Certain ideas dominate debate about the state of competition in the United States: that market shares for top firms are rising, that consumers and competitors are suffering, and that a lack of enforcement of antitrust laws is a key cause of these difficulties.

Such sentiments echo through the 2020 Democratic presidential primary. In one recent TV debate, Sen. Elizabeth Warren (D‑MA) vowed not to “let a handful of monopolists dominate our economy,” while Sen. Amy Klobuchar (D‑MN) claimed we are living through “another gilded age.” Sen. Bernie Sanders (I‑VT) expressed the predictable policy conclusion: “We need a president who has the guts to appoint an attorney general who will take on these huge monopolies.”1

The impression given is that America’s economy is besieged by a generalized monopoly problem.2 Fewer firms are said to be dominating industries, enjoying rising markups of price over cost. Consumers are supposedly suffering higher prices and less innovation as a result of these companies’ growing market power. Competitors, meanwhile, allegedly struggle to stay afloat because of unfair behavior by these behemoths. And all this, scholars and politicians tell us, is due to a failure to enforce or strengthen antitrust laws to prevent anti-competitive behavior.3

Such a narrative, though, is highly challengeable. The measures of concentration taken as proxies for the health of competition often do not reflect the dominance of top national firms in actual relevant product markets. Local measures of industry concentration, contrary to national trends, appear to have fallen. What’s more, recent evidence suggests that jumps in national concentration have been driven by the strength of highly productive market-leading firms, which are expanding, not constraining, output—not what one would expect from firms with monopoly market power.

Economists have long known that increasing concentration need not signify rising market power in an industry. In fact, it can be driven precisely by the competitive process—for example, by consumers opting to buy from more-productive and more-innovative market leaders that have found cost-effective ways to serve more markets. That rising market concentration has also occurred in Europe, which applies competition law very differently than the United States does, suggests that weak enforcement of U.S. antitrust laws is not the likely cause of any rising concentration we have seen.

Rising National Concentration?

In 2016, President Barack Obama’s Council of Economic Advisers (CEA) kicked off the narrative about rising market concentration across the U.S. economy.4 Examining changes in the revenue share of the largest 50 firms in very broad sectors between 1997 and 2012, the CEA’s analysis found that concentration had increased in 10 of 13 of those industries.

The analysis was careful to point out that rising concentration need not be evidence of weakened competition or harm to consumers. But the findings were not treated with such caution in subsequent reporting. The presentation of the analysis didn’t help—the table presenting the results appeared in a section titled “Indicators of Declining Competition.”

The industrial groupings presented, though, were clearly absurd for thinking about meaningful product-market competition.5 Industrial classifications as broad as retail meant, in principle, assessing firms such as Walmart, IKEA, McDonald’s, Foot Locker, and car dealers as if they were meaningfully competing. Other sectors were also as extensive in scope as transportation and warehousing, finance and insurance, and utilities.

Former deputy assistant attorney general for economics Carl Shapiro identified other problems with the analysis.6 Even if it had used more-targeted industrial classifications, a 50-firm concentration ratio would not be particularly informative about the health of competition, given that (for genuinely national markets) that’s already a lot of firms.

Economic Census data, as used by the CEA, also only include production that takes place domestically. Given that imports of manufactured products have grown massively in the time frame examined, the CEA methodology risks making U.S. product markets seem much less competitive than they are. Google chief economist Hal Varian gives the example of the assembled-smartphones sector.7 The only U.S. company that assembles them in the United States is Motorola. Under the CEA methodology, the assembled-smartphones industry would appear to have a 100 percent concentration ratio despite the obvious import competition.

Despite these problems, though, another more granular analysis has indeed found upward trends in national concentration measures across industries. In a 2017 paper, economist David Autor and others assessed changes in concentration for 676 four-digit industries between 1982 and 2012 using data from the Economic Census.8 These industries were drawn from six broad sectors (manufacturing, retail trade, wholesale trade, services, utilities and transportation, and finance) and were assessed using three concentration measures (the top 4 firm sales share, the top 20 firm sales share, and the Herfindahl-Hirschman Index).

Autor and others concluded that “there has been a rise in sales concentration within four-digit industries across the vast bulk of the U.S. private sector.” This confirms findings of other studies: economists Gustavo Grullon, Yelena Larkin, and Roni Michaely, for example, found that concentration levels had increased in more than 75 percent of industries in the past 20 years.9

Though industries have become more concentrated on average, the work done by Autor and others shows that concentration measures examining the top 20 or fewer firms in any industry tend to show bigger jumps in concentration than broader measures. This shows that findings of higher concentration are being driven by the very largest firms becoming relatively larger than before. Interestingly, Autor and others also found that the leading firm in any given industry tends to operate in fewer other discrete four-digit industries today than it did in the 1980s. In other words, top firms tend to be increasingly specializing to core product markets (Amazon is the exception rather than the rule).

In sum, problematic as they are as proxies for product-market competition, measures of national concentration seem to have risen modestly to significantly among most industries over the past two to three decades, driven by the very biggest firms, which tend to be more focused on narrower industries than they were before.

Falling Local Concentration

Unfortunately, even these narrower industrial classifications at a national level may not be particularly helpful as proxies for the health of real-world competition. In order to get a grip on that, one must first define the relevant product market and its geographical contours. In doing so, it becomes obvious that many real markets are incredibly local, not national. This is particularly true in retail, which, according to much analysis, has seen the largest rise in concentration of any major sector.

Consider the market for health and personal care products, such as over-the-counter drugs or shampoos. A consumer looking to purchase them might go to a local CVS, Walmart, another supermarket, or an independent pharmacy or order online from Amazon or an independent seller. A high measure of national concentration of the top four firms in the health and personal care products sector says nothing about the meaningful competition between companies in any individual locale.

Suppose Starbucks opened a new outlet in a small rural town, entering a geographical market that had contained only a local café and a bagel store that also sold coffee. Meaningful competition would rise in this market, with the choice for consumers of where to purchase coffee increasing. But the national concentration measure of limited-service restaurants would probably go up, reflecting the addition to Starbucks’s already large national footprint. In other words, rising national concentration might be driven by the same trends driving falling local concentration—an increase in the number of competitors in new localities.

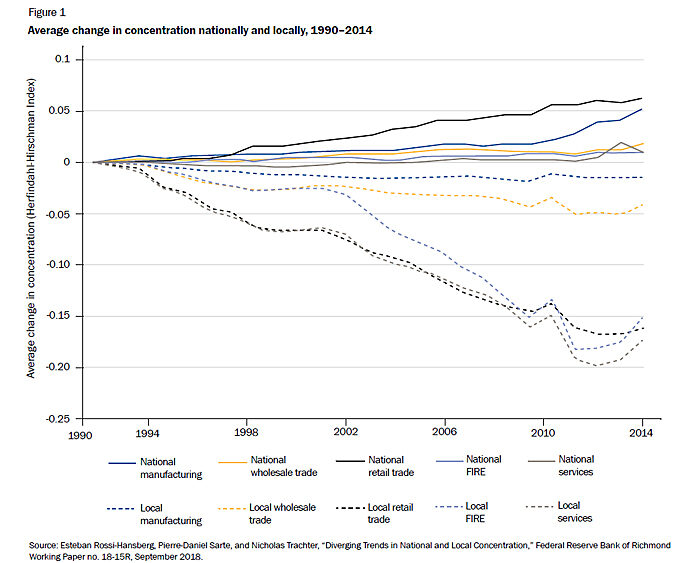

Good evidence suggests that this type of story has actually been observed across the U.S. economy. A 2019 report by Princeton University’s Esteban Rossi-Hansberg and the Federal Reserve Bank of Richmond’s Pierre-Daniel Sarte and Nicholas Trachter confirmed that national product-market concentration had increased between 1990 and 2014. But it found that in sectors accounting for 72 percent of employment and 66 percent of sales, concentration fell in narrower geographic-market territories, such as urban areas, counties, or ZIP codes (see Figure 1).10

For example, Rossi-Hansberg, Sarte, and Trachter found that when Walmart opens a new store, local concentration tends to fall at a ZIP-code level, indicative of more competition. A new Walmart store, on average, increases the total number of local establishments by 0.75 (showing that in some areas Walmart replaces existing firms, but on average tends to add to the number of firms).11

All this suggests that the observed increases in national concentration in the past two to three decades have been driven in part by large enterprises expanding into new local markets. The rising national concentration that we hear so much about might therefore be indicative of more, rather than less, firm competition at the local level. The concern about weak antitrust policy driving higher concentration may be completely invalid.

The Rise of Superstar Firms

Economists have long known that concentration measures are hugely problematic as guides to competition. In fact, the higher national concentration measures we have seen in many industries may themselves be the result of healthy market competition.

In the past two years, a number of papers have pointed in that direction. Economist Sharat Ganapati’s work, for example, found that rising industry concentration was associated with higher productivity and real output growth but not with rising prices.12 This is not what one would expect if we were facing a situation of anti-competitive monopoly power—where firms would be expected to cut output and raise prices.

Increasingly, economists are developing models of “superstar firms” in the modern economy that might help explain the trends of rising national concentration, falling local concentration, rising markups, and falling labor income share. The basic idea is that more strenuous global competition and changing technologies are enabling highly productive firms to dominate more than before, not least by expanding into new markets.

Economists Rossi-Hansberg and Chang-Tai Hsieh’s version of this thesis has been called “The Industrial Revolution in Services.”13 They examine how in services, retail, and wholesale trades, top firms are increasingly those that have invested in new information technology—this comes with high fixed costs but with the benefit of reducing the marginal costs of standardization.

These productive investments allow superstar firms to capture more market share by serving more locations cost-effectively. The economists highlight the Cheesecake Factory as an example. The company has invested in technologies that help with staff management, food purchasing, and menu adaptation, allowing them to roll out menu items nationwide in just seven weeks.

Hospital chains and other service, retail, and wholesale industries are seeing market leaders proliferate geographically too. Employment is rising in industries that are becoming more highly concentrated nationally, suggesting that this isn’t a situation of monopoly power constraining output and raising prices. Instead, what we’re seeing is productive firms serving more places—hence the associated fall in local industry concentration. Rossi-Hansberg and Hsieh estimate that a full 93 percent of the growth in concentration across national industries comes from large firms serving more localities.

If this were true, we would expect to see rising national concentration of industries being driven by a relative reallocation of output toward highly productive, innovative firms. This is exactly what the work done by Autor and others appears to show. They present evidence that there is a significant and positive relationship between the growth of concentration and total-factor productivity in manufacturing industries. In fact, for all six of the broad sectors they examine, they likewise find that “the industries exhibiting rising concentration are more dynamic as measured by innovative output and productivity growth.”14

As economist Timothy Taylor has noted, firms engaging in big investments that lower their marginal costs may enjoy rising markups of price over marginal cost while also seeing a decline in their labor intensity.15 As these firms capture greater market share, industries as a whole will therefore see greater national concentration, rising markups, and falling labor shares—all trends that pundits, economists, and politicians have been worried about. But this will have been driven by positive trends: new technology facilitating more-aggressive competition, with markets facilitating leading innovators to obtain greater market share.

An Antitrust Explanation

In theory, then, the higher national concentration we see alongside rising markups in many U.S. industries over the past two to three decades could be evidence of worrying anti-competitive consolidation, or it could be a consequence of competition in a world of globalization and technological change. But the evidence—particularly that industries with higher concentration tend to see robust productivity growth—increasingly points to the latter.

There are other reasons to doubt the commonly held view that weak U.S. antitrust legislation or enforcement is to blame for rising concentration. Autor and others show that the broad patterns of rising national industry concentration and the phenomenon of superstar firms are common among members of the Organisation for Economic Co-operation and Development, including those in the European Union, despite big differences in the application of antitrust and competition law.

A skeptic of this positive explanation of rising national concentration might say, “OK, that may explain the trends of rising concentration in some markets. But, surely, in competitive markets, firms wouldn’t enjoy sustained higher markups of price over cost.” In other words, shouldn’t a competitive market see markups from leading firms driven down quickly as other competitors or new entrants adopt any new cost-effective technologies? Economists might worry that firms that were initially innovative, having obtained a market-leading position, are now “rigging” the market to their own ends—and so are still benefiting from lax antitrust enforcement after initial consumer welfare-enhancing behavior.16

But Varian posits a simpler explanation: diffusion of the best technological and organizational practices in an industry takes time, particularly in industries where demand is constrained. Consumers are currently enjoying more choices as a result of superstar firms’ innovations. But they will not experience the full benefits of lower prices enabled by these productive improvements until the best technologies and practices are more broadly adopted.

Conclusion

Democratic presidential candidates have jumped on the ideas that American industries are becoming less competitive, that consumers and competitors to dominant firms are suffering, and that anti-competitive behavior facilitated by weak antitrust enforcement is to blame.

Yet increasing evidence suggests that rising national concentration among industries may not be reflective of reduced competition in relevant markets or reflect harm to consumers’ welfare. Instead, economists more frequently see rising national concentration as a consequence of globalized competition in which lumpy investments can allow leading firms to productively serve more local markets.

About the Author

This work is licensed under a Creative Commons Attribution-NonCommercial-ShareAlike 4.0 International License.