Over the last 60 years, the federal government has showered the domestic steel industry with every conceivable form of protection from import competition, from tariffs, quotas, and trade remedies to voluntary export restraints, Buy American procurement preferences, and restrictions on trade and foreign investment under the guise of national security. These policies have further entrenched the steel industry as a protected constituency that wields significant influence over trade policy, which in turn has led to more—and increasingly complex—schemes for further shielding the industry from imports.

As steel is an essential input for many products, from vehicles and appliances to construction materials and machinery, the unholy alliance between Washington and Big Steel has come at a high cost for steel-using firms in the United States, and therefore for Americans who consume final goods made with steel and who fund public infrastructure projects through their taxpayer dollars. Moreover, the federal government’s endeavors to protect the domestic steel industry have sowed political dysfunction both at home and abroad, with industry advocates cycling through the proverbial revolving door of Washington politics, and officials’ attempts to cater to Big Steel undermining international trade negotiations, relationships with long-standing trading partners, and even the functioning of the World Trade Organization.

And yet for all the protection that the government has conferred to the industry and all its costs, the steel industry’s prospects show remarkably little improvement: Major producers are struggling to innovate and compete, output and capacity utilization have stagnated, employment continues its long-term decline, and prices are among the highest in the world. Altogether, the history of steel protectionism in the United States is yet another case study in the failures of protectionism to reinvigorate declining industries and the consequences of pursuing these policies.

Introduction

For more than half a century, the steel industry has been one of the most protected sectors of the American economy, benefiting from an array of trade restrictions including quotas, tariffs, and aggressive trade remedies. Despite claims that US trade policy has embraced unfettered free trade, the steel industry tells a very different story—one of persistent and escalating protectionism that continues to dictate much of trade policy.

In the first half of the 20th century, the steel and iron industries flourished in the Midwest, particularly in Ohio, as well as in Pennsylvania. These states possessed abundant deposits of iron ore, coal, and limestone, the key components of steelmaking.1 The Great Lakes and the extensive rivers provided a critical transportation network for moving raw materials and finished products relatively efficiently. In the late 19th and early 20th century, massive steel mills popped up in cities such as Pittsburgh, Youngstown, and Cleveland to benefit from these advantages.

The roots of modern steel protectionism trace back to the 1960s, when technological progress and growing competition from rebuilt Japanese and German producers sparked calls for import restrictions. Yet the legacy companies’ troubles stem mostly from technological change and domestic competition, particularly the rise of mini mills that use electric arc furnaces to recycle scrap steel.

This extensive protection comes at a significant cost to the American economy. Steel prices in the United States are consistently higher than the world price. These inflated prices raise costs for countless downstream manufacturers who use steel as an input, ultimately making American products less competitive globally. And even if protectionism increases domestic steel production, there are legitimate questions about whether the extra capacity is needed and worth the cost. Likewise, it is unlikely that employment in domestic steel production will increase in meaningful ways.

American steelmakers complain about unfair competition from foreign subsidized steelmakers, and these complaints have some merit. Trade officials should address this in multilateral forums. But these foreign supports do not justify the widespread protections given to steel firms or the harm those protections inflict on consumers. This paper examines the evolution of steel protectionism from the 1960s to the present day, analyzing its economic impacts and questioning whether such extensive protection serves the national interest. As policymakers grapple with promoting domestic manufacturing while maintaining international competitiveness, the experience of the steel industry offers important lessons about the true costs and consequences of sustained industrial protection.

The Steel Industry Today

Today the domestic steel industry continues to struggle. Steel production has increased over the past 10 years, yet the size of the increase pales in comparison to the magnitude of the trade barriers that have been imposed during that time span. Meanwhile, capacity utilization has not seen sustained improvement, and employment has continued its long-term decline. Output is concentrated in a handful of producers, and consumers face higher prices than anywhere else in the world.

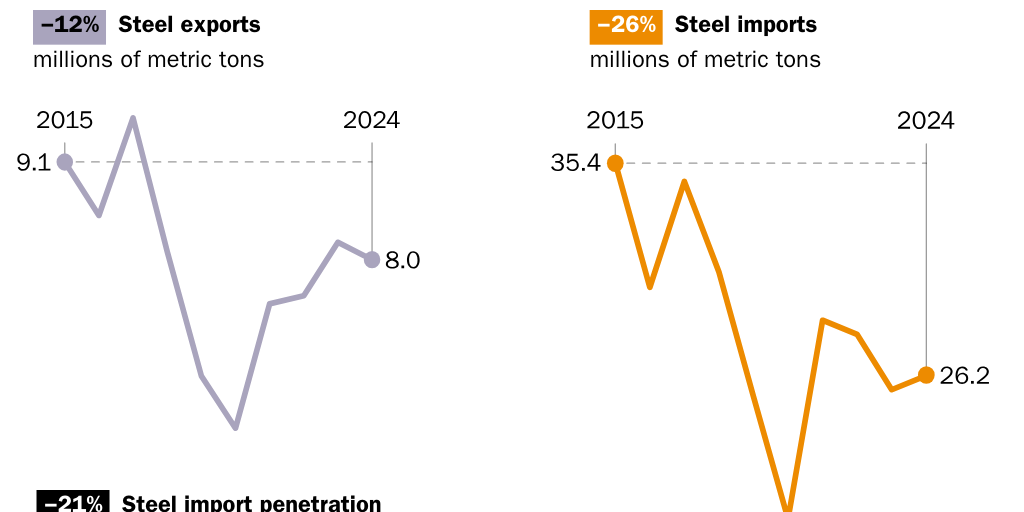

In 2024, domestic steel production totaled around 79.9 million metric tons (MMT). Total US steel consumption was about 98 MMT. Exports of steel totaled a little more than 8 MMT while imports totaled 26.2 MMT.2 The top domestic producers of steel in 2024 were Nucor (18.2 MMT); U.S. Steel (12.3 MMT); Cleveland-Cliffs (10.6 MMT); Steel Dynamics (10 MMT); and Commercial Metals Company (4 MMT). These five companies represented nearly 70 percent of all steel production in 2024. According to the American Iron and Steel Institute, the construction and automotive industries were the leading users of domestic steel in 2023.3

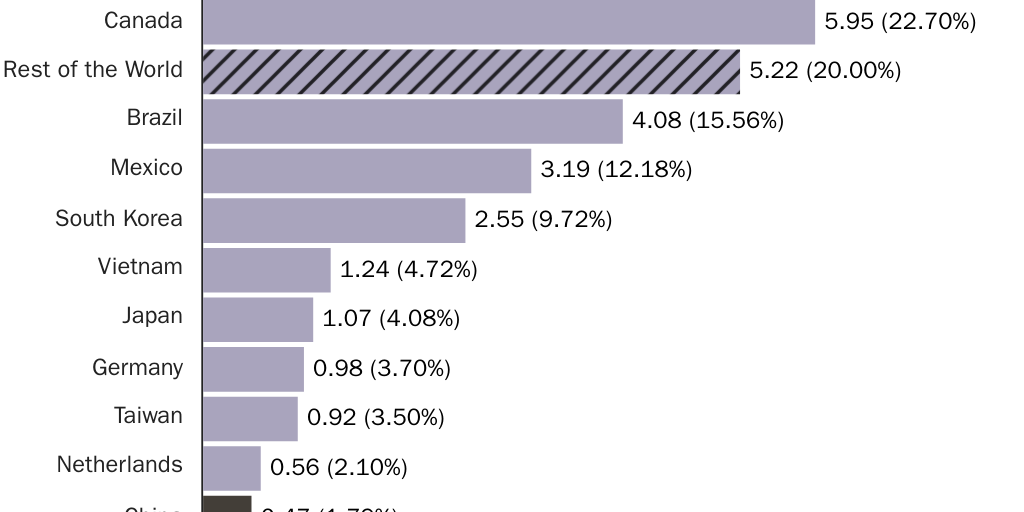

As mentioned, the United States imported 26.2 million metric tons of steel products, which was a slight increase from 2023.4 Between 2017 and 2022, the volume of steel imports fell by about 26 percent.5 As Figure 1 shows, the top sources of the 26.2 MMT of steel imported in 2024 include close allies, including Canada (5.95 MMT, or 22.7 percent of imports); Brazil (4.08 MMT, or 15.56 percent); Mexico (3.19 MMT, or 12.18 percent); South Korea (2.55 MMT, or 9.72 percent); Vietnam (1.24 MMT, or 4.72 percent); and Japan (1.07 MMT, or 4.08 percent).6 Of the top 10 supplier countries in 2024, only China (0.47 MMT, or 1.79 percent) could be considered an adversary of the United States. The top 10 countries provided more than 80 percent of all steel imports in 2024.7 In total, 79 countries provided steel to the United States in 2024.8

Between 2015 and 2024, steel imports declined by 26 percent—from 35.4 MMT to 26.2 MMT—and exports declined by nearly 12 percent. The steel import penetration ratio in 2024—steel imports as a percentage of total domestic steel consumption—was 26.73 percent, down from 33.69 percent in 2015.9 These declines coincide with the Trump administration’s national security tariffs on steel imports (discussed in more detail later) and the global economic slowdown brought on by the COVID-19 pandemic.

Over the same period, domestic steel production increased slightly, from 78.8 MMT to 79.9 MMT, or about 1.4 percent, despite aggressive protective tariffs over the period. Overall, “apparent consumption” (a measure of steel demand) declined by about 7 percent over the period, from 105.2 MMT to 98.1 MMT (Figure 2).10 At the same time, capacity utilization in the domestic steel industry was slightly lower in 2024 (70.5 percent) than in 2015 (71.9 percent), despite increasing in some years in between, and employment was also lower in 2024 (85,700 workers) than in 2015 (89,200 workers).11

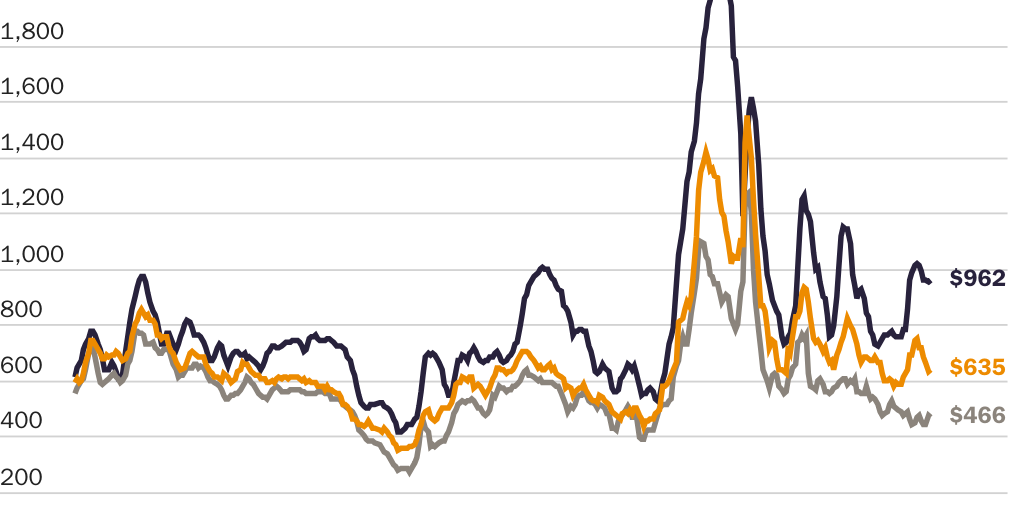

Today, steel prices in the United States are generally significantly higher than in most of the rest of the world. As Figure 3 shows, the average price of a metric ton of hot-rolled band steel was $962 in the United States at the end of July 2025, compared with $635 in Western Europe and $466 on the world market. Those are differences of $327 and $496, respectively, meaning the steel was about 51 and 106 percent more expensive in the US.12 This figure is not an anomaly; steel prices in the United States have been persistently higher than world prices.13 This dynamic unnecessarily inflates input prices for American producers using steel and makes their products less competitive globally.

Beginning in the late 1960s and continuing today, the domestic steel industry has been able to secure substantial protection from import competition in the form of quotas, foreign export restraints, antidumping and countervailing duties, safeguards, and national security tariffs. This history is summarized in Table 1 and discussed below.

History of Steel Protectionism in America

1960 to 2000: Creeping Protectionism

Emerging victorious from World War II, the United States had an outsized role in the global economy, including in the steel industry. In 1950, for example, American firms accounted for 53 percent of the world’s steel production.14 Yet that market share was soon to erode as other economies were redeveloping from the wreckage of the war.

During the summer of 1959, the United Steel Workers (USW) went on strike for more than 100 days. Over that period, steel-consuming manufacturers turned to imported steel to fill the void and, for the first time in the 20th century, steel imports exceeded steel exports. As Dartmouth economist Douglas Irwin notes, “The lesson that management took from the costly shutdown was that labor peace had to be purchased with generous wage concessions in order to keep factories running and prevent consumers from buying foreign steel.” Those higher labor costs were untethered from productivity increases.15 Whereas in previous eras steel producers could pass along the inflated costs to steel consumers in the absence of serious foreign competition, that was no longer the case.

Japan and Germany’s steel industries expanded throughout the 1950s as their economies recovered from World War II.16 As will be discussed in more detail later, foreign steel producers, often aided by overly generous subsidies, were also quicker to embrace new technologies such as basic oxygen furnaces that produced steel more efficiently than the open hearth furnaces largely used by American steel producers, and thus increased their output.17

Between 1960 and 1970, the share of imports as a percentage of domestic steel consumption rose from about 5 percent to 15 percent. In response to growing foreign competition, steelworkers, management, and policymakers from steel-producing areas began to clamor for protection. In 1967, legislation was proposed to cap steel imports at slightly under 10 percent of the domestic market. In response to growing protectionism in Congress, Germany and Japan offered to voluntarily restrict their exports of steel to 5.8 million tons each, down from 7.5 million tons from Japan and 7.3 million tons from the European Economic Community (the precursor to the European Union), with a 5 percent increase each year over the course of the initial three-year agreement (1969–1971).

The Johnson administration welcomed this agreement as an alternative to legislative efforts from Congress. The voluntary restraint agreement (VRAs) would be renewed for another three years, from 1971–1974. Imported steel volumes fell over this period but the values did not because “foreign producers upgraded the quality of their exports to higher value stainless and alloy steel products.”18 Research by the Brookings Institution found that the trade restrictions raised the price of steel between 1.2 and 3.5 percent in 1971 and 1972.19 The export restrictions, which lapsed in 1974, were not renewed.

The US economy began to slow down in the mid-1970s. At the same time, foreign subsidies to steel producers continued apace, and capacity grew. This led to a glut of steel on the world market. Meanwhile, domestic producers, saddled with higher wage costs, failed to improve their productivity. Amid slumping demand as the economy slowed, steel companies, steelworkers, and policymakers began exploring ways to curb steel imports. Japan once again agreed to export restrictions, but the European Economic Community did not. In response, the domestic steel industry began filing numerous antidumping petitions against European producers. The Carter administration, concerned about the proliferation of antidumping cases creating “insurmountable barriers to imports,” negotiated a trigger-price mechanism that would allow the government to “monitor prices and accelerate an antidumping investigation if imports arrived at prices below the specified triggers.” The agreement was reached in early 1978, and it used Japanese steel production costs and other factors as the reference price. Given that Japanese steel production costs were generally below European steel production costs, European steel still made its way into the US in large quantities. In 1980, after another antidumping case was filed against European producers, the Carter administration suspended the price floors and then reinstated the trigger-price mechanism at a 12 percent higher price level in exchange for withdrawing the antidumping petition.20

The US economy was still reeling in the early 1980s. Major domestic producers laid off large numbers of steelworkers. Between 1979 and 1982, imports as a share of domestic steel consumption increased from about 15 percent to 22 percent. To combat this, in 1982, major domestic steel companies filed 155 antidumping and countervailing duty petitions targeting 41 companies from 11 different countries, most of which were European. As Irwin notes, “The ITC ruled affirmatively in about half of these cases, but the prospect of long-lasting and severe tariff penalties on European producers, as well as highly varied antidumping duties being imposed across a range of countries and producers, was unattractive to all parties.” Seeking to head this off, the Reagan administration negotiated a new VRA with the European Economic Community, capping European exports to 5.5 percent across 11 product categories, and the domestic firms dropped their petitions. Japan continued to restrict its exports as well. By 1985, steel restrictions were reached with 15 countries, covering a number of products, which represented 80 percent of all steel imports.21

A 1987 study by the Brookings Institution examined US steel protectionism (along with auto protectionism) from the Johnson administration to the Reagan administration and found the policies to be counterproductive. While they did help curb imports, the policies were pyrrhic victories: They discouraged product quality improvements and led to overinvestment and overinflated labor contracts that “simply postpone[d] part of the necessary adjustment to the loss of competitiveness.”22

As the VRAs were set to expire in 1989, steel companies and the USW again demanded that they be extended for another five years. Caught between steel producers and steel-consuming industries, the George H. W. Bush (Bush 41) administration supported a two and one-half year extension of the VRAs and argued that the concurrent General Agreement on Tariffs and Trade (GATT) negotiations offered the best path forward for targeting subsidies and excess capacity. After those VRAs lapsed, the domestic steel industry again turned to antidumping and countervailing duty cases, but most were dismissed by the USITC.23

Although the Clinton administration levied minor duties on certain steel products,24 it rejected industry requests to impose sweeping import restrictions.25 Moreover, in the Uruguay Round negotiations, which converted the GATT to the current World Trade Organization (WTO) in 1995, voluntary export restraints were prohibited.

Were Imports Truly to Blame for the US Steel Industry’s Struggles?

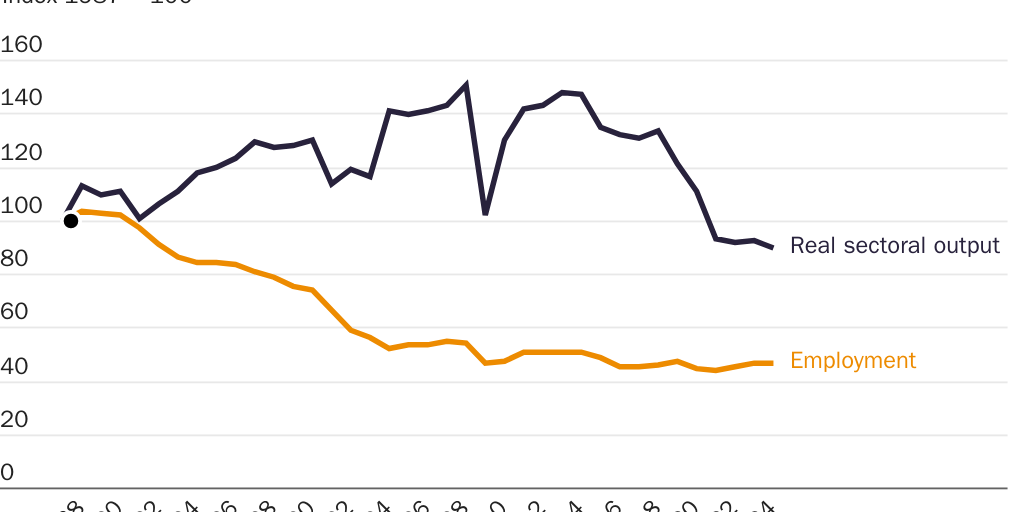

The above discussion only covers the international angle of the steel market between the 1950s and 2000s. Over roughly the same period, 1962–2005, it is estimated that the domestic steel industry lost about 400,000 employees, or about 75 percent of its workforce. Protectionists argue this was the result of import competition, some of which was subsidized by foreign governments. Yet productivity growth, driven by technological breakthroughs, is the primary driver of job loss in the domestic steel industry, particularly the rise of the mini mill. Mini mills are small steel plants that utilize electric arc furnaces to recycle scrap steel. Mini mills are cheaper to operate and can adapt to changing market demands more quickly than larger, integrated mills. Over this period, total factor productivity in the steel industry grew by 38 percent and output per worker grew by five times—making steel one of the fastest-growing industries during that period. As economists Allan Collard-Wexler and Jan de Loecker note, “The period of impressive productivity growth—28 percent compared to the median of 3 percent—occurred while the sector contracted by 35 percent. The starkest difference is the drop in employment of 80 percent compared to a decline of 5 percent for the average sector.”26

Between 1972 and 2002, total imports of steel increased by 4.1 percent, whereas nonsteel manufactured imports increased by 66 percent. The import penetration ratio in the steel industry increased by 8 percent compared to 15 percent for rest of the manufacturing industry. As a result of the increase in productivity in the steel industry, “it is not the case that the exceptional productivity growth in steel was contemporaneous with an exceptional increase in import competition for steel producers.”27

Between 1960 and 2000, foreign steel producers—particularly those from post-war Japan and Europe—did make inroads into the US market. But the evidence shows that productivity-enhancing technological breakthroughs—particularly mini mills—were the primary driver of job losses in the domestic steel industry. Rather than blaming imports or globalization for steel’s transformation, the data suggest that domestic technological innovation fundamentally reshaped the industry’s labor needs and production capabilities, marking a significant shift in American steel production (see Figure 4).28

From 2000 to Today: Safeguards, Strengthened Buy American Mandates, and National Security Protectionism

Since the turn of the century, both Republican and Democratic policymakers have imposed increasingly costly restrictions on steel imports. Such restrictions also reflect an expansion and abuse of discretionary authorities delegated to the executive branch to regulate and influence international trade and investment.

Bush Steel Tariffs

In the aftermath of the Asian financial crisis of 1997–1998, steel prices fell substantially. As a result, a number of antidumping cases were filed in the United States.29 Between 1997 and 2001, more than 30 steel-producing and steel-processing firms filed for bankruptcy.30 On the presidential campaign trail in 2000, George W. Bush (Bush 43) promised to help struggling steelworkers.31 Once he was in office, domestic steel producers began pressuring the Bush administration to make good on campaign promises.

In June 2001, the Bush administration initiated a Section 201 investigation into 33 categories of steel imports.32 Administered by the US International Trade Commission (USITC), Section 201 of the Trade Act of 1974 provides the president with a tool to restrict imports when the USITC finds that a domestic industry is seriously injured—or threatened with serious injury—because of increased imports. Under such circumstances, a president can impose temporary trade restrictions to alleviate the injury or threat of injury.33

In October 2001, the USITC announced that increased imports of about half the surveyed steel categories were injuring or threatening to injure domestic producers.34 Shortly thereafter, in March 2002, the Bush administration announced it would impose temporary tariffs ranging from 8 percent to 30 percent on steel plate, hot-rolled sheet, cold-rolled sheet, coated sheet, tin mill products, hot-rolled bar, cold-finished bar, rebar, certain welded tubular products, carbon and alloy fittings and flanges, stainless steel bar, stainless steel rod, and stainless steel wire, along with a tariff rate quota on slab.35 The tariffs were initially imposed for a three-year period with a year step-down, and then were to be gradually phased out by March 2005. Canada, Mexico, and other countries with whom the United States had preferential free trade agreements—as well as several developing countries—were exempt from the tariffs.36 Within about six months of the tariffs’ implementation, the average price of hot- and cold-rolled steel had increased about 25 percent.37 By September 2003, steel prices were 10–20 percent higher than the period immediately preceding the tariffs.38

In response to the tariffs, the European Union (EU) and other trading partners challenged the measures at the WTO. In July 2003, a WTO panel ruled that the Bush administration’s steel safeguards were inconsistent with the United States’ WTO obligations, and the Appellate Body concurred with the panel’s ruling in November 2003.39 Following the adverse rulings, the EU announced it would retaliate against American products. In early December 2003, the Bush administration withdrew the tariffs, well short of the three-year period initially proposed.40

Assessing the Effects of the Tariffs

What effects did the tariffs have on the steel industry? Raw steel production edged up slightly between 2001 and 2003.41 Economist Chad Bown found that imports of steel from countries affected by the measures fell by 28 percent in 2002 and 37 percent in 2003, while steel imports from countries not subject to the tariffs increased substantially: 40 percent from free trade agreement partners in 2002 and 28 percent from developing countries over 2002–2003.42 Over the year following the implementation of the tariffs, steel imports actually increased by about 3 percent. As economists Sebastien Jean and Ariell Reshef note, “trade diversion—not import reduction—was the main effect on trade flows.”43 Share prices of domestic steel companies did increase following the USITC’s affirmative determination, and again when the safeguard tariffs were announced; share prices fell in response to the WTO’s ruling.

Because steel is a crucial input to a number of downstream industries, the tariffs caused significant harms to the broader economy as steel prices increased. At the time the tariffs were implemented, workers in steel-consuming industries dwarfed those employed in the steel-making industry by a magnitude of 57:1—12.8 million to 170,000.44 Research from Trade Partnership Worldwide found that the steel tariffs resulted in about 200,000 job losses in 2002, many concentrated in metal manufacturing, machinery and equipment, and transportation equipment and parts manufacturing.45

Even though the tariffs were lifted at the end of 2003, economist Lydia Cox of the University of Wisconsin, Madison, found that the negative effects of the tariffs were highly persistent for US exports, production, and employment. She found that the “tariffs caused declines in exports of between 10 and 50 billion dollars per year between 2002 and 2009—equivalent to around 4 percent of exports.” Over that same seven-year period, Cox found that the tariffs were responsible for about 168,000 fewer jobs per year in steel-using industries, relative to the immediately preceding period. She notes that this is more jobs than the entire steel-producing sector. Meanwhile, manufacturing production shipments declined by about 1 percent over that same period.46

Likewise, research from James Lake and Ding Liu found that the Bush 43 steel tariffs had a substantial short-run effect on steel-consuming downstream employment, with no increase in employment in domestic steel production. Mirroring Cox’s findings, Lake and Liu found the negative effect on downstream employment to be highly persistent, continuing for a full five years after the tariffs were eventually lifted. Indeed, their analysis showed that the reduction in US manufacturing employment caused by the Bush steel tariffs in 2008—years after their termination—was 30–40 percent as large as the displacement caused by increased Chinese import competition (the so-called “China Shock”) that same year. More broadly, they found that the tariffs “can explain about 24 percent of the 2000–2007 decline in US manufacturing share of employment (compared to 40 percent for the China Shock).”47 (Other economists, it should be noted, found that increased Chinese imports caused much smaller, and perhaps even positive, employment effects.)48

In total, the Bush administration’s steel tariffs were a failure. The marginal improvement in the domestic steel industry’s production was substantially outweighed by the persistent downstream costs on steel-consuming industries. Thankfully, policymakers wised up and removed the tariffs, but not before substantial economic damage was inflicted.

Strengthened Buy American Mandates

At various points since 1933, when Congress passed the Buy American Act, policymakers have imposed measures requiring the federal government and federally financed construction projects to prioritize using domestically produced goods, particularly steel and iron. These mandates have become more stringent over time, both by covering more types of infrastructure projects and requiring that a greater share of a steel product’s content be made in the United States. On the last point, whereas the original law defined a US-made steel product as one that had more than 50 percent domestic content, subsequent buy-local mandates and revisions to the Buy American Act have required that nearly all manufacturing processes for a steel product, including the initial melting of iron ore or scrap, take place in the United States. This requirement is commonly referred to as the “melted and poured” standard, and it effectively shuts off many companies in the steel industry that are not involved in the melting stage from the government procurement market, including processors that import semi-finished steel to roll into other products.49

Obama Administration and the American Recovery and Reinvestment Act of 2009

In the early stages of the Obama administration, Congress passed the American Recovery and Reinvestment Act of 2009 (ARRA) in response to the Great Recession. Among other provisions, ARRA appropriated about $85 billion for funding the construction, maintenance, or repair of public buildings or infrastructure.50 For projects using construction materials made predominantly of iron or steel, the act required that the iron or steel be almost entirely manufactured in the United States in order for the project to qualify for ARRA funding.51 These obligations were stricter than those codified in the Buy American Act of 1933. Although ARRA provided for the waiver of its Buy American requirements under limited circumstances, these were also narrower in scope than those provided for in the Buy American Act.52

Several pieces of economic and anecdotal evidence suggest that ARRA’s Buy American provisions imposed significant costs on government agencies—and thus taxpayers—as well as on the economy more broadly. The Peterson Institute’s Gary Clyde Hufbauer and Cathleen Cimino-Isaacs estimated that the steel provision, specifically, added about $5.7 billion to ARRA project costs over a three-year period.53 This estimate, however, is based solely on the higher average price of US steel relative to foreign steel. Accounting for bureaucratic inefficiencies would likely push the total cost of ARRA’s Buy American regime even higher. For instance, in 2010 the Government Accountability Office found that five federal agencies—including the Departments of Commerce, Education, Homeland Security, Housing and Urban Development, and the Environmental Protection Agency—along with two states and one municipality, said that ARRA’s Buy American requirements affected their or their grantees’ ability to select and start some ARRA-funded projects, thus causing delays. Some delays were derived from the complexity and incongruency of agencies’ waiver processes, others resulted from contractors with already established supply chains having to find alternate suppliers and even change the design of their projects to comply with ARRA’s Buy American restrictions.54

These distortions to supply chains induced by ARRA’s Buy American regime, moreover, caused harms to firms and workers supplying goods for government procurement. A Peterson Institute report noted the case of a steel plant near Pittsburgh (owned by a Swiss and Russian conglomerate but employing US workers) that lost its largest client because its coils were made from imported steel slab and thus did not meet ARRA’s Buy American restrictions on steel, as well as that of a Canadian pipe manufacturer with facilities in the United States and Canada whose products also did not meet ARRA’s Buy American restrictions despite having 70 to 90 percent of US content, simply because the pipe was finished in Canada.55

Other ARRA-induced distortions in domestic and foreign markets harmed consumers, firms, and workers. On the domestic side, as the Buy American restrictions limited foreign competition, they contributed to an overconcentration in the domestic market for certain products, for instance, ductile iron pipe fittings, on a handful of US producers, further increasing costs for consumers and taxpayers.56 At the international level, ARRA’s Buy American preferences led to a trade spat with Canada: Despite the substantial and long-standing presence of Canadian firms in US supply chains, including for infrastructure, the provisions largely shut Canadian firms out of ARRA-funded projects, as the United States had no obligations to open subfederal procurement markets to Canada under either the Agreement on Government Procurement Agreement (GPA) or the North America Free Trade Agreement (NAFTA).57 While the matter was resolved in 2010 through a bilateral agreement that opened subfederal procurement markets in both countries to both US and Canadian firms, the Buy American provisions created outrage in Canada and prompted campaigns by some Canadian municipalities to purchase goods from countries that did not discriminate against Canadian products. And, as the Peterson Institute report further notes, it is possible that foreign countries such as Japan and China emulated ARRA’s Buy American requirements with buy local preferences of their own.58

First Trump Administration’s Buy American Executive Orders

Driven by the working class Rust Belt constituency that helped propel him to the presidency, Donald Trump’s protectionist America First trade policy targeted the steel industry as one of its primary beneficiaries. In addition to the Section 232 national security tariffs on imported steel, President Trump signed three Executive Orders aimed at strengthening existing Buy American rules, in large part to encourage greater use of US-made steel in federal procurement:

- Buy American and Hire American (EO 13788, signed April 18, 2017)

- Strengthening Buy-American Preferences for Infrastructure Projects (EO 13858, signed January 31, 2019)

- Maximizing Use of American-Made Goods, Products, and Materials (EO 13881, signed July 15, 2019)

The April 2017 and January 2019 Executive Orders did not enact changes to existing Buy American regulations or create additional legal requirements.59 Moreover, evidence about the effect of these provisions in promoting the use of US-made products in public procurement is mixed, and it is not granular enough to ascertain the effects of the Executive Orders on the procurement of steel products in particular.60

The July 2019 Executive Order, on the other hand, did lead to significant changes to Buy American rules. The Executive Order directed the Federal Acquisition Regulatory Council to consider proposing amendments to existing Buy American regulations, including raising the US content threshold for steel end products from 50 percent to 95 percent, and raising the cost-differential threshold (i.e., the rate at which a foreign product must be cheaper than a domestic product) for the issuance of waivers from 6 to 20 percent for products sold by large US businesses and from 12 to 30 percent for products sold by small US businesses.61 In other words, the Executive Order sought to spur regulatory changes that would require steel to be almost entirely US-made for use in federal procurement and would make it more difficult to obtain waivers based on the difference in cost between cheaper foreign-made steel and more expensive US-made steel. The FAR Council proposed the amendments in September 2020 and finalized them on January 19, 2021, just a day before the inauguration of President Joe Biden.62

Biden Administration and the Infrastructure Investment and Jobs Act of 2021 and Inflation Reduction Act

Much like his predecessor, President Joe Biden sought to enact policies to bolster the US manufacturing industry and support its workers. In addition to taking action via Executive Order—to, among other things, establish a Made in America Office in charge of overseeing potential waivers to Buy American or Buy America requirements and increasing both the domestic content and price preference threshold for US-made manufacturing end products—the administration pushed landmark legislation in Congress to increase spending on infrastructure and support the deployment of clean energy with a preference for US-made products, including steel.

First, the Infrastructure Investment and Jobs Act of 2021 (IIJA), which authorized $1.2 trillion for transportation and infrastructure spending over five years, expanded the coverage of Buy America preferences for infrastructure projects at the state and local levels funded through federal grants and loans. Notably, Buy America preferences (these are different from Buy American, which covers procurements by the federal government only) require that a steel product used in a covered project must be almost entirely manufactured (“from the initial melting stage through the application of coatings”) in the United States. Since their initial inclusion in the Surface Transportation Assistance Act of 1982 and before the enactment of the IIJA, this melted-and-poured standard applied to federal financial assistance programs for transportation and water infrastructure–related projects only; the IIJA’s Build America, Buy America (BABA) provisions extend coverage of these requirements to also include programs funding many other kinds of infrastructure projects, including electrical transmission facilities and systems, utilities, broadband infrastructure, and buildings and real property. Notably, these BABA provisions also apply to programs that are not funded by the IIJA.63

The effects of the IIJA’s steel-related BABA provisions on US steel output and employment, on the one hand, and on project costs and timelines, on the other hand, remain unclear. Most concerns about the far-reaching nature of the provisions center on the expansion of Buy America preferences to other construction materials and manufactured products, whereas steel-related Buy America preferences already existed prior to the IIJA.64 Notably, the US steel industry and organized labor opposed de minimis or minor components waivers (i.e., authorizing use of noncompliant steel products whose value is below a certain threshold) issued by agencies such as the Department of Transportation since the IIJA was enacted.65

But perhaps the most notable expansion of Buy American policies under the Biden administration occurred through the Inflation Reduction Act (IRA), which partly aimed to boost production of clean energy and clean energy technologies in the United States. As James Bacchus explained in a Cato Institute Policy Analysis, the several subsidies provided for in the IRA discriminate against non-US-made products “by conditioning the availability of the subsidies on the use of domestic content in the subsidized production.”66 For instance, for clean energy (i.e., wind, solar, geothermal, and hydropower) facilities, the IRA extends a 10 percent bonus credit for facilities that are constructed using steel made in the United States.67 Furthermore, the IRA’s standard for steel made in the United States is directly taken from the Federal Transit Administration’s Buy America preferences, which stipulate that “all steel and iron manufacturing processes must take place in the United States, except metallurgical processes involving refinement of steel additives.”68 (According to guidance from the Internal Revenue Service, certain steel products are not subject to this domestic-content preference.69) In sum, the IRA extends Buy America rules with respect to steel beyond their typical domain—government procurement—to that of private-sector investments funded with assistance from the federal government.

National Security Tariffs

During the 2016 presidential campaign, Donald Trump made trade policy a central issue. Trump promised to radically overhaul the largely pro-trade policies of each of his Democratic and Republican predecessors, from Franklin Roosevelt to Barack Obama. Shortly after taking office, he began making good on those promises. One of his first official acts as president was to withdraw the United States from the Trans-Pacific Partnership, a Washington-led trade pact with 11 other Pacific Rim countries that was designed to counter China’s growing influence in the region and to set higher standards for international commerce.

In April of 2017, Trump instructed his commerce secretary, Wilbur Ross, to initiate a Section 232 investigation into whether steel70 and aluminum71 imports jeopardize national security. In February 2018, Commerce issued its reports, finding in the affirmative72 despite Trump’s defense secretary, James Mattis, noting in memorandum that the US military only needed 3 percent of total domestic production of both steel and aluminum.73 Shortly thereafter, Trump announced 25 percent tariffs on imports of steel and 10 percent tariffs on aluminum, which were originally applied to all sources.74 The tariffs covered basically all steel products and, as of 2020, covered certain derivative steel products, such as nails. It is worth noting that steel imports predominantly originate in allied countries, not adversarial countries such as Russia or China.

Even the 3 percent figure cited by Secretary Mattis may have been overstated. William Greenwalt, former deputy undersecretary for industrial policy at the Department of Defense, notes that, historically, the Pentagon has purchased less than 1 percent of domestic steel output; the steel the military needs is very high quality and is purchased in small quantities from the Cleveland-Cliffs plant in Pennsylvania.75

The Trump steel tariffs were little more than protectionism for the domestic industry and leverage to extract concessions from trading partners, and not protection for national security. During a television interview, for example, Secretary Ross explained that the tariffs were intended to be motivation for Canada and Mexico to agree to a fair deal in the ongoing negotiations to rewrite the North American Free Trade Agreement.76 The Trump administration eventually granted Mexico and Canada exemptions from the tariffs once it became clear the tariffs were major sticking points in trade negotiations for the US–Mexico–Canada Agreement (USMCA) and had prompted painful retaliation.77 Both countries ultimately agreed to separate bilateral agreements with the United States that provided for establishing mechanisms to prevent bilateral trade in unfairly dumped/subsidized and transshipped steel. (See the “Undermining Long-Standing North American Trade Ties” subsection under the “Steel Protectionism Breeds Political Dysfunction” section below.)

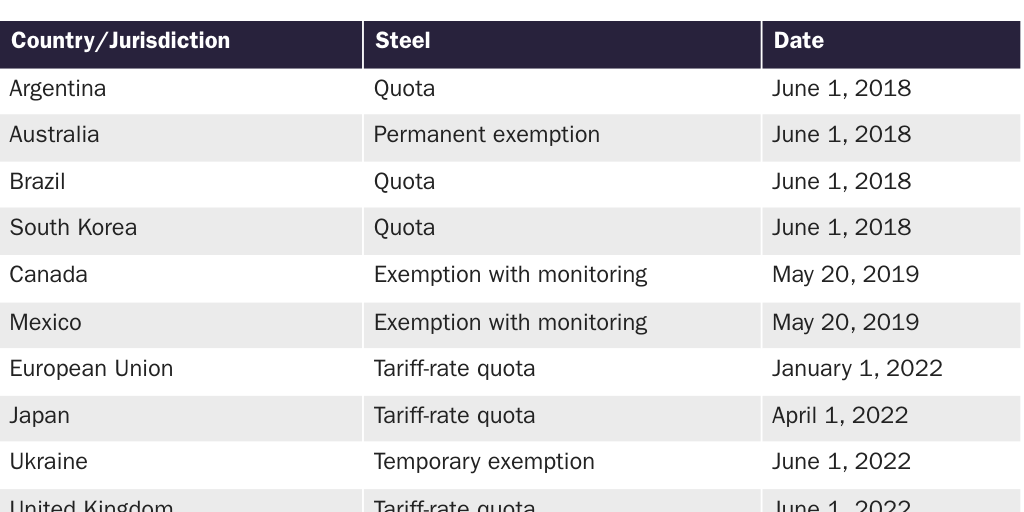

Likewise, the Trump administration used the tariffs as leverage to obtain minor concessions from South Korea during the talks to renegotiate the Korean–US Free Trade Agreement, which were launched shortly before the tariffs were announced.78 Australia was likewise granted an exemption, while several other trading partners were able to switch their tariffs for import quotas (Table 2).79

In late 2021, the Biden administration and the European Union agreed to the US–EU Arrangements on Global Steel and Aluminum Excess Capacity and Carbon Intensity. Under the deal, the US agreed to convert the tariffs on steel and aluminum to tariff-rate quotas, which assessed a lower tariff on imports up to a certain amount, after which a higher tariff was assessed. This was in effect from January 1, 2022, through December 31, 2023.80 The tariff-rate quota was set based on historical volumes. In exchange, the EU lifted its retaliatory tariffs and agreed to suspend its WTO disputes. The two sides also agreed to attempt to negotiate a more permanent solution that would target excess capacity and address carbon intensity in steel production.81 They were unable to come to a permanent agreement by the self-imposed deadline of the end of 2023, but agreed to extend the temporary agreement and the deadline to March 2025, at which point it lapsed and the EU retaliatory tariffs were reinstated.82

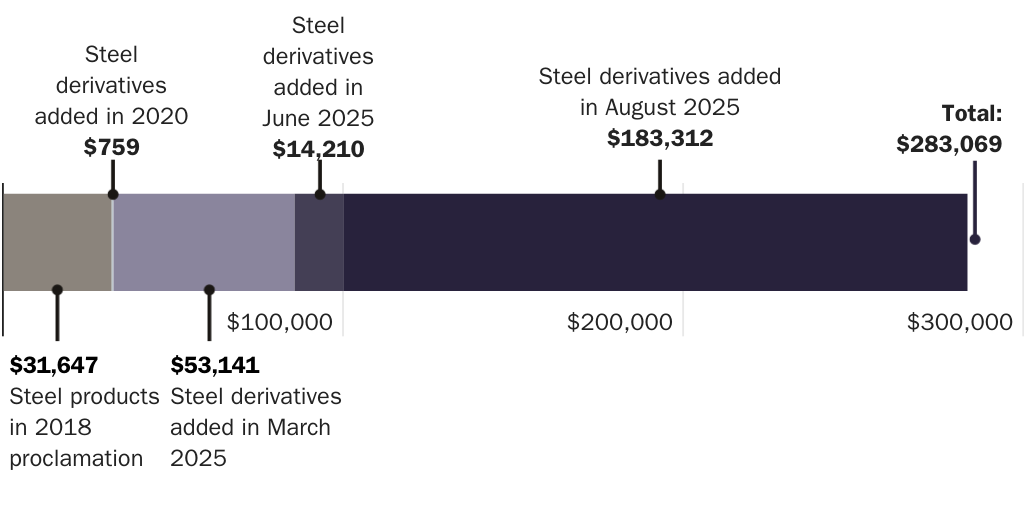

Early in his second administration, Trump effectively terminated all steel quota agreements and exemptions.83 While maintaining the 25 percent tariff rate, the policy’s scope was expanded to include additional derivative products—the first Trump administration had previously extended the tariffs to an initial set of derivative products in January 2020—with an exemption for products using steel melted and poured in the United States.84 The administration also abolished the exclusion process.85 In response, trading partners previously operating under quotas and exemptions announced plans for retaliatory measures.86 Notably, the tariffs on steel derivatives today include goods that lack any discernible connection with national security, such as refrigerator-freezers, washing machines, electric cooking stoves, and office furniture. These tariffs, moreover, cover a higher value of US trade (based on 2024 import values) than the tariffs on primary steel products (Figure 5).87 In June 2025, Trump raised the tariff rate on the covered imports to 50 percent.88

So, did the tariffs succeed in stemming the flow of imported steel into the United States while rejuvenating the domestic steel industry? According to a 2023 report from the USITC, steel imports decreased by about 17 percent between 2017 and 2021. Today, 80 percent of steel consumed in the United States is domestically produced.89 Domestic steel production has actually fallen between 2017, the year before the tariffs were implemented, and 2024—from 81.6 MMT to 79.9 MMT. Although domestic iron and steel capacity utilization increased by more than 5 percentage points—from 73.6 percent to just over 79 percent—between 2017 and 2021, it declined to 70.5 percent in 2024.90 Meanwhile, overall iron and steel capacity was about 3 percent lower in 2024 than in 2017, although it has been increasing in recent years, with steelmakers reportedly undertaking an aggressive expansion in capacity that was equivalent to about a quarter of total US steel production in 2024.91 Finally, steel producers’ net operating profits rose from about $5.5 billion in 2017 to $29.2 billion in 2021, before dipping to $10.3 billion in 2024.92 Although not all of these increases can be attributed to the Section 232 tariffs and/or increased antidumping/countervailing duties, certainly some can. And the steel industry is still clamoring for more protection, including more favorable antidumping and countervailing duty (AD/CVD) rules.93

Costs to the US Economy

These tariffs have been extremely costly for the United States. Despite Trump’s repeated assertions to the contrary, Americans, not foreigners, paid the cost of the tariffs. Looking at all of Trump’s 2018 tariffs (which includes tariffs on imports from China as well as the steel and aluminum tariffs), economists Mary Amiti of the New York Federal Reserve, Stephen J. Redding of Princeton University, and David E. Weinstein of Columbia University found that the tariffs were almost entirely passed through to domestic prices in the first year, leaving exporter prices unchanged.94 Focusing just on the steel tariffs, economists Brian D. Kelly and Gareth Green of Seattle University found that the tariffs were “fully absorbed by importers and led to price increases, roughly equal to the tariffs, in the American steel industry.”95 The USITC found that the tariffs increased the imported price of steel by 22.7 percent and found nearly complete pass-through of the tariff costs. That same USITC study found that the tariffs increased the average price of steel in the United States by 2.4 percent, with domestic steel prices increasing as well.96 Meanwhile, Gary Hufbauer and Euijin Jung of the Peterson Institute for International Economics estimate that the Section 232 tariffs increased aggregate income in the steel industry by about $2.4 billion in 2018 while raising the cost for steel consumers by close to $6 billion, meaning that the tariffs cost about $650,000 for each steel job saved.97

Because steel is a crucial input in myriad products, raising steel prices through import restrictions makes a number of domestically manufactured products less globally competitive. Economists Lydia Cox and Kadee Russ estimate that the increase in input costs from the Section 232 steel tariffs led to 75,000 fewer US manufacturing jobs by 2019.98 Kyle Handley, a Cato scholar and economist at the University of California, San Diego, and others found that export growth fell by 0.11 percent for each 1 percent increase in steel and aluminum tariffs because of increased input costs.99 Citing the USITC study, the Tax Foundation notes, “‘downstream’ industries experienced an annual $3.4 billion decrease in production from 2018 to 2021 due to the price increases, a 0.6 percent reduction per year on average.”100

Likewise, the steel tariffs triggered predictable foreign retaliation against American exports. Canada, China, the European Union, India, Japan, Mexico, Russia, and Turkey initially imposed more than $35 billion worth of tariffs on American exports. Because of country exemptions, retaliatory tariffs currently target fewer American exports, but the damage done was substantial nevertheless.101 In particular, American farmers and ranchers paid a heavy price because of the foreign retaliation resulting from the Trump administration’s steel, aluminum, and China tariffs. Eventually, the US Department of Agriculture dusted off a New Deal–era program to dole out bailout payments of about $30 billion to those farmers and ranchers affected by foreign retaliation.102

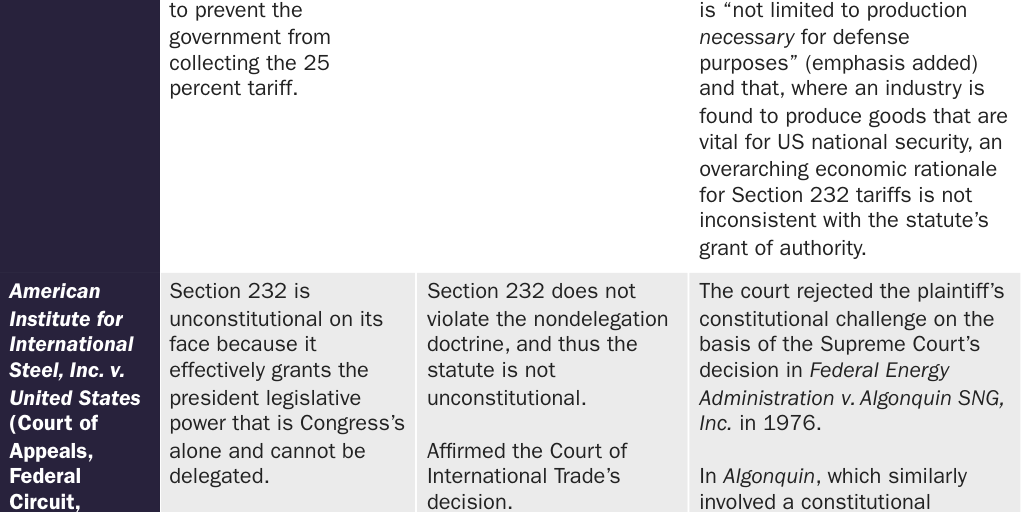

Although there have been legal challenges to the Trump administration’s Section 232 steel tariffs filed by various importers challenging procedural and substantive aspects, the government has won every case, and the Supreme Court has refused to hear appeals to lower court decisions upholding the tariffs, as Table 3 summarizes.103 Six-plus years after their implementation, the tariffs remain and continue to inflict pain on the US economy.

A holistic accounting of the Section 232 tariffs establishes that they fail to meet a basic cost-benefit analysis. While the tariffs may have boosted US steel company profits and spurred some domestic steel production, the gains were modest, and boosting inefficient domestic production should not be considered a positive outcome—especially if it requires perpetual tariffs or subsidies to survive, or if it leads to an oversupply of steel in the market. More importantly, these gains pale in comparison to the tariffs’ high economic and geopolitical costs. A recent analysis from the Tax Foundation found that repealing the Section 232 steel and aluminum tariffs would increase GDP by 0.02 percent and $3.5 billion, increase wages by 0.01 percent, increase capital stock by 0.02 percent, and create more than 4,000 jobs.104 Repealing the tariffs should be a priority for future presidential administrations.

Trade Remedies

Although the United States had long used its post–World War II economic heft to negotiate agreements to lower global trade barriers such as the GATT and NAFTA, it simultaneously enhanced its ability to use aggressive trade remedies, particularly antidumping (AD) and countervailing duties (CVD), both of which are recognized as exceptions to general WTO trade rules prohibiting discrimination.105 Today, the domestic steel industry is the largest user (abuser) of US trade remedies and drives many of the legal and regulatory changes that have turned the remedial AD/CVD laws into protectionist cudgels.

Under US antidumping laws, dumping occurs when a foreign company sells goods in the United States below fair value. Beginning in 1916, and then through a series of revisions, US law provided a mechanism—AD—to protect domestic producers that have been, or are threatened with, material injury from imports sold at prices determined to be less than fair value.

There is a two-pronged analysis for antidumping duties to be imposed: First, the Department of Commerce’s International Trade Administration (ITA) must determine whether an imported product is being sold, or likely to be sold, in the United States at less than fair value. Next, the USITC (an independent, bipartisan agency) investigates whether the domestic industry is materially injured or threatened with material injury because of the importation of a product sold at less than fair value.106 If there is an affirmative finding by both Commerce and the USITC, the product is determined to be dumped in the US market, thus entitling the import-competing industry to relief.

The value of the import relief—known as the margin—is ostensibly calculated by comparing the sales price of the product in the home country versus the sales price charged in the United States. In the event there are not enough sales in the producer’s home market to establish a normal value, Commerce will typically look at two alternatives—either the producer’s sales prices in third-party countries, or Commerce will construct a value by adding the cost to produce the US-bound product plus reasonable allowances for expenses and profits.107

Meanwhile, CVD law was originally developed in the 1890s as a tool to offset foreign export subsidies. Like AD law, CVD law has been revised several times over the years to expand the definition of dutiable foreign subsidies and change administrative procedures. Like AD cases, there is also a two-pronged analysis for an affirmative finding, and thus, application of CVDs: First, Commerce is tasked with determining whether there is a basis to believe that a foreign government is providing a subsidy for the product sold in the United States. Second, the USITC must determine whether the imported product has caused injury or is likely to cause injury to the domestic industry.108 If affirmative determinations are made, Commerce calculates a subsidy rate for each exporter and producer individually investigated, which serves as the basis for the duty.

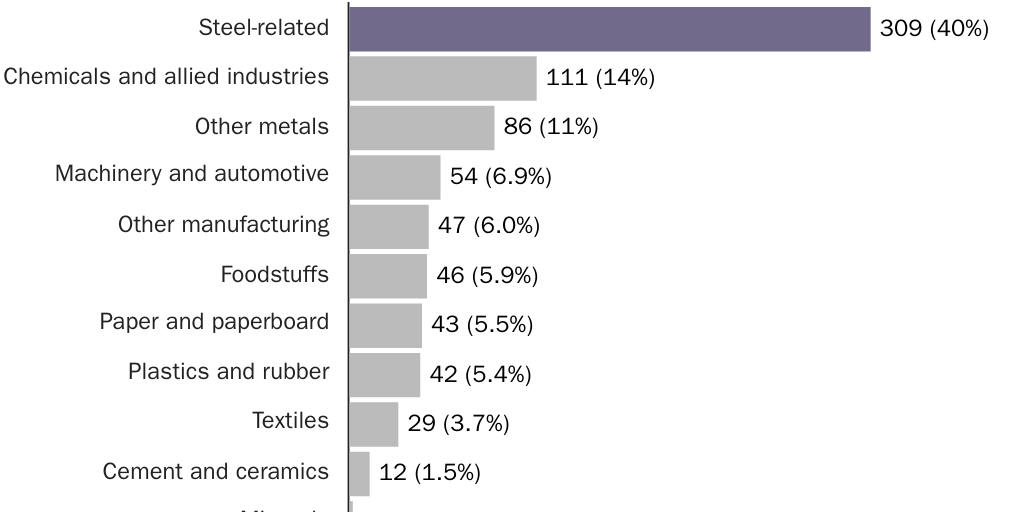

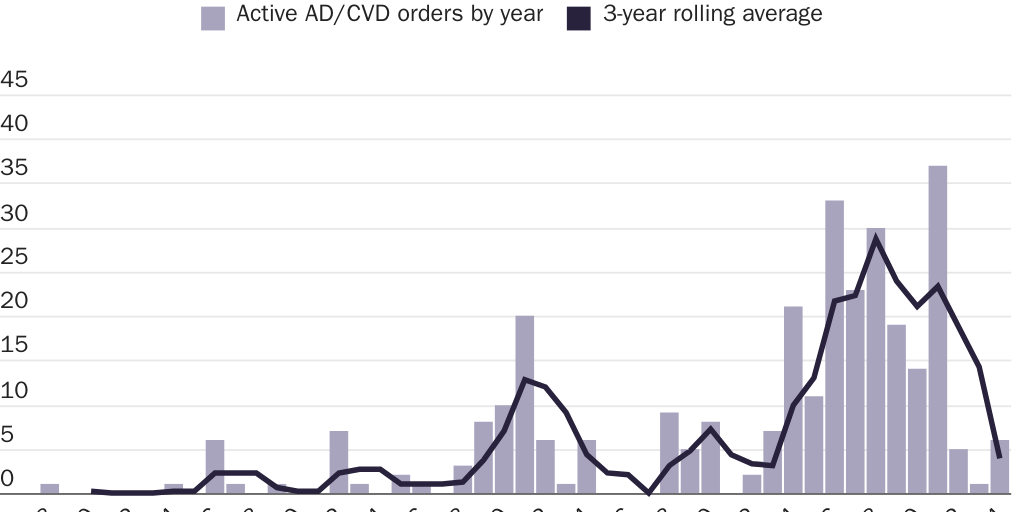

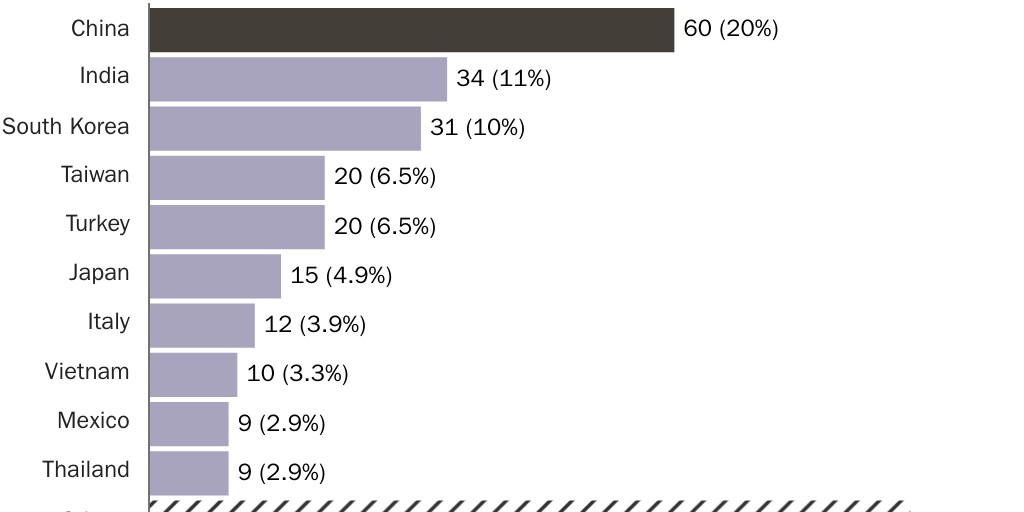

Over the years, the domestic steel industry has successfully lobbied Congress to reform AD/CVD laws in ways that favor more affirmative findings by Commerce and the USITC at higher and higher margins for steel and nonsteel petitioners. And once laws were changed, the domestic steel industry became an aggressive user of the US trade remedies regime, to the detriment of domestic steel users, whose interests by law cannot be considered by the USITC. As Figure 6 shows,109 there are 310 steel-related antidumping and countervailing duties and suspension agreements in place out of a total of 721 such investigations—more than 40 percent.110 Between 2016 and 2023, the USITC noted that there were more than 140 AD/CVD orders imposed on steel mill products originating in 34 countries.111 In other words, the domestic industry is increasingly turning to AD/CVD laws to protect themselves from foreign competition (Figures 7 and 8).112

The domestic steel industry and its protectionist supporters in Congress have long influenced Commerce’s decisions in AD/CVD cases. Based on investigations by Commerce’s Office of Inspector General, interviews with former congressional and Commerce Department staff revealed troubling patterns of bias favoring the steel industry. Career Commerce Department officials who oversee all antidumping determinations in steel cases regularly met with Congressional Steel Caucus members and staff to discuss ongoing antidumping and countervailing duty proceedings. These Commerce officials sometimes shared draft investigation results with the Steel Caucus before official announcements, enabling the Steel Caucus to provide input. Senior agency officials repeatedly pressured lower-level Commerce Department staff who are investigating foreign steel producers to recalculate figures and modify methodologies, which led to increased AD/CVD duties.113 Not only is the steel industry an aggressive user of AD/CVDs, but it and its protectionist supporters in Congress have found innovative ways to inflate duty rates in AD/CVD cases.

Zeroing

Another protectionist sleight of hand in the dumping context is a methodological practice known as “zeroing,” which helps inflate final duties. In antidumping investigations, Commerce calculates the average US prices for each product under investigation. These prices are then compared to the “normal value,” which “can be calculated a number of different ways but is ideally the weighted-average net price of the most similar product sold in the home market.”114 Antidumping calculations can involve thousands of price comparisons to generate a single margin for the product in question.115 Zeroing is the process by which Commerce handles these price comparisons:116

- When the home market price is higher than the US price, the difference counts as a positive dumping margin for that product;

- When the US price is higher than the home market price, which should count as a negative in the overall margin calculation, Commerce sets the difference to zero instead of using the actual negative value.

Commerce then adds all these comparisons together and divides by the total export sales to calculate the final dumping margin. By eliminating negative margins through zeroing, Commerce artificially inflates the overall dumping rate. The steel industry, in particular, has been a major beneficiary of zeroing methodologies in dumping investigations.117 The United States is the only country that actively utilizes zeroing in its antidumping methodologies.118 The zeroing methodology has been challenged numerous times at the WTO and has generally been found to be inconsistent with the United States’ WTO obligations.119

2015 Reform

As the Obama administration was finalizing the Trans-Pacific Partnership negotiations, Congress passed the Trade Preferences Extension Act of 2015 (TPEA). The law renewed Trade Promotion Authority, but it also contained novel tools to inflate dumping margins long sought by the domestic steel industry.120

Particular Market Situation

Under prior antidumping law, Commerce was only permitted to adjust a respondent firm’s submitted costs “only if those costs failed to reconcile to the company’s audited financial statements, the respondent was uncooperative or incapable of supplying the requested information, or those costs reflected transactions not made at arm’s length.” Under such circumstances, Commerce had to find a “viable third-country home market to serve as the comparison market. Absent a viable third-country home market, it was instructed to rely on the respondent’s cost data to calculate a constructed value estimate of what those home market prices should be.”121 Under the TPEA, Commerce is not required to use a third-country home market if it determines that a particular market situation (PMS) exists in the home market, and is therefore empowered to go to a cost-based, constructed value approach and use any calculation methodology to construct normal value, which has proven to be extraordinarily broad in practice. In essence, the law removed old constraints and gave Commerce sweeping authority to reject, revise, and recalculate costs at its own discretion—and thus substantially inflate dumping margins (and antidumping duties).

The first application of this new authority came in 2017, when Commerce reviewed an antidumping order on oil country tubular goods (OCTG)—steel pipes used by the oil and gas industry to drill and transport oil and gas—from South Korea. Commerce determined that a PMS existed, claiming that the South Korean producers’ cost data understated their true costs based on the collective impact of five factors: the Korean government’s subsidies for hot-rolled coil (HRC) production (which accounts for a large portion of the cost of OCTG production); strategic alliances between HRC and OCTG producers creating distortions in prices; government-led restructuring of the South Korean steel industry; the Korean government’s involvement in the electricity market; and imports of HRC from China.122 This finding led to upward adjustments in the surveyed South Korean producers’ reported costs and significantly higher duties for US importers of Korean OCTG.

The subsequent use of PMS provisions in 11 additional cases revealed the extraordinary breadth of Commerce’s new discretion. Under this approach, Commerce was free to act with extremely wide latitude, even when its decisions appeared partial or arbitrary, while remaining well within the bounds of the law. This development raised serious concerns about the delegation of congressional authority and the rule of law itself.

In 2022, the US Court of Appeals for the Federal Circuit issued its opinion in Nexteel Co., Ltd. v. United States, which involved an appeal from Commerce’s administrative review of the antidumping order on OCTG from South Korea. The Court of Appeals criticized Commerce’s PMS determinations for a number of reasons: Commerce relied on outdated HRC subsidy rates by the South Korean government; Commerce failed to show that subsidies were passed through HRC prices or uniquely affected Korean OCTG producers; Commerce failed to establish true strategic alliances between HRC and OCTG producers; and Commerce had no actual evidence to support the South Korean government’s involvement in industry reshuffling during the relevant review period.123 The Appeals Court agreed that Commerce’s PMS finding was not supported by sufficient evidence and remanded the case for further consideration.

Shortly after the US Court of Appeals for the Federal Circuit issued its opinion in Nexteel, Commerce issued its first regulatory guidance since the 2015 cost-based PMS provision was established.124 Whereas prior law did not establish standards by which Commerce could find a PMS, thus permitting a case-by-case analysis, the new rulemaking provides some guidelines for how Commerce will do its PMS analysis. Yet the now codified guidelines are very favorable to petitioners in AD proceedings, as the domestic steel industry frequently is. Specifically, the new rules allow Commerce to make PMS determinations without precisely quantifying distortions; allow Commerce to consider weak human-rights records, property, and labor protections as factors; allow Commerce to find PMS, even if similar situations exist in other countries; and allow PMS adjustments even if Commerce is addressing the same issue in CVD proceedings.

The PMS provision exemplifies how the antidumping law has evolved from a remedial tool into an instrument of aggressive protectionism. This transformation has had wide-ranging negative consequences. American companies that rely on imports face higher costs, consumers pay higher prices, and US exporters risk retaliation from trading partners. The provision has also strained international trade relationships and undermined the predictability of the global trading system.

In practice, the PMS provision has been particularly helpful to protectionist domestic industries, including the steel industry. Commerce has repeatedly used it to adjust costs upward based on various factors, including the effects of global steel overcapacity, government subsidies, and strategic alliances between producers. The department has shown a willingness to aggregate multiple factors to justify PMS findings, even when individual factors might not warrant such a determination.

This expansion of administrative discretion represents a worrisome trend in US trade law. By allowing Commerce to essentially rewrite foreign producers’ costs based on its own judgment, the PMS provision has moved antidumping proceedings further away from objective economic analysis and closer to subjective political decisionmaking. The result is a system that can be more easily manipulated to achieve predetermined outcomes regardless of the economic realities involved.

The transformation of antidumping law through provisions such as PMS reflects a broader shift in US trade policy toward more aggressive unilateralism. While ostensibly designed to address unfair trade practices, these changes have created a system that can be used to impose significant trade barriers with minimal accountability or oversight, potentially undermining the very principles of fair trade they were meant to protect.

Adverse Facts Available

The Commerce Department lacks subpoena power in antidumping and countervailing duty AD/CVD investigations, requiring it to rely on information voluntarily submitted by parties. Where information submitted is incomplete, Commerce fills in gaps with facts that are available—a practice accepted under WTO standards.125 Prior to 2015, when Congress passed the TPEA, Commerce could apply adverse facts available (AFA), often using petitioners’ data adverse to the noncooperative party’s interests, but this power was constrained by judicial oversight.

Two Federal Circuit decisions established important limitations on Commerce’s AFA authority:

- F.lli De Cecco Di Filippo Fara S. Martino S.p.a. v. United States (2000) required that AFA rates be “a reasonably accurate estimate of the respondent’s actual rate, albeit with some built-in increase intended as a deterrent to non-compliance.”126

- Gallant Ocean (Thailand) Co., Ltd. v. United States (2010) mandated that AFA rates must reflect “commercial reality.”127

These cases required Commerce to balance incentivizing compliance while ensuring fair trade, rather than doling out punishment and engaging in protectionism. The TPEA eviscerated these judicially established standards by eliminating the requirement that Commerce estimate what the actual dumping or subsidy rate would have been if the party had cooperated, and it removed any obligation to demonstrate that the AFA rate reflects the commercial reality of the interested party.128

The results have been severe. While proponents argue that AFA encourages transparency and expedites investigations, in practice it has led to extremely high margins. In one post-TPEA steel case, Commerce applied an outrageous 700 percent dumping margin, which clearly had no basis in commercial reality.129 Likewise, in the OCTG case referenced above, Commerce used an AFA finding from a subsidy investigation involving hot-rolled steel coil to conduct a PMS situation analysis and increase the respondents’ costs.130

The burden placed on foreign respondents in these investigations is already immense. Companies must respond to extremely detailed questionnaires and provide massive amounts of information within very tight deadlines—often just a few weeks. This is particularly challenging for smaller companies that may lack sophisticated accounting systems or the resources to compile the requested data in the specific formats required. Even minor mistakes or omissions in these complex submissions can trigger the new enhanced AFA, regardless of whether they are inadvertent or materially affect the investigation.

The collateral damage caused by AFA extends beyond the specific companies found to be non-cooperative. In cases involving “all others” rates, cooperative companies can be punished with high duties because of other companies’ noncooperation.131 In countervailing duty cases, entire industries may face steep duties because their government was deemed noncooperative, even if the companies themselves fully cooperated. US importers ultimately bear much of the cost burden of AFA duties, despite having no control over foreign companies’ cooperation.

Most fundamentally, AFA fails to strike an appropriate balance between administrative efficiency and fairness. While Commerce needs tools to conduct effective investigations, the current AFA framework provides inadequate procedural protections against abuse of discretion. The agency can apply AFA without sufficiently considering the nature and circumstances of alleged noncooperation or whether selected adverse facts reasonably reflect commercial reality. Today, the domestic steel industry has benefited from this aggressive approach to AFA applications and will continue to do so as long as the law remains unreformed.

The Nationalization of a Steel Firm: The Nippon–U.S. Steel Merger

The tariffs’ failure to produce a vibrant and globally competitive domestic steel industry—and the federal governments’ coddling of the industry—is evident in the case of U.S. Steel and its recent acquisition by Japan’s Nippon Steel.

The Committee on Foreign Investment in the United States (CFIUS) is an interagency panel tasked with determining whether proposed foreign investment and the purchase of US assets jeopardizes national security.132 On the recommendation of CFIUS, the president has the power to block proposed mergers, acquisitions, and takeovers. Between its creation in 1988 and today, presidents have blocked a total of nine transactions on national security grounds based on recommendations from CFIUS, including Nippon Steel’s proposed acquisition of U.S. Steel in January 2025 (before Trump reversed this decision and allowed the deal to go through in June 2025).133

During the summer of 2023, Cleveland-Cliffs, an Ohio-based steel producer, backed by the USW, made an unsolicited bid to purchase one of its largest domestic competitors, Pittsburgh-based U.S. Steel. Cleveland-Cliffs’ offer was for $7.3 billion. U.S. Steel rejected the offer.134 In late 2023, Japan-based Nippon Steel—which has operated in the United States since the early 1980s,135 including in unionized plants in Pennsylvania and West Virginia136—made a $14.9 billion offer to purchase U.S. Steel, which U.S. Steel accepted pending regulatory approval.137

Protectionist politicians across the political spectrum expressed opposition to the deal and urged the Treasury to use CFIUS to block the proposed acquisition on national security grounds.138 In early January 2024, CFIUS opened a probe into the deal as it became a hot-button topic in the run-up to the 2024 presidential campaign.139 In January 2025, the outgoing Biden administration announced it would block the proposed acquisition on national security grounds.140 Shortly thereafter, Nippon Steel and U.S. Steel jointly filed lawsuits against the outgoing Biden administration, on one hand, and Cleveland-Cliffs, its CEO, and the president of the United Steelworkers on the other, in a last-ditch effort to salvage the transaction.141 Both lawsuits were dropped after Nippon Steel acquired U.S. Steel in June 2025.142

Was the Proposed Acquisition a National Security Concern?

Today U.S. Steel is not the globally competitive behemoth it once was, and a short history is warranted. The company was formed in 1902 by merging Carnegie Steel and Federal Steel, along with several other smaller companies. The company was at its peak during World War II and shortly thereafter, it had grown to 340,000 employees.143 The entire US steel industry produced 60 percent of all the world’s steel, as other major producers had been destroyed during the war. At the time, U.S. Steel was nearly twice the size of its largest domestic competitor, Bethlehem Steel.144

Over time, U.S. Steel became complacent and was slow to adapt new technologies to enhance productivity and output. However, Japanese steel companies (heavily subsidized by the government) were quick to embrace basic oxygen furnaces, which were cheaper to build and produced steel more quickly than the legacy open hearth furnaces employed by most American steel companies, including U.S. Steel. Basic oxygen furnace technologies were first deployed commercially in Austria in 1952 but weren’t used by U.S. Steel until 1964. Meanwhile, Nippon Steel was leveraging economies of scale in the size of its blast furnaces. Indeed, “by the mid-1970s, average blast furnace size at Nippon Steel was 4 times the average at U.S. Steel, and by 1977 more than half the blast furnaces in Japan had a volume of more than 2000 cubic meters, compared to just 2.6% in the US.”145

U.S. Steel also faced stiff competition from innovative domestic firms. The company’s annual output peaked in 1979, when it produced 29 million tons of steel.146 Over time, U.S. Steel—like many legacy domestic producers—struggled to innovate, and its market share, both domestically and on the world market, began to decline.

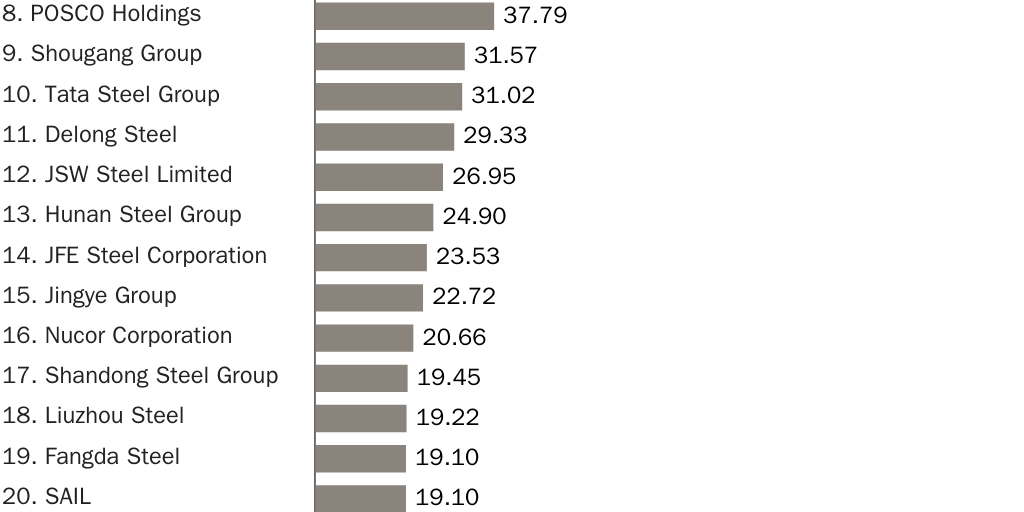

Today the company employs about 20,000 Americans.147 Yet that figure, as Cato’s Scott Lincicome noted, is just 0.15 percent of the United States’ manufacturing workforce.148 Once the largest company in the world by market capitalization, U.S. Steel’s market capitalization at the end of 2024 put the steel company outside the top 2,000 in the world.149 Likewise, U.S. Steel’s output in 2024 was 14.18 million tons of steel—less than half of its peak in 1979.150 U.S. Steel trails domestic competitors such as Nucor and Cleveland-Cliffs in terms of annual output, and it is the lowest domestic producer in terms of utilizing capacity.151 Globally, U.S. Steel was the world’s 31st-largest producer in 2024 (Figure 9).152 U.S. Steel’s sales revenue in 2024 was $15.6 billion, which placed it behind Nucor, Cleveland-Cliffs, and Steel Dynamics, among domestic steel producers.153

Given all this, there was no basis for the assertion that Nippon’s proposed acquisition of U.S. Steel posed a national security risk to the United States. In 2018, then-Defense Secretary James Mattis estimated that the US military only required about 3 percent of domestic steel capacity.154 U.S. Steel itself noted that its “manufacturing technologies and processes are not designed specifically for the production of steel with military applications, nor does U.S. Steel have any products, capability, or know-how that is specific to any US government applications, including US military applications.”155 Indeed, U.S. Steel has no current military contracts.156

Moreover, Japan is one of the United States’ strongest and most important allies. The US–Japan Security Treaty of 1960 obligates the United States to defend Japan militarily if the island nation is attacked. As Scott Lincicome has noted, Japan receives about 90 percent of its defense-related imports from the United States.157 Dan Ikenson, an international trade and investment expert, noted that

US and Japanese companies work together on defense-related projects and Japan is integral to the US-led efforts to deter China’s increasingly menacing behavior toward Taiwan and toward the Philippines, Vietnam and other countries in the region over various discredited maritime/territorial claims, which threatens one of the world’s most important commercial waterways.158

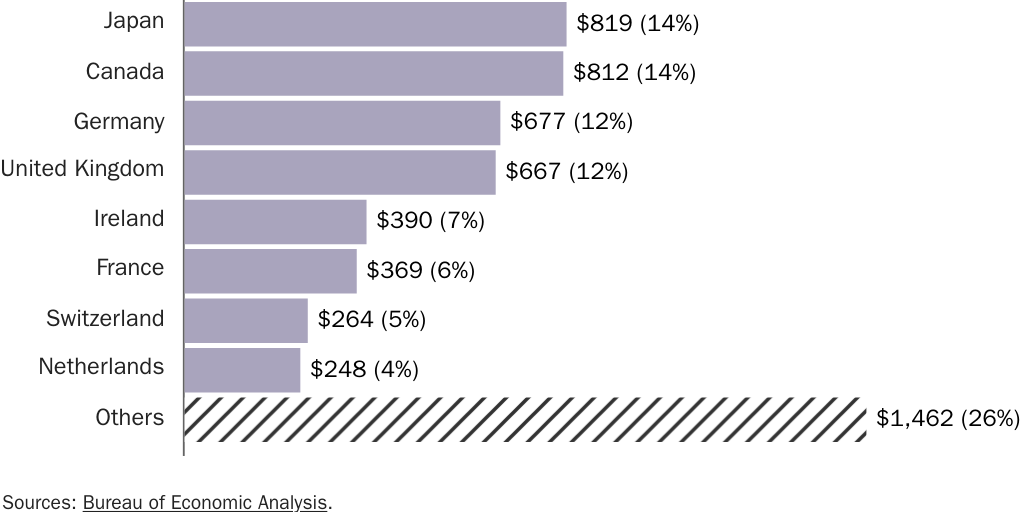

The two countries also have extensive economic ties. Japan is the largest source of foreign direct investment in the United States (Figure 10).159 As of 2024, Japanese firms and individuals had more than $819 billion invested in the United States. For example, Toyota and Honda automotive plants—and myriad other Japanese-based multinationals—are spread across the United States. Japanese-based firms operating in the United States employ nearly one million Americans.160 Yet in the perspective of total Japanese foreign direct investment, the U.S. Steel deal is insignificant.

Nippon’s offer made good economic sense for U.S. Steel’s shareholders and its employees. Nippon’s $14.9 billion offer represented a 40 percent premium over U.S. Steel’s share price as of December 15, 2023, the day the offer was made. Likewise, Nippon planned to invest $2.7 billion to upgrade U.S. Steel’s production capabilities in its integrated steel mills, including at least $1 billion to upgrade U.S. Steel’s Mon Valley Works and $300 million for Gary Works facilities.161 As part of the proposed acquisition, Nippon promised to keep the U.S. Steel name, maintain its headquarters in Pittsburgh, honor existing USW contracts, promised no layoffs or plant closures before 2026, agreed not to transfer production capacity or jobs outside the United States, and agreed to continue U.S. Steel’s antidumping/countervailing duties strategies.162 Likewise, the merger would allow U.S. Steel to leverage Nippon’s advanced technologies and research and development capabilities, creating a larger, more competitive firm that would operate domestically and internationally. U.S. Steel’s CEO warned that blocking the acquisition could force the company to shutter steel mills, just as it had closed parts of plants near Detroit and St. Louis.

The deal also made geopolitical sense. In 2022, 6 of the top 10 steel producers in the world were Chinese-based firms.163 Combining the output of Nippon and U.S. Steel would bump the conglomerate to the world’s third-largest steel company. For those concerned about Chinese overcapacity and Beijing’s willingness to engage in coercive trade practices, the newly strengthened company could serve as a bulwark.

Indeed, considering increasing competition between the United States and China, Washington policymakers should be diligently working to shore up trade and investment ties with reliable allies, particularly those in the Asia-Pacific region. Rhetorically at least, a bipartisan cadre of voices supports this idea: The Biden administration emphasized what it termed “friendshoring”164 and the House Select Committee on the Chinese Communist Party wisely recommended adding Japan to the whitelist of excepted foreign states that receive expedited CFIUS review.165 Yet this rhetoric is increasingly at odds with reality, which opens the door to Chinese leadership.

That was the promise of a merged private entity. What actually transpired is even more damning than simply denying the merger on national security grounds under CFIUS.

In June 2025, after an unjustified delay, the Trump administration granted approval for $14.9 billion Nippon‑U.S. Steel merger on the condition that the United States government receive a “golden share” in the merged entity. What should have been a quick, straightforward approval became mired in electoral politics and, ultimately, socialism, with the effective nationalization of the merged steel firm. Indeed, the golden share gives Trump, in his tenure as president of the United States, and the Department of the Treasury and the Department of Commerce after Trump’s presidency ends, control over key business decisions made by the new firm.166

The terms of the golden share are breathtaking in scope. As Commerce Secretary Howard Lutnick detailed, the federal government now holds a veto over virtually every significant business decision this new entity might make.167 The company is prohibited from relocating its headquarters away from Pittsburgh, it cannot change its name, it cannot reduce promised investments, and it cannot transfer production overseas or close plants without presidential approval. The government can name one of three independent directors and veto the other two choices.168

Our Cato colleague Scott Lincicome noted that this arrangement meets the federal government’s own definition of nationalization. When it comes to trade remedies law, the Commerce Department

treats “public entities” (aka “public bodies”) in its investigations of subsidized imports, repeatedly finding that foreign companies with little or even no direct government ownership can nevertheless be “meaningfully controlled” by a foreign government—and thus akin to the government itself—where the state remains involved in important aspects of the company’s business operations, such as plant closures or board of directors appointments.

Commerce regulations “repeatedly cited special ‘golden shares’ as evidence that a company under investigation is controlled by another company or by the state, even though the controlling entity doesn’t officially own a majority of voting shares in the company.”169

Likewise, Lincicome notes, the first Trump administration “incorporated the U.S. government’s broad view of state control over private commercial entities” into the USMCA, specifically on state-owned enterprises.170

The federal government effectively nationalizing a steel company presents all sorts of economic and political problems—the types of problems that perpetually plague socialist policies. Politically, this move further entrenches the unholy alliance between the federal government and the domestic steel industry as documented by this paper—particularly biasing US trade policy further toward domestic steel producers at the expense of domestic steel users, such as manufacturers and builders. Further, creating a government backstop will almost certainly lead to a bloated, inefficient firm.

As Lincicome noted, there are also implications for more nationalization. Given that the Trump administration has declared imports of a number of other products and industries to be national security risks, could more government control be on the horizon? Now that the door is open, will future presidents try to nationalize other firms when a foreign acquisition is tabled?

The long-term reputational damage to the United States from these series of misguided decisions could be even more detrimental than the shorter-term impact of U.S. Steel’s effective nationalization. In effect, this long and convoluted process exposed how a supposedly technocratic and dispassionate institution like CFIUS can be wielded against private companies from foreign countries—even those from long-standing allies and advanced market economies such as Japan. Ultimately this chapter of history is a sad reminder of how damaging the domestic steel industry’s stranglehold over public policy has been—and continues to be.