It is widely believe that aging populations and falling birth rates represent one of biggest global challenges for long-term economic stability.

How can a nation prosper, after all, if there are more and more old people over time and fewer and fewer workers? Don't these demographic changes put every-growing fiscal burdens on a shrinking workforce to support the elderly, leading to crippling tax burdens and/or enormous levels of debt?

In most cases, there are no good answers to those questions. So it is quite likely that many nations will face serious economic and fiscal challenges, as estimated by international bureaucracies such as the International Monetary Fund, the Bank for International Settlements, and the Organization for Economic Cooperation and Development.

Here are some charts1 showing the age profile of the world's population in both 1990 and 2100. As you can see, demographic changes are turning population pyramids into population cylinders.

See figure 1.

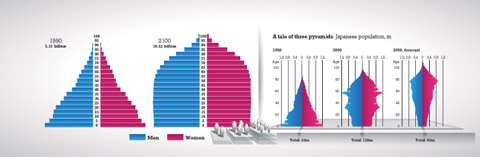

While the charts show the entire world, industrialized nations are facing even more dramatic population challenges. Consider what is happening to Japan. Over a 55-year period, a population pyramid turned into a population cylinder. And by the year 2050, something resembling a mixed pyramid/cylinder will return, but it will be upside down. See figure 2.

No wonder Japan has the most debt among all developed nations, both explicit and implicit, compared to economic output. Official government debt already is well above 200 percent of GDP, but that number is dwarfed by the unfunded liabilities of Japan's entitlements.

The United States has the dubious honor of having the largest absolute amount of explicit and implicit debt. According to very reasonable estimates, the unfunded liabilities of American entitlement programs are more than $100 trillion. Some well-respected economists even put the number higher than $200 trillion.

But the goal of this analysis isn’t to pick on Japan or the United States. The real issue is that virtually every industrialized nation is undergoing demographic changes that will produce some very painful fiscal consequences.

The “funded” pension revolution

Notwithstanding the depressing overall outlook, there are jurisdictions, such as Singapore and Hong Kong that are in reasonably good shape even though their populations rank among the nations with the lowest levels of fertility and longest life expectancies.

And other nations, including Sweden, Australia, Switzerland, and the Netherlands, have much smaller long-run challenges than other industrialized countries with similar demographic profiles.

Mandatory pension savings is a key reason why some jurisdictions have mitigated a demographic death squeeze. Whether they rely on occupational pensions, individual accounts, or even central provident funds, the common characteristic is that workers automatically set aside a portion of current income so it can be invested in some sort of retirement vehicle. Over several decades, this results in the accumulation of a substantial nest egg that then is used to provide retirement income.

These “funded” systems are in contrast to the “unfunded” retirement arrangements, such as America’s Social Security system, that simply rely on tax payments from workers to finance the retirement of current retirees. Often known as “pay as you go” plans, such arrangements can work so long as countries have population pyramids featuring ever-growing numbers of workers and smaller cohorts of retirees.

For advocates of funded pension systems, there is good news and bad news. The good news is that there has been a dramatic increase in jurisdictions that have adopted some form of private retirement system. Equally remarkable, there’s been support for this type of reform from places such as the World Bank, which generally have not been seen as hotbeds of pro-market reform.

Data from the World Bank confirms the growing number of nations with funded mandatory systems — sometimes referred to as “second pillars” in contrast to pay-as-you-go “first pillars” operated by governments — as well as the number of people covered by these new retirement structures. Chile was an early pioneer in the shift to funded systems, under the leadership of José Piñera more than 30 years ago. And if imitation is the highest form of flattery, Piñera launched a very popular wave of reform.

As of 2005, there were about 30 nations with some form of mandatory retirement savings, according to the U.S. Social Security Administration.

While this is impressive growth, the bad news is that mandatory private retirement systems still only cover a small fraction of the world’s workers. The vast majority of workers with retirement plans are compelled to participate in pay-as-you-go government schemes.

Asset accumulation

Discussions of private retirement regimes often revolve around the implications for government and personal finances. That’s understandable since politicians care about the money they control and households focus on the money they control. But there are broader economic ramifications.

Economists have been concerned about a triple-whammy caused by traditional tax-and-transfer retirement schemes. First, payroll taxes and other levies discourage labor supply during peak working years. Second, the promise of retirement benefits undermines a very significant incentive to save.

Third, the provision of retirement benefits discourages labor supply once a worker reaches retirement age.

Though it’s worth noting that payroll taxes are not as damaging as income taxes since workers will perceive (to varying degrees, depending on system design) that some portion of the tax will generate future benefit payments — sort of a nominal form of deferred compensation. Moreover, retirement benefits can be structured so that there is only a modest impact on labor supply.

But even with caveats, pay-as-you-go systems tend to have adverse economic effects. Systems based on private savings, by contrast, have very little economic downside. Workers are compelled to save and invest some portion of their income, but all of that money will be correctly seen as deferred compensation.

There presumably will be no negative impact on labor supply as a result, either during peak working years or during traditional retirement years.

Perhaps equally important, second-pillar systems boost national savings, which means more funds available to finance productive private-sector investment.

Almost all the leading countries have some form of mandatory retirement savings. To be sure, some people will engage in less voluntary savings because of mandatory retirement systems, so it would be an exaggeration to say that every penny in a second-pillar system adds to the pool of capital. But there surely is a significant net increase in national savings.

And additional savings will lead to deeper capital markets and a more robust financial sector, so the secondary economic effects also will be positive.

Risks

Mandatory private retirement systems are not a panacea. A nation with bad fiscal policy, excessive regulation, protectionism, and corruption is not going to enjoy good economic performance simply because of one reform, regardless of its desirability.

There’s also a danger that politicians may decide to loot the wealth accumulated in personal retirement accounts. That’s already happened in Argentina and Hungary, and it most recently happened in Poland.

This is why, in an ideal world, mandatory retirements systems should be designed so that workers can have some assets offshore, preferably managed by a non-domestic company. That provides at least some protection from expropriation.

One common criticism is that funded retirement systems are “too risky” because of volatility in financial markets. There is risk in such systems, of course. Some workers will do better than others for no other reason than being lucky in the timing of when they enter the labor force and leave the labor force.

There’s also risk in that some fund managers will do better than others when investing the money that workers set aside for retirement.

But these risks are very manageable, particularly when looking at the performance of financial markets over an average worker’s forty-plus years in the labor force. Indeed, Michael Tanner of the Cato Institute found that even workers who retired right after the stock market crash still would have been better off with personal accounts.

The extreme argument is that personal retirement accounts might be too risky if there is a stock market crash with no recovery, accompanied by a deep economic depression. To be sure, there are very pessimistic scenarios showing that workers in a funded system might get less than what is promised with government-run pay-as-you-go schemes.

But there’s a big difference between what a government promises and what it can deliver. If there’s an economic collapse that leads to very bad returns in a funded system, that economic collapse also wipe out any chance that a government will pay promised retirement benefits.

Transition

The other common critique of mandatory retirement savings is that shifting to such a system is unworkable because the payroll taxes that workers would shift to a personal account are the same funds that are used in pay-as-you-go systems to finance benefits to current retirees.

So if younger workers are allowed to shift their payroll taxes into personal accounts, policy makers would need to find lots of money over several decades (trillions of dollars in the American example) to fulfill promises made to existing retirees as well as workers that are too old to get much benefit from personal accounts.

This critique is completely accurate. After all, you can’t spend the same dollar twice. So it would be very costly, during a transition period, to move to personal accounts.

But here’s the catch. While trillions of dollars are needed to finance the transition to a system of personal accounts, it’s also true that trillions of dollars are needed to bail out the current system. In other words, the existing system puts nations such as the United States into a fiscal hole.

The real question is figuring out the best way to climb out of that hole. From a long-term fiscal and economic perspective, personal accounts are the more attractive option.

Conclusion

Funded pension systems obviously don’t fully solve long-run fiscal challenges. Almost all nations have government-run, pay-as-you-go healthcare schemes for older residents and these often represent even bigger fiscal burdens than retirement programs.

Moreover, a well-functioning pension system obviously won’t yield big benefits if a nation’s economy also is burdened by an unstable monetary system, a protectionist trade regime, an ossified regulatory structure, or rampant corruption.

Very few if any economic reforms are an elixir for permanent prosperity. That being said, retirement systems based on mandatory saving are a win-win-win for workers, governments, and national economies.

About the Author