According to former Reagan adviser Martin Feldstein, “Higher projected budget deficits could raise long-term interest rates, potentially triggering… a serious economic downturn.”

Has that ever happened?

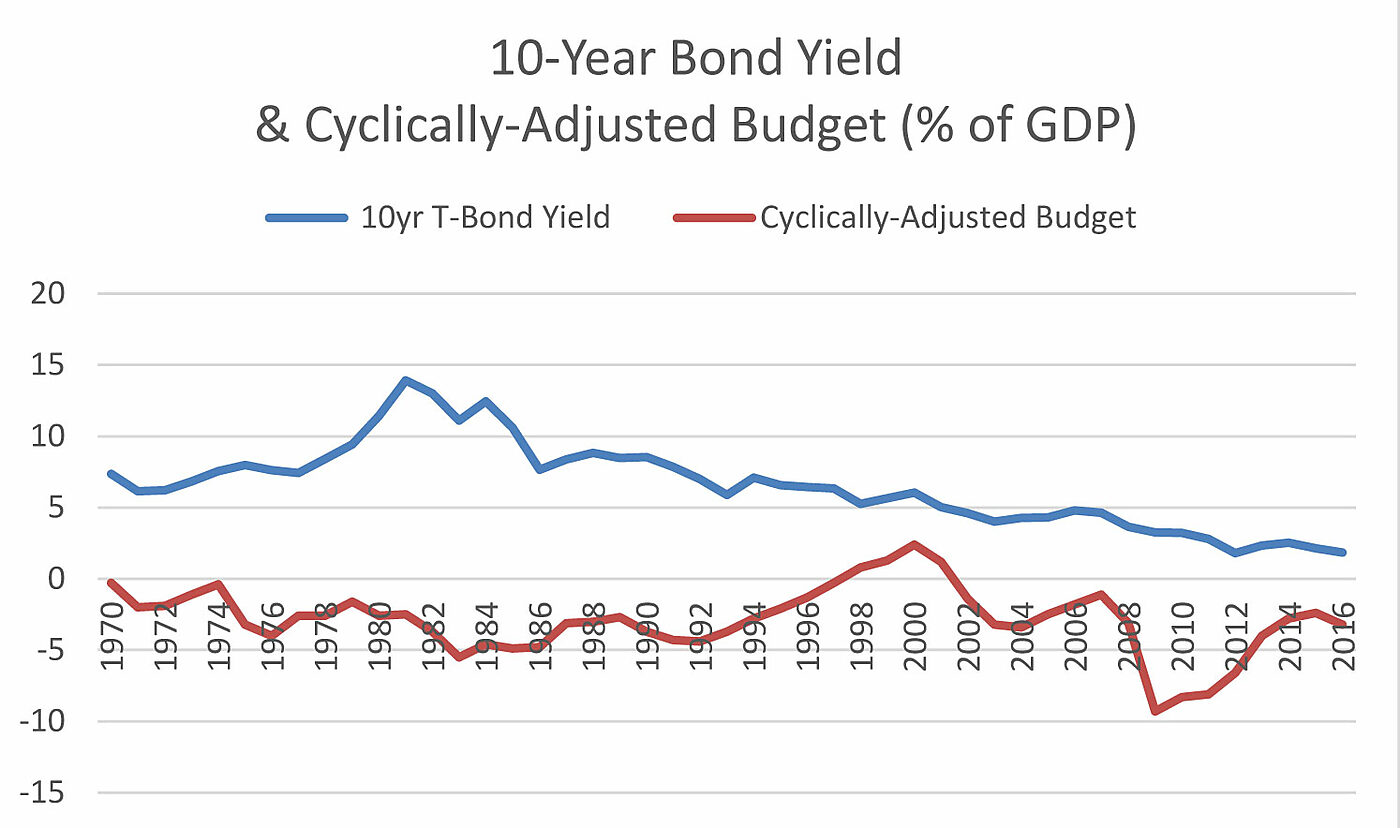

From 1977 to 1981 10-year bond yields nearly doubled, rising from about 7.4% to 13.9%, but budget deficits were relatively small, around 2.5% of GDP. Budget deficits were doubled from 1984 to 1993 (about 5% of GDP), yet bond yields were nearly cut in half, falling from 12.4% to 5.9%. Bond yields were no lower from 1997 to 2000 when the budget moved into surplus. But yields fell dramatically in 2008–2012, a period of record budget deficits.

One possible objection is that larger budget deficits were caused by recessions, which is why bond yields did not rise with larger deficits or fall with surpluses. The graph addresses this concern by using CBO estimates [.xls] of cyclically-adjusted budgets (“with automatic stabilizers,” in CBO vocabulary).

Still, there is clearly no correlation between bond yields and any measure of yearly budget deficits and surpluses. And that is also true in other times and places – Japan’s chronic large deficits and debt being an obvious example.

Another possible objection centers on Feldstein’s use of the phrase “projected budget deficits,” as though the CBO’s notoriously inaccurate long-run projections could somehow have an entirely different effect from actual deficits. I criticized the analysis and evidence behind that conjecture in a Treasury Department presentation which was condensed and simplified in a Cato Institute paper. I found the underlying analysis illogical and contradictory and the evidence worthless.

There is no need to make up stories about alleged effects of deficits on bond yields in order to make a strong case for minimizing frivolous government borrowing (e.g., to pay for transfer payments or government employee compensation).

Chronic deficits add to accumulated debt, and that debt will have to be serviced with future taxes even if it is rolled-over indefinitely. That is reason enough for Congress to keep growth of federal spending below the growth of the private economy – a task which requires frugality in spending but also a tax and regulatory climate which minimizes impediments to investment, entrepreneurship, education and work.