There may be many moving pieces surrounding what has happened with FTX, but a general takeaway from this saga is that the fall of FTX is a firm reminder of why cryptocurrency was created in the first place: to remove the need for third party intermediaries. With that in mind, Erik Voorhees, founder of ShapeShift, said it well when he noted: “The solution [to FTX] is right in front of us: decentralized protocols solve these very problems. … There’s just such hesitancy for people to step into the actual promise of crypto because they are comfortable in these walled gardens.”

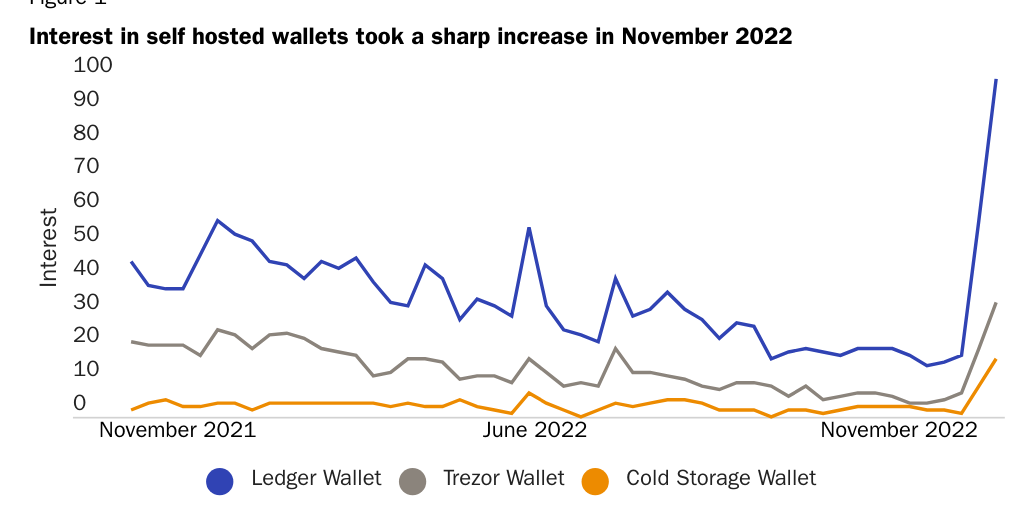

It’s certainly unfortunate that it took something like the events of the past few weeks to break through the hesitancy Voorhees described, but that seems to be what is starting to happen (Figure 1). At the very least, the rise in Google activity around terms like “Ledger Wallet,” “Trezor Wallet,” and “Cold Storage Wallet” suggests that people are aware that the full potential of cryptocurrency is better achieved by decentralization.

Self-custody, however, is not just important for protecting oneself against questionable custodians. As Representative Warren Davidson (R‑OH) pointed out when Canada froze the bank accounts of protestors, much of the protections from the state that decentralized cryptocurrencies like Bitcoin offer also depends on self-custody. For example, where current financial surveillance and control largely depends on the third-party doctrine, government officials would be required to secure a warrant to collect private information on someone holding cryptocurrencies in a self-hosted wallet because then exchanges only involve two parties.

The history of the third-party doctrine and the Bank Secrecy Act has been a consistent erosion of Americans’ financial freedoms, yet government agencies do not appear satisfied with their existing level of authority. In late 2020, the Financial Crimes Enforcement Network (FinCEN) attempted to expand its authority to cover self-hosted wallets. And similarly, the Department of Justice (DOJ) recently took a jab at self-hosted wallets in a report explaining cryptocurrency to the Biden administration. Such attempts to expand their reach have been unsuccessful thus far, but it was with these events in mind that Representative Davidson introduced the Keep Your Coins Act—a bill specifically designed to protect Americans from government agencies seeking to restrict the use of self-hosted wallets.

As the dust on FTX settles, Congress should remember that problems with third-party bad actors (custodians and governments, alike) are very different from problems with decentralized cryptocurrencies or self-hosted wallets. Based on current online trends, it seems that people around the world are clearly taking note of this difference.