Since its inception, supporters of the Jones Act have claimed that the law is essential to U.S. national security. Although indefensible on economic grounds, Jones Act advocates argue that its restrictions promote the development of both a U.S. merchant marine and shipbuilding and repair capability that can be utilized by the country’s military in times of war. This rationale appears to be more of an article of faith than the product of rigorous analysis.

This paper examines the national security justification. Contrasting the Jones Act’s stated objectives with observable results, the law is revealed to be a national security failure. With dwindling numbers of ships, mariners, and shipyards, the U.S. military’s ability to leverage these civilian assets during times of war has been deeply compromised. This paper finds this maritime decline to be the predictable result of the Jones Act’s misguided protectionism, whose theoretical underpinnings are deeply at odds with both sound economics and modern maritime realities.

Rather than continue this flawed policy, the Jones Act should be either repealed or significantly reformed. This paper proposes alternative methods for ensuring military access to civilian mariners that offer greater cost transparency and increased certainty of the mariners’ availability.

Introduction

If the Jones Act’s fortunes hinged on economics alone the law would have been repealed long ago. Economists who have studied the Jones Act are in near unanimity that it diminishes U.S. prosperity.1 A recent analysis published by the Organisation for Economic Co-operation and Development (OECD) estimates that the law’s repeal would increase U.S. economic output by up to $135 billion.2

But Jones Act supporters inevitably respond that the law’s economic costs are justified by its contributions to U.S. national security. Indeed, the conventional wisdom on Capitol Hill is that the Jones Act plays a vital role in undergirding the U.S. military and protecting the U.S. homeland.

Related Read

The Jones Act Is Protecting U.S. Shipyards to Death

Faced with such high prices shipping companies have delayed replacing their vessels and instead keep them years — and sometimes even decades — past their typical useful life.The Jones Act—formally known as Section 27 of the Merchant Marine Act of 1920—requires that vessels engaged in the domestic transport of goods be built in the United States, crewed by U.S. citizens, owned by U.S. citizens, and registered under the U.S. flag.3 The law’s advocates claim that these requirements bolster U.S. national security by ensuring the Department of Defense has wartime access to a merchant marine that can be used to transport military supplies and equipment. Indeed, the law itself lists in its stated purpose the necessity of a “merchant marine of the best equipped and most suitable types of vessels sufficient to carry the greater portion of its commerce and serve as a naval or military auxiliary in time of war or national emergency [emphasis added].”4

Claims that the Jones Act is a national security asset have generally gone unchallenged and, as a result, this justification is more an article of faith than the result of rigorous analysis. Much has changed in the nearly 100 years since the Jones Act became law, and the economic, maritime, and geopolitical realities that shaped policy in 1920 differ considerably from those of today. Taking account of these modern realities, this paper scrutinizes the Jones Act’s impact and concludes that the law has failed to bolster U.S. national security. In fact, it has likely subverted it.

The Essence of the National Security Rationale

Jones Act supporters claim that the law’s restrictions on foreign competition help foster a merchant marine and shipbuilding and repair capability that can be harnessed by the United States in times of war.5 This is the theory. The reality is quite different.

In the early 1990s the Jones Act was put to the test. Following Iraq’s invasion of Kuwait, the United States rushed soldiers, military equipment, and supplies to Saudi Arabia. Although this military build-up was highly successful, the Jones Act’s ship contributions were marginal at most. Of the 281 Ready Reserve Force (RRF)6 and commercial ships chartered by the Military Sealift Command during the conflict,7 a mere 8 were Jones Act–eligible, consisting of one roll-on/roll-off (RO/RO) ship, one heavy-lift ship, and six tankers.8 Of these eight, just five entered the Persian Gulf and only the lone RO/RO, a dilapidated ship called the Ponce, transported equipment from the United States to Saudi Arabia.9

Rather than the Jones Act ensuring even an adequate supply of U.S.-flagged ships, the United States found itself dependent on foreign-flagged vessels to transport the needed equipment and supplies. No fewer than 177 foreign-flagged commercial ships were chartered by the United States for the Persian Gulf War. Those ships transported 21.2 percent of total dry cargo and 26.6 percent of total unit cargo (U.S.-flagged commercial ships carried 12.7 percent of total unit cargo—cargo specific to particular military units—with the balance transported by U.S. government-owned vessels).10 So pressed was the United States for sealift capacity that it twice requested the use of Soviet-flagged cargo ships, but was rejected by Moscow both times.

The situation was little better on the manpower front. The promised pool of Jones Act mariners to crew government-owned ships was found distressingly shallow, producing a scramble to find the needed personnel. As the U.S. military’s official history of the Transportation Command’s performance during Operations Desert Shield and Desert Storm points out:

For Desert Shield/Desert Storm, [the Maritime Administration (MARAD)] needed nearly 4,200 additional commercial mariners to crew the RRF [Ready Reserve Force]. Who were they? Many who heeded the unions’ call were former merchant mariners who came out of retirement. Some of those were veterans of World War II, the Korean War, and the war in Southeast Asia. Nearly 200 cadets from the U.S. Merchant Marine Academy, Kings Point, New York, also served, as did 6 students and 6 professors from Massachusetts Maritime College. Some were raw recruits. The Seafarers International Union expanded its entry-level training program from 60 to 200 students per month to help put bodies on ships fast. The union also increased skill-upgrading courses for firemen and steam engineers from once a quarter to once a month. The Marine Engineers Beneficial Association/National Maritime Union, the Sailors Union of the Pacific, and other maritime unions developed similar programs to expand the pool.11

In explaining this lack of mariners, the report hints at the decline of the U.S. commercial fleet, of which Jones Act ships form more than half:

Fewer ships meant fewer jobs for merchant mariners and, as a consequence, manpower had dwindled almost 60 percent since 1970 to a current level of about 10,000. MARAD projected that it would be less than half that amount by the turn of the century. In 1990, the average age of a U.S. merchant seaman was 49 years old, which meant many of the mariners who manned the RRF ships during Desert Shield/Desert Storm were in their 60s and 70s. At least two were in their 80s. The oldest was 92. There were teenagers as well.12

Other actions to remedy the dearth of mariners included the waiving of licensing requirements and allowing crew members to sail with reduced qualifications.13 Yet despite such measures, the effort to secure sufficient manpower nearly met with disaster. When MARAD attempted to activate a second wave of 34 RRF ships to follow on its first wave of 55, it ran out of mariners from the U.S. crew pool before the activations could be completed. Fortunately, mariners from the Great Lakes fleet were willing and able to fill in after the lakes froze in January 1991.14

The Gulf War was no anomaly. Crew shortages also proved a headache for U.S. logisticians during the Vietnam War. Speaking at the Naval War College in 1969, the commander of the Military Sea Transportation Service,15 Vice Admiral Lawson Ramage, called the merchant marine manpower pool “barely adequate,” adding, “Crew shortages and consequent ship delays have been a continuing problem almost from the outset of the Vietnam escalation.”16 Statistics bear this out, with 42 percent (592 of 1,405) of the National Defense Reserve Fleet/Ready Reserve Force’s scheduled sailings delayed because of crew shortages during the years 1966–1968.17

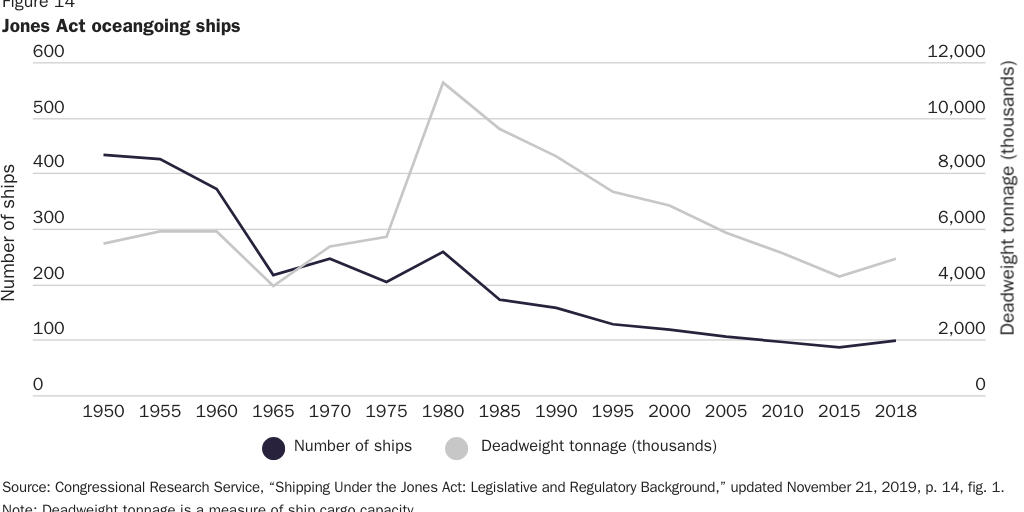

Downward pressure on the merchant mariner pool has not abated. The Jones Act fleet continues to atrophy, currently standing at a mere 99 ships, as seen in Figure 1.

The effect of the Jones Act fleet’s decline on mariners was underscored by a 2017 MARAD report, which warned that in a wartime scenario the United States would be at least 1,839 mariners short of the 13,607 needed to perform sustained sealift operations and to crew the U.S. commercial fleet.18

Alarmingly, that projection represents a best-case scenario that assumes all mariners with unlimited credentials (i.e., able to serve on any size ship operating anywhere) are available and willing to crew sealift vessels as well as the U.S.-flagged commercial fleet. These civilian mariners provide their services on a volunteer basis, however, and the report admitted that their willingness to actually do so in a war or national emergency is “beyond prediction.”19

Related Read

Jones Act Expensive, Benefits Questionable

The argument that removal of the Jones Act would leave the noncontiguous jurisdictions — Alaska, Hawaii, Guam and Puerto Rico — without adequate shipping, meanwhile, is completely specious and used by Jones Act interests to scare the public.The situation is equally grim on the shipbuilding and repair front. From 1983 through 2013, approximately 300 shipyards closed20 and shipbuilding employment fell from 186,700 in 198121 to 94,000 as of 2018.22 Today a mere four shipyards in the United States are in the business of constructing large oceangoing commercial ships.23 One of those four, the Philly Shipyard, currently has no ships on its order book and as of July 2019 had seen its employment reduced to approximately 80 people.24

The U.S. maritime industry’s dire state is obvious enough that even ardent supporters of the Jones Act, which was ostensibly meant to guarantee the industry’s welfare, concede that all is not well. Maritime Administrator Mark H. Buzby, for example, admitted in congressional testimony this year that U.S. commercial shipyards lack the “scale, technology, and the large volume ‘series building’ order books” to compete internationally. He noted that the five largest U.S. shipyards have collectively produced, on average, a mere five ships per year over the past five years.25 One senior official with a maritime union noted in 2018 that “the pool of licensed and unlicensed mariners has shrunk to a critical level” and that, absent changes, “the military will no longer be able to rely on the all-volunteer U.S. Merchant Marine.”26 Rep. John Garamendi (D‑CA), meanwhile, has questioned the country’s ability to keep its troops supplied if they were to repeat an invasion of Guadalcanal.27

In 2018 the head of the U.S. Transportation Command, General Darren W. McDew, commented that while the Jones Act was intended to ensure a baseline level of business to support both U.S. shipping and shipbuilding, the domestic fleet’s dwindling size “demands that we reassess our approach.” The country, he added, may need to “rethink policies of the past in order to face an increasingly competitive future.”28

The maritime status quo, of which the Jones Act plays a foundational role, appears increasingly untenable.

Jones Act: National Security Asset or Liability?

Given these realities, it seems increasingly apparent that the Jones Act’s contributions to national security are overstated and diminishing. In fact, the case stands on its merits that the law makes no contribution to national security and may even subvert it. There is considerable evidence that the Jones Act is a net national security liability.

As already described, the Jones Act’s domestic-build requirement means that Americans must buy ships for domestic use that are far costlier than those constructed abroad, as U.S. commercial shipbuilding has degenerated into its current uncompetitive state. This results in fewer ships and fewer mariners to draw on in times of war or national emergency.

Jones Act advocates counter that the provision is ultimately beneficial because it promotes U.S. shipbuilding. But that assertion is mistaken on at least two counts. First, as a 1985 government report notes, “sealift requirements for the initial stages of a modern major conflict depend more on the sufficiency of U.S.-controlled shipping—and on trained U.S. crews—than on shipbuilding capacity.”29 In other words, in the critical early stages of a conflict, a country’s shipbuilding capacity is less important than its ability to mobilize ships and crew—and the Jones Act’s domestic-build provision results in reductions of both. In addition, it is far from clear that the Jones Act has contributed to a more-robust shipbuilding capacity than would otherwise be the case.

That a law ostensibly meant to strengthen domestic shipbuilding by stifling foreign competition would have the opposite effect—a weakened industry—should not be a surprise. Some have argued that the rising fortunes of British commercial shipbuilding in the mid-1800s were due in part to the United Kingdom’s decision to discard its protectionist Navigation Acts. As author Clinton H. Whitehurst notes:

Another major factor that contributed to British shipbuilding and shipping success was the repeal in 1849 of the last of the Navigation Acts … [T]he English-built ship was protected from foreign competition in that foreign ships were excluded not only from England’s colonial trade but from home trade as well. The result of this protectionism was, at best, a mixed blessing. While these statutes ensured English shipping profits, they acted as a tranquilizer with respect to improvements in building wooden sailing ships. As one British authority points out:

Protection from foreign competition resulted in British ship design of 1845 differing little from the style to be found in 1815. [And] … statistics confirm the overall stagnant nature of the British shipbuilding industry in the 35 years before 1850.

With repeal of the Navigation Acts, the shipowner was free to buy his vessels anywhere he chose. But a policy of “free ships” also meant the shipbuilder must be competitive. No longer could he take a year or more to construct a vessel for a trading opportunity that could be gone before the ship was delivered to her owner. The competitive British clipper ship was fair evidence of the success of the new policy.30

It is, of course, impossible to know exactly how U.S. shipbuilding would have fared absent the Jones Act and other protectionist maritime laws that preceded it. Improving on the existing record, however, would not seem to be a terribly difficult task. As already shown, recent decades have seen substantial declines in U.S. shipbuilding measured both in terms of the number of shipyards and the number of workers employed there. This should be entirely expected given the costly nature of the ships built in these U.S. yards. Such high costs reflect a long-standing qualitative gap between U.S. shipyards and their foreign peers.

A 1983 government report authored by the now-defunct Office of Technology Assessment (OTA), for example, said that U.S. shipyards “generally employed lower levels of technology” than their foreign counterparts and had “not installed the level of modern shipbuilding technology necessary for high productivity in the construction of today’s major merchant ships.31 Comparing U.S. shipyards to those of Japan and South Korea, the report listed numerous ways in which the former fell short, which ranged from inferior levels of research and development to the reduced adoption of automation and robotics.

Two years later, a report issued by the U.S. International Trade Commission (USITC), citing industry observers, found that “the U.S. shipbuilding industry lags behind many of its foreign competitors in the use of modular construction techniques, in tooling, in the degree of automation, in the use of robotics, and in the methods of processing, joining, and assembling materials.”32 The report added that U.S. commercial shipyards “require approximately 40 to 60 percent more man-hours to construct the same ship as many foreign yards.”

A 2001 Commerce Department study provided a similarly gloomy assessment, noting that U.S. shipbuilding productivity had not improved since the mid-1980s and that U.S. shipyards lagged their foreign counterparts in ship construction and design, shipyard layout, and product engineering. “Among shipbuilding nations,” the report added, “U.S. shipbuilders rank at or near the bottom in terms of productivity, and the gap is widening [emphasis added].”33

A 2009 National Defense University (NDU) report suggested the picture was little changed. Once again comparing U.S. shipbuilders to those in Asia, the report found that the Asian yards offered lower prices, greater efficiency, and had higher industry best-practice ratings.34 An NDU report issued three years earlier, meanwhile, said that “a company representative [from a leading maritime consulting firm] familiar with the techniques employed by U.S. and European shipyards advised us that the U.S. shipbuilding industry is currently about fifteen years behind in implementing changes that would enhance productivity,“35 while a 2016 NDU report noted that U.S. shipbuilding is “an average of twenty years behind international shipyards regarding advanced technology.”36

Notably, both the OTA and the 2009 NDU reports suggested that the Jones Act was at least partly culpable for the yawning gap with foreign shipyards. The OTA report noted that, owing to federal shipbuilding subsidies (since discontinued), as well as the Jones Act, the United States has become an anomaly in the construction of major merchant ships. As the report states:

In many other major maritime countries, shipbuilding is viewed on a global perspective. This is not the same in the United States, where only 1 to 2 percent of the world merchant fleet is now built. The U.S. shipbuilding industry is basically quite different from that of Europe, Japan, and Korea. Those countries have built most of today’s modern shipping fleets and compete for orders in a world market. The United States does not.

This is completely logical. The Jones Act’s U.S.-build requirement has incentivized American shipyards to orient themselves away from the competitive international market and toward this captive domestic shipbuilding market. This, in turn, means reduced output (a mere two or three oceangoing ships per year), less competition, and the failure to develop a specialized market niche.37 All of these missing elements are vital to increased productivity and lowered costs. As the OTA report points out:

Briefly stated, U.S. yards have never had sufficient volume of merchant ship orders to specialize, to become truly expert, or to develop high efficiency. Flexibility to build many different varieties of ships and other marine equipment has been maintained in U.S. shipyards. Thus, the economies of mass production have seldom been adopted.38

The 2009 NDU report laid at least partial blame for the lack of U.S. shipbuilding competitiveness on “protectionist policies, such as the Jones Act, that have shielded domestic shipbuilders from the pressures of global competition,” while a 2007 NDU report sounded a similar note:

U.S. shipyards are not currently cost competitive in any of the major classes of large ships, and their annual market is limited to the six to ten large Jones Act ships destined for the domestic U.S. trade. Since the total Jones Act requirement is only a small fraction of the output of the largest Asian yards, the U.S. shipbuilding industry is locked in a cost/quantity trap, one that it appears unlikely to escape.39

This lack of shipbuilding competitiveness has wreaked havoc within the maritime industry, thus undermining national security. As a 2019 Congressional Research Service (CRS) report notes, the high cost of U.S. shipbuilding has prompted the Department of Defense to reconsider a plan requiring sealift ships to be built domestically and to instead focus on the purchase of foreign-built substitutes.40 “I can’t afford a lot of $600 million ships. I can’t really afford a lot of $400 million ships when I can go out and buy used RO/ROs for $35 to $40 million,” said Secretary of the Navy Richard Spencer in May 2019.41 The head of U.S. Transportation Command, meanwhile, explained the decision to pursue used foreign-built ships during a March 2019 congressional hearing by noting that such vessels cost $25–60 million depending on age. New domestic-built ships, he added, would cost twenty-six times as much.42

The U.S. military, in other words, has effectively been forced to look abroad to meet some of its ship construction needs because of cost inefficiencies encouraged by the Jones Act. As a 2015 NDU report states, “The Jones Act creates an environment where the U.S. government must pay a premium to buy a world-class navy.“43

Dependence on foreign-built ships to meet U.S. sealift needs is long-standing. Of the 46 vessels in the RRF, only 16 were constructed in U.S. shipyards. The 60 privately owned ships that participate in the Maritime Security Program are entirely foreign-built.44 So, the majority of the current putative sealift fleet is foreign-built and the U.S. Navy now plans to continue on the foreign-build path for the foreseeable future, given the destitute state of U.S. shipbuilding competitiveness.

This is nearly the exact opposite of what Jones Act supporters claim the law was meant to achieve.

Among Jones Act shipping companies, the costs of this policy are also evident. High domestic shipbuilding costs mean these carriers pay higher prices for ships and must charge higher freight rates. Higher rates deter the use of coastwise shipping, which, in turn, decreases the demand for ships, resulting in fewer ships and mariners available in times of war and national emergency. It also means less repair and maintenance work for U.S. shipyards that are part of the defense industrial base.

The paltry Jones Act fleet is lacking not just in raw numbers but also the diverse set of capabilities appropriate for an advanced economy. Ship types such as liquefied natural gas (LNG) carriers, liquefied petroleum gas carriers, and livestock carriers are entirely absent. Other ship types, although present, exist in extremely limited numbers. There are, for example, a mere two dry bulk ships—both of which are nearly 40 years of age—and a single chemical tanker, built in 1968. The fleet also does not feature any heavy-lift vessels. This, according to the CRS, has forced the Department of Defense to use “ ‘national defense’ waivers of the Jones Act to move radar systems and newly built vessels on foreign-flag heavy-lift vessels.”45

In addition, the Jones Act encourages the use of vessels that would be considered well past their useful life outside of the protected Jones Act market. Jones Act carrier Matson, for example, as of this writing employs a container ship, the Lihue, that was constructed in 1971. Another one of its ships, the RO/RO vessel Matsonia, was built in 1973 and in early 2019 suffered a major hull failure likely related to age-induced decrepitude.46

As of August 2019, nearly one-third of the Jones Act fleet—30 of 99 ships—was built in 1994 or earlier.47 Among the 42 nontanker ships, 26 were at least 25 years of age. To place this in perspective, Maritime Administrator Rear Admiral Buzby testified before Congress in March 2019 that it’s “rare to find ships in the commercial world beyond 15–20 years of age.”48 The advanced ages of these ships and their likely degraded condition would seem to call into question the Jones Act fleet’s ability to serve as a “naval or military auxiliary” in time of war or national emergency.

Access to dramatically lower-priced foreign-built ships is one obvious solution. As a 1985 report from the National Advisory Committee on Oceans and Atmosphere noted, “A modernized Jones Act fleet, including some low-cost, foreign-built vessels, would help not only the domestic ship operator, but the U.S. consumer at large and the Nation as a whole by enhancing the defense utility of the U.S. flag fleet [emphasis added].”49

Evidence of the benefits of competition to both consumers and U.S. companies is abundant throughout the economy. In other forms of transportation not subject to domestic-build requirements—which is to say, all other forms of transportation—U.S. firms play leading roles. Within the auto sector, Ford and General Motors are among the world’s top five largest automakers50 and the United States produces more autos than any country except China.51 Among aircraft manufacturers, the United States is a global juggernaut, with Boeing ranked as the world’s largest in 2018.52

That Boeing prospers in the absence of a domestic-build requirement is particularly noteworthy given the many similarities between the airline and shipping industries. Both are subject to cabotage restrictions, with foreign-registered airlines prohibited from transporting passengers or goods within the United States (with a limited exemption for Alaska).53 Like Jones Act ships, U.S.-registered airlines are also required to have at least 75 percent U.S. ownership. Furthermore, airlines play a key role in U.S. national security, with commercial aircraft often relied on in times of war to transport military personnel. In the Persian Gulf War, for example, more than 60 percent of the troops and 25 percent of the cargo airlifted were carried aboard civilian airliners.54 In 2003 nearly 500,000 troops were transported via the Pentagon’s Civil Reserve Air Fleet program.55

Yet, despite this critical national security role, there has been no serious effort to impose a domestic-build requirement on U.S. airlines. This is perhaps because there is a recognition that such a mandate would impair the ability of U.S. airlines to acquire the aircraft needed to build their fleets and compete in a cost-effective manner. The pressure of international competition benefits the U.S. aircraft manufacturing industry by forcing it to constantly improve and innovate. A domestic-build requirement would reduce those incentives, leaving U.S. aircraft manufacturing in a weakened position.

Productivity comparisons between shipbuilding, aircraft, and auto manufacturing are illuminating. According to the Commerce Department, output per employee in shipbuilding rose by 45 percent from 1977 to 1998, while over the same period auto assembly output per employee increased by 117 percent and aircraft assembly output rose 88 percent.56 Were the U.S. shipbuilding industry able to achieve similar productivity gains, it would reduce the cost of U.S.-built ships. This, in turn, would increase the number of vessels built and the number of U.S. mariners who crew them.

Useful lessons may also be found in the examination of shipbuilding sectors from other highly developed countries. Norway and Finland, for example, do not have domestic-build requirements and they have less onerous cabotage restrictions than the United States.57 These two countries have a combined population that is nearly 30 times smaller than that of the United States, yet they feature shipbuilding employment that is only seven times smaller.58 Furthermore, both countries have internationally competitive shipbuilding segments—offshore service vessels and fishing vessels in the case of Norway,59 and cruise ships and icebreakers in the case of Finland (the country produces 70 percent of the world’s icebreakers).60

The European Union, meanwhile, has approximately 40 large shipyards active in the global market for large seagoing commercial vessels.61 In contrast, the United States builds no oceangoing ships for export62 and as a 2017 National Defense University report states, “There seems to be little prospect of U.S. shipyards winning much export business for commercial vessels.”63

Such facts make it easier to understand why a 2019 Organisation for Economic Co-operation and Development study concluded that, in the long term, repeal of the Jones Act has the potential to increase the U.S. commercial shipbuilding industry’s total output from $859 million to $1.47 billion—as well as raise its value-added by about $44 million (from $412 million).64

Other factors also merit consideration in the national security calculus. The Jones Act is based on the notion that U.S. self-reliance—in this case, in terms of shipbuilding, ships, and mariners—is preferable to relying on foreigners, including U.S. allies and partners. Yet the Jones Act discourages the very self-reliance it is premised on. A 2013 Government Accountability Office (GAO) report, for example, cited numerous anecdotes of importers in Puerto Rico choosing foreign goods over those produced in the United States because the high cost of Jones Act transportation made them too expensive. Among these examples were jet fuel sourced from Venezuela instead of the U.S. mainland, as well as other products from foreign sources including fertilizer, feed, corn, and potatoes.65

Perhaps most infamously, the law also effectively forces Puerto Rico to source its natural gas from abroad, as there are no Jones Act–eligible ships to transport the fuel from the U.S. mainland. In 2018, Russian natural gas was imported into Massachusetts during a wintertime demand spike—despite the fuel’s domestic abundance—owing to the total lack of Jones Act ships.66

Finally, it should be noted that, despite being commonly hailed as a national security asset, the Jones Act has regularly been suspended in times of war or national emergency, including World War II, the Persian Gulf War, and in the wake of various natural disasters. In other words, when the exact situations that the Jones Act was intended to address arise, the law often must be waived because it has failed so abjectly. At such times, reality intrudes and common sense prevails.

Destined to Fail

The Jones Act’s glaring deficiencies do not surprise, given the incongruity between the law’s objectives and the means by which it seeks to accomplish them. Based on a theoretical underpinning that is deeply at odds with modern maritime realities, the Jones Act’s failure is merely the law reaching its inescapable conclusion.

Shipping versus Shipbuilding

A desired U.S. capability to be able to construct and repair the large numbers of ships required in a global conflict helps explain the impetus for the Jones Act’s domestic-build requirement. By preventing Americans from using foreign-built ships to conduct domestic commerce, the law provides U.S. shipbuilders with a captive market. These U.S.-built ships, however, are vastly more expensive than those produced overseas. This means that the buyers of these ships are footing the bill for what amounts to a massive subsidy to the shipbuilding sector (to the degree that demand even exists for such expensive ships).

Such extremely high price tags limit the demand for ships, raise the cost of transporting cargo, and consequently make waterborne transport a less attractive option for moving goods. This, in turn, means fewer ships are available to serve the needs of the U.S. economy and to respond effectively to national emergency. Meanwhile, U.S. shipyards—and their skilled workers—are themselves harmed because fewer ships means reduced opportunities to perform maintenance, repairs, and upgrade work. Moreover, the dearth of ships frustrates the policy goal of ensuring sufficient numbers of mariners to crew both government-owned and commercial ships in wartime.

The inherent conflict between the protection of U.S. shipbuilding and the desire for robust U.S.-flagged shipping has not escaped the notice of military logisticians. Writing in the Defense Transportation Journal in 1993, former commander of the U.S. Transportation Command General Duane H. Cassidy said that if he was king for a day, one of his decrees would be to decouple the U.S.-flagged shipping industry and the shipbuilding industry. “The continued yoking of these two industries stifles competition for both,” Cassidy said. “Carriers, to be competitive, need to buy new ships where the market dictates, like any other U.S. business.”67

Jones Act’s Limited Wartime Benefit to U.S. Shipbuilding

One of the Jones Act’s advertised benefits—a domestic capability to build large, oceangoing ships during times of war—has proven to be of limited utility. Since the Jones Act’s passage, the United States has been in only one conflict, World War II, that required a large increase in shipbuilding. In many of the other military interventions, such as the 1991 Persian Gulf War, the conflict ended long before a new ship could have been built had the necessity arisen.

Even during World War II, however, it is not apparent that the Jones Act contributed much to the country’s shipbuilding capacity. Scant commercial shipbuilding took place in the years preceding the war and a vast expansion of U.S. shipbuilding capacity was required to meet the country’s wartime needs.68 An emergency shipbuilding program announced by President Franklin D. Roosevelt in January 1941—nearly a year before the United States entered the war—for the construction of 260 cargo vessels, for example, necessitated approval for the construction of nine new shipyards.

Costlier Ships

When the Jones Act was passed, U.S.-built ships were estimated to be 20 percent more expensive than those built overseas.69 Since that time, the cost premium attached to vessels constructed in the United States has risen dramatically. As a 2019 Congressional Research Service report points out:

The cost differential increased to 50% in the 1930s. In the 1950s, U.S. shipyard prices were double those of foreign yards, and by the 1990s, they were three times the price of foreign yards. Today, the price of a U.S.-built tanker is estimated to be about four times the global price of a similar vessel, while a U.S.-built container ship may cost five times the global price, according to one maritime consulting firm.70

The picture worsens when the time required for construction is considered. A 1981 GAO report found that “it takes about 2 years longer to build oceangoing vessels in the United States than overseas,“71 while a 1985 U.S. International Trade Commission study stated that “U.S.-built commercial ships take twice as long to build and cost two times as much money as many comparable foreign-built vessels.”72

Anecdotal evidence suggests this remains the case. From 2018 through mid-2019, a total of four Jones Act self-propelled oceangoing ships were built in U.S. shipyards. Two of these were 3,600 TEU (“twenty-foot equivalent unit,” a measure of volume equivalent to a twenty-foot-long shipping container) container ships built by the Philly Shipyard, and the remaining two were hybrid container-RO/RO vessels with a 2,600 TEU cargo capacity as well as room for 400 vehicles that were built by VT Halter Marine. These four vessels required 35 to 42 months to construct, measured from the time the keel was laid to the official date of completion. In comparison, one of the largest container ships in the world, the 21,413 TEU capacity OOCL Hong Kong, completed in 2017, had a build time of 18 months (and cost at least $50 million less than each of the 3,600 TEU ships built by the Philly Shipyard).73

Given such extraordinary cost differentials and the burden they put on the U.S. maritime sector, it is worth considering whether the Jones Act would be passed by Congress today.

Bifurcation of U.S. Shipbuilding

An important reason for the Jones Act’s U.S.-build requirement is that, presumably, it would help to ensure the existence of shipyards where vessels could be built for the U.S. military.74 But the degree of overlap between Jones Act commercial shipbuilding and naval shipbuilding is not nearly as great as many observers may believe. As a 2019 report from the Center for Strategic and Budgetary Assessment notes, “most shipyards that build larger U.S. Navy and Coast Guard ships do not generally construct commercial vessels.“75 Of the country’s major commercial shipyards, only one—General Dynamics NASSCO—constructs both large naval (noncombatant) and commercial ships. The Philly Shipyard, which has built approximately half of all large ocean-going Jones Act commercial ships since 2000, does not build any military vessels.76

A 2019 analysis performed by scholars at the American Enterprise Institute calculated that, for the six companies that have built naval and commercial vessels since 2000, Jones Act merchant vessels accounted for a mere 5 percent of orders (by the number of ships).77 This finding dovetails with a 2013 GAO report that noted the vast majority of military vessels are built at seven major shipyards, some of which “also construct a small number of commercial vessels.”78

There is little reason to think this will change, given the increasingly distinct nature of commercial and naval shipbuilding. As a 2001 Commerce Department report notes, “The technical specialization applied to a naval vessel is not applied to commercial ships, and the technology in both fields is advancing to such an extent that the two modes of construction are growing increasingly segregated.”79

U.S. Dependence on Foreign Components and Know-How

Jones Act supporters may be tempted to believe that the high cost of U.S.-built ships is a small price to pay for freeing the United States from dependence on foreign shipbuilding, but this “independence” is illusory. To comply with the Jones Act’s domestic-build mandate, ships must be assembled in the United States and all “major components of the hull and superstructure” fabricated domestically.80 This means, however, that other key parts of a ship can be—and often are—produced abroad. Even the steel plating used in a vessel’s construction can be of foreign origin provided it is delivered in “standard mill shapes and size.”81

A container ship delivered by the Philly Shipyard in 2018, the Daniel K. Inouye, serves as a good example. While Jones Act–eligible, the ship includes numerous components that were sourced from foreign firms, including the main generator engines (Hyundai Heavy Industries, South Korea); steering gear (Rolls Royce, United Kingdom); auxiliary boiler (Alfa Laval, Denmark); propulsion engine (MAN Energy Solutions, Germany); maneuvering thruster (Kongsberg Maritime, Norway); and propeller (Hyundai Heavy Industries).82

Beyond components, foreign know-how is also frequently required to construct many of the Jones Act fleet’s large ships. In 2006, one of the few U.S. shipyards that builds large oceangoing ships, General Dynamics NASSCO, signed a partnership agreement with Daewoo Ship Engineering Company that would see the South Korean firm “provide the detail designs, support services and some of the material necessary for ship production.“83 The fruits of this agreement are readily apparent, with Daewoo serving as the design agent for the Kanaloa-class ships currently being built at the shipyard.84 Philly Shipyard’s 2018 annual report, meanwhile, highlights its “access to global shipbuilding and design expertise with partners in Asia and Europe,” adding that the company typically seeks to “identify and license existing best-in-class designs and cooperate with the owners of such designs to make such modifications as are necessary.“85

Foreign reliance can also be seen in liquefied natural gas carriers, a type of ship that doesn’t even exist in the Jones Act fleet. As a 2015 GAO report noted, to build such a vessel—which has not been done in the United States since 198086—one shipyard acknowledged that it would likely have to “hire an additional 250 to 300 skilled Korean workers for the duration of the build time to ensure the work is done correctly.“87

A Jones Act ship built in 2018, the El Coquí, nicely captures the U.S. reliance on foreigners in ship construction. Designed by Finnish company Wärtsilä using teams in Norway and Poland, it features a foreign-built engine and liquefied natural gas fuel tanks, while the shipyard that assembled the vessel, VT Halter, is the U.S. subsidiary of Singapore-based firm ST Engineering.88

Shipyards in the United States may be engaged in limited construction of oceangoing commercial ships—albeit at frightfully high costs that would be even higher absent their access to foreign components—but it is an open question just how truly American these ships are or how meaningful the practical difference is between manufacturing these ships in the United States versus buying them from foreign yards.89

Wartime Availability of Allied Shipbuilding and Repair Facilities

Implicit in the Jones Act’s logic is that a premium should be placed on U.S. self-reliance for its shipbuilding and repair needs in time of war. Such thinking, however, ignores the fact that U.S. defense allies, particularly Japan, South Korea, and certain members of NATO, are some of the world’s leading shipbuilding countries. As a 2006 NDU report points out:

Another argument against overseas construction of naval ships is that access could be taken away, leaving the U.S. without the capacity to build ships when needed. This is unlikely since there are many yards that are allies, and it is unrealistic to assume all of them would simultaneously turn down revenues and deny access.90

It’s also worth pondering whether in conflicts with either China or Russia (cited by the 2017 National Security Strategy of the United States of America as “challeng[ing] American power, influence, and interests”), the United States would send its damaged ships to be repaired in the nearby shipyards of allied countries in Europe and Northeast Asia rather than having them limp or be towed back across the Pacific or Atlantic Oceans.91

Questionable Wartime Utility of Jones Act Ships

For the Jones Act–eligible ships that are assembled in U.S. shipyards, it is unclear how much benefit they offer in a wartime scenario. Built for commercial purposes, their capabilities do not always align with those demanded by the U.S. military. As a 1984 Congressional Budget Office study noted:

[T]here is a growing dichotomy between those features that produce a commercially efficient ship and those that yield ships more useful for support of military operations. In general, the most militarily useful ships tend to be:

- Relatively small—able to go in and out of shallow or otherwise restricted waters;

- Flexible—able to carry a variety of cargoes; and

- Self-sustaining—able to load and off-load cargo without specialized shore facilities.

Unfortunately, these characteristics are at odds with those of the most efficient commercial ships, which tend to be large, specialized, and dependent on port facilities for efficient loading and offloading. This difference in the qualities that provide military utility as opposed to those that produce commercial efficiency leads to some fundamental difficulties in developing an effective national maritime policy.92

This gap between military and commercial needs appears to have only widened in the years since the Congressional Budget Office report was first authored. A 2016 report from the National Defense University, for example, noted that the ships needed to transport military personnel and cargo “do not always line up with the vessels demanded by the market for moving commercial merchandise across the waterways.”93 A 2015 CRS report, meanwhile, pointed out that “the trend toward highly specialized and larger ships in the commercial sector appears inconsistent with the military’s shipping needs.”94

The CRS report’s description of RO/RO ships offers an instructive example:

Roll-on/roll-off ships are particularly useful for the military, and they make up a disproportionate share of the vessels eligible for cargo preference. In the commercial market, however, this ship type has evolved into specialized vessel types that do not offer the flexibility the military requires. One example is “pure car carriers,” ships designed around the weight and dimension of the passenger automobile and unable to accommodate the wider variety of equipment and supplies for which military sealift may be required. The military also seeks fast ships whose engines are fuel-inefficient relative to commercial carrier needs. Commercial vessels built during the past few years have generally been designed to operate at relatively slow speeds to conserve fuel, and this is potentially inconsistent with military needs.95

This divide between military and commercial shipping needs appears particularly pronounced in terms of U.S.-built ships—the basis of the Jones Act fleet. Indeed, a 2010 CRS report flatly stated that “very few commercial ships with high military utility have been constructed in U.S. shipyards in the past 20 years.” Consequently, when the Military Sealift Command has the need to charter a vessel, the report added, “nearly all of the offers are for foreign-built ships.“96

Given such facts, it’s perhaps not surprising that the CRS stated in its 2015 report that the military value of the U.S. Merchant Marine—of which the Jones Act fleet is a key component—“may now have more to do with the crews than with the ships themselves.“97

Puerto Rico poured $285 million to turn the old port of Ponce into a major transshipment hub for the container trade, dubbing it “Puerto de Las Américas,” but the expectation that ocean carriers would take advantage of a new, centrally located Caribbean facility has not panned out.So far the port is mostly empty, unable to attract much business from ocean carriers. It is a virtual ghost town.Analysts point to the Jones Act as a reason for the port’s lack of appeal to carriers.

Limited Ship Availability

Further evidence for the devalued importance of Jones Act ships in a national security context is the limited availability of such vessels. Despite the pressing need for sealift during the Persian Gulf War, only a single Jones Act ship, the Ponce, was taken out of commercial service to support the military’s logistical needs. The reason for this may be that the limited number of Jones Act ships had to remain at home because they were vital to the country’s domestic transportation needs. This is particularly true in the case of its noncontiguous states and territories where the fleet’s container and RO/RO ships exclusively operate. Thus, pulling ships from those trades could introduce considerable havoc through the disruption of key supply linkages for the inelastic necessities that provide the basis for employing these costly ships.

It is for this reason that even defenders of the Jones Act admit to the limited wartime utility of such vessels. “Today the only such [commercial] ships being built in the U.S. are those destined for Jones Act routes,” says Loren Thompson, chief operating officer of the Lexington Institute. “That is not a lot of vessels, and if war broke out most of them would already be engaged in other tasks.”98

Policy Alternatives

The Jones Act is a failure. Its goal of ensuring sufficient sealift capacity for U.S. military forces, however, is completely reasonable. Indeed, it is a necessity for U.S. national security.

In a world where ships are ubiquitous and shipbuilding capacity for all kinds of vessels is deep and broad, the Jones Act could contribute to national security by focusing on the objective of ensuring a ready reserve of trained mariners to crew our sealift ships. If the Jones Act’s onerous and unusual domestic-build requirement alone were repealed, the supply of ships and the demand for mariners would rise.

The following are three approaches to eliminating the current shortfall of U.S. mariners and for sustaining a sufficient number of sailors. Each could be implemented in conjunction with the Jones Act’s repeal.

Establish a Civilian Merchant Marine Reserve

The U.S. Merchant Marine occupies an interesting position within U.S. national security. Assigned a vital role in defense planning, its strategic value is reflected in the U.S. Merchant Marine Academy’s status as one of the country’s five military service academies. But, despite their importance to national security, most U.S. merchant mariners are not members of the military. Their civilian status and the absence of an attendant obligation that comes with military service make uncertain the numbers who would be willing and able to serve in a wartime scenario.99

Beyond generating uncertainty, there are intrinsic disincentives for mariners to serve in times of conflict. For example, mariners are asked to place themselves in harm’s way, but are generally not considered veterans for the purpose of accessing related federal benefits.100 There are other complications, as well. John Konrad, founder of the maritime website gCaptain, notes that despite the critical military role played by civilian merchant mariners, the U.S. military does not provide them training on such important matters as how to join a military convoy or share information with Naval Intelligence.101

One option for resolving this problem is to formalize the Merchant Marine’s role through the establishment of a civilian Merchant Marine Reserve—something akin to the reserve components of other military services. Members of this reserve would receive periodic training to keep them up-to-date on new ship technologies and systems, to obtain needed military knowledge and skills, and to help ensure their crewing licenses are maintained. They could then be called on in time of war or national emergency to crew government and/or commercial ships needed to provide sealift. Those called up for wartime service would be provided with veteran’s benefits commensurate with the importance of this critical military service.

The establishment of such a reserve has been previously studied by the U.S. government. Reports authored by the Maritime Administration in 1987 and 1991 examined such an approach for ensuring a pool of qualified, committed mariners, and a 1991 Department of Transportation Inspector General report recommended that such a program based on MARAD’s 1991 study be implemented. A 1991 Department of Defense and Transportation Ready Reserve Force working group report also endorsed this approach.102

The establishment of a civilian Merchant Marine Reserve would have at least three key advantages over the status quo.

First, it would help remove uncertainty as to the number of mariners the U.S. government could rely on in a wartime scenario, since these mariners would be compelled to report for duty.

Second, the federal funding of such a reserve would be a much more equitable system of providing military sealift. Under current arrangements, the cost of the Jones Act is disproportionately borne by the country’s noncontiguous states and territories that heavily rely on ocean transport for their trade with the U.S. mainland. This means that, to the extent the Jones Act provides a sealift capability for the U.S. military, it is disproportionately paid for by citizens of these states and territories, including poverty-stricken Puerto Rico. No other national defense program relies on such small portions of U.S. society in such a concentrated fashion.

Third, such an approach would make the costs of providing military sealift transparent. By effectively funding much of the existing military sealift through the Jones Act, the costs are rendered opaque. Similarly, the law’s claimed benefits, such as the number of U.S. mariners that exist because of the Jones Act, are not known with any great precision. Federal funding would eliminate these unknowns and provide greater clarity about costs, benefits, and the tradeoffs between them.

Furthermore, previous studies suggest the cost-effectiveness of a civilian reserve. The 1987 MARAD study placed the cost of such a program comprising 6,480 mariners at $46 million ($104 million in 2019 dollars).103 This amount is a small fraction of the loss in economic welfare that most analyses of the Jones Act attribute to the law.

Provide Merchant Marine Wage Subsidies

An alternative approach, or perhaps a complementary program, to the establishment of a Merchant Marine Reserve would be to offer wage subsidies to U.S. mariners in order to help preserve a pool of Americans who could crew U.S. ships in wartime or national emergency. Such subsidies would be paid to the employers of these U.S. seamen to boost the attractiveness of employing Americans. In exchange for such subsidies, these employers would be obligated to allow these crew members to serve aboard U.S. ships in time of war or national emergency without losing their employment.

As with a Merchant Marine Reserve, such an approach would offer the advantages of greater equitability and transparency in the provision of U.S. sealift.

Allow the Wartime Use of Foreign Mariners

If the pool of U.S. mariners is deemed insufficient to meet both military and commercial needs in wartime, then policymakers should consider allowing foreign mariners to crew chartered auxiliary commercial sealift ships. Foreign citizens, it should be remembered, are allowed to enlist and serve in the U.S. military. Foreign citizens also have a history of providing support to the U.S. military in civilian capacities. In recent times, for example, tens of thousands of foreign nationals have helped carry out logistical functions while working on U.S. military bases in Iraq and Afghanistan.104

The use of foreign crews on ships that transport U.S. military supplies is far from unprecedented. As already noted, dozens of foreign-flagged and foreign-crewed ships were used as part of the sealift effort in support of Operations Desert Shield and Desert Storm. In addition, a 2002 GAO report notes that “about 43 percent of cargo shipped overseas in 2001 as part of deployments involving major equipment in support of overseas operations was carried on foreign-flagged ships.“105 There are no known instances of sabotage being conducted by foreign crew in either the 2001 deployments or as part of Desert Shield/Desert Storm.

That is not to deny that there are issues of concern. During the sealift effort in support of Desert Shield/Desert Storm, 13 (out of 177) foreign-flagged ships either hesitated or refused to deliver their cargo to its final destination.106 To reduce the possibility of such occurrences or other associated risks, the U.S. military or Military Sealift Command could restrict senior positions on the ship to U.S. citizens. Another possible measure might be to perform background checks on these foreign mariners to prequalify them prior to the outbreak of hostilities and/or restrict eligibility for this program to citizens of countries that have defense treaties with the United States.

Related Read

The Obscure Shipping Law Leaving New Englanders in the Cold

At the same time the United States has emerged as one of the world’s largest exporters of liquified natural gas, by law, none of it can be transported by ship to New England — or anywhere else in the country.While using foreign mariners may present risks, it should be remembered that the use of U.S. mariners is also not risk-free and that the current shortage of U.S. mariners presents its own significant risk.107

Conclusion

With the number of shipyards, ships, and mariners all in decline, the Jones Act can only be described as a massive policy failure. Worse, the law has produced an outcome that is perilously at odds with its stated goals. Policymakers must consider either major reform of the law or outright repeal.

The law’s failure was an utterly predictable consequence. Conceived in discredited protectionist fallacies, the Jones Act deprives U.S. shipbuilding of the most essential ingredients of continuous improvement and innovation: foreign competition. The law effectively has condemned U.S. shipbuilding to second-rate status, which becomes more apparent with each passing decade. Meanwhile, a country whose geography would seemingly make it destined for maritime commercial greatness has a domestic fleet whose size and strength continues to plumb new depths.

A law meant to ensure maritime strength has delivered the exact opposite.

After nearly 100 years of failure, it’s time for a new approach. Shipbuilding and coastwise transportation in the United States must be exposed to the competition that has proved to be so successful for industries throughout the U.S. economy. Beyond the economic boon it will inspire, the Jones Act’s repeal would help restore the maritime industry’s former greatness and make the country safer and more prosperous.

Citation

Grabow, Colin. “Rust Buckets: How the Jones Act Undermines U.S. Shipbuilding and National Security” Policy Analysis No. 882, Cato Institute, Washington, DC, November 12, 2019. https://doi.org/10.36009/PA.882.

About the Author

This work is licensed under a Creative Commons Attribution-NonCommercial-ShareAlike 4.0 International License.