American news stories about the Greek financial collapse frequently echo complaints of government employees and their supplicants about “budget cuts.” In reality, Greek government spending rose from 44.6 percent of GDP in early 2006 to 54 percent in 2010 and 59.2 percent in 2014 (although this is partly because private GDP fell even faster than government spending). Military spending is particularly lavish in Greece, second only to the United States within NATO as a percentage of GDP.

What is rarely mentioned in all the one-sided confusion about “austerity” is the other side of the budget–namely, taxes.

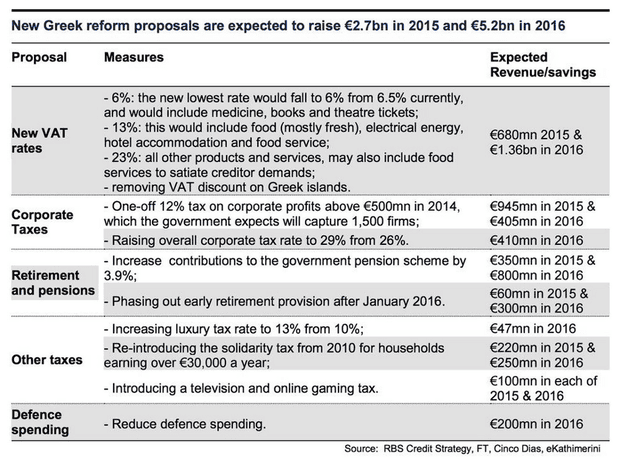

As if Greece didn’t have enough troubles, the Troika (International Monetary Fund, European Commission and European Central Bank) has promoted capital flight and a brain drain (exodus of skill and talent) by offering more and more loans to Greece in exchange for an increasingly suicidal blend of brutal taxes on both labor and capital. The table shows what happened to key Greek tax rates in the past few years.

| Current | Previous | |

| Corporate Tax Rate | 26.00 | 20.00 |

| Personal Income Tax Rate | 46.00 | 40.00 |

| Sales Tax Rate (VAT) | 23.00 | 18.00 |

| Social Security Rate | 42.01 | 29.05 |

Looked at separately, each of these higher tax rates might appear reasonable to fans of big government. Looked at together, they are totally unreasonable. To offer a Greek employee an extra 100 euros requires that 42 euros be subtracted for Social Security tax and then up to 46 more subtracted for income tax. Out of the original 100 euros of marginal labor cost, the remaining 14 euros of after-tax income going to the skilled worker can only buy about 10 euros worth of goods after the value-added tax is paid.

Little wonder that Greece has been suffering a massive brain drain –with hundreds of thousands of the best and brightest emigrating in recent years, including many doctors. At least a fourth of the remaining Greek economy survived by going underground, but that “shadow economy” ran on cash and banks are now sternly rationing cash withdrawals.

People, firms, or countries faced with an unbearable ratio of debt to income do not need more debt or less income (after taxes). Yet this is precisely what has been repeatedly prescribed for Greece –with the IMF and others demanding ever-increasing taxes to shrink private incomes so that the dwindling number of remaining Greek taxpayers can be saddled with ever-increasing debts. Amazingly, the latest “deals” with the Troika propose even higher tax rates, particularly on corporate profits and salaries above 30,000 euros.

In 1377, Ibn Khaldun published his introduction to history, The Muquaddimah, in Cairo. In that famed opus, Khaldun explained, about as well as anyone has, what happens to a country when the tax collectors get too greedy:

“Eventually, the taxes will weigh heavily upon the subjects and overburden them…The result is that the interests of the subjects in enterprises disappears, since when they compare expenditures and taxes with their income and gain and see the little profit they make, they lose all hope. Therefore, many of them refrain from all [economic] activity. The result is that the total tax revenue goes down.…Attacks on people’s property remove the incentive to acquire and gain property.…It is the state that suffers from all these acts, inasmuch as civilization…is ruined when people have lost all incentive”.

{kind=link}