Antidumping and countervailing duty (AD/CVD) measures are unable to fix the low-price problem afflicting U.S. steel producers because they amount to no more than a band-aid that can’t heal the wound. Worse, such trade remedy measures do great harm to manufacturing companies by making steel in the United States higher in price than in most of the rest of the world. This tends to make downstream manufacturers less competitive, thus encouraging imports of steel-containing products from other countries.

A better approach would be to take advantage of an underlying economic reality: because the U.S. steel-consuming sector is so much more economically significant than the steel-producing sector, low-priced steel imports provide a substantial net benefit to the U.S. economy. China’s policies encourage the export of steel at artificially low prices, which has the effect of transferring wealth from China to the United States. The United States should change the dynamic of the debate by encouraging China to continue transferring wealth by selling all the low-priced steel it possibly can in this country. That approach is likely to get the attention of Chinese policymakers and hasten the downsizing and restructuring that is so badly needed in that country’s steel sector.

In addition, U.S. statutes should be reformed to specify that AD/CVD duties would enter into effect only when economic analysis indicates that they would improve economic welfare in the United States. Yes, low-priced steel imports may be “unfair” to U.S. steel producers. But the United States should avoid responding to this unfairness with policies that are even more unfair because they impose much larger costs on the steel-consuming sector than any benefits that might accrue to steel producers.

China's Steel Overcapacity Can Benefit the United States

China's "socialist market economy" has been driven far too much by socialist planning and not enough by the actual marketplace. Decisions at various levels of government within China have encouraged undisciplined investments in steel capacity, which have led to a large gap between China's ability to produce steel and the demand for it. Because much of the production increase has been generated by government policies, it is clear that China's steel exports aren't really "fair." However, a lot of things in life aren't fair — it's just necessary to make the best of them.

So the question of interest to policymakers should be: What policy response would allow the United States to make the best of those unfair circumstances, preferably turning them to America's advantage?

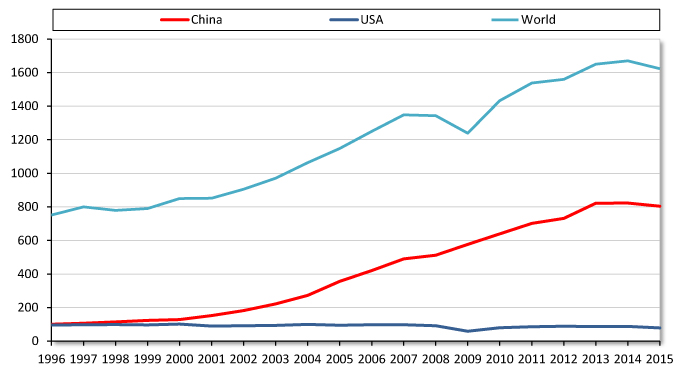

It is helpful to start by reviewing some realities of the political economy of China's steel market. Many Chinese steel mills never would have been built at all if those investors had been subject to the market pressures of a fully open and competitive economy. Earning a positive return on invested capital has not been an important objective for mills that are owned or heavily influenced by governments. As a consequence, capacity has been added for which there is no effective demand, either in China or overseas. Estimates of overcapacity worldwide (most of which is in China) range in excess of 600 million metric tons,1 equivalent to more than a third of annual global steel output.2 (See Figure 1 and Table 1.) Some of that capacity may close in the coming years, perhaps without ever having been operated profitably.

In the near term, however, China appears to be dealing with its unwise steel investments largely by making a second unwise decision — that is, operating many mills at a loss instead of just shutting them down. This is bad for China because it uses resources inefficiently. It also creates political complications for other countries, including the United States. However, the economics of the situation can work to America's benefit. Since China is selling steel for less than it would be worth in an economy guided solely by market forces, U.S. steel consumers are getting a bargain. China's decision to run its steel mills at negative rates of return means, in essence, that China is helping to increase the competitiveness of U.S. manufacturers that use steel as an input. In terms of the underlying economics, China takes the losses and the United States reaps the gains. What's not to like about those circumstances?

Table 1. Largest Steel Producing Countries, Million Metric Tons

Source: World Steel Association.

Figure 1. Crude Steel Production, 1996-2015, Million Metric Tons

Source: World Steel Association.

Trade Remedies Make the Situation Worse

Yes, domestic U.S. steel producers are exposed to unfairly low-priced steel and are understandably unhappy. Their traditional response has been to seek relief from troublesome imports, primarily by filing antidumping and countervailing duty (AD/CVD) petitions. There are two reasons that this approach does not serve the best overall interests of the United States.

One is that today's steel market for commodity products is so far out of balance that trade remedy measures simply can't bring the U.S. industry back to profitability. The global supply of commodity steel products is so large that prices are low worldwide. No matter how many trade remedy band-aids are placed on that wound, they won't raise U.S. prices sufficiently to stop the financial bleeding.

The other shortcoming of AD/CVD orders is that — even if they could provide some help to U.S. steel manufacturers — they would do great harm to downstream U.S. firms that use steel as an input. True, U.S. steel producers employ tens of thousands of people. But steel production adds far less value to the U.S. economy and employs far fewer people than do downstream manufacturers.

Data from the Bureau of Economic Analysis (BEA) at the Department of Commerce indicate that value added by "primary metal manufacturing" amounted to $59.7 billion in 2014.3 (Note: Primary metal manufacturing [NAICS 331] includes nonferrous metals, such as copper, aluminum, magnesium, lead, tin, silver, and gold, so is much broader than the steel industry.) Downstream manufacturers that utilize steel as an input generate value added of $990 billion, more than 16 times larger than primary metal industries. The disparity in employment also is more than 16 times greater. Primary metal manufacturing employed 399,000 people in 2014.4 Downstream manufacturers employed 6.5 million. (Employment by U.S. steel producers is somewhere in the neighborhood of 100,000.)

The point is not that steel production is a small and insignificant industry, because clearly it is not. Rather, the point is that the problems of the steel industry need to be kept in perspective. It would be a poor policy choice to attempt to protect steel producers in ways that do much greater harm to steel users.

One of the sad realities is that AD/CVD orders can make the United States a relatively high-priced island in a world awash with lower-priced steel. Not having access to competitively priced inputs can lead quickly to sales losses for companies that manufacture goods containing steel. Overseas firms that benefit from lower costs will be able to export products to the United States and undersell U.S. manufacturers. So imposing trade remedies is a great way to reduce the economic welfare of the United States, thus making this country poorer.

One example might be Carrier, the company that recently announced it would shift manufacturing air conditioners from two plants in Indiana to Monterrey, Mexico. This decision, which will lead to the loss of 2100 jobs, has inspired commentary in the presidential campaign. The company's official statement does not attribute the change specifically to higher U.S. prices for key inputs covered by AD/CVD orders. However, the statement does say, "This move is intended to address . . . ongoing cost and pricing pressures."5 It seems likely that some of those cost pressures relate to U.S. trade remedies, 19 of which restrict imports of various steel products from China. (Not all of those steel products would be used in the manufacture of air conditioners.) Other AD/CVD orders apply to imports of copper tubing, which is an important component of air conditioning systems, as well as aluminum extrusions. If the United States wishes to create a more favorable business climate for manufacturers, a good start would be to revoke AD/CVD orders that raise the costs of their components. These are costs that Carrier largely can avoid by moving operations to Mexico.6

A Better Approach

What should be done instead of using trade remedies? U.S. policymakers should take advantage of fundamental economics. China's decision to export steel for less than it is worth has the effect of transferring wealth from China to the United States. As a practical matter, the best way to encourage China to downsize and restructure its industry would be to reframe the debate by communicating the following message to the Chinese government:

Thank you for transferring so much wealth from China to the United States by selling low-priced steel! Please continue doing it! Is China willing to sign ten-year contracts guaranteeing that wealth transfers will continue?

By radically changing the terms of the discussion, this approach has a decent prospect for getting the Chinese quickly to rethink what they have been doing. The current U.S. approach is to complain to them about how much their exports are hurting American steel producers. Instead, that argument should be turned on its head by thanking them for helping to strengthen the competitiveness of the much larger U.S. steel-consuming sector.

Adopting that strategy is not only the right thing to do based on economics, it also would tend to get the attention of Chinese policymakers in a genuinely constructive way. China’s senior leaders may find it challenging to explain to their people why they are continuing to allow below-cost steel to be sent overseas to the great benefit of the United States and other countries. Temporarily maintaining employment in Chinese steel mills may be nice, but at the cost of subsidizing undeserving Americans? That’s probably not a winning political argument, even in China.

Implications for U.S. Steel Producers

Would removing all AD/CVD restrictions against steel imports sound the death knell for the U.S. steel industry? Fortunately, no. Steel producers understand that their markets tend to be cyclical. When prices are at cyclical lows, many U.S. steel companies experience financial losses. This is not a new phenomenon. Experience in previous periods of low prices indicates that capacity utilization rates for the industry as a whole tend to decline. Some mills producing commodity products may close for a few months, perhaps longer. There may be restructuring or consolidation among firms. These changes — especially in combination with industry downsizing and restructuring in China and other countries — would lead relatively promptly to restoring a balance between steel supply and demand that would allow profitable operation of U.S. mills.

It likely would be preferable to both employees and stockholders of steel companies to get past the bottom of the cycle as quickly as possible. There would be little joy from a prolonged downturn that could be expected in response to an ongoing series of AD/CVD orders imposed in a vain attempt to protect the U.S. steel industry from adverse market circumstances. Continuing on the traditional trade-remedy path likely would encourage Chinese leaders to resist reforms. Why should they suffer political costs to change policies in order to make the United States happy? By shifting the dynamic and encouraging China to continue exporting a large quantity of low-priced steel, the United States has a far better chance to get China to make badly needed adjustments in its industrial policies.

It is important to understand that the nature of the U.S. marketplace also provides some degree of protection to domestic steel companies, especially those producing high-quality and specialty steels. High-end items are more difficult to produce and are higher in price than commodity grades. The trend in recent decades has been for the U.S. steel industry to rely less on the sale of commodity products, instead moving toward manufacture of higher-value grades of steel. Specialty steels are required by customers for certain well-defined uses. Such customers will only use steel that has passed qualification tests in advance, so tend to have long-term relationships with suppliers. Manufacturers with exacting requirements for their steel inputs often are reluctant to attempt to qualify producers that previously have not been business partners, especially if those potential suppliers are located far away in other countries. Manufacturers find it somewhat comforting to have major suppliers located relatively nearby so that transportation logistics are not excessively complicated. In other words, realities of producer-customer relationships provide the U.S. steel industry with partial insulation from overseas competition.

Reform Trade Remedy Statutes

U.S. steel producers may not be comfortable with an open-market approach. The challenge to them is to outline an alternative policy that would do a better job of improving U.S. economic welfare. It is doubtful they can do so. Certainly it would be difficult for the U.S. steel industry to make a compelling argument that their economic interests are somehow more important than those of companies that require steel as an input for their value-added manufacturing processes.

The optimal policy response would be to reform U.S. trade remedy statutes by adding a new requirement: AD/CVD duties only should be imposed if economic analysis indicates that doing so would increase economic welfare in this country. This would be an elaboration of the “public interest” test applied by some other nations as they consider whether to impose AD/CVD measures.

Fortunately, adding such a requirement to U.S. law would not pose a substantial administrative burden. Economists on the staff of the U.S. International Trade Commission already have access to relevant data in the injury phase of AD/CVD investigations. They also have the necessary analytic tools and experience to provide this analysis. The statute should be changed to instruct ITC commissioners to consider the broad economic welfare effects of proposed AD/CVD duties and to vote in the affirmative only when those duties will redound to the net benefit of the United States.

People on both sides of this issue should be able to agree that the U.S. government should avoid policy responses that do more harm to the economy than any harm that could be done by unfairly priced imports. It is important to ensure that the policy “cure” isn’t worse than the “disease” of low-priced steel. The goal should be to pursue policies that serve the best overall interests of the United States.

Notes

1. Notes “Tata Steel: No, Thank You,” The Economist, April 2, 2016, www.economist.com/node/21695872/.

2. “Monthly Crude Steel Production,” World Steel Association, January 25, 2016, https://www.worldsteel.org/dms/internetDocumentList/steel-stats/2015/Crude-steel-production-Jan-Dec-2015-vs-2014_/document/Crude%20steel%20production%20Jan-Dec%202015%20vs%202014.pdf.

3. “Value Added by Industry,” Bureau of Economic Analysis, U.S. Department of Commerce, November 5, 2015, http://www.bea.gov/iTable/print.cfm?fid=928DEDAE7553EBE540634807A5540C6A1C7978C144702974BD43F0538F257772B50F6E8A941AE6A12DCD641CC0E5EFF419242D22DB27361F753F66E82FDBDA46.

4. “Full-Time and Part-Time Employees by Industry,” Bureau of Economic Analysis, U.S. Department of Commerce, August 6, 2015, http://www.bea.gov/iTable/print.cfm?fid=718A9A5150C52C20743F8882F711BA94B63DFA6A263656FABBCE94FA5A8705C8CF5AFBD927E63BB81584B114DE4F013CDD922DCFADAA9BE5CF8972E98CFDA979. (Steel consuming manufacturers are: fabricated metal products; machinery; computer and electronic products; electrical equipment, appliances and components; motor vehicles, bodies and trailers, and parts; other transportation equipment; furniture and related products; and miscellaneous manufacturing.)

5. Carrier, “Carrier to Relocate Indianapolis Manufacturing Operations,” news release, March 2, 2016, https://www.carrier.com/carrier/en/us/news/statements/.

6. Daniel Ikenson, “Economic Self-Flagellation: How U.S. Antidumping Policy Subverts the National Export Initiative,” Cato Institute, May 31, 2011, http://www.cato.org/publications/trade-policy-analysis/economic-selfflagellation-how-us-antidumping-policy-subverts-national-export-initiative. (Pages 14–17 provide examples of damage done by antidumping measures to U.S. firms using magnesium and hot-rolled carbon steel.)

About the Author

This work is licensed under a Creative Commons Attribution-NonCommercial-ShareAlike 4.0 International License.