Before COVID-19, the U.S. debt burden was large and on an unsustainable path under reasonable assumptions about economic fundamentals. Standard policy responses, such as higher taxes or lower discretionary spending, could not substantially slow the growth of the U.S. debt burden; only reduced growth in entitlement spending, especially on Medicare, had the potential to avoid eventual fiscal default. COVID-19, the ensuing recession, and the subsequent policy responses have all increased U.S. deficits substantially, potentially altering these conclusions. But these events are likely to be temporary and may be partially offset by other demographic and economic changes related to COVID-19. As a result, the pandemic did not substantially alter the projected path of the U.S. fiscal imbalance. That bit of good news does not alter the grim long-term U.S. fiscal outlook. The most effective way to slow the growth of the debt burden is to cut entitlement spending substantially.

Introduction

Long before COVID-19 struck the global economy, the U.S. debt-to-GDP ratio was large and growing. At the end of 2019, federal debt held by the public stood at 79.2 percent of GDP, up from 40 percent in 2008. The Congressional Budget Office (CBO) projected this ratio would reach 100 percent by 2032 and nearly 150 percent by 2049.1 Extending the CBO methodology suggested that, under existing policies, the debt would grow indefinitely relative to GDP.

Expert opinion varied widely about the policy implications of those projections. Some observers found them alarming, arguing that the U.S. faced near-certain default and fiscal meltdown (albeit not for years or decades, given historical experience).2 Other observers were less concerned, pointing to low interest rates as evidence that the market is not overly alarmed.3 Still other economists voiced concern about the slow U.S. recovery after the Great Recession and argued that additional fiscal stimulus would help long-term output, even if it meant higher deficits.4 Finally, some analysts and politicians simply prioritized greater spending or lower taxes, with little regard for the longer-term fiscal outlook.

In this paper, I address how the COVID-19 pandemic, the ensuing recession, and subsequent policy responses have affected the U.S. fiscal imbalance (FI). The answer is not obvious, since recent events and policies could push FI in both directions. Lower interest rates and higher mortality rates among the elderly imply a smaller FI, other things being equal. Lower tax collections as a result of the recession, and higher expenditures on COVID-19 policies and the fiscal stimulus, imply a larger FI. I use recently updated projections from the CBO to discuss the net effect of these forces.

The perhaps surprising conclusion is that, while COVID-19 has had a significant short-term effect on the debt-to-GDP ratio, it is unlikely to alter dramatically the trajectory of FI in the long run. Increased relief spending, lower GDP growth, and lower tax revenues will cause deficits to balloon over the next few years. Longer term, however, lower interest rates and slight declines in mandatory outlays will help offset some of these fiscal effects. And, presumably, most of these factors will be temporary, thus affecting the level of debt but not its long-term growth rate. Overall, COVID-19 has not changed the fact that FI remains large and unsustainable because pre-pandemic entitlement programs and other expensive policies—notably Medicare, Medicaid, Social Security, and the Affordable Care Act—had already put U.S. fiscal policy on that path.

In this paper, I will review the basic framework for projecting the deficit, debt, taxes, expenditures, and overall fiscal imbalance. Then I will review pre-pandemic estimates of the U.S. fiscal path, discuss the robustness of these estimates to alternative assumptions, and outline how different policy adjustments might affect that imbalance. Using updated CBO projections, I will examine how the fiscal outlook has changed and suggest that the pandemic has not substantially altered the policy options for addressing the imbalance.

Determinants of the Debt-to-GDP Ratio

The path of the debt-to-GDP ratio depends on three variables: the interest rate ( r), the GDP growth rate ( g), and the noninterest (primary) deficit relative to GDP ( p).

Specifically, the debt-to-GDP ratio at the end of year t + 1 is given by

where Debt t is the outstanding stock of debt at the end of year t, Primary t+1 is the primary deficit (total deficit minus interest payments) in year t +1, and Interest t+1 is net interest payments made by the government in year t + 1 (all values are in nominal dollars). The debt-to-GDP ratio grows at rate

where

g is the growth rate of nominal GDP, and, as above,

which is equivalent to the average nominal interest rate paid on federal debt. Whenever p < g − r, the debt burden declines.

In the special case where p = 0 and interest rates are lower than the growth rate, any amount of outstanding debt will shrink relative to GDP. In this scenario, the debt-to-GDP ratio grows at a rate of

In this case, as long as r < g, the debt-to-GDP ratio will decline, lowering the government’s debt burden and making interest payments more affordable.

But this scenario does not describe the current fiscal outlook. Although r < g, the federal government runs large primary deficits because it spends substantially more on noninterest categories than it collects in revenues: p > g − r. As long as this continues, the United States will not outgrow its debt.

Even worse, despite a recent decline in real interest rates, interest rates may not remain below the growth rate in the long run. The real interest rate depends on a variety of factors, including productivity growth, demographics, risk aversion, preferences for saving and investment, and the distribution of wealth and income.5 Several of these factors may evolve unpredictably. But even real-time estimates of the equilibrium real interest rate have large uncertainties: one study estimates a range between 0 percent to the pre-crisis level of 2 percent.6 Estimates from the past 10 years, in particular, may understate the real interest rate because of low trend growth after the recession.7 One should therefore not assume that the low interest rates of the past 20 years will continue.

As the debt burden rises, it may also push interest rates above the GDP growth rate.8 Government borrowing generally raises interest rates because it increases the demand for loanable funds and can cause investors to expect a higher risk of default, thus raising the premiums on government debt. The CBO estimates that an increase in the deficit equal to 1 percent of GDP would raise the interest rate on new government debt by 2 to 3 basis points (hundredths of a percent) when the economy is operating at potential.9 Calls to perpetually increase the debt must therefore recognize that a rising debt burden could cause interest rates to rise above the growth rate. If interest rates exceed growth rates, the debt-to-GDP ratio will rise even if the government runs no primary deficit.

The U.S. Fiscal Outlook before COVID-19

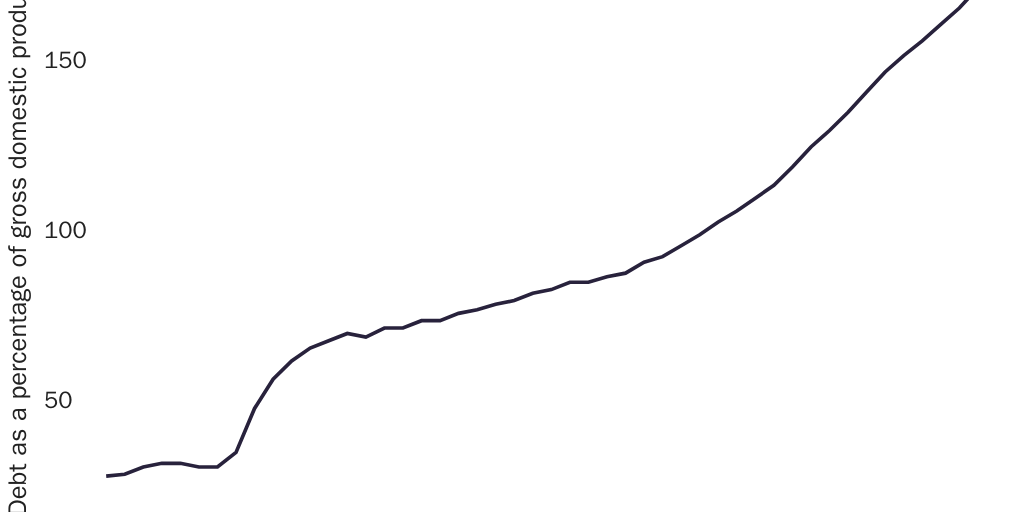

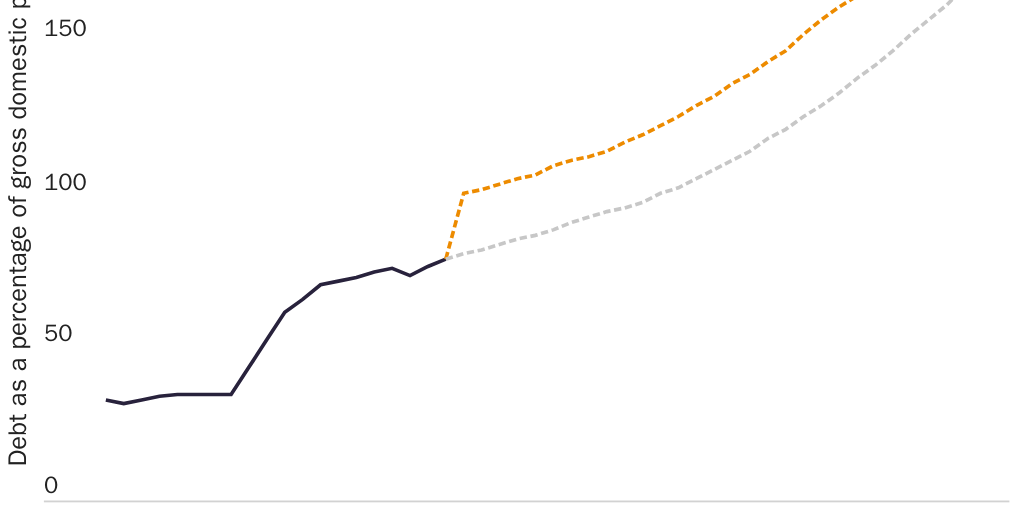

Figure 1 presents the CBO’s January 2020 projection of the debt-to-GDP ratio for the United States over the next 30 years.10 According to these forecasts, the U.S. debt-to-GDP ratio was on track to increase indefinitely. As debt grows relative to GDP, the probability of repayment declines, prompting lenders to charge higher interest rates. This further increases the debt burden and eventually spurs a default, leading to a fiscal crisis and a decline in consumption.

These projections rely on assumptions about economic fundamentals, and they assume current tax and expenditure policies remain in place. To address the role of the key economic assumptions and evaluate the effect of possible policy responses to the unsustainable debt path, I have created a pre-pandemic baseline projection using CBO estimates and assumptions but utilizing individual spending trends for Medicare, Medicaid, Social Security, and discretionary spending through 2050.11 This allows projection of the debt burden under different assumptions for individual spending categories. This “disaggregated” approach produces virtually identical conclusions to the baseline CBO projections, given their assumptions about fundamentals.

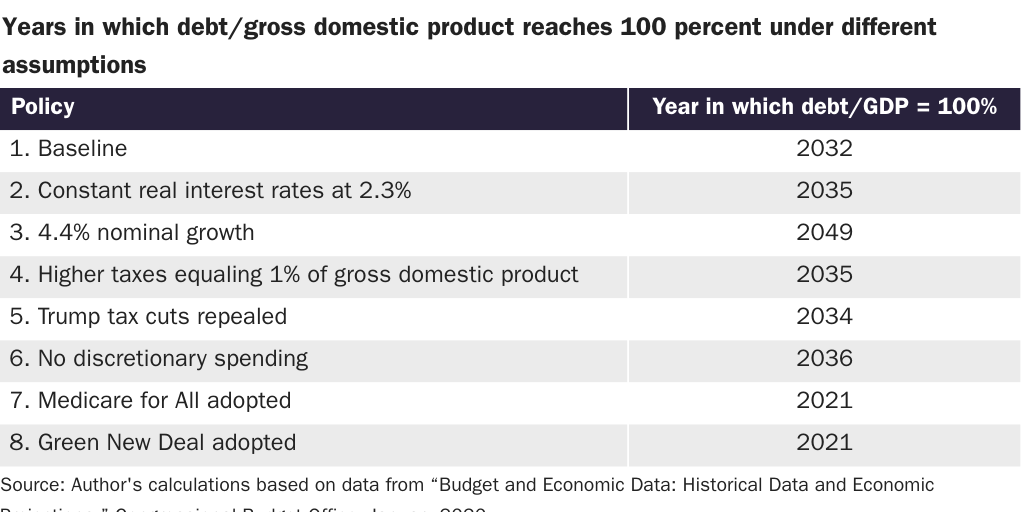

One assumption underlying the CBO projections is that interest rates will increase over time as debt rises relative to GDP. This assumption might seem strong, since debt relative to GDP has increased considerably in past decades, yet interest rates have fallen. But even if interest rates remained at pre-pandemic levels indefinitely, my projections show that high primary deficits would still cause the debt burden to increase substantially. In fact, under constant real interest rates, the debt-to-GDP ratio would reach 100 percent of GDP in 2035—only three years later than in the CBO’s baseline projection (see Table 1, line 2).

Moderately higher GDP growth also fails to prevent the debt-to-GDP ratio from increasing indefinitely. The CBO projects that nominal GDP growth will average about 3.9 percent from 2019 to 2049, which implies a real GDP growth rate of about 1.9 percent. This is below long-term historical trends (real GDP growth has averaged 2.5 percent since 1990) but is consistent with slowing real growth over the past 20 years. Even if nominal GDP instead grew at 4.4 percent indefinitely (which is faster than the CBO’s baseline assumption of 3.9 percent nominal growth per year), tax revenue increased proportionally, and the dollar value of federal deficits were unchanged from my baseline scenario, the debt-to-GDP ratio would still rise indefinitely, reaching 100 percent in 2049 (see Table 1, line 3).

The CBO projections and my robustness checks thus imply that under pre-pandemic policy, the U.S. debt-to-GDP ratio would grow indefinitely. Thus, even before the pandemic, avoiding eventual fiscal default required substantial policy changes.

One policy to reduce the debt burden is higher taxes. My projections show, however, that even substantial increases in federal revenue relative to GDP would not lower the debt burden meaningfully, since higher revenue decreases the level of debt but not its growth rate. For example, if long-term revenue exceeds the baseline by 1 percent of GDP (or about 6 percent of annual federal revenue), the debt-to-GDP ratio will reach 100 percent in 2035, only three years later than in my baseline estimate (Table 1, line 4). This assumes no disincentive effects of higher taxes on GDP growth. Repeated tax hikes that initially decrease the growth of debt-to-GDP would likely reduce growth at some point and therefore fail to raise further revenue.12 Meanwhile, repealing the Trump administration’s 2017 tax cuts in 2021 would raise revenue slightly, but the debt-to-GDP ratio would still hit 100 percent by 2034 (Table 1, line 5).13

An alternative policy to reduce the debt burden is lower discretionary spending. The CBO’s projections from January 2020, however, already assumed that discretionary spending would decline as a share of GDP and that mandatory outlays for programs other than Medicare, Medicaid, and Social Security would remain stable as a share of GDP. Yet even before COVID-19 and the resulting economic crisis, further cuts in discretionary spending were politically unlikely. Regardless, eliminating all spending other than Medicare, Medicaid, and Social Security would only delay the date at which the debt-to-GDP ratio reaches 100 percent by four years (Table 1, line 6).

Other policy proposals to slow the debt burden’s growth include those that might boost economic growth, such as reducing distortionary taxes or increasing incentives for investment. These policy changes are plausibly desirable on microeconomic grounds. As previously discussed, however, even moderately higher economic growth would not prevent the debt burden from growing indefinitely.14

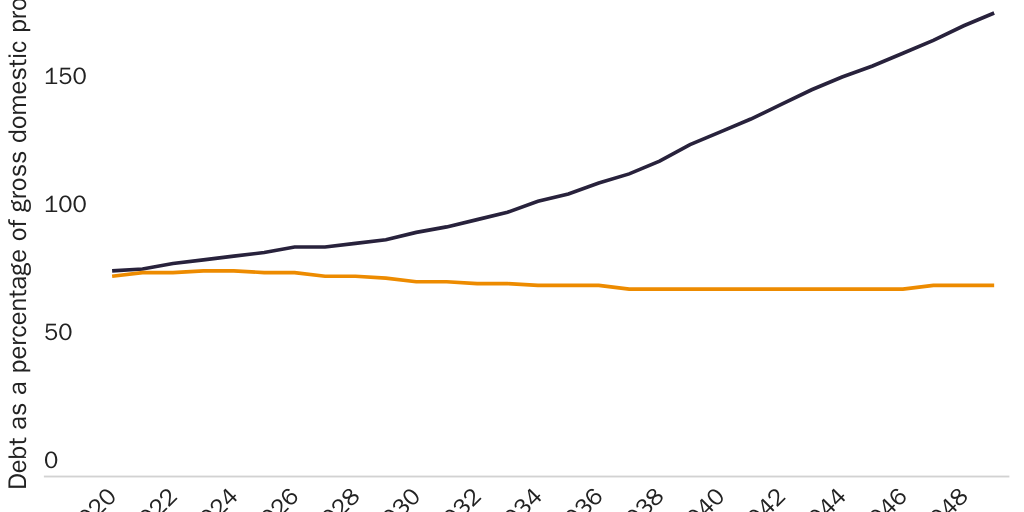

If the United States cannot slow the debt buildup materially via higher taxes, lower discretionary spending, or faster economic growth, that leaves slowing the growth of Medicare, Medicaid, and Social Security as the principal option.15 These are the programs that have historically grown faster than GDP and that the CBO projects will continue to do so. If spending on these programs grows no faster than GDP beginning in 2020, and discretionary spending remains constant as a share of GDP, the debt-to-GDP ratio peaks at 80 percent in 2024. After that, rising revenue and low interest rates cause debt to decrease relative to GDP (i.e., p + r < g). If slower growth for Medicare, Medicaid, and Social Security phases in gradually, rather than in 2020, the long-term debt burden still stabilizes but peaks at a higher level than under earlier cuts.

This assumes that cutting spending on Medicare, Medicaid, and Social Security will reduce deficits by more than it reduces GDP because existing evidence suggests that cuts in government spending do not lower GDP significantly in the short run and have a significant positive effect in the long run.16 Furthermore, Medicare and Social Security mainly cover retirees, who contribute little to national output, and as much as 30 percent of health care spending in the United States is wasted on administrative costs, fraud, or other inefficiencies and so does not directly fund health care services.17 Many experimental and quasi-experimental studies find no effect of federal spending on health outcomes that might translate into higher economic growth, although some have found moderate benefits for specific populations that are not necessarily generalizable.18

Figure 2 displays projections for the debt-to-GDP ratio under my baseline, pre-COVID scenario and under the assumption that spending on Medicare, Medicaid, and Social Security stays constant as a share of GDP beginning in 2020. The most important finding is that if these programs are reduced so that they only grow at the same rate as GDP, the long-term debt burden stabilizes.

Current Policy Proposals

Reducing the U.S. debt to a more sustainable level ought to be a bipartisan priority, but neither party has given the issue sufficient attention in recent years. Democratic presidential candidates advocate for trillions of dollars in increased spending through new programs such as a universal basic income and free college tuition.19 In July 2019, the Trump administration backed a budget deal that suspended the debt limit for two years, adding $1.7 trillion to deficits over the next 10 years on top of the $1.9 trillion increase from the 2017 tax cuts.20 Even prominent economists have downplayed the debt burden, arguing that because of historically low interest rates, the federal government should increase spending on infrastructure, education, health, and other allegedly productive investments.21

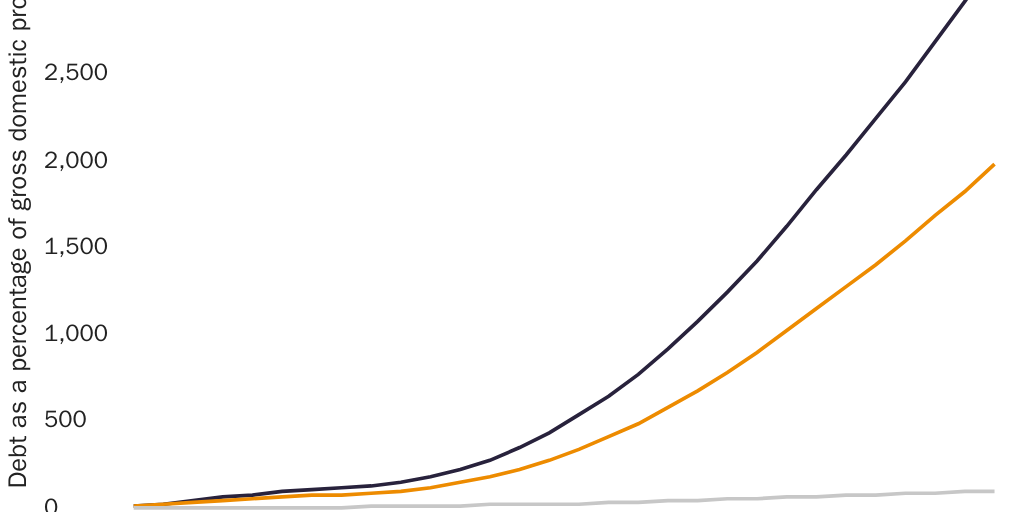

Alarmingly, several popular policy proposals would substantially increase the debt burden’s growth rate. The Urban Institute, a center-left think tank, estimates that Medicare for All would increase federal spending by $32 trillion over the next decade.22 The American Action Forum, a center-right think tank, estimates that the Green New Deal would cost $52–$93 trillion over the next 10 years, although this estimate is imprecise.23 Figure 3 displays my projections for the debt-to-GDP ratio under these policies compared to the baseline, pre-pandemic scenario. Under Medicare for All, the debt-to-GDP ratio would reach 100 percent in 2021 and 150 percent in 2026; under the Green New Deal, it would reach 100 percent in 2021 and 150 percent in 2024. Making matters even worse, both of these programs would accelerate the accumulation of debt indefinitely as a result of compounding interest burdens.

Most proposals that do address the debt burden focus on cutting discretionary spending, raising taxes, or adopting policies that might stimulate the economy’s growth rate.24 Generally absent from the discussion is any mention of cutting the three largest entitlement programs: Medicare, Medicaid, and Social Security. Neither party advocates substantial reductions in entitlement spending. The Social Security 2100 Act that was introduced in the Senate in January 2019 would maintain the Social Security Trust Fund’s solvency, but increase both taxes and spending. In July 2019, the House of Representatives voted nearly unanimously to repeal the “Cadillac tax” on expensive health insurance plans; the CBO projects that repeal would increase the deficit by nearly $200 billion over the next decade.

Determining the best way for the United States to slow entitlement growth is outside the scope of this paper, but a successful strategy would likely involve raising the eligibility age for Social Security and Medicare. This would reduce expenditure directly, and by reducing the demand for health care, it should moderate the growth of health care prices. Lowering the debt burden would also likely involve raising deductibles and copays in Medicare and Medicaid, which directly reduces spending and increases consumers’ sensitivity to the price of health care.25 Alternatively, the federal government could transfer all such programs to state governments, allowing each state to choose its own generosity level. This would likely restrain spending, since many states may want to avoid overly generous programs that attract residents from other states. But it would almost certainly not mean the end of public health and pension programs for retirees, since states routinely offer more generous programs than required by any state mandate. For example, most states expanded Medicaid under the Affordable Care Act even though they were not required to do so.

Overall, the CBO projections and my variation of those projections suggest that under pre-pandemic policies, the U.S. debt-to-GDP ratio would grow indefinitely absent major reductions in the growth of entitlements.

COVID-19’s Effect on Fiscal Imbalance

Congress enacted numerous relief measures and stimulus interventions to mitigate the economic and public health effects of COVID-19, including the CARES Act, the Families First Act, and the Paycheck Protection Program (PPP) and Health Care Enhancement Act. According to the Committee for a Responsible Federal Budget, as of August 2020 the federal government had already spent well over $2.7 trillion in direct COVID-19 spending.26 Democratic and Republican lawmakers have already proposed trillions more in additional relief spending, and the recession has reduced tax revenues substantially.

I therefore update my projections to account for pandemic-related changes in spending and economic conditions, according to the CBO’s updated outlook for the next 10 years. As of July 2020, the CBO projects that GDP will fall by approximately 5.1 percent in 2020, followed by several years of slightly higher-than-average economic growth. Tax revenues as a share of GDP will also fall in 2020 because of higher unemployment, furloughs, and wage cuts, all of which lead to lower overall income levels. The updated projections also include an additional $2.7 trillion in extra discretionary spending (relative to the pre-pandemic baseline) from federal stimulus measures.

As Figure 4 illustrates, the federal debt-to-GDP ratio has already skyrocketed past the symbolic 100 percent level because of recent COVID-19 relief spending and the dramatic contraction of the U.S. economy during the first half of 2020. This marks the largest year-over-year increase in federal debt on record, and the highest U.S. debt-to-GDP ratio since World War II. Absent any new measures to curtail spending, the debt-to-GDP level will continue to increase at an accelerating rate, hitting 150 percent by 2039. These long-term projections are highly consistent with other studies that model the pandemic’s effect on U.S. fiscal health.27

Perhaps surprisingly, however, COVID-19 has not dramatically altered the long-term direction of fiscal imbalance. The federal debt level is poised to soar in 2020 and 2021, but these effects will be relatively short-lived—assuming, of course, that the economy begins to recover from COVID-19 within the next year. Over the long run, FI will continue accelerating at roughly the same rate as before, for several reasons. First, the government’s recent COVID-19 relief spending still represents a small fraction of total existing federal debt. Second, the CBO projects that the federal government will benefit from a prolonged period of lower interest rates (around 1 percent through 2025), which slows the increase in total debt. Finally, the underlying drivers of the federal deficit—Medicare, Medicaid, and Social Security—remain essentially unchanged. In fact, COVID-19 may slightly reduce Social Security and Medicare outlays because of the virus’s tragic and disproportionate effect on senior citizens. Roughly 80 percent of COVID-19 deaths so far have been among individuals aged 65 and older.28 With fewer elderly individuals alive, Medicare and Social Security spending may fall by as much as 0.5 percent until a vaccine becomes widely administered. Preliminary data from spring 2020 also suggest that mortality rates from other causes have also increased during the pandemic, perhaps because many people are unwilling or unable to seek treatment for other medical ailments. This trend may also have non-trivial effects on Social Security finances.29 On the other hand, the pandemic may accelerate early retirement trends or depress labor force participation among older Americans, which could worsen the fiscal shortfalls for these entitlement programs.30

These conclusions have two implications. On one hand, they suggest that the effect on the debt burden is not a compelling reason to oppose federal stimulus or COVID-19 relief programs. Those measures may be misguided for other reasons, but assuming they are temporary, they do not substantially change the long-term path of the federal debt burden. In fact, they may help prevent greater declines in tax revenue by stabilizing the economy and boosting growth over the next several years. On the other hand, the sudden increase in America’s debt burden is a stark wake-up call that we can no longer ignore the country’s fiscal imbalance. The U.S. fiscal path is unsustainable, and slowing entitlement growth is the only way to change that path substantially.

Conclusion

The current fiscal path is unsustainable. The primary drivers of America’s growing debt burden are Medicare and Medicaid, which are projected to grow faster than GDP indefinitely. Social Security is projected to grow faster than GDP for at least the next 20 years. Thus, stabilizing the debt-to-GDP ratio requires lowering the growth rate of spending on these programs. The recent wave of COVID-19 spending has pushed the debt-to-GDP level past 100 percent for the first time in multiple generations. In the long run, however, the pandemic will not dramatically alter the debt burden’s path. Rather than focusing on cutting spending for COVID-19 relief, Congress should focus on curbing the growth in mandatory entitlement spending.

The debt path implied by current policies is unsustainable. In particular, an ever-growing debt burden is virtually inevitable even if interest rates remain low or the growth rate increases, and higher taxes or reductions in discretionary spending are unlikely to prevent the debt-to-GDP ratio from rising indefinitely. Only slowing the growth of entitlement spending—especially on Medicare—can meaningfully slow the projected path of the debt-to-GDP ratio.

The specifics of shrinking these programs aside, the key message is that policymakers must do something to slow the growing debt burden or else face a major fiscal meltdown. Cutting entitlement spending sooner rather than later prevents the problem from getting worse. Further, adopting new long-term spending programs—especially those that are likely to expand over time—would be irresponsible, even if well-intentioned. Proposals such as Medicare for All and the Green New Deal would only make the looming fiscal crisis worse.

For an earlier analysis of the issues presented in this paper, see Jeffrey Miron, “U.S. Fiscal Imbalance over Time: This Time Is Different,” Cato Institute White Paper, January 26, 2016.

Citation

Miron, Jeffrey. “COVID-19 and the U.S. Fiscal Imbalance,” Policy Analysis no. 905, Cato Institute, Washington, DC, December 8, 2020. https://doi.org/10.36009/PA.905.

About the Author

This work is licensed under a Creative Commons Attribution-NonCommercial-ShareAlike 4.0 International License.