During the fall of 2009, George Papandreou headed the ticket of the Panhellenic Socialist Movement, known by its acronym PASOK, against the then-governing conservative party, New Democracy, in the Greek national elections. Papandreou ran on a platform that featured highly expansive fiscal spending. During a press conference on September 13, 2009, he was asked where he would find the money to fund his party’s spending proposals. His answer was that given in the above quotation, by which he meant that Greece had abundant fiscal space to increase government spending; he believed that tax revenues could be sharply raised through stricter enforcement of laws against tax evasion. On October 4, PASOK won a landslide electoral victory, garnering 43.9 percent of the popular vote, compared with 33.5 percent for the second-place, incumbent New Democracy party, with the result that Papandreou became Greece’s prime minister. In the following months, a sovereign-debt crisis erupted in Greece that, within a year, engulfed much of the euro area through contagion. In November 2011, Papandreou resigned the premiership, becoming the first Greek prime minister in almost 50 years to be forced out of office by his own cabinet. An article in the Financial Times, reporting on his ouster, stated: “George Papandreou will be remembered by Greeks with more than a trace of bitterness as the man who smilingly declared ‘the money’s there’ ” (Hope 2011). In the next Greek elections, held in June 2012, PASOK won only 12.3 percent of the vote.

In her influential book The Deficit Myth, Stephanie Kelton advances the view that the money could have been there for Greece if the country had not been part of the euro area. In particular, Kelton provides a diagnosis of what went wrong in Greece and a roadmap to the economic promised land for countries that follow her advice. Greece, it turns out, is Kelton’s poster child for the way not to enter the promised land. “We all know what happened in Greece,” she writes (Kelton 2020: 81). Greece, according to Kelton, began its journey into turbulent economic waters when it abandoned its national currency, the drachma, in 2001 and adopted the euro. By doing so, the country gave up its monetary sovereignty. It no longer was able to print its own currency to pay its debts, with the result that—well, “we all know what happened.” Or do we? The problem is that Kelton does not know what happened.

If Greece is Kelton’s poster child for the way not to run an economy, Kelton has become the poster child of the group of economists who advocate Modern Monetary Theory, or MMT. Kelton’s The Deficit Myth made the New York Times bestseller list (for hardcover nonfiction) and has been the object of numerous reviews—including in this journal.1 MMT itself has been embraced by several high-profile politicians.

This article is an assessment of what went wrong in Greece through the lens of Kelton’s exposition of MMT. To set the stage, I first describe the central characteristics of MMT. As I will document, Kelton asserts that MMT builds on the idea of functional finance, developed in the 1940s by Abba Lerner. Functional finance views the issue of a balanced budget as of secondary importance; the primary purpose of functional finance is to ensure noninflationary full employment. Next, I provide a narrative of what went wrong in Greece. As I show, the origins of the Greek crisis had nothing to do with the loss of monetary sovereignty. Greece had monetary sovereignty in the 1980s but nevertheless found itself ensnared in financial crises because it engaged in fiscal profligacy. The fiscal profligacy led to high inflation, something that, as we shall see, Kelton says will not happen to a country that has monetary sovereignty. After Greece entered the euro area in 2001, the country acted as though it had unlimited fiscal space, resulting in the outbreak of the financial crisis in 2009. The common denominator of the crises of the 1980s and the 2009 crisis was the absence of fiscal discipline.

I then show that MMT is, in fact, a combination of two ideas developed in the 1940s: Lerner’s idea of functional finance and a proposal developed at the University of Chicago by Henry Simons, Lloyd Mints, and Milton Friedman. Like Kelton, the Chicago economists believed that fiscal deficits should be entirely backed by money creation. The Chicago proposal, however, was formulated with the objectives of disciplining fiscal policy and limiting the amount of money that could be created. The proposal aimed to attain price stability at full employment. In contrast, MMT provides no fiscal discipline and no limit on money creation, despite Kelton’s claims to the contrary. Moreover, the Chicagoans were concerned that discretionary policies can be destabilizing in light of long and variable lags. Consequently, their policy framework was rules based. As I document, functional finance’s failure to take account of the destabilizing properties of discretionary policies provided the basis of a highly critical assessment of Lerner’s functional finance proposal by Friedman.

MMT: Core Characteristics

At the “heart of MMT,” writes Kelton (2020), is the “distinction between currency users and the currency issuer” (original italics, p. 18). A currency issuer is a country that has monetary sovereignty. Four conditions, she contends, are needed to attain monetary sovereignty: (1) a country must issue its own currency (p. 19); (2) it must borrow in that currency (p. 145); (3) it must let its currency float against other currencies (p. 145); and (4) the currency in question must be inconvertible—that is, it is “also important that [countries] don’t promise to convert their currency into something of which they could run out (e.g., gold or some other country’s currency)” (pp. 18–19). Countries like the United States, Japan, the United Kingdom, Australia, Canada, and “many more,” Kelton asserts, are currency issuers. These countries “never [have] to worry about running out of money.” The United States, for example, “can always pay the bills, even the big ones” (p. 19) because it can always print enough dollars to pay those bills.2 Kelton writes: “Congress has the power of the purse. If it really wants to accomplish something, the money can always be made available … spending should never be constrained by arbitrary budget targets or a blind allegiance to so-called sound finance” (p. 4). Fiscal deficits, she argues, are not a problem so long as the deficits do not lead to inflation (more about that shortly). “This book,” Kelton audaciously asserts, “aims to drive the number of people who believe the deficit is a problem closer to zero” (p. 8).

The situation for currency users is very different. The countries that fall into this category have either (1) fixed their exchange rates, “like Argentina did until 2001,” or (2) “taken on debt denominated in a foreign currency, like Venezuela has done,” or (3) abandoned their national currency, as “Italy, Greece and other eurozone countries,” have done (p. 19). Those countries do not have access to the printing press to backstop their debts. Thus, we are told: “The US can’t end up like Greece, which gave up its monetary sovereignty when it stopped issuing the drachma in order to use the euro” (p. 19).

As mentioned, Kelton (pp. 60–63) acknowledges that MMT is guided by the idea of functional finance, developed by Lerner. Let’s take a look at what Lerner had to say about functional finance. In his 1944 book, The Economics of Control, Lerner argued that the government should not hesitate to incur fiscal deficits required to achieve full employment. If the attainment of this objective entails persistent fiscal deficits (or surpluses), so be it. The size of the national debt, Lerner argued, is not important: “The [size of the] debt is not a burden on posterity because if posterity pays the debt it will be paying the same posterity that will be alive at the time when the payment is made. The national debt is not a burden on the nation because every cent in interest or repayment that is collected from the citizens as taxpayers to meet the debt service is received by the citizens as government bondholders” (Lerner 1944: 303).3 Likewise, argued Lerner, “the interest on the debt is not a burden on the nation” because those payments “are merely transferred to the recipient from taxpayer or from new lenders, and if it should be difficult or undesirable to raise taxes the interest payment can be met, without imposing any burden on the nation as a whole, by borrowing the money or printing it” (Lerner 1944: 303).

Kelton believes that Lerner “turned conventional wisdom on its head,” since Lerner showed that the size of a nation’s debt and its fiscal position are unimportant. Kelton states: “Instead of trying to force the economy to generate enough taxes to match federal spending, Lerner urged policy makers to think in reverse. Taxes and spending should be manipulated to bring the overall economy into balance” (p. 61). Such a policy might require “sustained fiscal deficits over many years or even decades” (p. 61). So long as inflation remains under control, “Lerner saw this as a perfectly responsible way to manage the government budget” (p. 61). Kelton’s depiction of Lerner’s argument that fiscal deficits and the size of a nation’s debt do not matter is accurate so long as a very important qualification made by Lerner is taken into account. In particular, Lerner made it clear that a necessary condition had to be in place for a nation’s fiscal position, including its debt level, not to matter. This condition, which I discuss below, is not taken into account by Kelton.

After describing Lerner’s concept of functional finance, Kelton expresses the following view: “Lerner’s insights are important to MMT, but they don’t go far enough.… We think Lerner’s prescriptions will still leave too many people without jobs” (p. 63). Lerner, argues Kelton, thought that attaining what he called full employment would be accompanied by a level of involuntary unemployment, leaving some people out of work. To ensure that everyone has a job, “MMT recommends a federal job guarantee, which creates a nondiscretionary automatic stabilizer that promotes both full employment and price stability” (p. 63).

Here is the way MMT’s economic program would work. The Federal Reserve would become subservient to the U.S. Treasury. To ensure that “funding … can always be made available” (pp. 234–35) for whatever purpose is deemed worthwhile, “the Federal Reserve carries out an authorized payment on behalf of the Treasury” (p. 235). Specifically, the Fed would print whatever money was needed to finance the government’s spending intentions: “[W]e must recognize that the US government can supply all the dollars our private sector needs to reach full employment, and it can supply all the dollars the rest of the world needs to build up their reserves and protect their trade flows” (original italics, p. 151). What spending would be worthwhile? In addition to the federal job guarantee, the ability to print currency would provide the fiscal space to fund Medicare for all; free college; middle-class tax cuts; a full Green New Deal; free child care; the cancelation of student debt; affordable housing for everyone; a national high-speed rail; a Civilian Conservation Corps, the responsibilities of which would include fire prevention, flood control, and sustainable agriculture; and expanded Social Security. MMT’s program would reduce racial inequalities, decrease poverty, build stronger communities, and more (pp. 229–63).

Under the federal job-guarantee program, if “the economy were to crash the way it did in 2008, the job guarantee would catch hundreds of thousands of people instead of allowing them to fall into unemployment” (p. 67). Moreover, the government would steer spending to preferred sectors of the economy. Thus, Kelton argues that: “With decent jobs guaranteed for all, workers can engage in a public-led industrial policy aimed at producing sustainable infrastructure and a wider array of public services” (italics supplied, p. 152). The program would establish a wage floor of “say $15 per hour” (p. 68). That floor, in and of itself, would help “to stabilize inflation by anchoring a key price [i.e., the wage rate] in the economy” (p. 67). Yet, despite the foregoing menu of spending intentions, Kelton tells the reader that MMT “is not a plot to grow the size of government” (p. 235).

Apart from the minimum wage’s anchoring role under the federal job program, how would Kelton keep inflation in check? She is very vague: “MMT would make us safer [against inflation] because it recognizes that the best defense against inflation is a good offense” (original italics, p. 72). What is a good offense against inflation? She continues: “We want agencies like the CBO helping to evaluate new legislation for potential inflation risk before Congress commits to funding new programs so that the risks can be mitigated preemptively.” In this connection, “If the CBO and other independent analysts concluded it [higher spending] would risk pushing inflation above some desired inflation rate, then lawmakers could begin to assemble a menu of options to identify the most effective ways to mitigate that risk” (original italics, p. 72). What are these options? Congress would “work backward” to identify areas where spending could be cut, thus ensuring “that there is always a check on any new spending. The best way to fight inflation is before it happens” (original italics, pp. 72–73). Essentially, Kelton maintains that there is always spare capacity in the economy such that the aggregate supply curve is flat. Consequently, a large, sustained fiscal stimulus, financed by money creation, would neither crowd out private expenditure nor ignite inflation.

With fiscal policy bearing the heavy work in economic stabilization, Kelton asks: “Can fiscal policy really take over the economic steering wheel? What’s left for monetary policy?” (p. 242). With the Federal Reserve having become an arm of the Treasury, monetary policy—open-market operations, changes in the discount rate, and changes in reserve requirements—merit essentially no role in Kelton’s scheme: “MMT considers fiscal policy a more potent stabilizer [than monetary policy]” (original italics, p. 243).

Two points about the financing of the fiscal deficits under MMT are important. First, as indicated in the foregoing synopsis of Kelton’s book, money creation would be the primary means of financing increases in government spending. Kelton argues that money and government bonds are essentially identical assets in private-sector portfolios. Why, then, does the government borrow? Why not just pay for government spending by running the printing press? Kelton states: “[The government] chooses to offer people a different kind of government money, one that pays a bit of interest. In other words, US Treasuries are just interest-bearing dollars” (original italics, p. 36). It follows that the government can make “the national debt disappear” by letting the Federal Reserve purchase all the outstanding government debt (p. 99).4 Thus, “the purpose of auctioning US Treasuries—that is, borrowing—isn’t to raise dollars for Uncle Sam” (p. 36).5

Second, as is the case with sovereign borrowing, Kelton believes that taxation should not normally be used to finance government spending. Nevertheless, she maintains that taxes serve several key functions within an economic system: (1) “taxes enable governments to provision themselves without the use of explicit force”—without that tax obligation, people would not have a reason to demand the government’s fiat currency (p. 32); (2) should the need arise, taxation provides a means to combat inflation (p. 33); (3) “taxes are a powerful way to alter the distribution of wealth and income” (p. 33); and (4) taxes are a way “to encourage or discourage certain behaviors” (p. 34).

The MMT framework, including Kelton’s rendition of that framework, has been subjected to considerable, tough criticism from leading economists. Kelton’s rendition, for example, has been criticized for (1) its neglect of the 1970s, a period during which expansionary policies led to increases in both inflation and unemployment (Cochrane 2020); (2) the likelihood that it would induce unexpected inflation, reducing the purchasing power of those caught holding “old money” as “new money” is printed (Andolfatto 2020, Dowd 2020); (3) its strong proclivity to increase the size of the government in the economy, thereby diverting resources from productive firms to the quixotic public sector (Coats 2019, Tenreiro 2020); (4) its neglect of the fact that, in the absence of monetary accommodation, fiscal expansion can be a weak policy instrument (Greenwood and Hanke 2019); and (5) its neglect of the literatures on central-bank independence, the term structure of interest rates, and the effects of portfolio-balance decisions by investors on the way that policies interact with key economic variables (Edwards 2019).6 Krugman (2019) likened MMT to Calvinball, a game under which its adherents keep changing their arguments in response to criticisms; Rogoff (2019) called MMT “nonsense”; and Summers (2019) wrote that it is “a recipe for disaster.” Yet, in the present low-inflation environment, MMT continues to thrive in certain political circles and to be the focus of debate among academics while Kelton has become the leading spokesperson for the movement. After all, if inflation has remained below 2 percent in most major economies despite the highly expansionary monetary and fiscal policies of the past decade, why not take advantage of the benefits that MMT promises to deliver? Let me, therefore, assess MMT through the lens of Kelton’s “poster child” currency user.

Back to the Past, I: The Poster Child

In Kelton’s book, the case of the Greek sovereign-debt crisis is the prime example of what happens when a country gives up its monetary sovereignty to become a currency user. Here are several examples:

- “I never worry about the US ending up like Greece” (p. 81).

- “To cover [its fiscal] deficits [in 2009], Greece had to borrow. The problem is that under the euro, the Greek government no longer had a central bank that could act on its behalf by clearing all its payments” (p. 85).

- “But the US is not like Greece (which borrows in euros)” (p. 91).

- Adoption of the euro “relegates all eurozone members to mere currency users. This point is crucial to understanding Greece’s seemingly endless debt crisis” (p. 145).

What exactly happened in Greece to ignite the financial crisis that erupted in 2009? Kelton maintains that Greece fell victim to the 2008 global financial crisis and the accompanying global recession:

Countries like Greece and Italy, along with the other seventeen members of the eurozone, gave up their sovereign currencies in order to use the euro. Since they can’t issue the euro, member governments must cover fiscal deficits by selling bonds.… The problem is that lending to these countries became especially risky once they started promising to repay bondholders in a currency they could no longer issue themselves. This became painfully clear in the wake of the 2008 financial crisis, as the global recession pushed the budgets of Greece and other eurozone countries deeply into deficit.… Governments had no choice but to borrow in private financial markets, and they had to pay whatever the market demanded to secure the funding they needed.… In Greece, the poster child for the crisis, interest rates on ten-year government bonds skyrocketed from 4.5 percent in September 2008 to nearly 30 percent by February 2012 [p. 124].

Two points made in the above excerpt concerning Greece are important to highlight. First, Kelton argues that it was the global recession associated with the 2008 financial crisis that pushed Greece’s budget “deeply into deficit.” Second, Kelton identifies the period during which interest rates on Greek government bonds “skyrocketed” as having begun in September 2008. (Recall that September 2008 saw the collapse of Lehman Brothers.)

Kelton’s assessment of the origin of the Greek financial crisis begs the question: Why Greece? Germany, Luxembourg, and the Netherlands are members of the euro area. Those countries also gave up their monetary sovereignty to adopt the euro. Yet, those countries—and others in the euro area—did not experience financial crises following the outbreak of the 2008 global recession. As I explain below, there was a reason for this circumstance.

Greece became a member of the euro area in 2001. Why did the country decide to transform itself from a currency issuer to a currency user? To address this issue, let’s go farther back in time to the 1980s and the early 1990s, a period during which the country had its own currency, the drachma. Beginning in 1981, the country undertook highly expansionary fiscal policies.7 As a result, the fiscal deficit, which was 2.6 percent of GDP in 1980, rose to 8.7 percent of GDP in 1981. During the period 1981 to 1994, the deficit-to-GDP ratio averaged 11.7 percent.8 During most of the period, the Bank of Greece was subservient to the government. Indeed, at one point, the same individual simultaneously held the positions of finance minister and governor of the Bank of Greece. Consequently, monetary policy’s role was to help finance the fiscal deficits—annual money growth averaged more than 20 percent during the period 1981 to 1994.9 In light of the large fiscal deficits, the debt-to-GDP ratio exploded, from 28.4 percent in 1980 to 107.9 percent in 1994. The key macroeconomic performance indicators during 1981 to 1994 tell the resulting story: the nominal interest rate on the 10-year government bond was consistently near 20 percent, despite the activity of the Bank of Greece in the sovereign-bond market; inflation—something that Kelton says will not happen to a currency issuer—averaged 18 percent; real growth averaged 0.8 percent; and the current account consistently registered deficits in the range of 3 percent to 5 percent of GDP. In those circumstances, the country faced a series of financial crises as the drachma came under attack. Several adjustment programs were undertaken, but they were subsequently abandoned in favor of a reversion to fiscal and monetary expansion.

Having experienced the costs (very low growth, high inflation, financial crises) of overly expansionary macroeconomic policies, in the mid-1990s, Greece committed to putting its economic house in order with the goal of joining the euro area.10 Fiscal and monetary policies were tightened. The reorientation of policies succeeded, inflation and the fiscal imbalances were reduced, and the country entered the monetary union. The adoption of the euro was expected to produce a low-inflation, low-interest-rate environment conducive to economic growth.

That is precisely what happened—at least for a while. From 2001 to 2007, inflation moved into the low single digits and real growth averaged about 4 percent a year. In addition, interest rates came down. The spread between 10-year Greek and German sovereigns fell from over 600 basis points in the late-1990s to between 10 and 20 basis points several years after Greece joined the euro area. Greece seemed to have found the magic formula for economic success.

Beneath the surface, however, deep-seated problems emerged. An expanding government sector underpinned economic growth, and the country was internationally uncompetitive. Consider the following developments, mainly during the period from 2001, the year of entry into the euro area, to 2009:

- Fiscal deficits consistently topped 6 percent of GDP, peaking at 15 percent at the end of the period.

- The widening of the fiscal deficits was mainly expenditure driven; the share of government spending in GDP rose by eight percentage points—to 54 percent.

- The ratio of government debt to GDP rose from below 100 percent in the late 1990s to 125 percent at the end of the period. Between 2001 and 2009, the level of government debt almost doubled, from 163 billion euros to 301 billion euros.

- The fiscal expansion was mainly financed by external borrowing. The share of government debt held by non-Greek residents rose from 48 percent in 2001 to 79 percent in 2009.

- Greece’s competitiveness, measured in terms of unit labor costs relative to those of its major trading partners, deteriorated by 30 percent.

The loss in competitiveness, and the relatively high growth rates, led to a widening of the current account deficit. Greece entered the euro area with an already-high current account deficit equal to almost 7 percent of GDP. Near the end of the period, that deficit had widened to 15 percent of GDP.11

Despite these large and growing imbalances—which should have sounded loud warning alarms to the financial markets, but did not—and despite the global financial crisis that erupted in August 2007 (and intensified in September 2008 with the collapse of Lehman), interest rates on Greek sovereigns remained at low levels until 2009. The markets apparently believed that, regardless of the Maastricht Treaty’s no-bail-out clause, if things went wrong, Greece’s euro area partners would be obliged to bail out the country to maintain the cohesion of the monetary union and to prevent negative spillovers to other countries.12 The markets continued to lend to the Greek government, and the government continued to spend and borrow as though it had unlimited fiscal space.

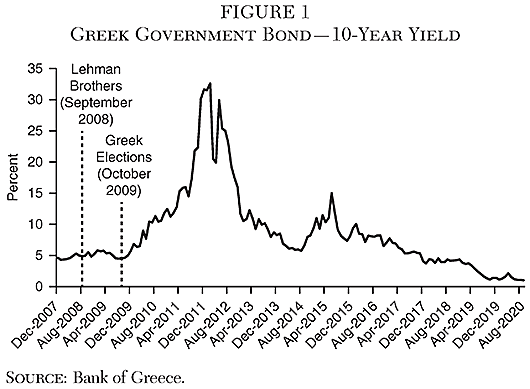

The turning point came during the elections in the fall of 2009. In October, shortly after the national elections, the new PASOK government announced that the 2009 fiscal deficit would soar to 12.5 percent of GDP, far higher than estimates provided by the former conservative (New Democracy) government (Barber 2009).13 The announcement focused market attention on Greece’s large fiscal imbalances, including the amount of government debt owed to non-Greek residents. Figure 1 shows the time profile of the interest rate on 10-year Greek government bonds. As shown in the figure, interest rates spiked upward in October 2009 and continued to rise for the next several years. What caused the Greek financial crisis was fiscal profligacy. Prior to October 2009, financial markets behaved as though the country’s fiscal and external positions were sustainable. Those euro area countries that did not incur fiscal and external imbalances—such as Germany, the Netherlands, and Luxembourg—did not face a crisis.14 Contrary to what Kelton argues, what caused the Greek financial crisis was not the loss of monetary sovereignty.

The following conclusions emerge. First, Kelton’s thesis that the 2008 global recession pushed Greece’s fiscal position “deeply into deficit” is incorrect. The 2008 recession exacerbated Greece’s already large fiscal deficits. The country ran fiscal deficits on the order of 7 percent of GDP throughout the period leading up to 2008.15 Second, Kelton’s argument that interest rates on Greek government debt “skyrocketed” beginning in September 2008, which, if accurate, would support her contention that the origination of the Greek financial crisis lay with factors external to Greece, is similarly incorrect. As clearly shown in Figure 1, interest rates on Greek sovereigns began their ascent in October 2009, coinciding with the market’s recognition that Greece’s fiscal situation was unsustainable. The interest rate on the 10-year Greek government bond was 5.0 percent in September 2008 (Figure 1).16 It fell subsequently, reaching 4.5 percent in September 2009. Following the announcement about the size of the 2009 fiscal deficit in October of that year, the interest rate began its upward climb. By January 2010, the rate was at 6.9 percent; by June 2010, it had reached 10.5 percent. The rate peaked at 32.6 percent in February 2012. Third, Greece experienced financial crises both in the 1980s and during the period from 2009 to 2015. In the former period, the country was a currency issuer. In the latter period, it was a currency user. Both periods were marked by fiscal profligacy as successive governments behaved as if they had unlimited fiscal space. Fiscal profligacy was the common denominator in the crises.

Back to the Past, II: Kelton, Lerner, and Chicago

Two monetary doctrinal issues shed light on the cohesiveness and soundness of Kelton’s framework: (1) Kelton’s treatment of Lerner’s functional-finance proposal and (2) the similarities and differences between Kelton’s framework and the monetary framework developed by Chicago economists in the 1940s. Kelton generously acknowledges the influence of Lerner’s formulation of functional finance on her rendition of MMT (pp. 60–63). Like Lerner, Kelton believes that the national debt is not a burden on future generations. Like Lerner, Kelton maintains that the interest paid on the debt is also not a burden on the nation. However, as I mentioned, Lerner believed that an important, third condition had to be in place for the previous two conditions to be valid. What was that third condition? Lerner recognized that the national debt had to be internally owned. He wrote:

All this is true, of course, only of internally held national debt. Increasing debt to other countries or to the citizens of other countries does indicate impoverishment of the borrowing country and enrichment of the lending country.… For a country to borrow from another country may be foolish or wise according to circumstances, just as in the case of individual borrowing. Such debt should be limited because the repayment will constitute a real burden on the country just as the borrowing provided a real benefit quite different from any benefit that can accrue from internal borrowing. When the time comes to make the repayment there may be great inconvenience which could lead to default [Lerner 1944: 305; italics supplied].

Lerner believed that all externally owned debt was a burden on a country; he did not distinguish between external debt that was denominated in a particular country’s currency and external debt that was denominated in foreign currencies.

Kelton does not mention the above qualification made by Lerner to his idea of functional finance.17 In Kelton’s view, the United States performs a service for other countries when it supplies those countries with U.S. dollars, and those countries use the dollars to buy U.S. Treasury bonds. When the United States imports goods from China, for example, and pays for the imports with newly created dollars, Kelton writes: “We’re not really borrowing from China [even though the U.S. dollars are a debt obligation of the United States] so much as we’re supplying China with dollars to be transferred into a U.S. Treasury security.… [Therefore,] terms like borrowing [to describe the U.S. side of the transaction] are misleading. So is labeling these securities as national debt. There is no real debt obligation” (original italics, p. 83). Why is there no real debt obligation? Kelton argues there is an unlimited demand for the dollar as an international currency. Thus, the United States can simply keep printing dollars to pay for the maturing Treasury securities held by China (pp. 82–83).

A fundamental condition for the international use of a currency is that there has to be confidence in the currency’s value. Specifically, high or variable inflation rates add to the costs of using a currency internationally by generating nominal exchange rate depreciation and variability. These factors increase the costs of acquiring information and making efficient calculations about the prices bid and offered for tradable goods and capital assets. Thus, they undermine a currency’s use as an international medium of exchange, unit of account, and store of value. Furthermore, inflation increases the costs of holding a currency by eroding its purchasing power, debasing the currency as an international store of value. Kelton’s roadmap to the economic promised land considers that money creation will be subservient to the fiscal authorities and politicians’ needs and desires. Consequently, money creation would be endogenous. The fiscal authorities and the politicians would see to it, Kelton believes, that money-financed deficits will not create inflation. However, as we have seen in the case of Greece in the 1980s, making money creation subservient to the fiscal authorities can be a roadmap—not to the economic promised land but to inflation, higher long-term interest rates (because of inflation), higher-risk premia, and financial crises. I suggest that the dollar’s international role, and the seigniorage that the United States derives from that role, would not last long under Kelton’s roadmap.

Kelton’s policy framework shares several characteristics with the framework developed in the 1940s by Chicago economists, Simons, Mints, and Friedman. Nevertheless, Kelton’s—and MMT’s–policy proposals were orthogonal to the proposals pushed forward by the Chicagoans. Hence, a comparison of those frameworks will be instructive. I should mention that, unlike Lerner’s work, Kelton evinces no awareness of the contributions made by the Chicago economists in the 1940s.18

Lerner (1944: 303) was indifferent between bond-financed and money-financed fiscal deficits. In contrast, the earlier Chicago economists believed that fiscal deficits should be entirely backed by money creation, a view shared by Kelton.19 Like Kelton, the Chicagoans believed that the Federal Reserve should be made subservient to the U.S. Treasury.20 Like Kelton, the Chicagoans thought that reliance on open-market operations to conduct monetary policy should be reduced.21

There were, however, foundational differences between the framework developed by the earlier Chicagoans and Kelton’s framework. First, the Chicagoans believed that money was a crucial variable in the economy and that its quantity needed to be controlled. Otherwise, increases in the quantity of money could lead to self-generating rises in inflation. In contrast, Kelton’s framework makes the quantity of money endogenous to the government’s fiscal position. Second, the Chicagoans believed that monetary policy uncertainty was a primary cause of disturbances to the economy. Kelton’s proposal does not consider the role of policy uncertainty. Third, in light of the first two factors, the Chicagoans thought that monetary policy should be based on a rule that aims to achieve a stable price level.22 Such a rule would, in turn, help keep money creation out of the political process by strictly limiting the quantity of money. Simons (1944: 224) put it as follows: “[O]nly by recognizing and by accepting this [price-level-stabilization] rule can legislatures be made responsible financially or business spared intolerable monetary uncertainty.“23 In contrast, Kelton’s framework is discretion based. She believes that her federal job-guarantee proposal would be compatible with price stability under the watchful (i.e., discretionary) eye of the Congressional Budget Office; she does not address the role of monetary uncertainty in the economy.

Under the Chicago framework, the role of the government would be to establish the monetary rule and to ensure that it was followed—that is, the government’s role would be constitutional as opposed to administrative. Under that framework, the budget would be balanced over the course of the business cycle, with the aim of limiting the size of the government. Should the automatic stabilizers fail to provide sufficient demand during the trough of the cycle, increases in the size of the fiscal deficit, and, thus, increases in the quantity of money, would be generated through reductions in taxes—and not by increases in government spending.24 The Chicagoans believed that the amount of fiscal space available was subject to strict limits. In contrast, under Kelton’s proposal, which would increase the size of the government sector, the government’s role would be administrative. Under her proposal, the amount of fiscal space would be unlimited before a vaguely defined inflation constraint kicks in.

There was an important reason underlying the Chicagoans’ aim to prevent the concentration of power in the government: those economists wanted to preserve individual liberty. In a 1945 paper, Simons expressed this view as follows:

[The] strength [of the competitive system] is in its implied political philosophy. Its wisdom is that of seeking solutions which are within the rule of law, compatible with great dispersion or deconcentration of power, and conducive to extensive supranational organization on a basis that facilitates indefinite peaceful extension.… Certainly another kind of system, ruled by authorities, might be more efficient and more progressive—if one excludes liberty as an aspect of efficiency and capacity for freedom and responsibility, among individuals and among nations, as a measure of progress. Discretionary authorities, omniscient and benevolent, surely could in some sense do better than any scheme involving democratic, legislative rules and competitive dispersion of power. After any disturbing change they could promptly effect the same arrangements which competition would achieve slowly or with ‘unnecessary’ oscillations. Indeed, they could probably avoid all real disturbances by anticipating them! But some of us dislike government by authorities, partly because we think they would not be wise and good and partly because we would still dislike it if they were [Simons 1945: 308–9; original italics].

Additionally, the Chicagoans believed that discretionary policies can, in practice, be destabilizing. Specifically, the long and variable lags associated with discretionary policies can mean that countercyclical actions will be a source of disruptions. For example, the effects of a policy easing aimed at supporting aggregate demand and raising inflation might not kick in until the expansionary phase of the cycle. Lerner’s functional-finance proposal’s failure to take account of lags formed the basis of Friedman’s criticism of the proposal. In a 1947 article, “Lerner on the Economics of Control,” Friedman appraised functional finance as follows:

[Functional finance] conflicts with the hard fact that neither government action nor the effect of that action is instantaneous. There is likely to be a lag between the need for action and government recognition of this need; a further lag between recognition of the need for action and the taking of action; and a still further lag between the action and its effects. If these time lags were short relative to the duration of the cyclical movements government is trying to counteract, they would be of little importance. Unfortunately, it is likely that the time lags are a substantial fraction of the duration of the cyclical movements. In the absence, therefore, of a high degree of ability to predict correctly both the direction and the magnitude of required action, governmental attempts at counteracting cyclical fluctuations through “functional finance” may easily intensify the fluctuations rather than mitigate them. By the time an error is recognized and corrective action taken, the damage may be done, and the corrective action may itself turn into a further error. This prescription of Lerner’s, like others, thus turns into a exhortation to do the right thing with no advice how to know what is the right thing to do [Friedman 1947: 315–16].

Conclusion

Kelton’s book makes many promises and offers a straightforward way to pay for them: run the printing press. The appeal of the proposal, especially to some politicians, is that it aims to deliver a “people’s economy” at no cost. However, Kelton’s appraisal of her poster child, Greece, for the way not to run an economy is an inaccurate depiction of monetary history. Greece’s recent monetary history shows that it was the country’s fiscal profligacy—not its status as either a currency issuer or currency user—that lay at the heart of the country’s financial crises. Greece’s economic waters were turbulent for many years before the country adopted the euro; those waters only stabilized—temporally—by the commitment to fiscal sobriety prior to its entry into the euro area. Moreover, Kelton’s description of Lerner’s idea of functional finance is an inaccurate depiction of doctrinal history. In contrast to Kelton, Lerner evinced a deep concern about the consequences of any fiscal program that does not pay attention to externally held government debt. The above comparison of Kelton’s framework with that of Chicago economists in the 1940s shows that, unlike the latter framework, Kelton’s scheme does not aim to provide limits on money creation needed to maintain price stability, assumes essentially unlimited fiscal space, does not account for monetary uncertainty or the destabilizing effects of lags under discretionary policy, assumes that there is always spare capacity such that the aggregate supply curve is flat, and would increase both the size and the administrative role of government in economic affairs.

An important consideration in evaluating Kelton’s proposal is that the author has ventured into an area—the subject of money—which appears to be uncharted waters for her. She is by no means the first person to have done so; nor is she likely to be the last. Let me, therefore, conclude with something that Chicagoan Mints wrote in his 1950 book, Monetary Policy for a Competitive Society:

[M]onetary policy is a subject which requires the exercise of judgement, and this being so, it can hardly be expected that differences of opinion will not arise. For the same reasons it is also nearly inevitable that monetary cranks of many descriptions should appear who have their “sure cures” for the afflictions of society. They see one thing that might possibly be accomplished by monetary measures, but they do not understand the many other effects of their proposals [Mints 1950: v].

References

Andolfatto, D. (2020) “Modern Monetary Theory.” MacroMania (March 14).

Barber, T. (2009) “Greece Vows Action to Cut Budget Deficit.” Financial Times (October 20).

Coats, W. (2019) “Modern Monetary Theory: A Critique.” Cato Journal 39 (3): 563–76.

Cochrane, J. H. (2020) “ ‘The Deficit Myth’ Review: Years of Magical Thinking by Stephanie Kelton.” Wall Street Journal (June 5).

Dellas, H., and Tavlas, G. S. (2009) “An Optimum-Currency-Area Odyssey.” Journal of International Money and Finance 28 (7): 1117–37.

Despain, H. G. (2020) “Book Review: The Deficit Myth: Modern Monetary Theory and the Birth of the People’s Economy by Stephanie Kelton.” Available at https://blogs.lse.ac.uk/lsereviewofbooks/2020/06/22/book-review-the-deficit-myth-modern-monetary-theory-and-the-birth-of-the-peoples-economy-by-stephanie-kelton.

Dorn, J. A. (2018) “Monetary Policy in an Uncertain World: The Case for Rules.” Cato Journal 38 (1) (Winter): 81–108.

Dowd, K. (2020) “Book Review: The Deficit Myth: Modern Monetary Theory and the Birth of the People’s Economy by Stephanie Kelton.” Cato Journal 40 (3): 795–809.

Edwards, S. (2019) “Modern Monetary Theory: Cautionary Tales from Latin America.” Cato Journal 39 (3): 529–61.

Friedman, M. (1947) “Lerner on the Economics of Control.” Journal of Political Economy 55 (October): 405–16. Reprinted in M. Friedman (ed.), Essays in Positive Economics (1953: 303–24). Chicago: University of Chicago Press.

________ (1948) “A Monetary and Fiscal Framework for Economic Stability.” American Economic Review 38: 245–64. Reprinted in Essays in Positive Economics, 133–56.

Garganas, N., and Tavlas, G. S. (2001) “Monetary Regimes and Inflation Performance.” In R. C. Bryant, N. C. Garganas, and G. S. Tavlas (eds.), Greece’s Economic Performance and Prospects, 43–95. Athens and Washington: Bank of Greece and Brookings Institution.

Greenwood, J., and Hanke, S. H. (2019) “Magical Monetary Theory.” Wall Street Journal (June 4).

Hope, K. (2011) “Humiliating End to Greece’s Social Reformer.” Financial Times (November 7).

Kelton, S. (2020) The Deficit Myth: Modern Monetary Theory and the Birth of the People’s Economy. New York: PublicAffairs.

Krugman, P. (2019) “Running on MMT (Wonkish).” New York Times (February 25).

Lerner, A. P. (1944) The Economics of Control: Principles of Welfare Economics. New York: Macmillan.

Mints, L. (1950) Monetary Policy for a Competitive Society. New York: McGraw-Hill.

Nelson, E. (2020) Milton Friedman and Economic Debate in the United States, 1932–1972. Chicago: University Chicago Press.

Papandreou, G. A. (2009) Press conference, 74th Thessaloniki International Fair (September 13).

Rogoff, K. (2019) “Modern Monetary Nonsense.” Project Syndicate (March 4).

Simons, H. C. (1936) “Rules versus Authorities in Monetary Policy.” Journal of Political Economy 64: 1–30. Reprinted in H. C. Simons (ed.), Economic Policy for a Free Society (1948: 160–83). Chicago: University of Chicago Press.

________ (1944) “On Debt Policy.” Journal of Political Economy 52: 356–61. Reprinted in H. C. Simons (ed.), Economic Policy for a Free Society (1948: 220–30). Chicago: University of Chicago Press.

________ (1945) “The Beveridge Program: An Unsympatheric Interpretation.” Journal of Political Economy 53: 212. Reprinted in Economic Policy for a Free Society, 277–312.

Summers, L. H. (2019) “The Left’s Embrace of Modern Monetary Theory is a Recipe for Disaster.” Washington Post (March 5).

Tavlas, G. S. (1991). On the International Use of Currencies: the Case of the Deutsche Mark. Princeton University, Department of Economics, International Finance Section Essays in International Finance No. 181 (March).

________ (1993) “The ‘New’ Theory of Optimum Currency Areas.” World Economy 16 (6): 663–85.

________ (2015) “In Old Chicago: Simons, Friedman, and the Development of Monetary-Policy Rules.” Journal of Money, Credit and Banking 47 (1): 99–121.

________ (2019) The Theory of Monetary Integration in the Aftermath of the Greek Financial Crisis. The Seventh Annual Marco Minghetti Lecture, with comments by P. C. Padoan and P. Savona. Rome, Italy: Istituto Luigi Struzo (January).

________ (2020) “On the Controversy Over the Origins of the Chicago Plan for 100 Percent Reserves: Sorry Frederick Soddy, It Was Knight and (Most Probably) Simons!” Hoover Institution, Economics Working Paper No. 20102. Forthcoming in Journal of Money, Credit and Banking.

Taylor, J. B. (2017) “Rules versus Discretion: Assessing the Debate over the Conduct of Monetary Policy.” NBER Working Paper Series No. 24149. Available at www.nber.org/system/files/working_papers/w24149/w24149.pdf.

Tenreiro, D. (2020) “What the Deficit Myth Lacks.” National Review (June 8).

This work is licensed under a Creative Commons Attribution-NonCommercial-ShareAlike 4.0 International License.