 through March 2023 were up, on average, 14 percent year on year. It remains to be seen whether the warmer winter in most parts of the United States was sufficient to compensate for this large price increase or if heating bills increased more than the 7 percent that the EIA forecast.

The same is true for residential gas prices that rose, on average, 21 percent year on year in 2022.91 It seems less likely that the warm winter was enough to overcome this large increase, meaning a greater increase in heating bills than the 14 percent that the EIA forecast. In any event, flat domestic gas production and rising LNG exports presage even higher gas prices for Americans. Although very seasonal and volatile because of cold snaps, prices broke out in 2021, long before the invasion. The trend looks set to continue, regardless of year-to-year variation in weather severity.

It is also worth noting that increasing the price or limiting the availability of gas would hurt lower income households much more because they spend three times more of their income on energy than non-low-income households do. Sixty-seven percent of low-income households, disproportionately with minority and elderly members, face a high energy burden.92 Besides heating, residential customers also use gas for cooking, heating water, and drying clothes, meaning that the total impact will be greater.

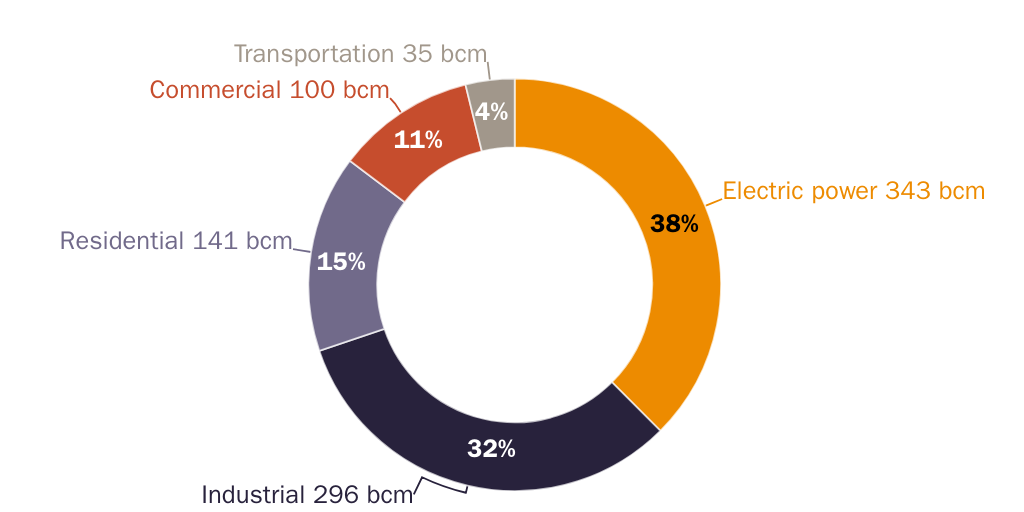

In addition to residential use of gas, there is also the considerable cost of heating in factories, stores, schools, industrial processes, etc. Figure 16 shows that residential use, while significant at 15 percent of total use, is roughly a third of industrial (32 percent) and commercial (11 percent) combined. In 2022, natural gas prices to commercial and industrial consumers rose 29 percent and 44 percent, respectively, although the latter represents only 14 percent of sector sales.93 The added cost to the commercial and industrial sectors in 2022 may have exceeded $37 billion, especially given that the volume of gas consumed increased by 5.5 percent.94 For 2023, only two months of price and volume data are available, making forecasts difficult. However, in light of the trends previously discussed, an increase of less than $37 billion would seem unlikely.

In total over the last two years, the added annual cost of heat and electricity could average $754 per family, or $92.2 billion for the nation. Again, these are only the direct residential heating and electricity costs and do not consider the added costs to companies, schools, and other facilities that will be passed on to consumers. Also, these increases will be higher if gas prices continue to rise.

These trends look set to continue and intensify. As LNG producers seek higher prices for their cargoes abroad, domestic market prices could become permanently higher simply because of demand chasing reduced supply unless U.S. gas production increases. In August 2022, Europe had to offer a premium to Asian markets to attract LNG cargoes away from Asia, where LNG already traded at a premium to U.S. markets, adding more pressure.95 If U.S. policies are not changed or at least softened, politicians will face increasingly tough questions from voters because of their policy choices. Isolation from the volatility in foreign natural gas prices has been an economic and political blessing for the United States. Importing that volatility would be a curse.

In Europe

In Europe, fuel prices have spiked, with the cost of imported gas more than tripling year on year to some €400 billion in 2022, causing high inflation in food, electricity, and heat prices.96 EU inflation in February 2023 was 9.9 percent year on year, less than the 11.5 percent in November 2022 but still very elevated, and some components show very high levels of inflation (e.g., energy, food, alcohol, and tobacco at 15 percent).97 There are also large regional differences, with the Baltic states and Poland experiencing inflation above 17 percent.98

Featured Media

In the fourth quarter of 2022, EU bankruptcies spiked 26.7 percent, particularly in sectors that are more sensitive to fuel prices, such as transport.99 In Germany, bankruptcies rose 19.5 percent in the third quarter, the most since 2008, with a 0.4 percent contraction in GDP, and are expected to increase 15 percent in 2023 with industry in recession in the first half of the year.100 The German government has imposed caps on electricity and gas prices representing 80 percent of average consumption, part of a €200 billion package to counteract the damage done by the war and economic sanctions.101 Whether this huge drag on German public finance will alleviate economic suffering remains to be seen.

Throughout Europe, red-hot inflation for nearly all goods and services, and the subsequent decline in living standards resulting from some basic goods becoming unaffordable, led to protests and strikes.102 The decline in production caused by strikes in turn will lead to lower output and higher prices.

Large swathes of steel, zinc, aluminum, and ammonia production have been shut down, with many more facilities to follow, some forever, leading to what has been termed “de-industrialization.”103 To save fuel, the EU and member states asked Europeans to be colder in winter and hotter in summer, to take shorter and fewer showers, and to spend more time in the dark.104 The potential for major political unrest has remained high since elevated inflation has showed no sign of abating, and the economic situation continues to worsen.

Undaunted, European leaders have maintained that such costs are worth it to save Ukraine. “We will never be able to match the sacrifice that the Ukrainians are making,” European Commission President Ursula von der Leyen remarked, adding, “You’ll have your European friends by your side as long as it takes.”105 Despite protests across the continent and the serious potential for social unrest in the coming months, EU bureaucrats have continued to justify open-ended sacrifices from Europeans. “We will continue to stand with Ukraine,” said EU foreign affairs chief Josep Borrell. “We cannot reduce our commitments or lessen our resolve, even when the price goes up.”106

In Germany, Chancellor Olaf Scholz said in August 2022 and has maintained that Germany “will keep up this support, reliably and, above all, for as long as it takes.”107 In France, protests became increasingly violent in 2023. The spark that set them off was the bill raising the retirement age to 64 and that it was adopted without legislative approval (i.e., by the bureaucracy). Fundamentally, this change was required due to massive budget shortfalls, which have been exacerbated by sanctions driving up prices and shutting down businesses.108 Germany has seen massive strikes by workers seeking higher wages to tackle the rising cost of living.109 In addition to rising prices caused by sanctions, shuttering of some German industrial capacity has put pressure on the economy. Such protests and actions have the potential to intensify if citizens feel no relief.

European farmers began protesting their governments’ policies that have allowed Ukrainian grain to flood the markets due to lower input prices and the absence of strict EU environmental regulations. In a sign that elected leaders may have had to respond to their electorates, Poland, Hungary, and Slovakia banned Ukrainian grain imports.110 As of July 2023, this had been the exception but could become the rule if discontent escalates.

Migration to Europe from the developing world has risen to the highest level since 2015 and may increase further if flows of gas and gas-derived products continue to be disrupted.111 This surge has been driven in part by food insecurity because of the war and sanctions and could have been worse if not for the UN Black Sea Grain Initiative.112 If Russian grain exports are expedited by granting RusAgroBank access to SWIFT, or the Society for Worldwide Interbank Financial Telecommunication, as well as Western insurance and logistics services, as per a UN memorandum of understanding, food insecurity and migration should further abate.113 If the Grain Initiative is not extended, the situation could materially worsen.

The negative effects of the war on the economy and inflation have put considerable pressure on European currencies, especially since commodities, oil, and gas are priced in dollars (see Figure 17). This in turn makes the economy and inflation even worse. Although there are other reasons for weak currencies, such as loose fiscal and monetary policy, the war and sanctions are major factors.

In the Global South

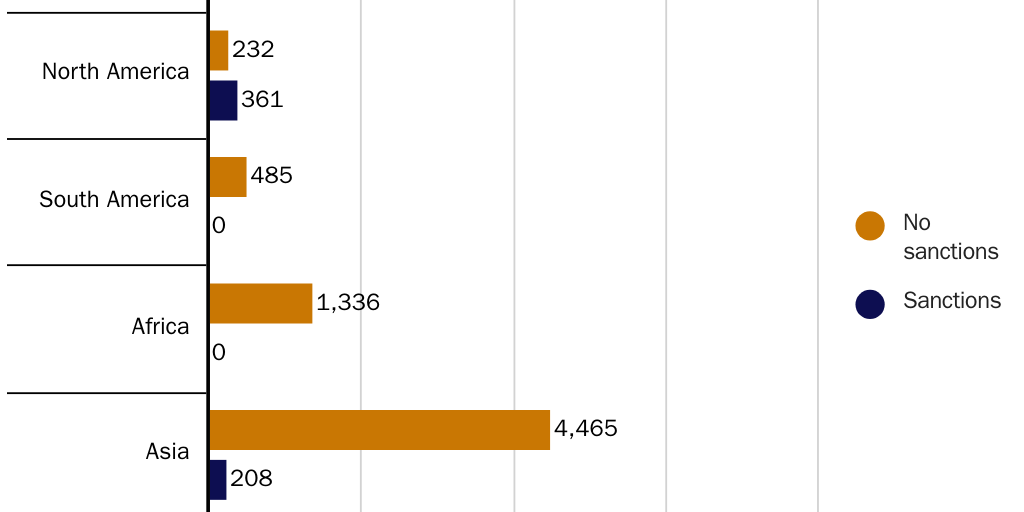

In those countries that have imposed sanctions on Russia, government officials and the media claim that the world is united in sanctioning Russia and that Russia’s invasion of Ukraine was unprovoked and unprecedented. Both these statements are articles of faith in NATO-aligned countries. However, they are not accepted in the nonsanctioning countries, most importantly the Global South, China, and India, which represent 86 percent of the Earth’s population (see Figure 18).

Many of these countries have refused to sanction Russia or even condemn what they see as a regional conflict not affecting them. “A position of neutrality” has been repeatedly expressed by the president of Mexico, who also pointed out “politics was invented, among other things, to avoid war.”114 The world’s largest democracy, India, continues to buy Russian oil and weapons because “we make judgements which are reflective of both our future interest as well as our current situation” and “for multiple decades, western countries did not supply weapons to India and, in fact, saw a military dictatorship next to us as the preferred partner.”115

Countries in the Global South have been actively pushing back against attempts to force them to toe the sanctions line. Seated next to U.S. Secretary of State Anthony Blinken, South African Minister Naledi Pandor crystalized many countries’ position on secondary sanctions: “And one thing I definitely dislike is being told ‘either you choose this or else.’ When a minister speaks to me like that, which Secretary Blinken has never done, but some have, I definitely will not be bullied in that way, nor would I expect any other African country worth its salt to agree to be treated.”116

Such sentiment was widely expressed at the UN General Assembly in September 2022. The president of Argentina said: “I want to call attention to the use of unilateral coercive measures. According to the UN Charter, the only legitimate sanctions are those imposed by the Security Council.”117 This was echoed by many others, including the president of Brazil: “We support all efforts to reduce the economic impacts of this crisis. But we do not believe that the best way is to adopt unilateral and selective sanctions that are inconsistent with international law.”118

That countries such as South Africa and Brazil openly make such statements should serve as a wake-up call to U.S. policymakers as they are two of the largest economies in the Global South and members of BRICS, a grouping of countries striving to champion emerging markets. This is likely to continue to embolden other nations to pursue a more independent course. If the United States wants to retain influence, avoiding the use of threats and economic penalties to force other countries to sanction Russia and to stop buying Russian goods and services would seem prudent.

The Global South resists restrictions on trade first and foremost because it hurts its economic interests, and in some cases could result in humanitarian crises, but also because it fears becoming the target of such sanctions. If the United States continues to pressure these countries to impose sanctions or simply not buy Russian products, its relationship with them will worsen. For short-term gains, U.S. policies may lead others in the Global South to follow India’s path, through the Cold War to today: nominally neutral but closer to Russia.

Another consequence of massive shifts in European energy consumption for the Global South has to do with where additional supplies would come from. To replace Russian gas, LNG would be sourced from countries that have questionable policies and human rights records, such as Qatar and Saudi Arabia, since their production and transportation costs to Europe are lower than those of their American and Australian competitors. Until recently, European leaders were criticizing such countries for everything from near slave-like labor conditions to murdering journalists. Some are accused of directly financing terrorism while others project soft power (e.g., construction of madrassas and supporting radical groups). What will be the effect of directing more money to them? Are they more or less likely to change their policies? Will they use the additional funds to curtail or expand behaviors undesirable to the West? To punish Russia, Europe may rush to embrace bad actors and bad policies, leaving everyone in a worse situation. Few have considered the long-term implications of this radical realignment of global energy flows.

By and large, Russian pipeline gas flows cannot be redirected, whereas LNG exports from the Middle East, Africa, and Asia can go anywhere. In this situation, it is possible that Russia may offer carrots in the form of money, advanced weaponry, and political concessions to induce other LNG exporters to redirect cargoes away from Europe to support Russian pipeline gas flows.

If such conversations are not taking place in diplomatic circles, they are most certainly being contemplated, more so given many of these nations’ desire to reduce U.S. influence on their domestic and international affairs. This is yet another reason why the United States and the West should rethink their politics relating to gas, LNG, and Europe.

For the Environment

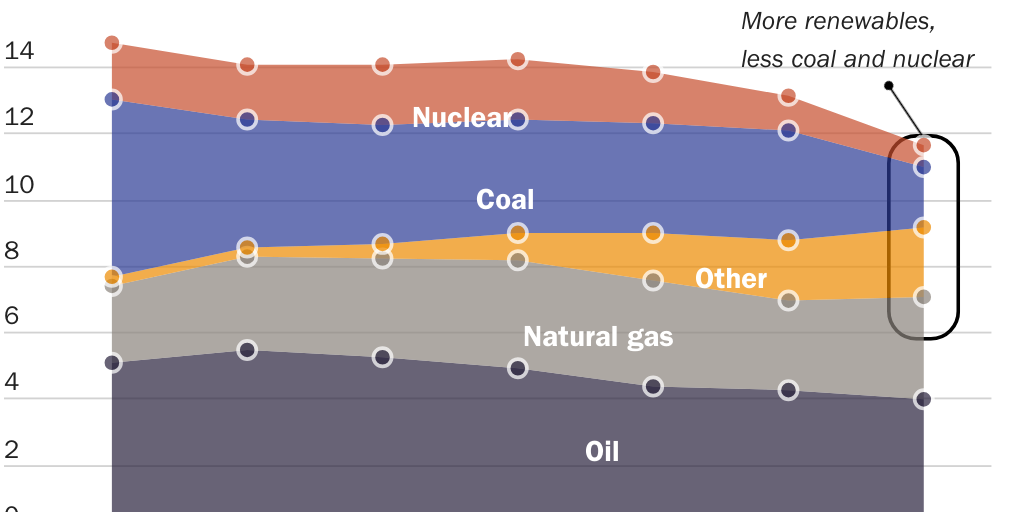

Given the success of its gas-purchasing relationship with Russia, Germany decided to shut down coal-fired electricity capacity and scale back nuclear power, especially in the wake of the Fukushima disaster (see Figure 19). This, coupled with overly rosy projections of the contribution from “green” energy, increased the importance of the Germany-Russia relationship even further. The economic performance of Germany and other European states has been built on the stability and competitiveness of Russian gas.

With the recent closure of its last three nuclear power plants, the energy balance in Germany will deteriorate further and become less green.119 Similar problems can be expected across Europe, especially given that 17.5 percent of French nuclear capacity is still offline due to maintenance and repairs.120 These problems have been exacerbated by the dry and hot summer in 2022 that resulted in lower water levels, causing problems and increasing costs in delivery of coal to power plants.121 More importantly, many hydropower stations were forced to shut down, resulting in the loss in 2022 of 63 terawatt-hours (TWh).122 Barring an especially wet spring, hydropower’s woes are set to continue. The loss of 119 TWh from these two sources could be very significant due to intermittency and other problems inherent in solar and wind generation.

From an environmental point of view, gas delivered by pipeline is superior to LNG, given the excess energy waste and carbon emissions arising from liquefaction, long ocean voyages with cargo requiring very cold temperatures, and regasification. Without Russian pipeline gas, Europe would require increased use of less green alternatives, such as coal. Indeed, not only did the share of coal in electricity generation increase in 2022, but coal mining in Europe also has been expanded, including of lignite, the dirtiest and lowest grade, angering the Greens.123 Much of the imported coal could be of lower energy content, meaning more must be burned, and must be transported from farther away (e.g., South Africa, Australia), entailing higher transport costs and even more carbon emissions.

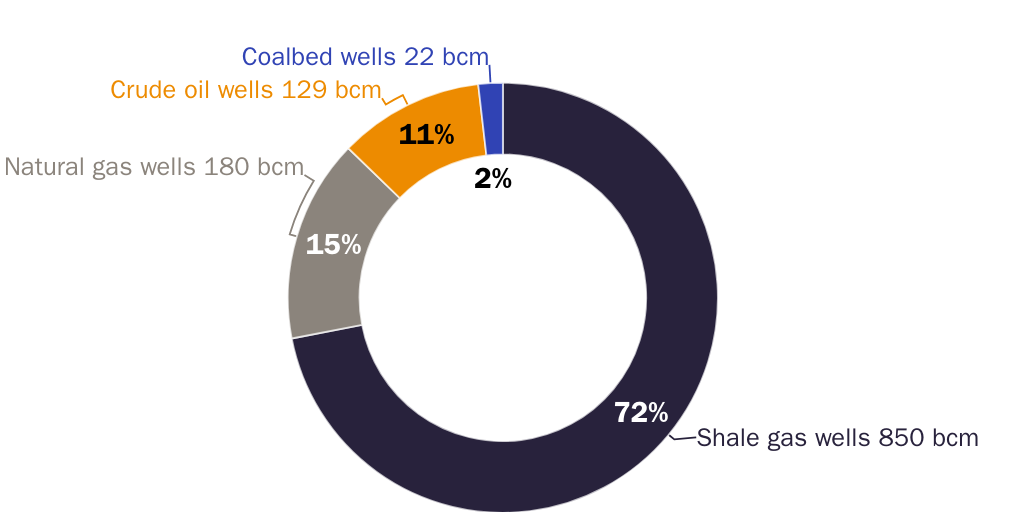

Importing more U.S. LNG has consequences that European Greens theoretically abhor. As shown in Figure 20, the vast majority (72 percent) of the natural gas feedstock for LNG is produced by fracking hard rock deposits with water and various chemicals, which then are discarded. Environmentalists have historically denounced this natural gas extraction method as irresponsible.124 The point is not to say that environmental considerations should trump any political goal. Rather, it is to remind policymakers that these are unavoidable tradeoffs posed by present policies.

Instead of straightforwardly acknowledging these tradeoffs, European states have relied on dubious accounting approaches. For example, the EU and UK classify burning wood as carbon-neutral, despite all the carbon soaked up by trees over decades being released in an instant when they are burned. This represents much of the so-called renewable energy in European energy balances.125 There is massive cutting of forests in Europe to generate electricity in stations that have been converted from coal. The switch to coal was key to the Industrial Revolution but also ended deforestation in Europe that had become serious. Hopefully leaders will pursue different policies before the reforestation that Europe has experienced for 30 years reverts to deforestation.126

Worse still, forests in North America are being clear-cut to make combustible pellets that are shipped across the Atlantic. If burning trees was not bad enough, this requires consumption of additional fuel both to make the pellets and for ocean voyages. Also, whole trees are used, not waste wood from logging or mills.127 This not only consumes considerable energy but also squanders the beauty and other uses of our forests.

Conclusion

This paper has outlined the hard and mostly immutable economic realities resulting from the Russian invasion of Ukraine and the West’s response to it. These realities cannot be overcome by political will. Only a portion of Russian energy can be replaced in any reasonable time frame, and even then, it would be at great cost to economic well-being. U.S. LNG exports could help but cannot replace Russian supply and likely will result in higher prices across the board for Americans. The damage to the global economy, already significant, will be more so over the medium term.

In the developing world, food insecurity and elevated migration are likely. In the developed world, Europe is likely to bear the brunt of escalating prices and shortages, meaning a highly diminished quality of life and partial deindustrialization. Unelected EU bureaucrats and many European politicians proclaim that these costs are worth bearing to save Ukraine. Due to falling living standards and rising costs, Europeans have begun to protest, calling for a change of course. The mild 2022–2023 winter softened the blow, but future winters could be severe, exacerbating the situation.

Political leaders should recall that their primary duty is the well-being of their people, not solving foreign problems. Thus far, there has been little pushback in the United States, but as the costs pile up, both direct (military and financial aid) and indirect (higher prices fueled by chaos in energy markets, sanctions, and embargoes), Americans are likely to question whether supporting Ukraine indefinitely is worth it. Already, many are alarmed by the prospect of nuclear war.128 Some have begun to protest.129 If U.S. policies are not changed, politicians will face tough questions from the electorate.

The United States enjoys only limited international support for sanctions against Russia. Expanding this approach by putting a cork into Russia’s natural gas supplies and arm twisting to find support in the Global South could have significant implications for the United States’ ability to forge coalitions to achieve policy goals on other issues. It also adds to the pressure to look for an alternative to the U.S. dollar.

Policymakers should focus on finding a plausible way out of the current situation. The United States, as both Ukraine’s leading benefactor and Russia’s principal adversary, is uniquely positioned to establish a path forward. The current brinkmanship, insistence on total victory, and absolute refusal to negotiate on all sides are a path to a dark future.

This conflict and its horrible consequences for all parties could go on for a long time. Continued fueling of the war and endless sanctions should give way to the seemingly lost art of diplomacy and negotiation. This paper does not have the answers to what a political settlement would look like, but the U.S. national security bureaucracy should adopt a greater sense of urgency on the matter. Even if we bracket away the prospect of disastrous military escalation, the unavoidable economic fact of Europe’s reliance on Russian gas demands consideration.

Citation

Semet, Scott. “Corking Russian Gas: Global Economic and Political Ramifications,” Policy Analysis no. 957, Cato Institute, Washington, DC, August 17, 2023.

About the Author

This work is licensed under a Creative Commons Attribution-NonCommercial-ShareAlike 4.0 International License.