Chairman Barr, Ranking Member Moore, and distinguished members of the Committee on Financial Services Monetary Policy and Trade Subcommittee, my name is George Selgin, and I am the Director of the Cato Institute’s Center for Monetary and Financial Alternatives. I am also an adjunct professor of economics at George MasonUniversity, and Professor Emeritus of Economics at the University of Georgia. I am grateful to all of you for having granted me this opportunity to testify before you on the subject of “Monetary Policy v. Fiscal Policy: Risks to Price Stability and the Economy.”

Rather than attempt to address each of the many facets of this broad subject, I wil devote my remarks to one that seems to me especially important. I refer to the risks to price stability, to the efficient employment of the public’s scarce savings, and ultimately to economic growth, posed by the Fed’s decision, made during the 2008 financial crisis, to switch from its traditional operating system to a radically new one, involving the payment of interest on banks’ excess reserves at above-market rates.

Although it has attracted less attention, and generated less controversy, than some of the Fed’s other crisis-related innovations, the Fed’s decision to pay interest on excess reserves (henceforth IOER, to use the Fed’s own preferred acronym) has had more profound and enduring consequences than those of most of its other crisis-inspired undertaking. And despite Fed officials’ intentions, those consequences have been almost entirely harmful. While those officials claimed, and presumably believed, that IOERwould assist them in maintaining the flow of private credit in the face of extremely low and falling interest rates, the new policy’s actual effects have been very much at odds with those intentions.

Among other things, the Fed’s resort to IOER, and its particular settings of the IOER rate,

- intensified an already severe economic downturn by serving as the means by which the Fed maintained an excessively tight monetary policy;

- led to a sustained collapse in the interbank market for federal funds, thereby destroying the Fed’s traditional means of monetary control;

- dramatically reduced the effectiveness of open-market operations, so that even massive Fed asset purchases might not supply the stimulus to investment and spending that much smaller purchases would once have achieved; and

- undermined productivity by substantially increasing the Fed’s role in allocatingscarce credit.

Today, the Fed’s practice of encouraging banks to hold excess reserves, besides continuing to have many of the harmful consequences it has had in the past, also threatens to prevent Fed officials from honoring their promise to shrink the Fed’s balance sheet and to otherwise “normalize” monetary policy.

The rest of my testimony will explain in detail how the Fed’s IOER experiment—which should henceforth be understood to mean, not just paying interest on excess reserves, but doing so at above-market rates—came about, what its intended and actual consequences have been, and why Congress should bring it to an end as rapidly as can bedone without causing further economic damage.

II. Origins of IOER

Economists have long understood that, to the extent that they bear no interest, bank reserves, including both banks’ holdings of vault cash and their Federal Reserve deposit balances, serve as a tax on bank deposits, and therefore on bank depositors. Although the Fed earns interest on the assets backing such reserves, until October 2008 it didn’t share that interest with commercial banks. Instead, thanks to its monopoly privileges and close relation to the government, it remitted all its interest earnings, net of its operating expenses, to the U.S. Treasury.

Though it was only in the midst of the recent financial crisis that the Fed first began paying interest on bank reserves, the possibility of its doing so has long been a subject of discussion and debate. Indeed, the idea was initially broached during the discussions that led to the passage of the original Federal Reserve Act in 1913. That original suggestion was ultimately rejected, in large part because of opposition from Wall Street banks, which saw it as a threat to their lucrative correspondent business.1

So matters stood for more than half a century, thanks to the generally low inflation and interest-rate environment that prevailed during most of that time, and, after 1933, to the fact that Regulation Q and other provisions of the 1933 Banking Act relieved commercial banks themselves of pressure to pay competitive rates of interest on their own deposit balances.

Starting in the mid 1960s, however, a combination of rising inflation rates, declining Fed membership, the rise of Money Market Mutual Funds, and increasingly intense global banking competition, revived Fed officials’ desire to be able to pay interest on bank reserves, as an alternative to dispensing with mandatory reserve requirements, which they regarded as an aid to monetary control (see Weiner 1985; Higgins 1977; and Eubanks 2002). Over the course of the next several decades Fed officials tried several times to gain Congress’s permission to pay interest on reserves.2 Until 2006 these attempts were successfully opposed by the U.S. Treasury, which feared having its seigniorage earnings substantially reduced. But in that year the Fed finally managed to have the authority it had long sought included among the provisions of the Financial Services Regulatory Relief Act.

The Fed’s ultimate success was made possible in large part by reduced Treasury opposition, itself due to a considerable decline, during the 1990s, in the burden posed by mandatory reserve requirements, and the corresponding decline in the Treasury’s seigniorage revenues. Although actual requirements were reduced somewhat, their reduced burden was mainly due to banks’ successful employment of “sweep accounts” to avoid them. By substantially reducing the effective reserve tax base, these developments also reduced the cost to the Treasury of allowing the Fed to pay interest on reserves.

By the same token, however, the reduced burden of reserve requirements also limited the “regulatory relief” banks would gain from interest payments on reserves. Perhaps in recognition of this, Fed officials, in making their successful bid for the right to pay interest on bank reserves, offered new grounds for doing so that had nothing to do with reducing the reserve tax. In particular, then Fed Governor Donald Kohn (2005) argued that, besides making it unnecessary for banks to resort to sweep accounts and other “reserve avoidance measures,” interest on reserves, and on excess reserves especially, would assist the Fed in conducting monetary policy “by establishing a sufficient and predictable demand for balances at the Reserve Banks so that the System knows the volume of reserves to supply (or remove) through open market operations to achieve the FOMC’s target federal funds rate.”

Importantly, in view of later developments, Kohn’s statement implied that IOER was meant to support, rather than supplant, the Fed’s traditional methods of monetary control, including its reliance upon open-market operations as its chief tool for reaching its monetary targets.

Finally, Kohn said that the IOER rate

would act as a minimum for overnight interest rates, because banks would notgenerally lend to other banks at a lower rate than they could earn by keeping their excess funds at a Reserve Bank. Although the Board sees no need to pay interest on excess reserves in the near future, and any movement in this direction would needfurther study, the ability to do so would be a potentially useful addition to themonetary toolkit of the Federal Reserve (ibid.; emphasis added).

These remarks suggest that the Fed was contemplating a “corridor system” of the sort that many central banks were then employing. In such a system, the IOER rate serves as a lower bound for the central bank’s policy rate, while the central bank’s emergency lending rate serves as an upper bound. Although the policy rate can vary within these limits, it generally stays close to a target set, in most instances, half-way between them. Most importantly, it is kept there by means of the central bank’s additions to or subtractions from the quantity of bank reserves. Except on those infrequent occasions when one of the limits becomes binding, changes to the supply of reserves continue to be the chief means by which the central bank conducts monetary policy (Kahn 2010, pp. 13– 15).

Had the Fed actually employed IOER to establish a corridor system, its doing so wouldn’t have constituted a radical change. But as we shall see, when the Fed actually put its new tool to work, a corridor system was no longer what it had in mind.

III. IOER and the 2008 Emergency Economic Stabilization Act

III. a. Fear of Falling

The 2006 Act would have allowed the Fed to begin paying interest on depository institutions’ reserve balances commencing October 1, 2011. However, the worsening financial crisis of 2008 led to the passage of the Emergency Economic Stabilization Act, which advanced the effective date of the 2006 measure to October 1, 2008.

Fed officials sought and received Congress’s authorization to begin paying interest on reserves three years ahead of the originally planned date for a reason completely unrelated to those that Kohn and others had offered in defense of the original measure. As Ben Bernanke explains in his memoir,

We had initially asked to pay interest on reserves for technical reasons. But in 2008, we needed the authority to solve an increasingly serious problem: the risk that our emergency lending, which had the side effect of increasing bank reserves, would lead short-term interest rates to fall below our federal funds target and thereby cause us to lose control of monetary policy. When banks have lots of reserves, they have less need to borrow from each other, which pushes down the interest rate on that borrowing—the federal funds rate.

Until this point we had been selling Treasury securities we owned to offset theeffect of our [emergency] lending on reserves (the process called sterilization). Butas our lending increased, that stopgap response would at some point no longer be possible because we would run out of Treasuries to sell. At that point, without legislative action, we would be forced to either limit the size of our interventions…or lose the ability to control the federal funds rate, the main instrument of monetary policy. [By] setting the interest rate we paid on reserves high enough, we could prevent the federal funds rate from falling too low, no matter how much [emergency] lending we did (Bernanke 2015, pp. 325–6; emphasis added).

The same understanding of the Fed’s intention in implementing IOER three years ahead of the original, 2006 schedule was conveyed in the Board of Governors’ October 6, 2008 press release announcing the Fed’s new tool:

The payment of interest on excess reserves will permit the Federal Reserve to expand its balance sheet as necessary to provide the liquidity necessary to support financial stability while implementing the monetary policy that is appropriate in light of the System’s macroeconomic objectives of maximum employment and price stability.3

The chart below may further clarify the Fed’s reasoning. The solid line in it shows the Fed’s total assets, while the dashed line shows its Treasury holdings, before and since Lehman’s failure. That failure was followed by a dramatic increase in the Fed’s emergency lending. But because the Fed’s Treasury holdings had already fallen by then to what Fed officials considered a minimal level, they had to find other ways to prevent growth in its balance sheet from undermining its ability to keep new reserves from flooding into the fed funds market. While the Treasury, at the Fed’s behest, did its part by diverting funds to a “Supplementary Finance Account” created for the purpose of reducing banks’ share of total Fed balances (dotted line), for the most part the Fed was counting on IOER to encourage banks to accumulate excess reserves instead of lending them.

III. b. From Corridor to Floor

Whether Fed officials realized it at the time or not, their new IOER plan was fundamentally at odds with having the IOER rate serve as the lower-bound of a “corridor” system. In a genuine corridor system, as we’ve seen, the IOER rate is supposed to be set below the monetary authority’s intended policy rate target, and changes in the stock of bank reserves are supposed to keep the rate near that target. In contrast, if IOER is to have the effect of preventing additions to the supply of reserves from influencing the fed funds rate, the IOER rate must be set at, if not above, the prevailing fed funds rate.

The Fed’s strategy called, in other words, not for a “corridor” system, but for what Marvin Goodfriend (2002) and others have termed a “floor” system. In a floor system the IOER rate itself becomes the central bank’s policy rate, and hence its chief instrument of monetary control, replacing management of the stock of bank reserves in that role. The difference between the two arrangements is illustrated in the figure below. In a corridor system, as we’ve seen, the target fed funds rate is set between, and typically half-way between, the IOER rate and the discount (or primary credit) rate, and open-market operations are employed to keep the effective funds rate close to its target value. In a floor system, in contrast, the Fed sets an above-market IOER rate equal to its desired fed funds rate target, thereby allowing the IOER rate to serve, in Goodfriend’s words, as both a “floor under which banks would not lend reserves to each other” and “a ceiling above which banks would not lend to each other.” The Fed is therefore able to maintain a desired fed funds rate despite flooding the market with bank reserves.

(Reproduced from Keister 2012)

III. c. A Dubious Advantage

Would a floor system save the day by allowing a rapidly-expanding Fed to maintain an above-zero fed funds rate? As I’ve observed elsewhere,4 the logic underpinning the Fed's plan was more than a little tortured. If there is reason to fear the zero lower bound, it’s because, once the fed funds rate reaches zero banks, instead of seeking to exchange excess reserves for other assets, will become indifferent between those alternatives. As Marvin Goodfriend (2002) explains,

banks will never lend reserves to each other at negative (nominal) interest if reserve deposits are costless to store (carry) at the central bank. The zero bound on the nominal interbank rate is a consequence of the fact that a central bank stores bank reserves for free (p. 2).

At the zero lower bound, ordinary Fed rate cuts are no longer possible. Those inclined to identify monetary easing with rate cuts see this as “the” problem. But that’s taking a superficial view of matters. The real problem is that, at the zero lower bound, the (zero) yield on bank reserves ceases to be lower than the yield on other short-term assets. Consequently, further additions to the total reserve supply—the Fed’s ordinary means of stimulating the economy—no longer inspire further bank lending and deposit creation.

Instead, the economy becomes mired in a “liquidity trap,” with banks sitting on any fresh reserves that come their way. As Congressman Alan Goldsborough famously put it in 1935, in attempting to induce more lending the Fed would find itself “pushing on a string.”

How, in that case, could a positive IOER rate help? To be sure, it can solve the “zero lower bound problem” superficially, by establishing a positive fed funds rate floor. But to what end? IOER would then render additions to the stock of bank reserves ineffective as a source of stimulus before the fed funds rate reached zero rather than once it did so. Yes, with the help of (positive) IOER, the Fed might set and achieve whatever positive rate target it liked; and it might do so regardless of how many reserves it created. But this “decoupling”5 of interest rates changes from changes in the scarcity of bank reserves, applauded by Goodfriend (ibid.), Keister (2012), and Keister, Martin, and McAndrews (2008) as a feature of a floor system, is really a bug: the extra freedom it entails comes at a very great price, to wit: the Fed’s inability to use its reserve-creating powers to promote additional bank lending and spending.6

When driving an automobile, one can get away with only so many combinations of steering-wheel movements on the one hand and the gas pedal pressure on the other. Wouldn’t it be nice to be able to have complete freedom to step on the gas, and yet steer whichever way we like? Well, there’s a solution: put the transmission in neutral! The hitch of course is that, while one can now steer any way one likes, and stomp on the gas all one likes, one cannot get very far doing either.

An above-market IOER rate can likewise allow the Fed to steer the fed funds rate any way it likes, while stepping on the reserve-creation peddle as hard as it likes, only by putting the usual monetary transmission mechanism in neutral. For the usual zero-lower- bound liquidity trap, it substitutes an above-zero liquidity trap in which monetary policy remains, despite appearances to the contrary, more-or-less equally impotent. The zero lower bound problem is thus avoided, but in a way that may still leave the economy in a depressed state, with little scope for monetary policy stimulus of the old-fashioned sort. It is as if (to offer one last simile), out of concern for would-be jumpers, the designers of a skyscraper decided to construct a broad concrete veranda around their building's second floor, to prevent them from ever hitting the ground!

Just how the Fed proposed to stimulate the economy with its ordinary monetary policy transmission mechanism stuck in neutral, as it were, was a challenging question Fed authorities would eventually have to answer. For the time being, however, stimulating the economy wasn’t their concern. Instead, their concern was to avoid stimulating the economy unintentionally. For that purpose, IOER, administered according to the requirements of a floor system, would serve the Fed’s needs well. Indeed, in retrospect, it was to serve them all too well.

III. d. From Floor to Ceiling

Although the Fed’s plans called for a floor rather than a corridor operating system, with the IOER rate set high enough to encourage banks to accumulate excess reserves, the Board of Governors appears to have failed at first to grasp this necessity. Instead, in the same press release announcing its desire to employ IOER to bolster the fed funds rate, it declared its intention to set the IOER rate at a level equal to “the lowest targeted federal funds rate for each reserve maintenance period less 75 basis points.”

Just how an IOER rate set 75 basis points below “the lowest targeted federal funds rate” could possibly assist the Fed in achieving its immediate monetary policy goal, and specifically how it could keep the effective fed funds rate from eventually slipping as much as 75 basis points below the Fed’s target, the press release didn’t explain. Nor could it have, since IOER could only keep the fed funds rate from falling below the Fed’s target if the IOER rate was set equal to, or rather (for reasons we’ll come to) above, that target. Partly for this very reason, the effective fed funds rate continued to decline, as can be seen in the next chart.

The Fed’s announcement provided, however, that “the formula for the interest rate on excess balances may be adjusted subsequently in light of experience and evolving market conditions.” The Fed was, unsurprisingly, quick to take advantage of this clause, which it did by reducing the gap between the IOER rate and its fed funds target, first to 35 basis points, and finally, on November 6, 2008, to zero. However, the gap between the Fed’s rate target and the effective fed funds rate had itself continued to grow in the meantime. The end result of the Fed’s maneuvers, therefore, was an IOER rate well above what banks might actually gain by lending federal funds.

That IOER failed to keep the fed funds rate on target even once the IOER rate was set equal to that target was both inconsistent with the way a floor system was supposed to operate, and a source of considerable disappointment to Fed officials and economists. Blame for it has been placed on the fact that, in addition to banks, various GSEs, including Fannie Mae, Freddy Mac, and the Federal Home Loan Banks, keep deposit balances at the Fed, but aren’t eligible for interest on those balances.7 The GSEs access to the fed funds market therefore creates an arbitrage opportunity Fed officials didn’t anticipate, with GSEs lending fed funds overnight to banks in exchange for a share of the latter’s IOER earnings. When the IOER rate was set at 25 basis points, for example, one of the Federal Home Loan Banks might lend funds overnight to a commercial bank for less than 25 basis points, allowing the commercial bank to profit from the spread, while securing for itself a return greater than the zero rate it would earn if it just held on to its Fed balance.

Consequently, instead of getting the solid floor system it wanted, the Fed had to settle instead for a “leaky” system. Indeed, because the effective fed funds rate tended to fall below the IOER rate, the latter ended up looking less like a floor than like a ceiling— just the opposite of corridor arrangement. When, in mid-December 2015, the Fed began making use of a new overnight reverse repurchase agreement (ON-RRP) facility to establish what Stephen Williamson (2016) has called a “floor-with-sub-floor” system, with the effective fed funds rate trading within a target “range” defined by the IOER rate (floor), and the ON-RRP (subfloor), the resemblance of the Fed’s new system to a corridor system gone topsy-turvy became all the more complete.

Setting the IOER Rate

IV. a. Original Intent: A Below-Market IOER Rate

Having shifted, between 2006 and 2008, from an IOER scheme aimed at ending the implicit taxation of bank reserves and perhaps at establishing a corridor system of monetary control, to one aimed at establishing a floor system, however leaky, the Fed was bending the law. For the new policy marked a radical change, not just from what the authors of the 2006 legislation had envisioned, but from what that legislation provided for in fact.

The pre-crisis opinion had been that IOER should be used cautiously, with the IOER rate set low enough to avoid making reserves seem “more attractive relative to alternatve short-term assets.” Otherwise, that opinion held, IOER, instead of simplifying monetary policy, would further complicate it (Weiner 1985, p. 30).8

Such was clearly Federal Reserve Governor Laurence H. Meyer’s understanding when, in arguing the case for allowing the Fed pay interest on reserves before the House Banking Committee in 2000, he explained that

If the bill becomes law, the Federal Reserve would likely pay an interest rate on required reserve balances close to the rate on other risk-free money market instruments, such as repurchase agreements. This rate is usually a little less than the interest rate on federal funds transactions, which are uncollateralized overnight loans of reserves in the interbank market (Meyer 2000, p. 10).

What Governor Meyer considered an appropriate proxy for “the general level of short-term interest rates” in 2000 was presumably still appropriate in 2006. Since unsecured overnight rates, such as the federal funds rate and the London Interbank Overnight Rate (LIBOR), entail greater risk than overnight repos, to abide by the intent of the 2006 and 2008 laws, the Fed would have to keep the interest rates paid on reserve balances somewhat below these somewhat more risky overnight interbank lending rates. In this way, as one Fed official explained when the 2006 legislation was being considered, banks would have no reason “to significantly shift their financial resources to take advantage of this [the IOER] rate” (Eubanks 2002, p. 11). In particular, banks would continue to keep only such reserve balances as they needed to meet their legal and clearing-balance requirements. The main difference reformers anticipated was that they would no longer bother using sweep accounts to avoid an implicit reserve tax.

The provisions of the 2006 legislation reflected these same considerations. According to Title II of that measure, the Fed might pay interest on depository institutions’ reserve balances “at a rate or rates not to exceed the general level of short- term interest rates.” The 2008 Financial Services Regulatory Relief Act left this language unaltered.

IV.b. Above the Law?

Fed officials therefore found themselves in a quandary. As we’ve seen, they wanted to be able to resort to IOER three years ahead of schedule precisely for the purpose of making excess reserves “attractive relative to alternative short-term assets.” That meant setting the IOER rate above the going, but still positive, equilibrium fed funds rate. Indeed, given the “leakiness” of the Fed’s floor system, the IOER rate would have to be set considerably above the Fed’s target rate. In practice that also meant keeping the IOER rate above other, comparable market-based short-term interest rates. According to the law, on the other hand, the Fed was only supposed to pay interest on bank reserve balances at a rate “not to exceed the general level of short-term interest rates.”

That the Fed did in fact settle on an IOER rate above comparable market rates can be seen in the next sequence of charts, the first of which compares its IOER rate to both the effective federal funds and the LIBOR rate:

Because the fed funds and LIBOR rates are rates for unsecured overnight loans, they include a small risk component, while the IOER rate is equivalent to a risk-free overnight rate. For that reason, and as Governor Meyers suggested in his previously- mentioned testimony, the rate implicit in overnight, Treasury-secured repurchase agreements might be a more appropriate market-rate benchmark. That rate has also tended to fall below the IOER rate.

Finally, it's instructive to compare the IOER rate to rates on Treasury bills of various maturities. The latter rates should, for obvious reasons, generally be above equivalent, risk-free overnight rates, according to the securities' term to maturity. Yet, as the next chart shows, rates on both 4-week and 3 month T-bills have also been persistently, and often substantially, below the IOER rate. Indeed, from the spring of 2011 through mid-summer of 2015, even rates on 1-year Treasury bills remained below, and generally well below, the IOER rate:

In short, it’s impossible to reconcile the Federal Reserve’s setting of its IOER rate with any reasonable understanding of the law’s stipulation that it is “not to exceed the general level of short-term interest rates.”

IV. c. “One of these rates is not like the others…”

In an apparent attempt to legalize the Fed's IOER rate settings after the fact, Fed officials, in drafting the final rules implementing the 2008 statute, as published in the Federal Register on June 22, 2015, determined that for that purpose

‘‘short-term interest rates’’ are rates on obligations with maturities of no more than one year, such as the primary credit rate and rates on term federal funds, term repurchase agreements, commercial paper, term Eurodollar deposits, and other similar instruments (Regulation D: Reserve Requirements for Depository Institutions 2015, p. 35567).

While most of the listed rates are unobjectionable, even if they fail to include overnight obligations (which are, after all, closer equivalents to reserve balances than term obligations are), the presence of the primary credit rate is a glaring anomaly, for that’s the discount rate that the Fed charges sound banks for short term emergency loans. As such it isn’t a market rate at all but one set administratively by the Fed’s Board of Governors. Moreover, since 2003 the Fed has always set its primary credit rate “above the usual level of short-term market interest rates” (Board of Governors 2017b). Since the Fed began paying interest on reserves it has also deliberately set its primary credit rate above the IOER rate.9 The Fed has thus found a way by which to claim, with an implicit appeal to Chevron deference, that its IOER rate settings have after all been consistent with the requirements of the 2006 law!10

That the Fed should thumb its nose thus at the statute granting it the authority to pay interest on reserves would be regrettable enough if its doing so had only benign consequences. Yet that is far from being the case. On the contrary: by bending the law to conform to its plan to make the accumulation of reserve balances more attractive to banks than other forms of investment, the Fed fundamentally altered the workings of the U.S. monetary system, with grave consequences for the U.S. economy.

V. IOER and Reserve Hoarding

Many observers have assumed that the seemingly modest rate the Fed has paid on banks’ excess reserve balances, which has so far never exceeded 125 basis points, and which was a mere 25 basis points from December 2008 until December 2015, has never been high enough to have had any substantial bearing on banks’ decision making, and particularly on either the total supply or the allocation of credit.

But as we’ve seen, these seemingly low IOER rates have not been low relative to comparable market rates. For that reason, their influence on banks’ behavior has been anything but modest. As Simon Potter (2015), a Federal Reserve Bank of New York Vice President, and head of its Market Group, explains,

The IOER rate is essentially the rate of return earned by a bank on a riskless overnight deposit held at the Fed, thus representing the opportunity cost to a bank of using its funds in an alternative manner, such as making a loan or purchasing a security. In principle, no bank would want to deploy its funds in a way that earned less than what can be earned from its balances maintained at the Fed.

Thanks to IOER, banks have refrained from acquiring assets bearing a net return below what they might earn simply by retaining Fed reserve balances. Some, indeed, have found it worthwhile to actively acquire Fed balances for the sake of arbitraging the spread between the return on such balances and private-market borrowing costs. Because IOER was implemented for the express purpose of getting banks to accumulate excess reserves, these outcomes should not surprise anyone.

V. a. The Accumulation and Distribution of Excess Reserves

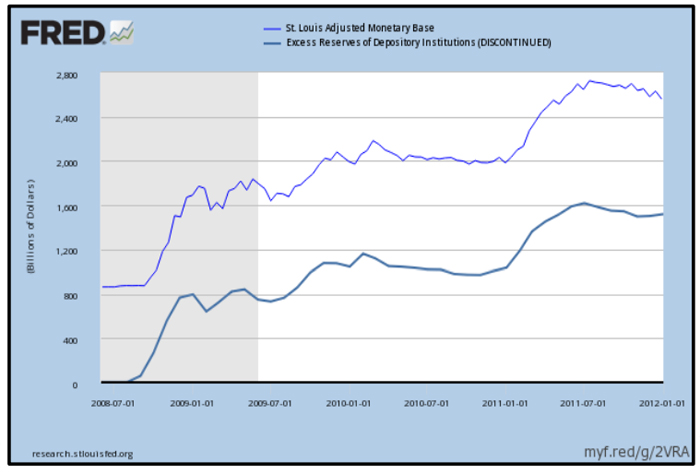

The most obvious consequence of IOER has been unprecedented growth in banks' excess reserves balances, meaning the Fed balances they hold beyond those serving, together with banks' holdings of vault cash, to meet their minimum legal reserve requirements.

In the two decades prior to October 2008, banks generally held between $1 and $2 billion in excess reserves, in part for the sake of avoiding shortfalls from their required reserves, but mainly to avoid relatively costly clearing overdrafts. (The few exceptions consisted of short-lived spikes in excess reserves following crises, like that of September 11, 2001, when banks briefly held over $19 trillion in excess reserves.) Banks' minimum reserve requirements were, in contrast, largely met by their holdings of vault cash. Between them, minimum reserve requirements and banks' demand for excess reserves for settlement purposes determined banks' overall need for reserve balances, together with their desired ratio of such balances to their demand deposits. As the chart below shows, reserve balances normally amounted to between one-fifth and two-fifths of one percent of demand deposits only.

As the next chart shows, after Lehman Brothers' failure, banks' excess reserve holdings began growing in lock-step with growth in the Fed's balance sheet, starting with growth fueled by the Fed's post-Lehman emergency lending, and continuing, after December 2008, with its several rounds of large-scale asset purchases (LSAPs). By August 2014 excess reserves, which had rarely surpassed $2 billion before the crisis, had risen to almost $2.7 trillion.

That banks held on to reserves that came their way was a predictable consequence of the Fed's above-market IOER rate.11 Still, banks didn't all take part equally in the vast reserve buildup. Instead, as the next set of charts shows, a very large share of it went to the very largest U.S. banks or to U.S. branches of foreign banks. As of early 2015, the top 25 U.S. banks, by asset size, held more than half of all outstanding bank reserves, with the top three alone holding 21 percent of the total. Foreign bank branches accounted for most of the rest. The cash assets of small U.S. banks, in contrast, rose only modestly.

That the very largest banks secured such a large share of the total accumulation of excess reserves is partly explained by the fact that those banks include some of the primary dealers that served as the Fed’s immediate counterparties in its asset purchases (Craig, Millington, and Zito 2014). Having thus had “first dibs” on new reserves the Fed created, primary dealer banks simply refrained from letting go of reserves they acquired. That practice was, of course, quite contrary to what primary dealers were normally expected to do, and to what they generally did do before the crisis, when the Fed was still relying on its traditional means of monetary control. Indeed, in the early stages of the subprime crisis, Fed officials worried that the collapse of ailing primary dealers would prevent them from serving as reliable conduits through which fresh reserves would make their way from the Fed to the rest of the banking system (e.g., Kohn 2009). Now, paradoxically, IOER was itself serving to close the same conduits, along with much of the rest of the interbank market, but was doing so deliberately as part of the Fed’s new monetary control strategy.

As for U.S. branches of foreign-owned banks, because many aren’t eligible for deposit insurance, they also aren’t subject to FDIC premium assessments based on their total assets, including the reserve balances they hold. For that reason, and also because many of their parent companies enjoy much lower net interest margins than U.S. banks, they’ve found it especially profitable to acquire fed funds for the sake of arbitraging the difference between the Fed’s IOER rate and lower private-market arbitrage rates. In consequence these banks ended up playing a particularly important part in keeping rowth in the total quantity of reserve balances from contributing to corresponding growth in overall bank lending.

V. b. Excess Reserves and the Fed's Balance Sheet

Some insist that, instead of stemming from the Fed's decision to pay interest on excess reserves, the post-Lehman accumulation of excess bank reserves was an inevitable consequences of the Fed's asset purchases. In an influential Liberty Street post, for example, Todd Keister and Gaetona Antinolfi (2012) criticized Alan Blinder (2012) and others for claiming that lowering the IOER rate would encourage banks to lend more and thereby reduce their excess reserve balances:

Because lowering the interest rate paid on reserves wouldn’t change the quantity of assets held by the Fed, it must not change the total size of the monetary base either. Moreover, lowering this interest rate to zero (or even slightly below zero) is unlikely to induce banks, firms, or households to start holding large quantities of currency. It follows, therefore, that lowering the interest rate paid on excess reserves will not have any meaningful effect on the quantity of balances banks hold on deposit at the Fed. … In fact, the total quantity of reserve balances held by banks conveys no information about their lending activities—it simply reflects the Federal Reserve’s decisions on how many assets to acquire (Keister and Antinolfi 2012).

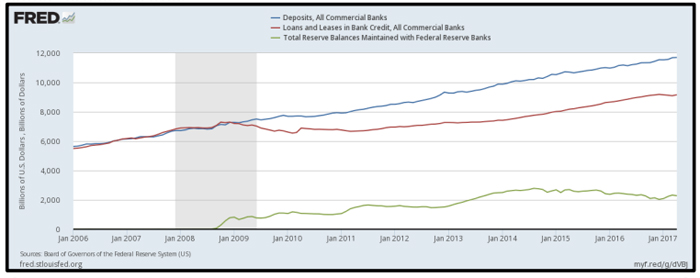

It’s of course true, as any money and banking textbook will affirm, that banks cannot alter the total quantity of reserve balances simply by trading them for other assets, as doing so only transfer the balances to other banks. But the question isn’t whether a lower IOER rate would reduce total reserves. It’s whether a lowered rate can result in a lower quantity of excess reserves. The answer to that question is “yes,” because, as the same textbooks also explain, as banks trade unwanted reserves for other assets, they also contribute to the growth of total banking system deposits; the fact that unwanted reserves get passed on like so many hot potatoes only makes deposits grow that much more rapidly. The growth of total deposits serves in turn to convert former excess reserves into required reserves, where “required” means required either to meet minimum legal requirements or for banks’ clearing needs.

That, at least, is what always happened before the Fed began encouraging banks to cling to excess reserves. For example, as the chart below shows, prior to October 2008, banks routinely disposed of unwanted excess reserves in the manner just described, thereby keeping system excess reserves at trivial levels, and doing so despite additions to the total supply of bank reserves that were, by pre-2008 standards at least, far from trivial.

It follows that, when banks hold a large quantity of excess reserves, that fact actually conveys very significant “information about their lending activities.” Specifically, it tells us that they have refrained from engaging in such activities to some considerable extent.

In reply to these criticisms, Mr. Keister has suggested (in personal correspondence) that, IOER or no IOER, the unprecedented scale of the Fed’s post- Lehman balance sheet growth would have rendered the traditional means by which banks disposed of unwanted excess reserves inoperable, because banks couldn’t possibly achieve the expansion in their total assets and deposit liabilities required to convert so vast an increase in total reserves into an equally vast increase in required reserves. But this counter-argument is also contradicted by relevant historical evidence, consisting of instances of hyperinflation in which central banks expanded their balance sheets on a scale much larger still than that seen in the U.S. since 2008. During the notorious Weimar hyperinflation, for example, the (proportional) growth in German bank reserves far exceeded that witnessed in the U.S. since Lehman’s bankruptcy. Yet, according to Frank D. Graham (1930, p. 68), Germany’s banks, far from accumulating excess reserves, increased their lending more than proportionately. “It would appear,” Graham writes, “that the commercial banks extended loans throughout the period of post-war inflation considerably in excess of a proportionate relationship with the increase in the monetary base. … The increase in deposits issuing from loans was especially marked in 1922 and till stabilization in 1923.”

It doesn’t follow, of course, that, had it not been for interest on excess reserves, the Fed’s post-Lehman asset purchases would have led to hyperinflation. Instead, Fed officials would have not have felt compelled to purchase as many assets as they did; in any event, they would have stopped purchasing assets once confronted with evidence that the inflation rate was in danger of exceeding its target. As it was, by relying on IOER to discourage banks from dispensing with excess reserves, the Fed ended up falling short of, instead of surpassing, its inflation target. That outcome came as a surprise to those accustomed to the workings of the Fed’s traditional monetary control framework. But in the context of its new IOER framework, any tendency for the Fed’s asset purchases to raise prices would itself have been surprising.

V. c. Reserve Demand and Opportunity Cost

Final proof, should it be needed, of the bearing of IOER on banks' willingness to accumulate excess reserves comes from consideration of how that willingness varied with changes in the relationship between the IOER rate and corresponding market rates. If banks' demand for excess reserves is driven by the yield on such reserves compared to that on other assets, then the banking system excess reserve ratio—the ratio of total excess reserves to total bank deposits—should vary with the difference between the IOER rate and comparable short term market rates, such as the overnight LIBOR rate. As the next chart shows, this has indeed clearly been the case.

VI. IOER and Interbank Lending

As we’ve seen, when the Fed began paying interest on bank reserves, its immediate concern was to keep its emergency lending from causing the fed funds rate to drop below 1.5 percent—the target it set when it announced its IOER plan. To repeat Ben Bernanke’s words once again, “by setting the interest rate we paid on reserves high enough, we could prevent the federal funds rate from falling too low, no matter how much [emergency] lending we did (Bernanke, 2015)."12

But interest on reserves could not discourage banks from placing newly-created reserves into the fed funds market without discouraging them from supplying any funds to that market: if a dollar of reserves that landed in a bank’s Fed account as a result of the Fed’s post-Lehman emergency lending earned more sitting in that account than it could earn if lent to another bank overnight, the same was true of a dollar of reserves held beforehand. Consequently, as the next chart shows, IOER served, not only to keep fresh reserves from lowering the fed funds rate, but to dramatically reduce the total volume of lending on the fed funds market: whereas financial institutions lent over $200 billion on the fed funds market during the last quarter of 2007, by the end of 2012 that figure has fallen to just $60 billion (Afonso, Entz, and LeSueur 2013).

As was to be expected, banks and bank holding companies (BHCs) that were eligible for IOER almost completely stopped lending overnight funds. Only the Federal Home Loan banks and other GSEs continued to lend as much as ever, for the sake of securing a share of banks' IOER earnings. The fed funds market thus ceased to function, as it had for decades, as banks' preferred and most reliable source of last-minute liquidity, having instead been transformed into a mere vehicle for bank-to-GSE interest-rate arbitrage.

VI. b. IOER vs. Perceived Counterparty Risk

Although some have attributed the decline in fed funds lending to a post-Lehman increase in perceived counterparty risk, that increase is no more capable of explaining the persistent decline in interbank lending than it is capable of explaining banks' persistent accumulation of excess reserves. While the TED spread—a popular measure of the perceived counterparty risk, equal to the difference between the interest rate on short- term interbank lending and the interest rate on Treasury securities—spiked at the time of Lehman's failure, it began to decline soon afterwards when the Fed decided to come to AIG's rescue, eventually falling to levels even lower than those that that prevailed before the crisis. Interbank lending, on the other hand, never recovered. The Fed's decision to pay interest on excess reserves therefore appears to have been the fundamental cause of the enduring post-Lehman decline in such lending.

The timing of the substantial rise in banks' excess reserves reinforces the last conclusion. Although banks accumulated excess reserves immediately following Lehman's failure, most of the increase occurred after the Fed began paying interest on reserves. Overall, the evidence suggests that, while an increased fear of counterparty risk accounted for banks' increased excess reserve holdings immediately following Lehman's failure, IOER was responsible for the subsequent more substantial and lasting increase in those holdings.13

Finally, the close relationship between the total volume of interbank lending and the opportunity cost of reserves holding, as measured by the difference between the interbank lending rates and the IOER rate, also supports the view that IOER drove the decline in interbank lending. Although the relationship is similar for all banks, it is clearest for foreign banks which, as we've seen, were especially tempted to accumulate excess reserves. Particularly striking is the almost exact coincidence of the precipitous decline in the opportunity cost of reserves coinciding with the introduction of IOER and an equally precipitous, initial decline in interbank loans.

VI. c. From Lender to Borrower of First Resort

The collapse of interbank lending created a further motive, beyond the return on reserves itself, for banks to accumulate excess reserves, as banks that once routinely relied on overnight unsecured loans to meet their liquidity needs discovered that, owing to the substantial decline in the availability of fed funds, doing so was no longer prudent. Because that decline at first caught many banks by surprise, its immediate effect was a sharp spike, on October 7, 2008, in the fed funds rate, which rose to 2.97 percent, or almost twice the Fed’s target at the time. Banks adapted by raising their excess reserve holdings so as to have sufficient precautionary reserves to cover those reserve needs that they had previously met by borrowing federal funds.

As Gara Afonso, Anna Kovner, and Antoinette Schoar (2010, p. 1) point out, until these changes came about, the fed funds market had long served as “the most immediate source of liquidity for regulated banks in the U.S.” Consequently any disruption of that market could “lead to inadequate allocation of capital and lack of risk sharing between banks.” In extreme cases, they add, it might “even trigger bank runs.” By paying IOER at above-market rates, the Fed, which is supposed to serve as a lender of last resort, unwittingly became both a borrower of first resort and the agent of destruction of banks’ traditional, first-resort source of emergency funds.

VII. IOER and Retail Bank Lending

VII. a. Lending Before and Since the Crisis

Between the week just before the Fed began paying interest on bank reserves, when it reached its pre-crisis peak, and the third week of March 2009, when it reached its post-crisis nadir, overall U.S. commercial bank lending declined from over $7.25 trillion to about $6.5 trillion—a decline of $1.25 trillion. Although reduced real estate lending accounted for the greatest part of this decline, other kinds of lending, including business lending, also fell sharply.

Although lending has recovered to a considerable extent since the crisis, at least relative to its pre-subprime boom trend, this recovery was painfully slow. Furthermore it masks an enduring and substantial post-crisis decline in the ratio of overall bank lending (“loans and leases”) to total bank deposits. Whereas total bank lending tended to match total bank deposits in the years leading to the crisis, since then, and specifically since IOER was introduced, it has declined to about 80 percent of deposits. Over that same period, bank reserves, as a percentage of total bank deposits, have increased from trivial levels to roughly 20 percent of bank deposits. In short, as a matter of simple balance- sheet arithmetic, the rise in banks’ holdings of (mainly) excess reserves has gone hand-in- hand with a corresponding decline in bank lending.

VII. b. The Direct Influence of IOER on Bank Lending

But does this correspondence mean that IOER was actually responsible for the decline in retail bank lending as a share of bank deposits? Many insist that IOER rates have been too low, compared to the rates on commercial bank loans, to have had more than a minor influence on bank lending. For example, Ben Bernanke and Donald Kohn (2016) observe that, during the long interval when the IOER rate stood at 25 basis points, “the only potential loans that would have been affected by the Fed’s payment of interest [on reserves] are those with risk-adjusted short-term returns between precisely zero and one-quarter percent.”

That view is, however, mistaken, on both empirical and theoretical grounds.

First of all, as we've seen, the growth in banks' excess reserve holdings was not an inevitable response to growth in the Fed's balance sheet: banks are always materially capable of reducing their excess reserve holdings, collectively as well as individually, either by making loans or by buying securities. It follows that the existence of substantial excess reserve balances is ipso-facto proof that the banks that acquired those reserves considered them more desirable than any other assets they might have acquired.

Standard microeconomic theory suggests, furthermore, that in equilibrium all of a banks' various assets should have, not the same marginal return, but the same marginal net return. Consequently, in theory at least, for any bank that holds excess reserves, the marginal net return on lending must not be any greater than the marginal return on such reserves. That means in turn that, if the return on reserves goes up, total bank lending must decline enough to once again make the marginal net return on loans the same as the return on reserves. To put this another way, although reduced short-term lending, and interbank lending especially, may be the first and most obvious consequence of an increase in bank reserves' relative yield, the eventual consequences will also include some reduction in longer-term bank lending.

Can this theory account for the apparent decline in lending as a share of deposits? It can, provided one understands, first of all, that not all banks enjoy equally high gross returns on lending. That fact is at least roughly reflected in different banks' net interest margins: the difference between the interest they earn and the interest they pay on bank deposits, expressed as a percentage of bank assets. Because bank deposit rates have themselves been extremely low since the crisis, and are in many cases at zero, banks' net interest margins supply a rough indication of their gross interest returns; and those margins have in fact been considerably lower for the largest U.S. banks, and lower still for foreign banks, than they have been for U.S. commercial banks as a whole. Whereas the net interest margin for all U.S. commercial banks has steadily declined from not quite 4 percent in early 2010 to just over 3 percent in 2017, the margin for banks in New York, which is home to the very largest banks, has been around 2 percent for most of that same period, while that for foreign banks generally has generally been less than 1.5 percent.

And it is, as we've seen, the very large domestic banks, as well as foreign bank branches, that have been holding most of the outstanding excess reserves.

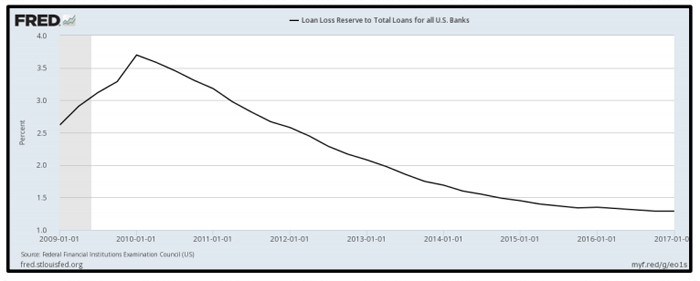

Even 150 basis points is many times 25 basis points. But that's still not the right comparison, because there are substantial non-interest expenses involved in making loans, whereas the only non-interest expense of holding Fed balances consists of FDIC premiums assessed against a bank's total assets—and even that cost does not apply to most foreign bank branches. ECB area bank operating expenses, for example, are equal to about 60 percent of their interest income. And because borrowers sometimes default, and banks must make allowances for such defaults, loan loss provisions further reduce the net return on bank loans (Noizet 2016). As the next chart shows, those provisions reached a peak of 3.7 percent of total bank assets at the beginning of 2010, from which they've gradually fallen to their present level of 1.29 percent. Taking such losses as well as other costs of lending into account, it's no longer at all difficult to understand how a modest IOER rate might have made holding excess reserves seem more lucrative than granting a loan at a considerably higher non-risk-adjusted rate.

Nor is that all. Banks' net interest margins are a measure of the return on their entire loan portfolios. But allowing that the demand schedule for bank loans is downward-sloping, the return on a banks' marginal loan is necessarily lower than that on its loan portfolio as a whole; and it's this marginal return, net of both the interest and the non-interest expense associated with the marginal loan, that is supposed, in equilibrium, to be no higher than the bank's net marginal return on other assets, including any excess reserves it holds. Consequently, the mere existence of a positive difference between a banks' net interest margin and the IOER rate, even after allowing for the noninterest cost of loans, is perfectly consistent with the theory that banks' have found it more profitable to accumulate excess reserves than to part with those reserves by lending more.

The diagram below illustrates the last point. In it, the blue line represents the downward-sloping marginal revenue schedule for loans confronting the banking system, while the horizontal grey line represents the IOER rate, here assumed to be 100 basis points. For simplicity, I ignore banks' noninterest expenses altogether, while assuming that the Fed adjusts the total stock of reserves so as to keep total bank deposits constant.

In that case, assuming that they have $10 trillion in deposits at their disposal, the banks will collectively lend $8 trillion, while maintaining $2 trillion in excess reserves. But although the net return on the marginal loan is the same as the IOER rate, the banking system net interest margin, represented here by the orange line, will necessarily be higher than the IOER rate. Reducing the IOER rate to zero, on the other hand, encourages banks to lend 100 percent of their deposits, instead of holding any excess reserves.14

VII. c. Excess Reserves and Bank Lending in Japan

Some authorities doubt that IOER accounts for U.S. banks’ exceptional demand for excess reserves, and the associated decline in bank lending, because the same phenomena have occurred in other countries, and most notably in Japan, and did so even when banks’ reserve balances in those places bore no interest. As Kazua Ogawa (2005, p. 1) observes, “Japanese banks have chronically held excess reserves since the late 90’s,” with excess reserves tending, as in the U.S. since October 2008, to rise pari passu with the Bank of Japan’s additions to the total reserve stock.

However, Kazua also observes that Japan is no exception to the rule that “reserve supply does not necessarily automatically create a demand for reserves,” and that Japan’s banks, no less than U.S. banks, “have their own motives for excess reserves.” The motives have, moreover, been more-or-less the same in both cases.

U.S. banks, as we’ve seen, accumulated excess reserves because the positive return on those reserves was greater than the still-positive return on wholesale as well as some retail loans. Japanese banks, in contrast, began hoarding reserves long before the Bank of Japan began paying interest on reserves a month after the Fed’s having done so, in November 2008.

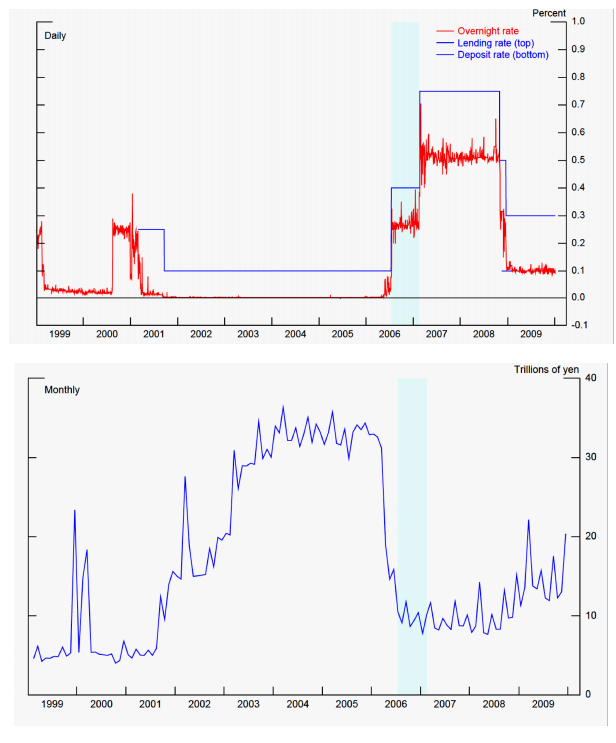

But as the U.S. case itself demonstrates, what matters isn’t the absolute IOER rate, but how that compares to rates on alternative uses of bank funds. In Japan before November 2008, although the IOER rate was zero, the overnight uncollateralized call rate—Japan’s equivalent to the fed funds rate—had itself fallen to zero, making reserves and call loans very close substitutes despite the fact that reserves bore no interest. The fact that Japanese depositors became increasingly leery of bank failures in the 90s finally tipped the scale in favor of reserves, as Japanese banks gained a further incentive to bolster their precautionary balances.

As can be seen in the pair of charts below, reproduced from Bowman, Gagnon, and Leahy (2010, p. 32), so long as the Bank of Japan paid no interest on banks’ reserve balances, Japanese banks accumulated excess reserves only after March 2001, when the Bank of Japan, in initiating its Quantitative Easing Program, allowed the call rate itself to fall to zero. When the BOJ ended that program five years later, while also increasing its lending rate, the call rate again rose above zero, causing Japan's banks to reduce their excess reserve balances. Finally, in November 2008, by beginning another round of Quantitative Easing, and reducing its lending rate to 30 basis points, the Bank of Japan brought the call rate back down 10 basis points, while simultaneously beginning to pay banks 10 basis points on their reserve balances. Consequently, Japanese banks once again began accumulating excess reserves.15

In short, like the Fed after October 2008, the Bank of Japan saw to it, intentionally or not, that Japanese banks' excess reserve balances rose and fell in lockstep with changes in the size of its balance sheet, which they would not have done had it maintained a positive spread between the call rate and the rate it paid on excess reserves. According to Ogawa's estimates, had Japan's call rate been 25 basis points rather than zero after 2000, even with no improvement in Japanese banks' perceived financial health, banks' subsequent demand for excess reserves might have been reduced by as much as 70 percent!

Thanks to the Bank of Japan's strategy, and in agreement with our own understanding that the influence of IOER on bank lending will be greatest where bank net interest margins are lowest, Japan's Quantitative Easing programs, instead of resulting in more lending by Japanese banks, had just the opposite effect, as seen in the next chart:

While it doesn't contradict the claim that IOER can be a crucial determinant of banks' willingness to accumulate excess reserves, Japan's experience does cast doubt on the suggestion that a U.S. IOER rate of zero would have sufficed after 2008 to have kept banks there from hoarding excess reserves. Whether it would have depends on whether other U.S. short-term rates, and the effective fed funds rate in particular, would have remained above zero. If not, nothing short of a negative IOER rate would have served to preserve a positive opportunity cost of reserve holding. Even so, a zero IOER rate would have supplied less of an inducement for reserve hoarding than a positive one. More importantly, as we shall see, Fed officials themselves were convinced that, had they returned the U.S. IOER rate to zero, the effective fed funds rate, despite falling further, would nevertheless have remained positive.

VII. d. IOER, Liquidity, and Bank Lending

Besides directly reducing bank lending by encouraging banks—and large U.S. banks and U.S. branches of foreign banks especially—to prefer, at the margin, acquiring excess reserves to making bank loans, IOER has also reduced it indirectly, by depriving those (mainly smaller) banks that have not been so inclined to accumulate excess reserves of their traditional means of covering themselves against the risk of short-run reserve shortages that additional lending entails. As the late Ronald McKinnon observed in a 2011 Wall Street Journal Op-Ed,

Banks with good retail lending opportunities typically lend by opening credit lines to nonbank customers. But these credit lines are open-ended in the sense that the commercial borrower can choose when—and by how much—he will actually draw on his credit line. This creates uncertainty for the bank in not knowing what its future cash positions will be. An illiquid bank could be in trouble if its customers simultaneously decided to draw down their credit lines.

Ordinarily, McKinnon continued, banks can cover their unexpected reserve shortfalls by borrowing funds from other banks on the interbank market. However, if “large banks with surplus reserves become loath to part with them for a derisory yield,” while smaller ones “cannot easily bid for funds at an interest rate significantly above the prevailing interbank rate without inadvertently signaling that they might be in trouble,” interbank borrowing ceases to be an attractive alternative to maintaining higher excess reserve cushions, even where the marginal return on reserves is less than that on loans.

The situation McKinnon describes is, of course, precisely the one that has prevailed ever since October 2008.

VII. e. Other Constraints on Bank Lending

To insist that IOER contributed to the post-Lehman decline in bank lending, and especially to the decline in lending as a share of total bank deposits, isn’t to deny that other developments also played a part in that decline. Most obviously, a decline in overall loan demand was part of the story. But to suggest that it was such a decline rather than IOER that mattered, as many in the banking industry seem inclined to do, is to erect a false dichotomy: if banks reduced their loans while increasing their reserves, they did so, not simply because lending became less lucrative, but because it became so relative to the alternative of reserve hoarding. Had it not been for IOER, banks would have been far less inclined to prefer reserves to low-yielding loans. IOER and reduced loan demand thus worked together, like the blades of a scissor, to discourage banks from lending.

A shortage of bank capital might, on the other hand, have prevented banks from increasing their loans despite the presence of both abundance of excess reserves and favorable lending opportunities. As Huberto Ennis and Alexander Wolman (2o11) explain,

As a readily available source of funding, high levels of reserves provide flexibility to a bank that is looking to expand its loan portfolio. However, loans (and risky securities) are associated with higher capital requirements than reserves. A bank that is holding reserves but is facing a binding capital constraint is thus unlikely to engage in a sudden expansion of lending. As with deposits, raising capital quickly can be costly. For this reason, even a bank that holds a high level of excess reserves may not be able to take advantage of new lending (or investment) opportunities (p. 276).

However, in their own study of this possibility, Ennis and Wolman find that, while many banks were indeed capital constrained during the Fed’s “first wave of reserve increases,” by the last quarter of 2009, bank capital had recovered to the point where, of $510 billion in reserves held by the biggest 100 banks, $485 billion were loanable. By the end of 2011, finally, almost all of the reserves held by the same banks were loanable given existing capital requirements. In separate study also looking at larger banks and BHCs, Jose Berrospide and Rochelle Edge (2010) likewise found that changes in BHCs’ capital ratios had only modest effects on loan growth. Instead of worrying about capital, banks and BHCs seemed more concerned about things like loan demand and risk. (Alas, Berrospide and Edge did not consider the possible influence of IOER.)

Nor does capital seem to have significantly constrained lending at the opposite end of the banking spectrum, where banks must usually rely on retained earnings to build capital. According to Jim Wilkinson and Jon Christensson (2011, pp. 43 and 46), who investigate lending by community banks in the Tenth Federal Reserve District between the start of 2001 and the end of 2009, programs established during the crisis for the purpose of placing funds into those banks’ capital accounts did so little to boost that lending that it would have been “more effective for policymakers to give money directly to small businesses in the form of grants or loans.”

VIII. IOER and Monetary Policy

VIII. a. IOER and Tight Money in 2008–9

Having considered the bearing of IOER on various sorts of bank lending, we're now equipped to consider how it influenced the course of the subprime recession and subsequent recovery. In brief, besides undermining economic productivity by diverting scarce savings from more to less productive uses, IOER contributed to both the recession itself and the slow pace of the subsequent recovery by serving as the instrument by which the Fed—whether wittingly or not—kept money too tight.

Although there were clear signs of trouble in the subprime mortgage market starting in early 2007, the recession to which those troubles eventually led didn't officially begin until December 2007. As is true by definition of any officially-designated recession, that one was heralded by a substantial decline in various measures of overall real economic activity, and particularly in the growth rate of real GDP, that had been going on for several months.

As is typically, though not necessarily, the case, the recession also involved a similar, but even sharper, decline in nominal GDP, or total spending on goods and services. From a peak growth rate of over 7 percent during the boom, nominal GDP growth declined gradually to about 4.75 percent in the third quarter of 2007. It then fell precipitously, reaching a low just shy of minus 3.2 percent by the second quarter of 2009. And although the growth rate of spending recovered considerably over the next year, since mid-2010 it has never again reached 5 percent, and has often been less than 3 percent. In short, spending has never made up the ground it lost during the recession's first year.

While the connection between reduced spending and recession isn’t inevitable, it’s a strong one, for reasons that aren’t difficult to grasp. For in order not to be accompanied by some decline in real GDP, a decline in nominal GDP would have to be matched by a proportional decline in prices, as measured by the GDP deflator. To the extent that it isn’t, because prices are “rigid” or “sticky” or for any other reason, real GDP must also decline. In practice, a sharp and persistent decline in overall spending is bound to bring a recession.

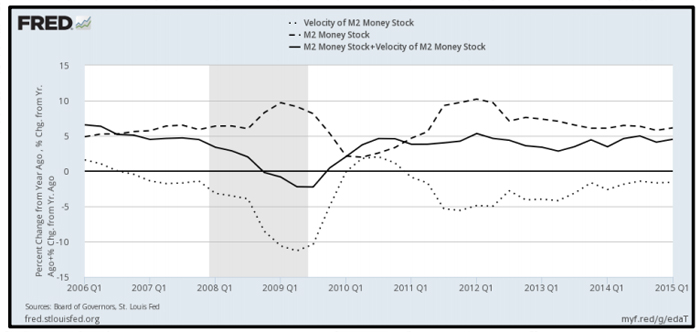

The volume of spending itself depends on the quantity of money, however one chooses to measure it, and its velocity, which can be understood as an inverse measure of the public’s demand for money balances, expressed as a share of their total earnings. As the next chart shows, although the velocity of M2 was growing at the beginning of 2006, by 2007 it was declining. That decline became increasingly rapid, and especially so after Lehman Brothers failed. By mid-2009, M2 velocity was more than 11 percent lower than it had been a year before. Although the quantity of M2 tended to increase as its velocity declined, the increase fell persistently and increasingly short of what was needed to maintain a steady growth rate of spending, let alone what it would have taken to restore spending to its original trend path. Instead, that growth rate fell steadily until, during the last quarter of 2008, it became negative.

In light of these statistics, it’s clear in retrospect that monetary policy had been too tight throughout 2007 and early 2008, and that this overtightening became especially pronounced during the last quarter of 2008 and the first quarters of 2009. Taking a 5 percent spending growth rate to represent the long-run trend, it’s equally clear that money remained too tight over the next several years to restore that spending growth rate, let alone make up for the fallen level of spending relative to where it would have been had the growth rate of spending never fallen below 5 percent.

The especially severe overtightening that followed Lehman’s failure reflected the FOMC’s desire to maintain the 2 percent fed funds rate target then still in effect. That target was, according to the committee’s reckoning, consistent with meeting the Fed’s inflation target, whereas anything lower risked surpassing that target. Finding that its subsequent emergency lending was undermining that chosen target, the Fed responded, as we’ve seen, by implementing IOER as a means for preventing any further “leakage” of its emergency credits into the fed funds market. IOER thus became the chief instrument by which the Fed aggravated, however inadvertently, the collapse in nominal spending that had already been in progress, making the recession that much more severe. Commenting on the Fed’s action not long afterward, blogger David Beckworth (2008) went so far as to compare the Fed’s mistake to the one it made in 1936–1937.

Not long ago another blogger, Scott Sumner (2017), having the advantage of hindsight, reached a verdict that was hardly less damning. “The decision to adopt IOR,” he writes (meaning, presumably, what we’ve labelled IOER), “helped to prevent the Fed from achieving its policy goals, by making the Great Recession more severe than otherwise.” He continues,

The world would be a better place today if the Fed had never instituted its policy of IOR in 2008. I really don’t see how anyone can seriously dispute this claim. If you want to dispute the claim, what specific way did IOR make the world a better place? When the policy was adopted in 2008, the New York Fed explained it to the public as a contractionary policy. Can anyone seriously argue that the world would be worse off if monetary policy had been less contractionary in 2008– 12? Why?

Fed officials were in fact aware of the economy's deteriorating state as they prepared to begin paying banks to hold reserves; that deterioration is what convinced them to finally reduce the federal funds rate target from 2 percent to 1.5 percent. Yet the Fed still went ahead, the very next day, with its IOER plan. The Fed chose, in other words, to ease monetary policy symbolically, while taking steps to prevent the reserves it was creating from actually contributing to a further lowering of the effective funds rate. The FOMC's next and final rate cut under what still appeared to be, but was in fact no longer, its traditional monetary control regime, from 1.5 percent to 1 percent, was likewise largely symbolic, for by then the fed funds market, considered as a market for interbank lending, had more-or-less ceased to function.

Thus far, at least, the Fed's experiment was proceeding according to plan. For despite the economy's ongoing decline, that plan called not for loosening monetary policy but for avoiding further loosening, along with the stimulus such loosening might provide, by preventing growth in the Fed's balance sheet from encouraging additional bank lending. By December 2008, however, the Fed concluded that the economy needed to be stimulated after all. The trouble was that achieving a stimulus in the Fed's new IOER- based regime was only barely possible in theory, and lamentably difficult in practice.

VIII. b. IOER and “Quantitative Easing”

The problem of course was that, so long as the IOER rate remained high relative to other short-term rates, including the going fed funds rate, the Fed’s asset purchases, no matter how large, would tend to lead to almost equal growth in banks’ excess reserve holdings, and therefore to very little growth in either bank deposits or monetary aggregates. That is, IOER would have the same effect during the Fed’s rounds of QE as it had beforehand, when the Fed’s balance sheet was expanding, not as part of a deliberate monetary stimulus program, but as the incidental consequence of its emergency lending. If it’s indeed true that “insanity is doing the same thing over and over again, but expecting different results,” then in expecting extra bank reserves to stimulate the economy after 2009, using the same operating framework they relied upon to prevent extra reserves from stimulating the economy following Lehman’s collapse, Fed officials were not playing with a full deck.

Small wonder then that, despite an almost 4.5-fold increase in the monetary base between December 2008 and December 2014, bank deposits grew only about 60 percent.16 Although this outcome took many commentators by surprise—including more than a few who feared that the Fed’s asset purchases would lead to high, if not hyper, inflation—it did so only because they hadn’t grasped the implications of the Fed’s IOER policy, and the new operating framework it established.

Fed officials, on the other hand, understood what they were up against. Indeed, they even disliked the expression “Quantitative Easing” because it suggested, misleadingly, that the Fed regarded LSAPs as a means for expanding the quantity of money, and for giving a boost thereby to spending, prices, and employment. Instead, the Fed hoped that its asset purchases might influence the real economy through other channels. In particular, they appealed to the existence of a “portfolio balance” channel, in which changes in nominal quantities, and in bank lending especially, played no essential part. Instead, the Fed’s asset purchases were supposed to boost real economic activity by altering relative asset prices. In particular, swapping bank reserves for long-term securities was expected to promote investment by lowering long-term interest rates.

But whether there really is such a thing as a portfolio balance channel is a matter of considerable controversy. Just before he left the Fed Bernanke, when asked how confident he was in QE’s effectiveness, famously replied that “The problem with QE is it works in practice, but it doesn’t work in theory (quoted in Harding 2014).” Though said in jest, there was more than a little truth in Bernanke’s remark—or in the last part of it at any rate. And Bernanke knew it. As a 2014 Financial Times article explains, according to theory that prevailed in the years before the crisis,17 so long as banks themselves are indifferent between holding new excess reserves and trading them for other assets, as they would be at the zero lower bound in the absence of IOER, and as they are if reserves bear interest at or above the going market rate, the Fed’s own asset purchases

should have no effects. All that happens is the central bank swaps one kind of government debt—money—for another kind of government debt, in the form of a long-term Treasury bond. That can only make any difference if investors have a strong preference for one kind of debt over the other (Harding 2014).

For the portfolio-balance channel to be relevant, it had to be the case, as Bernanke himself explained in his 2012 Jackson Hole speech, that “different classes of financial assets are not perfect substitutes in investors’ portfolios” (Bernanke 2012; my emphasis).

Concerning this theory, Stephen Williamson (2017) of the St. Louis Fed supplies what I believe to be the best, albeit very brief, assessment:

Basically, the idea is to think about QE for what it is—financial intermediation by the central bank. If QE is to work, and for the better, the reason has to be that the central bank can do a better job of turning long-maturity assets into short- maturity assets than either the private sector, or the fiscal authority.

So regarded, the theoretical merits of QE—or rather, of LSAPs—doesn’t seem especially compelling.

But did QE at least work in practice, as Bernanke claimed it did? In the aforementioned Jackson Hole speech, Bernanke went on to refer to statistical evidence that the Fed’s strategy had succeeded. But many other economists find this same evidence far from convincing. Williamson, for example, considers it “pretty sketchy”:

For the most part, the empirical work consists of event studies—isolate an announcement window for a policy change, then look for movements in asset prices in response. There’s also some regression evidence, but essentially nothing (as far as I know) in terms of structural econometric work, i.e. work that is explicit about the theory in a way that allows us to quantify the effects (ibid.).

The positive findings, furthermore, generally concern QE’s effects on bond yields only, rather than on more important macroeconomic variables, such as inflation and unemployment. As Mirco Balatti and his coauthors (2016, p. 3) quite properly observe, to conclude that QE was “effective” merely because it altered bond yields is to toy with the usual meaning of monetary policy effectiveness, by conflating a policy’s success in influencing an intermediate policy target with its success in achieving ultimate policy goals. According to those authors’ own assessment, while QE did indeed lower interest rates, and boost equity prices, it otherwise “struggled to propel the macroeconomy” (ibid., p. 5). Nor is their finding all that surprising. After all, not long before, former vice-chair Donald Kohn had reached a similar conclusion. “I think it’s fair to say,” Kohn remarked, that “although [LSAPs] were effective to some extent, people—even the Fed—were somewhat disappointed. It’s been a slow recovery from a very deep recession” (quoted in Harding 2014).18

The Fed’s post-crisis inability to achieve its desired inflation target offers striking proof of the inadequacy of its new operating system, and especially so since January 2012, when, for the sake of keeping the public’s inflation expectations “firmly anchored,” the Fed announced an explicit inflation target, consisting of a 2 percent annual increase in the Personal Consumption Expenditure (PCE) index (Board of Governors 2012). In making that announcement, the Board of Governors declared that “the inflation rate over the longer run is primarily determined by monetary policy” (ibid.). That was certainly true under the Fed’s traditional operating system, as is evident in the pre-crisis behavior of the PCE index, as shown in the chart below. During that time, for better or worse, the Fed had no difficulty maintaining a PCE inflation rate just a little in excess of 2%, which was then, according to many, the Fed’s implicit inflation target.19 In contrast, since it announced its explicit PCE target, with its new stuck-in-neutral operating system in place, the Fed has failed to reach that target in every quarter save that of the announcement itself—and has done so despite adding over one trillion dollars to banks’ reserve balances!

As the New York Times reported recently, although “the direct cost of mildly undershooting the Fed’s inflation target is low,”

hat is worrisome is not the direct damage, but the fact that the Fed has missed its (arbitrary) 2 percent target in the same direction—undershooting—year after year… . That in turn implies that the low-growth, low-inflation, low-interest rate economy since 2008 isn’t going anywhere. This would prove especially damaging if the economy ran into some negative shock; a lack of Fed credibility could leave it less able to prevent a recession (Irwin 2017).

VIII. c. Stimulus without IOER?

The most important question concerning the Fed’s approach to post-crisis stimulus is, not whether it was at all successful, but whether another approach might have been better. In particular, what would have happened had the Fed dispensed with IOER while still expanding its balance sheet?