Medicaid is a means-tested government health and long-term care program that states operate largely with funds from the federal government. In 2025, Medicaid will spend nearly $1 trillion on behalf of 84 million enrollees, or nearly $12,000 per enrollee. Medicaid is the largest purchaser of long-term care (LTC) in the United States, covering nursing home, memory, personal, and other forms of care for qualifying persons. In 2025, Medicaid will spend roughly $80,000 per enrollee receiving Medicaid LTC subsidies, which account for more than one-third of Medicaid spending and nearly half of total LTC spending. Yet, Medicaid subsidies reduce LTC quality, strain state budgets, and contribute to a federal debt that has surged past 100 percent of US gross domestic product.

Counterintuitively, Medicaid subsidizes LTC for middle-class and affluent individuals, who do not need government assistance. Middle-class people easily qualify for Medicaid under the basic financial eligibility rules. Some individuals with significant assets artificially impoverish themselves to become eligible for and receive Medicaid LTC subsidies.

Eliminating Medicaid LTC subsidies for individuals who could meet or could have planned to meet their own LTC needs would improve LTC quality and reduce the burdens Medicaid imposes on taxpayers. Middle-class and affluent seniors could draw on their assets and private LTC insurance, saving Medicaid as much as $100 billion per year without impairing its ability to serve those who truly need assistance.

Introduction

Long-term care (LTC) includes the long-term services and supports people require when they cannot perform basic activities of daily living without assistance. Individuals may need such assistance because of injury, illness, frailty, cognitive impairment, or old age. This need is growing as America’s vulnerable aging population surges.

Most people will not use commercial LTC services or will use them for only a short time. Some 55 percent of people who reach age 65 will not use any paid LTC services, while another 31 percent will purchase LTC services for two years or less.1 Richard W. Johnson and Claire Xiaozhi Wang found that “nearly nine in ten older adults have enough resources, including income and wealth, to cover assisted living expenses for two years.”2

The remaining 14 percent of the population, who will use commercial LTC for two years or more (especially the 4 percent who will use it for more than five years), incur large LTC expenditures.3 Median nursing home prices are $117,000 per year for a private room and $104,000 for a semiprivate room. Assisted living runs $64,000 per year. Full-time, year-round homemaker and home health aide services could cost $88,000 and $96,000, respectively.4 Longer-term LTC at those prices is unaffordable for many individuals and families—at least without LTC insurance, which too few people purchase.

Much of the popular and academic literature assumes that people across the country are spending huge sums of their own money on nursing homes, assisted living facilities, and long-term home care.5 The media tell us that many people spend down their life’s savings for this high-cost but rare—and therefore insurable—expense.

However, there is a problem with this conventional wisdom: The available evidence suggests that widespread, ruinous LTC spend-down does not occur.

Most LTC expenditures come not from individuals’ incomes or assets but from third parties—primarily government. Those subsidies are so easy to access that people who otherwise could use their own resources—to purchase LTC directly or purchase private LTC insurance—instead rely on taxpayer subsidies. The results are an anemic market for LTC insurance, a market for LTC services that exhibits shortages and low-quality care, and taxpayer dollars going to non-needy individuals who can afford to pay for their own LTC.

LTC Financing

The available evidence suggests that many individuals are not spending down their assets on LTC before government begins picking up the tab.

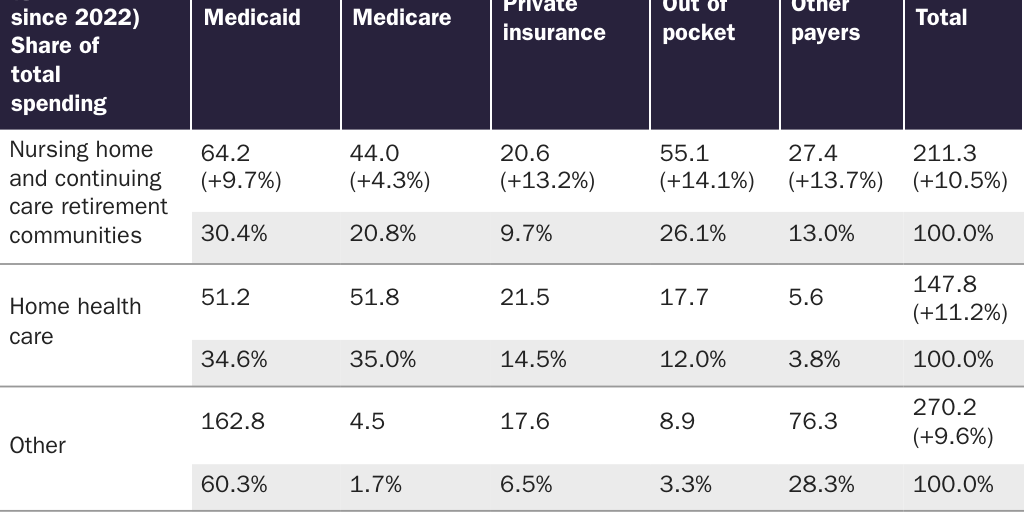

Consider what the data say about who pays for LTC. In 2023, total LTC spending was $629 billion (Table 1).6 Government paid for nearly two-thirds of that spending: Medicaid covered 44 percent, and Medicare (the federal program that subsidizes health care for the disabled and people over age 65) covered 16 percent. Private insurance paid 9 percent. Other public and private sources covered 17 percent. Personal out-of-pocket spending (OOP) accounted for just 13 percent.

That OOP share appears small relative to the assets that individuals could theoretically tap to finance LTC. US residents hold trillions of dollars in retirement savings ($40 trillion),7 home equity ($35 trillion),8 and life insurance ($22 trillion),9 for a total of $97 trillion from these resources alone. Research indicates that US seniors hold $14 trillion in home equity.10

Moreover, much of that 13 percent OOP share comes from personal income, not assets.11 As a result, only 6–7 percent of all LTC spending could possibly come from spend-down of private savings. At roughly $41 billion, OOP asset spend-down barely scratches the surface of seniors’ $14 trillion in home equity, much less all $97 trillion in available private wealth.

These facts don’t sit well with the conventional wisdom about widespread catastrophic private LTC asset spend-down. So what might better explain what we’re seeing in the numbers?

Medicaid’s LTC Financing Role

For answers, we look to Medicaid, a government welfare program that is the largest purchaser of LTC in the country. In 2025, it will spend roughly $994 billion on behalf of 84 million enrollees.12

Medicaid heavily subsidizes LTC for all who meet income and other requirements. In 2023, it accounted for 44 percent of total LTC expenditures.13 It pays for most of the longest, most expensive LTC needs. While fewer than 5 percent of enrollees receive LTC subsidies from Medicaid, LTC accounts for 33 percent of Medicaid expenditures.14 In 2025, Medicaid will spend on average $11,905 per enrollee.15 It will spend nearly seven times that amount—more than $80,000—per enrollee receiving LTC subsidies.16

On paper, Medicaid prohibits individuals with income and assets above certain limits from enrolling in the program and receiving those subsidies. It requires recipients with personal income, including Social Security benefits, to contribute to the cost of their LTC.17

Because Medicaid is a welfare program with supposedly draconian income and asset limits, and because it has become the dominant payer for the longest-term needs and largest LTC expenditures, most analysts and the media assume that Medicaid LTC enrollees must have spent down their income and assets for care until it impoverished them and they qualified for Medicaid benefits. This is a fallacy, and it is this fallacy that resolves the paradox of low personal OOP LTC spending despite sky-high national LTC expenditures.18

Financial Eligibility for Medicaid LTC

Medicaid income and asset limits are more lenient than most observers believe. Contrary to conventional wisdom, virtually no amount of income or assets automatically disqualifies someone from receiving Medicaid LTC subsidies. People with moderate income and assets qualify under the basic eligibility rules. For more affluent individuals, financial advisers can reconfigure practically any amount of wealth in a manner that allows the owner to receive the subsidies.

Medicaid does require a low income to qualify for LTC benefits. But most state Medicaid programs deduct private health and LTC expenditures from income before applying the low-income standard. As a result, even high-income individuals can qualify if their medical and LTC expenditures are commensurately high. (They usually are for seniors in need of expensive, long-term custodial or medical care.) Some states do impose a bright-line income limit, but those states also allow special income diversion trusts that achieve the same result of enabling higher-income people to qualify.19

Likewise, high assets scarcely interfere with eligibility for Medicaid LTC. States and the federal government exempt most of the large assets that seniors own—such as home equity, tax-favored retirement savings, or an automobile—from Medicaid’s asset limits. Medicaid usually caps countable assets such as cash, stocks, bonds—really anything easily convertible to cash—at $2,000. But would-be recipients can easily convert excess countable wealth to exempt status by using it to purchase exempt assets.20 The long list of exempt resources is readily available online or from financial advisers who specialize in adjusting clients’ income and assets to qualify them for Medicaid LTC subsidies.21 Medicaid disqualifies applicants if they have made certain asset transfers (e.g., to family) within the past five years, but ignores transfers that occur earlier.

Mystery Solved

It should be clear by now how private out-of-pocket LTC spending can be so low even though total national LTC spending is so high.

The public pays relatively small, shorter-term LTC expenses out of their available income and assets without great difficulty. But as LTC need extends in time and cost, pressure builds on families to find a way to fund the care. Millions heroically take on the responsibility of caring for loved ones without pay. But the financial and emotional stress is so great that many seek help elsewhere.

Whether from family, friends, LTC providers, financial advisers, or advertisements, the people seeking help eventually discover Medicaid. But it comes with downsides, such as the need to rejigger income and assets to qualify, access and quality problems, institutional (i.e., nursing home) bias, and long waiting lists for home care.

Because Medicaid saves families from having to spend down their assets for care—that is, because it does not require recipients to impoverish themselves before obtaining subsidies—very few people bother taking steps to protect themselves from those risks. Consciously or unconsciously, the public gets the message that insuring against these risks with private LTC insurance is not necessary.

Consequences

What are the ramifications of this unwieldy LTC system for each of its economic stakeholders?

For government, the dominant payer, LTC is a huge expense that unrelentingly compounds budget deficits and long-term debt. At one-third of total Medicaid spending, LTC subsidies both strain state budgets and add to a growing federal debt that has already surpassed 100 percent of US gross domestic product.22

For the public, LTC is a risk that individuals largely fail to appreciate until they need LTC services. At that time, Medicaid obviates the biggest cost. Each generation sees Medicaid pick up most of the cost, which desensitizes future generations to LTC risk.

Medicaid’s share of LTC expenditures understates the program’s effects on LTC recipients. The easy availability of large Medicaid subsidies crowds out demand for private LTC insurance.23 Medicaid pays LTC providers, on average, 70 percent of private-sector prices.24 Easy eligibility for subsidies, relatively low payments, and Medicaid’s poor oversight of LTC providers creates shortages and reduces the quality of care. By the time individuals need expensive LTC services, it is too late to purchase private LTC insurance that might provide higher-quality LTC.

At the same time, Medicaid allows affluent individuals to avoid the worst scenarios. Nursing homes are eager to accept self-pay residents because they pay higher prices than Medicaid. Financial advisers and elder-law attorneys advise such clients to retain enough cash or assets to purchase entry into higher-quality nursing homes at private-sector prices. Once that “key money” runs out, those affluent individuals can then switch to Medicaid. The nursing home’s revenue falls because it then receives Medicaid prices rather than private-sector prices, but Medicaid rules prohibit participating nursing homes from removing residents just for switching from private payment to Medicaid. Medicaid thus allows affluent enrollees to obtain subsidies for higher-quality LTC than needier enrollees can obtain.

For Medicaid planners, LTC generates big profits from artificially impoverishing affluent clients to qualify them for Medicaid at the cost of imposing higher taxes on lower-income individuals.

Finally, for insurers, LTC is a hopeless challenge. Private LTC insurance companies struggle to sell a product government has been giving away since Medicaid began in 1965.

What Can Policymakers Do?

Policymakers must disrupt this LTC system. Prices for LTC services should reflect the values of consumers and the actual costs of resources, not the preferences of government planners. Market prices would eliminate caregiver shortages and improve access and quality through competition.

To reduce its price distortions, Medicaid must cover fewer recipients. Policymakers can reduce Medicaid LTC dependence while still helping people in need. To accomplish this, Congress can tighten the program’s financial eligibility limits gradually so that the public has time to adjust to a new reality of facing LTC risk. To achieve that objective, Congress could exempt everyone over 55 years of age and anyone already qualifying for Medicaid LTC subsidies from the following changes:

- Keep Medicaid’s treatment of income the same, continuing to require a low-income standard after deducting private medical and LTC expenses from total income. Excess Social Security, pension, and other private income should continue to offset Medicaid’s outlays for a recipient’s care.

- Stop allowing Medicaid applicants to hide unlimited resources by purchasing exempt assets. Instead, treat asset spend-down the same as income spend-down. Limit it to deductions for actual, documented private medical or LTC expenditures.

- Bring seniors’ $14 trillion of home equity into the LTC financing system. Seniors hold enough wealth in home equity alone to solve most of LTC’s many access and quality problems. Medicaid diverts nearly all that wealth from LTC funding. Congress recently set a uniform national Medicaid home equity exemption of $1 million, which increased this exemption in most states.25 Congress should eliminate or vastly reduce Medicaid’s home equity exemption.

- Stop “Medicaid Asset Protection Trusts” and “Medicaid Compliant Annuities” from diverting vast sums of additional private wealth from LTC. These legal gimmicks exclusively benefit Medicaid planning specialists and their affluent clients. Congress should not allow the affluent to raid a program for the needy.26

- Extend Medicaid’s five-year asset-transfer look-back to 20 years.27 Five years is too short a period to prevent intentional, artificial self-impoverishment to qualify for Medicaid LTC subsidies. Medicaid eligibility workers could easily administer a 20-year look-back rule with data from county assessors and recorders, who record home ownership and transfers, respectively. This reform would end one of the most common methods of early Medicaid LTC abuse.

- End Medicaid abuse by the affluent. Today, affluent individuals use “key money” to get government to subsidize red-carpet LTC access that the less privileged cannot afford.28 For the well-to-do, Medicaid subsidizes the best facilities and services to the exclusion of needier groups, including racial and socioeconomic minorities.29 Tightening Medicaid’s income and asset rules would restrict the ability of affluent individuals to engage in this form of Medicaid LTC abuse.

- End Medicaid’s current incentive for states to spend money on able-bodied adults rather than vulnerable enrollees. The incentive to spend money on able-bodied adults is seven times greater than the incentive to spend on other Medicaid enrollees, including disabled and elderly enrollees who need LTC. This disparity naturally encourages states to divert funds from needy LTC recipients to less needy individuals. Congress can correct this disparity by funding Medicaid subsidies for able-bodied adults on the same terms as other Medicaid enrollees.30

- Give states greater flexibility. Ideally, Congress would give each state a fixed Medicaid block grant, with full flexibility on how to spend it.31 Short of block grants, Congress could allow states to experiment with creative ways to do more with less by encouraging and approving waivers that trade substantial reductions in federal funding for more state-level LTC policy flexibility.

These measures would vastly reduce Medicaid LTC caseloads over time, including many of the most expensive cases. The changes could save Medicaid up to $100 billion per year.32

Reform could provide better LTC for all participants. Middle-class and affluent people would no longer be able to qualify for Medicaid LTC while sheltering wealth. Instead, they would purchase higher-quality LTC, including via LTC insurance. They would enjoy greater access across the LTC continuum, from in-home care to nursing home care. With enormous sums of new private financing at market rates, commercial activity would flourish, generating additional tax revenue as more caregivers and LTC providers join the newly profitable sector. By concentrating scarce Medicaid funds on the truly needy, policymakers could improve quality of care for Medicaid LTC recipients.

Obstacles and Solutions

Those who believe catastrophic asset spend-down is the dominant precursor to Medicaid enrollment will excoriate this approach. They will claim incorrectly that the existing LTC system already impoverishes millions, and withdrawing Medicaid subsidies from the affluent will impoverish even more. On the contrary, those most in need and everyone over age 55 would remain eligible. Those who become responsible for their own LTC before qualifying for Medicaid would have time to adjust, prepare, and protect their assets. For those in need, as well as the affluent who lose Medicaid eligibility, these changes could mean better LTC.

The biggest challenge to reinventing LTC in this way is how to awaken the public to the new reality without inciting opposition. How to achieve a transition from current LTC complacency and government dependency to serious personal responsibility and planning is the major obstacle. Families struggling to make ends meet and save for their own retirement may not look kindly at the loss of a government subsidy, even one they do not realize has already been distorting their behavior for the worse. How to relieve them of that burden while simultaneously reducing the government subsidies that have failed everyone so miserably?

The solution is to reprioritize LTC among life’s responsibilities. Government encourages the accumulation of assets but discourages the use of private wealth to fund LTC. Preferential tax treatment for IRAs and 401(k)s encourages people to set aside funds for retirement. Subsidies for mortgages (through the Federal Housing Administration, Veterans Administration, and Department of Agriculture) and down payments, as well as preferential tax treatment of mortgage interest, promote homeownership and the accumulation of home equity. Life insurance receives favorable treatment through tax-deferred growth of cash value and tax-free death benefits. Again, these policies have encouraged seniors to accumulate $14 trillion in home equity and US residents broadly to amass $97 trillion in wealth.

Why should amassing wealth that will pass to heirs take precedence over funding quality LTC for the living? Why should Medicaid force taxpayers to pay for LTC for those who would get it anyway, where subsidies serve no other purpose than to protect the inheritances of those individuals’ heirs? What if public policy were instead to encourage preparing privately for future LTC needs? What might such a policy look like?

Step one would be to educate the public about the abuse of Medicaid by those who treat the program as a late-in-life, wealth-preserving safety net for the middle-class and affluent. Step two would be to inform the public that the current system is coming to an end.

The loss of the implicit subsidy that Medicaid currently provides would spur demand for objective analyses of individuals’ LTC risk and an estimate of the likely cost of the care they may need some day. Research shows that accumulating $70,000 by age 65 is sufficient with average appreciation to cover median paid LTC expenses.33 Individuals may set aside less or more and smooth out remaining risk with varying amounts of LTC insurance, depending on their circumstances. Rather than educate the affluent on how to take advantage of taxpayers, financial advisers and other market actors would help them develop LTC planning goals. Each person could then know what they should set aside to cover their expected LTC needs.

Encouraging every individual to take personal responsibility for LTC risk would not eliminate Medicaid’s back-end exposure to catastrophic risks. There are steps policymakers can take to reduce this risk significantly. In tandem with a 20-year look-back period, Medicaid could make the development and execution of LTC planning strategies no later than age 65 a precondition for any later Medicaid assistance. This strategy would substantially reduce that back-end risk, enabling Medicaid to do a better job for all remaining long-duration recipients.

How can public policy help people achieve their target level of LTC savings without burdening taxpayers? One way could be to change current rules to allow individuals and families to earmark other resources (e.g., retirement savings, home equity, and life insurance) for LTC. Medicaid could make such earmarking a condition of future assistance. In that manner, the things government does to encourage wealth accumulation can fund future LTC needs without impairing families’ current cash flow. Savings that would otherwise pass through inheritance would go to fund higher-quality LTC for the living and create a stronger inducement for younger generations to save, invest, or insure for their own future LTC needs.

Conclusion

It makes little sense that some government policies encourage citizens to accumulate savings while other policies discourage spending this wealth on LTC. Easy access to Medicaid LTC subsidies late in life enables people to ignore LTC risk. As a result, few people plan, save, invest, or insure for LTC early in life, ending up unnecessarily dependent on taxpayers late in life. Medicaid distorts the LTC market by dominating it, offering low-quality care, and causing caregiver shortages and other access and quality problems.

To fix LTC, Medicaid LTC caseloads must decline dramatically. Federal and state policymakers must tighten eligibility by ensuring that recipients actually spend down income and assets for care before becoming eligible. Reducing eligibility would lead those with means to identify their LTC risk and prepare with assets and private LTC insurance.

Those with means would plan for LTC earlier and pay privately for their care when possible, which would reduce the need for and cost of Medicaid LTC subsidies. A smaller Medicaid program could do a better job for the genuinely needy enrollees who remain.

The terrible condition of LTC delivery and financing in the United States is not the result of too little government funding and regulation, but too much. Reconfiguring the carrots and sticks in public policy to redirect vast personal savings toward private LTC financing is the key to improving LTC for everyone, rich and poor alike.

The author would like to thank Michael F. Cannon for his collaboration to craft and edit this article.

Citation

Moses, Stephen A. “Better Long-Term Care for Billions Less,” Policy Analysis no. 1008, Cato Institute, Washington, DC, November 11, 2025.

About the Author

This work is licensed under a Creative Commons Attribution-NonCommercial-ShareAlike 4.0 International License.