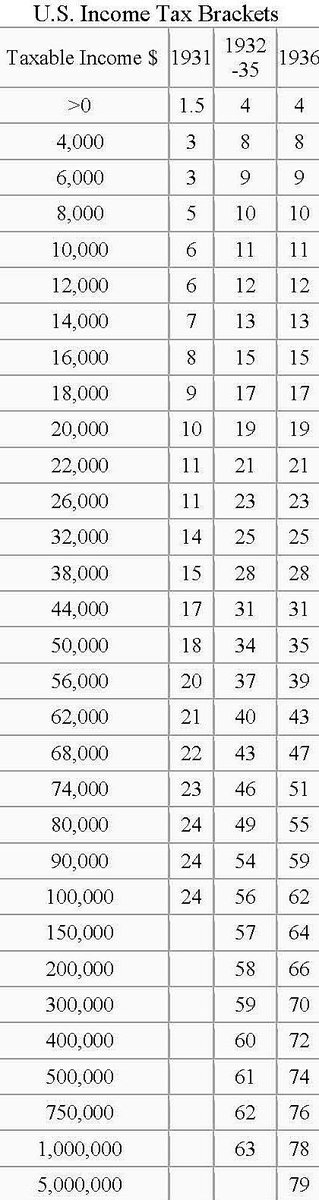

My recent Wall Street Journal op-ed, “Hillary Parties Like It’s 1938,” is not just about FDR’s self-defeating “tax increases” in 1936–37. It is also about the particularly huge across-the-board increase in marginal tax rates the Herbert Hoover pushed for and enacted retroactively in 1932. The primary motive in 1932, as in 1936, was to raise more revenue. Federal spending under President Hoover doubled from 3.4% of GDP in 1930 to 6.8% in 1932, and he believed that unprecedented spending spree required that tax rates be even more than doubled to “restore confidence.”

Unfortunately, things did not quite work out as planned. Total federal revenues fell dramatically to less than $2 billion in 1932 and 1933 — after all tax rates had been at least doubled and the top rate raised from 25% to 63%. That was a sharp decline from revenues of $3.1 billion in 1931 and more than $4 billion in 1930, when the top tax was just 25%.

Some may object that this is unfair, arguing that revenues should be expressed as a share of GDP because GDP fell so sharply in 1932 and 1933. But that begs a key question. Comparing the drop in revenues to the even deeper drop in GDP would make sense only if the depth and duration of the 1932–33 drop in GDP had absolutely nothing to do with higher tax rates (including Smoot-Hawley tariffs). Yet neither Keynesian nor supply-side economics would consider huge tax hikes are so harmless (though Keynesians, seeing no revenue gain, might come to the paradoxical conclusion the Hoover actually cut taxes).

In any case, dividing weak revenues by even weaker GDP doesn’t help support the conventional wisdom that higher tax rates always bring higher revenues. Revenues fell even as a share of falling GDP – from 4.1% in 1930 and 3.7% in 1931 to 2.8% in 1932 (the first year of the Hoover tax increase) and 3.4% in 1933. That illusory 1932–33 “increase” was entirely due to less GDP, not more revenue.

The 15 highest tax rates were increased again in 1936, dividends were made fully taxable at those higher rates, and both corporate and capital gains tax rates were also increased as explained in my Journal piece. Yet all of those massive “tax increases” imposed by Presidents Hoover and Roosevelt failed to bring as much revenue in 1936 as was collected with much lower tax rates in 1930.

If the goal is to shrink GDP, the 1932–37 experience suggests that steeply progressive tax rates certainly accomplish that, particularly when they’re aimed at business and investors.

If the goal is to raise more revenue, on the other hand, the fact is that a top tax of 28% brought in more revenue than we ever did with top tax rates of 70% or 91%.

{kind=link}

{kind=link}