Household debt is currently at record highs. The usual suspects—credit card balances and mortgages—have been covered heavily in the media, but some people have been wondering how the philosophy of “buy now, pay later” might fit into the story.

Last fall, Senator Mark Warner (D‑VA) likened the rise of buy now, pay later (and other fintech) services to the lead-up to the financial crisis. However, when considered alongside the data that is available, it appears clear that there is no such risk.

The Current Consumer Debt Landscape

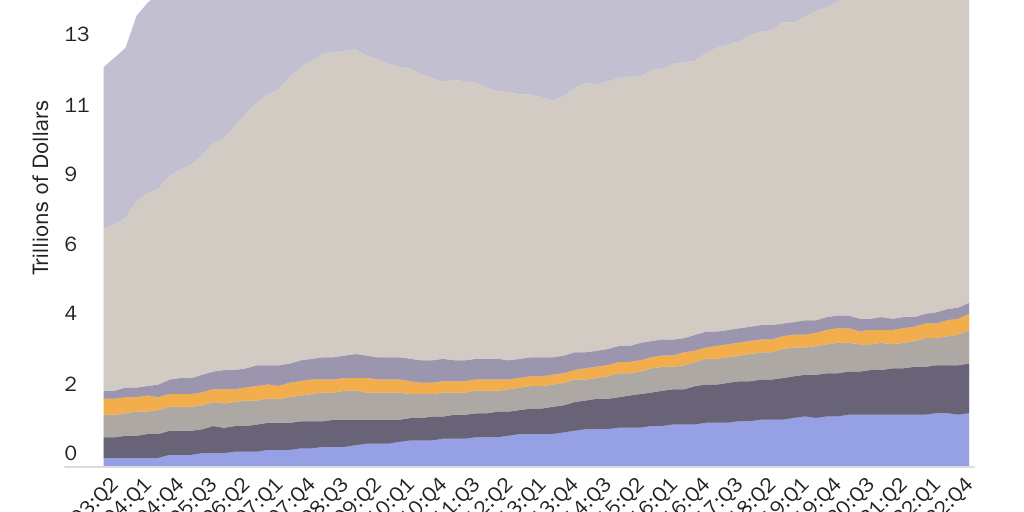

First, let’s consider the current landscape. The Federal Reserve reported that housing debt and non-housing debt in the fourth quarter of 2022 reached $12.26 trillion and $4.64 trillion, respectively. When broken down further (see Figure 1), it becomes clear this debt is primarily concentrated within mortgages (71 percent of all consumer debt), student loans (9 percent), and auto loans (9 percent).

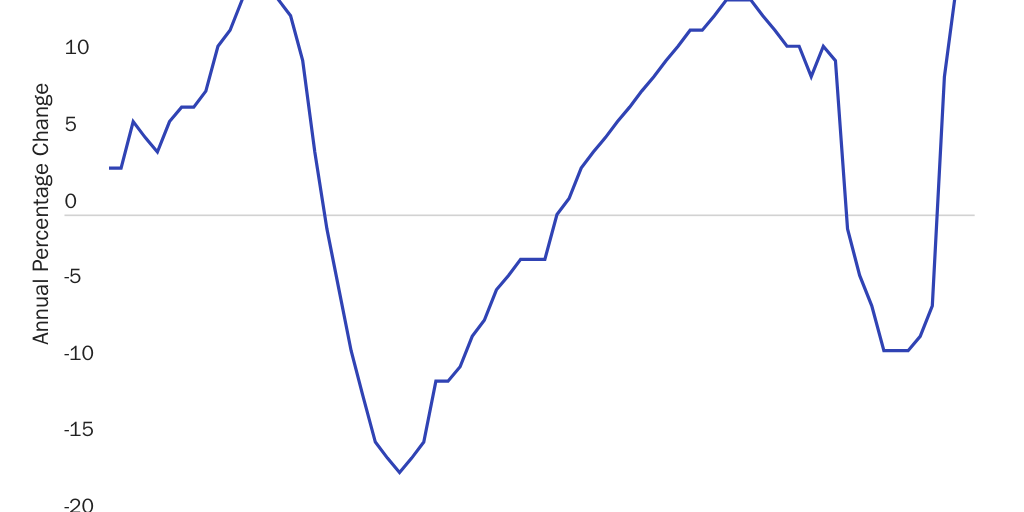

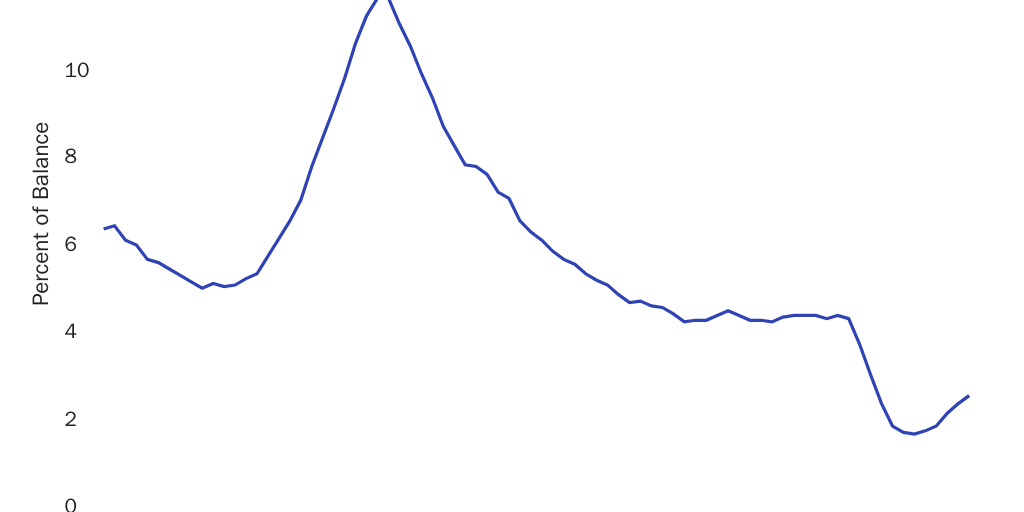

While credit card debt made up just 6% of the total share of consumer debt, it is notable that credit card debt alone increased 20% since this time last year (Figure 2). However, even though delinquencies are starting to pick up, they still pale in comparison to historic levels (Figure 3).

Buy Now, Pay Later Data

So where does the buy now, pay later industry fit into this story? Well, one complaint about the industry has been due to the lack of standard disclosures and supervision. And to be fair, it’s partly for that reason the industry is not included in the Federal Reserve’s data. However, being a line item in the Federal Reserve’s database should not be a condition of doing business. Moreso, despite not being in the Federal Reserve’s database, there is data available that allows us to piece together the size of this industry.

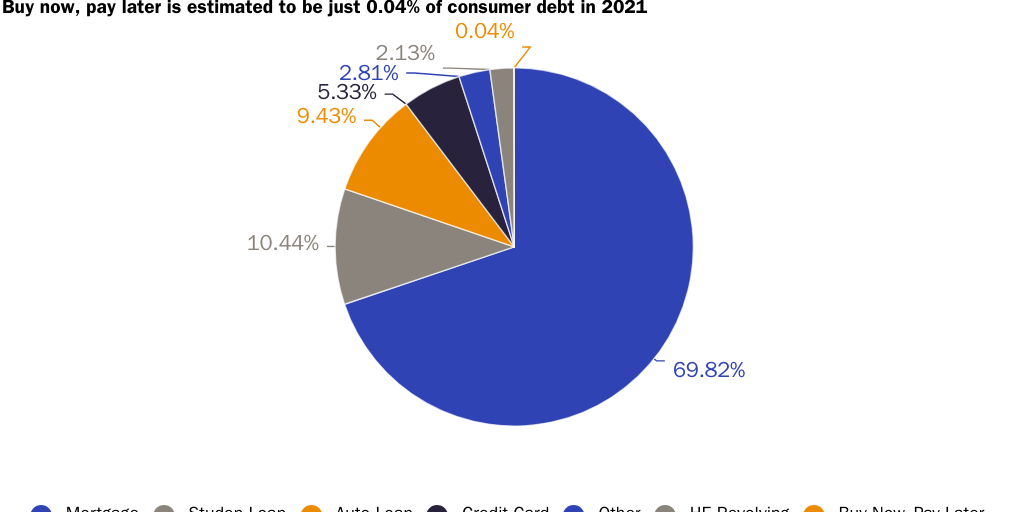

The Consumer Financial Protection Bureau (CFPB) reported the five largest buy now, pay later companies had facilitated $24.2 billion in spending in 2021. While it’s possible some of this spending was linked to credit cards, let’s assume for simplicity that this represents an isolated layer of debt. Under that assumption, if we compare these numbers with the Federal Reserve’s reports, it becomes abundantly clear how small the industry still is: buy now, pay later would have accounted for just 0.04% of consumer debt in 2021 (Figure 4).

For additional context, the Federal Reserve reports there are 500 million open credit accounts, and 191 million Americans have at least one credit card. In fact, that same Federal Reserve report found that 43 million Americans have five or more cards. In contrast, it’s estimated that only 93 million Americans used buy now, pay later in 2022.

There may be room to make arguments that the novel industry is too concentrated or there are problems with individual consumers taking on unsustainable debt. Still, policymakers should be mindful that to the extent these problems exist, it’s hard to imagine a wide-scale effect akin to the 2008 crisis taking place because of the buy now, pay later industry leading to unsustainable debt.

Conclusion

The buy now, pay later industry is new and will likely continue to evolve. Companies working in this space can certainly help their industry to be better understood during this evolution by being transparent and providing accessible data. However, that is not to say the government should step in to force this transparency. Considering the data available already shows there is little to be concerned about in terms of rising debt, using legislative or regulatory force to mandate disclosures from buy now, pay later companies does not seem justified.