When China began economic reform in 1978, it had only one financial institution, the People’s Bank of China (PBOC), which, at that time, served as both the central bank and a commercial bank and accounted for 93 percent of the country’s total financial assets. This was primarily because, in a centrally planned economy, transfer of funds was arranged by the state and there was little demand for financial intermediation. Once economic reform started, the authorities moved very quickly to establish a very large number of financial institutions and to create various financial markets. Forty years later, China is already an important player in the global financial system, including in the banking sector, direct investment, and bond and equity markets.

However, government intervention in the financial system remains widespread and serious. The PBOC still guides commercial banks’ setting of deposit and lending rates through “window guidance,” although the final restriction on deposit rates was removed in 2015. Industry and other policies still play important roles influencing allocation of financial resources by banks and capital markets. The PBOC intervenes in the foreign exchange markets from time to time, through directly buying or selling foreign exchanges, setting the central parity, and determining the daily trading band. The regulators tightly manage cross-border capital flows, and the state still controls majority shares of most large financial institutions.

Often such repressive financial policies are subject to criticisms in both academic and policy discussions. Academics believe that state interventions reduce financial efficiency and inhibit financial development (Lardy 1998; McKinnon 1973). Private businesses complain about policy discrimination, which made it very difficult for them to obtain external funding. Sometimes, China’s repressive financial policies are also a source of controversy in discussion of its outward direct investment (ODI). Some foreign experts argue that the Chinese state-owned enterprises (SOEs) compete unfairly with foreign companies, since they receive subsidized funding in China. This issue is also at the center of the current trade dispute between China and the United States (USTR 2018).

Despite all these potential problems, for quite a while, the repressive financial policies did not stop China from achieving rapid economic growth and maintaining financial stability. During the first three decades of economic reform, China’s GDP growth averaged 9.8 percent per annum and its financial system did not experience any systemic financial crisis, although the volume of nonperforming bank loans was quite large in the late 1990s. Unfortunately, during the past decade, the above rosy picture faded away quickly as economic growth decelerated and systemic financial risks escalated sharply. It appears that what worked before could no longer continue.

China’s unique experience of financial reform raises some important intellectual and policy questions. Why did the Chinese government maintain extensive interventions in the financial sector during the reform period? Is financial repression as bad as what is commonly believed? Do costs and benefits of repressive financial policies vary under different circumstances? How should the government respond to changing impacts of financial repression on economic growth and financial stability? At the background of these discussions, there is also a more fundamental but somewhat hypothetical question: Were China to adopt the “shock-therapy” approach in its financial reform at the beginning, would the Chinese economy have performed better?

This article addresses those questions and offers recommendations for future financial reform policies. It also draws some general lessons from the Chinese experiences that are relevant for financial liberalization in other developing countries.

Key findings of this article can be summarized as follows. First, China’s financial reform and development during the past four decades could be characterized as strong in establishing financial institutions and growing financial assets, but weak in liberalizing financial markets and improving corporate governance (see Huang et al. 2013). On the one hand, starting with one financial institution in 1978, China has built a very large financial sector, including large numbers of various financial institutions and gigantic sizes of financial assets. On the other hand, free-market mechanisms remain seriously constrained in the financial system, including in pricing and allocation of financial resources. This unique pattern of financial liberalization is closely linked with China’s gradual dual-track reform approach — maintaining SOEs while creating favorable conditions for the private sector to grow rapidly (Fan 1994; Naughton 1995). In retrospect, this gradual dual-track reform approach worked better than the “shock-therapy” approach as it helped maintain economic stability in the transition toward the market system. Repressive financial policies, through depressed cost of capital and discriminatory allocation of financing, provide de facto “subsidies” to the SOEs. In other words, financial repression is a necessary condition for the dual-track reform approach.

Second, several empirical analyses, using either Chinese data (Huang and Wang 2011) or cross-country data (Huang, Gou, and Wang 2014), confirm that repressive financial policies could have positive effects on economic growth and financial stability during early stages of development. But over time, such positive effects could turn to negative impacts. Possibly, there are two types of effects of financial repression: one is the McKinnon effect and the other is the Stiglitz effect (Huang and Wang 2017; McKinnon 1973; Stiglitz 1994). The McKinnon effect is generally negative, as financial repression hinders both financial efficiency and financial development, while the Stiglitz effect is mainly positive as repressive financial policies could help effectively convert saving into investment and support financial stability. Both effects exist in all economies, but their relative importance varies. The Stiglitz effect is more important when both the financial market and the regulatory system are underdeveloped. This, again, validates the observation that financial repression did not disrupt rapid economic growth and financial stability during Chinas’ early stage of reform.

And, finally, repressive financial policies began to hurt China’s economic and financial performance recently. Economic growth decelerated persistently after 2010. One of the important reasons is that, as China reached the high mid-income level, its economic growth has to rely more on innovation and industrial upgrading, instead of mobilization of more inputs. But repressive financial policies are not best positioned to support corporate innovation. They are also not well suited to provide asset-based income for Chinese households. In the meantime, systemic financial risks also rose markedly, as the two most important pillars supporting financial stability, sustained rapid economic growth and government implicit guarantee, weakened visibly. These suggest that the policy regime that worked quite effectively during the first several decades could no longer deliver the same results. Further reforms are urgently needed to support growth and stability in the future. These should probably focus on developing multilayer capital markets, letting market mechanisms play decisive roles in allocating financial resources, and improving financial regulation.

These findings offer important implications for the general thinking about economic reform and for the current trade disputes between China and the United States. In economies where financial markets and regulatory systems are underdeveloped, a certain degree of financial repression could actually be helpful. If China gave up all government interventions at the start of the reform, it would have experienced several rounds of financial crises. In this sense, repressive financial policies in China are transitory measures. They are an integral part of the gradualist approach and effective ways of supporting economic growth and financial stability. Today, however, the Chinese government needs to push ahead with further financial reforms, especially increasing the role of the market and opening the financial sector to the outside world.

The remainder of this article is organized as follows. In the next section, we briefly explain China’s process of financial reform and development, summarize its distinctive features, and rationalize the logic behind it. We then assess the reform policies and distinguish the McKinnon effect and Stiglitz effect of financial repression on economic growth and financial stability. Next, we discuss the recent deterioration of economic and financial performance in China and suggest some future directions of financial reform. Finally, we conclude by drawing some general implications for China and other countries.

Unique Pattern of Financial Reform and Development

At the Third Plenum of the 11th National Party Congress in December 1978, the Chinese leaders decided to shift policy focus from class struggle to economic development. They then launched a series of initiatives to rebuild and restructure the financial system. The following four decades may be divided into three stages according to key policy initiatives. The first stage started in 1979 when the authorities quickly reestablished three state-owned specialized banks — the Bank of China (BOC), the Agricultural Bank of China (ABC), and the China Construction Bank (CCB).1 At the beginning of 1984, the then PBOC was split into two parts, the Industrial and Commercial Bank of China (ICBC) and the new PBOC. The main policy efforts during this stage were to create large numbers of financial institutions, especially banks and insurance companies. The second stage began in 1990 when both Shenzhen and Shanghai stock exchanges were set up at the end of the year. This marked the begining of China’s capital markets. In 1996, the PBOC established the interbank market. Finally, China’s accession to the World Trade Organization (WTO) at the end of 2001 kicked off the third stage when the financial policies focused mainly on financial opening, especially opening of the domestic banking and securities industries to foreign institutions. From 2009, the PBOC also accelerated the pace of internationalizing renminbi (RMB).

China’s financial reform and development process exhibits a very unique pattern. On the one hand, the government made tremendous progress in establishing financial institutions and growing financial assets. On the other hand, it continued to intervene in the financial system extensively (Huang et al. 2013).

China already has a very large number of financial institutions, ranging across banking, insurance, and security industries. At the end of 2017, its broad money supply (M2) was already greater than that of the United States and equivalent to 210 percent of its own GDP, the third highest in the world, following Lebanon and Japan. In the same year, total bank assets reached 252 trillion yuan, which was 304.7 percent of GDP. This was much higher than those of Japan (165.5 percent), Germany (96.6 percent), and the United States (60.2 percent). The “big four” banks, ICBC, BOC, CCB, and ABC, are regularly ranked among the world’s top 10. China’s stock and bond markets are often regarded as “underdeveloped,” but they were, respectively, ranked second and third in the world, according to market capitalization measures.

Government interventions can be seen in almost all financial activities, from determination of bank deposit and lending rates to allocation of credit and initial public offering (IPO) quota, and from management of cross-border capital flows to majority control of large financial institutions. According to one measure of financial repression, constructed using the World Bank data, China’s Financial Repression Index (FRI) (Figure 1) dropped from 1.0 in 1980 to 0.6 in 2015 (Huang et al. 2018). These confirm that China made important progress in market-oriented financial reform. Nevertheless, the degree of financial repression remains high throughout the reform period. In 2015, China’s FRI was higher than not only the average of the middle-income economies but also that of the low-income economies. In fact, out of the 130 economies with data in 2015, China’s FRI ranked fourteenth.

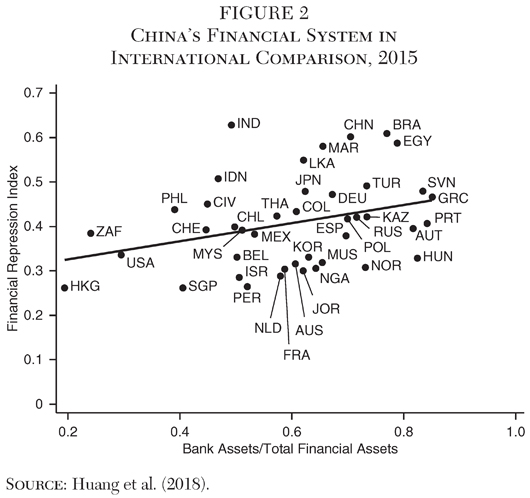

Compared to the international experiences, the Chinese financial system not only has a higher FRI but is also more dominated by the banking sector (CHN in Figure 2). One common understanding is that financial systems in the United States and the United Kingdom are market dominated while those in Germany and Japan are more bank dominated (DEU and JPN are on the right of USA in the figure). Cross-country data suggest possible positive correlation between FRIs and share of the banking sector, probably because banks are more suited to enforce government initiatives.

Rationales of Repressive Financial Policies

The high level of financial repression during China’s early reform period was likely a result of its unique dual-track reform strategy between the state and the nonstate sectors (Fan 1994). When economic reform started in 1978, the Chinese leaders did not have a blueprint for the reform policy. An urgent task for economic reform at that time was to improve productivity and raise output in both rural agriculture and urban industry. However, the political condition was not ripe for drastic reform, such as privatization of SOEs. Even the successful household responsibility system reform in agriculture continued with collective ownership of land. This strategy continued to support the SOEs through the old central planning system, which ensured no unemployment and no bankruptcy, at least initially. It also facilitated private-sector and market-oriented activities to grow. This reform approach, once characterized by Naughton (1995) as “growing out of the plan,” created a situation of “Pareto improvement.”

As the private sector grows faster than the state sector, this dual-track strategy could, in theory, enable the Chinese economy to transition smoothly from a central planned system to a market economy. The Chinese economic performance during the reform period was indeed impressive and was described as the “China miracle” by Lin, Cai, and Li (1995). In addition to rapid economic growth, there was no initial collapse of output and loss of jobs. SOEs’ share in total industrial output declined steadily, from around 80 percent in the late 1970s to around 20 percent in the mid-2010s. However, the state sector’s influence on the overall economy did not diminish accordingly. It actually caused some major macroeconomic problems, especially in the 1990s.

The main problem was that the SOEs’ financial performance deteriorated continuously. SOEs could not compete with more efficient private enterprises and foreign-invested firms, even though some studies discovered that SOEs’ productivity also improved over time (Huang and Duncan 1997). Gradual loss of monopoly power and intensification of competition pressure quickly eroded profitability of SOEs. By the mid-1990s, the state sector had become a net loss-maker (Huang 2001). To control bleeding, the government had to adopt a more aggressive reform program called “grasping the big and letting go the small and medium” in September 1995. The objective of this reform was for the government to focus only on the very large SOEs in strategic industries and to release all small and medium-sized SOEs in competitive industries. After this round of reform, the SOE sector shrank significantly. Its profitability also improved markedly because most of the remaining SOEs are gigantic and enjoy certain degrees of monopoly. Problems of the so-called soft budget constraint and relative inefficiency, however, continued.

The loss making by the SOEs around the mid-1990s caused at least two types of macroeconomic consequences, one was fiscal and the other was financial. The government almost suffered a fiscal crisis. The proportion of government revenues to GDP declined from 36 percent in 1978 to the trough of 11 percent in 1996. This decline was partly a result of the decentralization policy. SOEs, the dominant contributor to government revenues, not only contributed less over time but also demanded subsidies from the government. Although the private sector grew rapidly, most of the private enterprises were small and medium-sized enterprises (SMEs) paying little tax. Many foreign-invested firms enjoyed preferential policies such as tax exemption and tax concession. As a result, some local governments were unable to cover their overheads. To alleviate the fiscal stress, Beijing introduced a new tax-sharing system in 1994. Under the new system, some taxes (such as the income tax and customs duty) went directly to the central government, some (such as the resource tax and stamp duty) went to local governments, and others (such as the value-added tax) went to both the center and localities. The new system helped strengthen tax collection and increased the revenue share of the central government. Gradually, the proportion of tax revenues to GDP recovered to around 21–22 percent.

The banking sector also suffered severely, as the average bad loan ratio of the Chinese banks reached 30–40 percent around 1997 (Bonin and Huang 2001).2 This was because the banks’ largest borrowers were the SOEs, which faced a “soft-budget constraint.” Consequently, the government sometimes instructed the banks to make “stability loans” to financially troubled SOEs. Fortunately, there were no bank runs, as the banks also had a blanket guarantee from the government. From that time, the Chinese government adopted a series of measures to revamp the banking sector. In 1999, it established four asset management companies (AMCs) to resolve the bad loans. In 2003, the authorities established the Central Huijin Investment Company to inject capital into the banks and other financial institutions. In 2005, CCB introduced Bank of America as its first foreign strategic investor. Other banks took the same steps in the following years. And, in 2006, BOC and ICBC became publically listed companies on the Hong Kong and Shanghai Stock Exchanges.

All these problems highlight a key difficulty in implementing the dual-track reform approach — many of the SOEs are unable to survive without external support. One logical solution to this problem is for the government to provide fiscal subsidies to protect the SOEs. However, as the fiscal revenues declined rapidly relative to GDP throughout the 1980s, it became clear that the government would not have enough funding to support the SOEs. One alternative is through state intervention in factor markets in favor of the SOEs, both in terms of pricing and allocation of production factors. For instance, if the government could instruct the banks to continue to allocate large volumes of cheap credit to SOEs, then SOEs could survive even if their performance continues to deteriorate.

This logic was probably behind “asymmetric liberalization” of product and factor markets (Huang 2010; World Bank 2012). On the one hand, the government almost completely liberalized markets for agricultural, industrial, and service products, which allowed producers to identify market demand and profitable opportunities. With an open trade regime, Chinese industries can also easily participate in international competition. On the other hand, markets for production factors — including labor, capital, land, and energy — remained heavily distorted, and the government continued to intervene in their allocation and pricing. These distortions in the factor markets ensure that SOEs receive needed inputs at favorable prices. They are de facto subsidies. For instance, SOEs are often in privileged positions when purchasing energy products from the state power grid or the state-owned oil companies. The private enterprises would either not be able to acquire enough inputs or have to pay higher prices. The asymmetric liberalization approach between product and factor markets functions as a necessary policy instrument to support the dual-track reform between the state and nonstate sectors.

Repressive financial policies played an essential role in distorting factor markets and were important instruments to subsidize SOEs. Without those policies, the less-efficient SOEs would have been eliminated by competition a long time ago. Repressive financial policies also led to segmentation of the financial system into a formal sector and an informal sector. In the formal sector, the authorities depress costs of capital and allocate funds in favor of the SOEs. This has simply pushed a lot of non-SOEs out of the formal sector and caused the funding costs in the informal sector to be exceptionally high. Therefore, China has developed a very large financial system, and undersupply of financial services remains a very serious challenge, especially for the private enterprises. This is also why, in recent years, shadow banking and fintech industry expanded very rapidly. To a large extent, these developments were responses to financial repression in the formal sector. In many cases, they may even be regarded as “back-door” liberalization of interest rates and other policy distortions, because they bypass both regulations and restrictions in the formal sector.

Positive and Negative Effects of Financial Repression

It appears that repressive financial policies in China, at least initially, were necessary for the SOEs to survive, but how did they affect China’s economic performance during the reform period? On the surface, those policies did not prevent the economy from achieving rapid growth and financial stability. But the fundamental question remains: Did the Chinese economy achieve those successes because of, or despite, the repressive financial policies? The answer to this question might help us understand the mechanisms through which repressive financial policies affect economic and financial performance. It could even help us think about policy choices for China today and for other developing countries.

In an earlier study, Huang and Wang (2011) tried to quantify the impact of financial repression on economic growth in China during 1979–2008 by constructing a financial repression index. They first looked at the three-decade period as a whole and found a positive impact — that is, financial repression promoted economic growth. They then looked at three subperiods, separately, and found that, while financial repression promoted economic growth in the 1980s and 1990s, it became a drag in the 2000s. According to their study, if there had been full financial liberalization, real GDP growth would have been reduced by 0.79 percentage points in the 1979–88 period and by 0.31 percentage points in the 1989–99 period. But growth would have been increased by 0.13 percentage points in the 1999–2008 period.

The positive effect discovered for the 1980s and 1990s was consistent with the reasoning by Stiglitz (1994). In early stages of economic development, financial markets are often underdeveloped and might not be able to channel savings to investments effectively. Also, financial institutions are often immature and vulnerable to fluctuations in capital flows and financial stability. State intervention in forms of repressive financial policies can actually promote economic growth through support to confidence and effective conversion of saving into investment. Today, China is the only major economy in the world not experiencing a serious financial crisis. This is mainly because of government ownership anchoring investor confidence despite various risks that occurred during the past decades. For instance, without a relatively closed capital account, the Chinese economy would have been more seriously harmed by both the Asian financial crisis and the global financial crisis.

The negative impact of financial repression on economic growth found in the 2000s is in line with analysis by McKinnon (1973). State intervention in capital allocation might prevent funds from flowing to the most efficient uses. Protection of financial institutions and financial markets might also encourage excessive risk taking due to the typical moral hazard problem. Therefore, repressive financial policies would eventually hinder financial development, increase financial risks, reduce investment efficiency, and slow down economic growth. This should be easy to understand. For instance, if the less efficient SOEs continue to take in more and more financial resources, then efficiency of the overall economy would decline steadily. And if the government continuously provides implicit guarantee for any financial transactions, the risks could mount quickly and eventually reach a point of “blow-up.”

In a relatively recent study, Huang, Gou, and Wang (2014) examined the same question by using a cross-country dataset for the period 1980–2000. Similarly, they also found different impacts of financial repression on economic growth at different stages of economic development. Statistical analyses reveal that the growth effect of financial repression is insignificant among low-income economies, significantly negative among middle-income economies, and significantly positive among high-income economies. Furthermore, for the middle-income group, repressive policies on credit, bank entry, securities market, and the capital account significantly inhibit economic growth.

These empirical results suggest that the mechanisms through which repressive financial policies affect the economy and the financial system are complicated. The negative McKinnon effect and the positive Stiglitz effect of repressive financial policies on economic growth probably exist simultaneously in any economy (Huang and Wang 2017). The net outcome in an economy depends on the relative importance of these two effects (Huang et al. 2013). And the relative importance of these effects also changes under different economic and financial conditions. For instance, in early stages of economic development and reform, the contribution of financial repression to economic growth, through maintaining financial stability and converting saving into investment, is greater than its cost in terms of inefficiency and risks. Therefore, we should observe the Stiglitz effect. As the financial system matures, the negative impact of financial repression in terms of reduced capital efficiency and increased financial risks could outweigh its positive contribution. Then we should observe the McKinnon effect.

The recent transition from the dominance of the Stiglitz effect to the dominance of the McKinnon effect suggests that repressive financial policies have become a main drag on economic growth. After the global financial crisis, China’s GDP growth slowed steadily, from above 10 percent in 2010 to below 7 percent in 2015. There is probably a mixed set of factors responsible for this growth slowdown. Cyclical factors could include sluggish global economic recovery and weak Chinese export growth. Trend factors could refer to slower growth, on average, in more advanced economies. In the meantime, financial repression still favors less efficient SOEs in resource allocation and further impedes economic growth. This points to the urgent need to further liberalize financial policies.

The repressive financial policies actually contributed to the making of the “economic miracle” during the early decades of economic reform in China. Were China to have completely abandoned government intervention at the beginning of the reform, the financial system would, most likely, have experienced dramatic uncertainties and volatilities. Repressive financial policies probably still caused some efficiency losses, but the benefits were far greater. Equally important is that, even during that period, the level of financial repression was static. Financial liberalization continued, which should also generate significant efficiency improvement and strong momentums for growth.

Old Tricks No Longer Work

Economic and financial performance deteriorated markedly in China, especially after the global financial crisis in 2008. After a sharp rebound of GDP growth to 10.3 percent in 2010, following implementation of the massive stimulus package, the economy decelerated persistently to below 7 percent currently. Economists are divided on what caused this persistent slowdown — some speculate it to be a part of cyclical fluctuation, while some others believe this is a trend change. The most plausible explanation is probably the so-called middle-income challenge. As China’s GDP per capita moved from $2,600 in 2007 to $8,800 in 2017, it lost the low-cost advantage. Many of the industries that supported Chinese economic development for several decades, especially the labor-intensive manufacturing sectors, are no longer competitive. In order to continue with robust economic growth, China now needs to develop a large number of new higher tech and higher value-added industries that are competitive at high costs. Therefore, what is happening in China is not just slowdown of growth, but a paradigm shift in development.

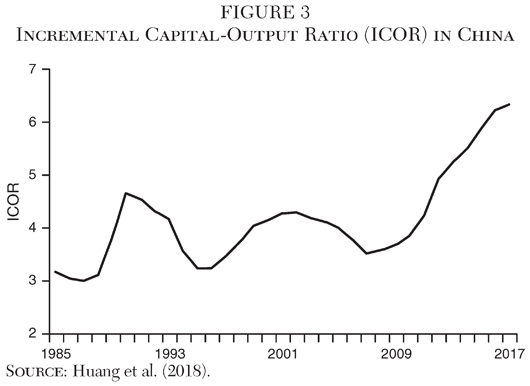

This is best illustrated by the rapidly rising incremental capital-output ratio (ICOR) in China (Figure 3). ICOR describes the number of additional units of capital input needed for producing one unit of additional GDP. The ratio was 3.5 in 2007, and it rose to 6.3 in 2015. Rapidly declining capital efficiency is truly worrisome. It might be related to the hangovers of the big stimulus package that the government implemented before. But misallocation of financial resources became an even bigger issue after the global financial crisis. As economic uncertainties stay at the escalated levels, the private enterprises deleveraged, while the SOEs leveraged, partly protected by the repressive policies and partly facilitated by the macroeconomic policies. But these led to sharp deterioration of corporate leverage quality (Wang et al. 2016).

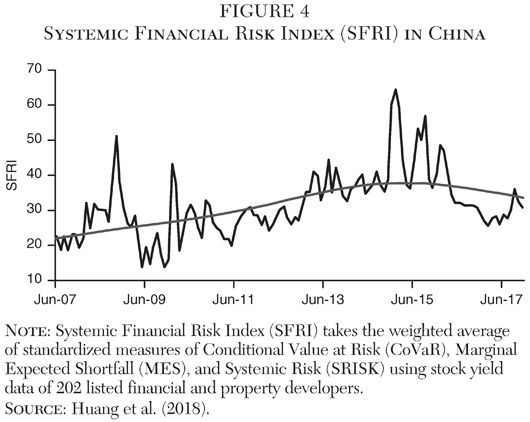

An even more worrisome development is the steady rise of financial risks. Although the Systemic Financial Risk Index (SFRI) fluctuates violently, it has been on the rise since 2008 and stays at elevated levels (Figure 4). At the macro level, there are at least three sets of factors contributing to the recent rise of SFRI. First, persistent growth slowdown led to significant deterioration of corporate balance sheets, which added to financial risks. The divergence of state and nonstate sectors’ corporate leverage ratios further exacerbated the problem. In particular, in the past, the Chinese economy grew at very rapid and stable growth rates. The authorities were able to resolve or, at least, to hide temporarily from any financial risk factors, even if they did occur. However, that is no longer possible.

Second, the government could no longer guarantee everything. In the past, the government could shield the economy from any major financial shocks. For instance, the state ownership ensured that there was no bank run in the late 1990s, even when one-third of banks were nonperforming. This is no longer possible, partly because the potential liabilities are much bigger today. Total banking assets are already more than 300 percent of GDP, while corporate debts are about 240 percent of GDP. More importantly, government liabilities, especially borrowings by the local governments and their affiliated investment platforms, have already become a source of financial risks.

Finally, the segregated financial regulatory regime could no longer keep financial risks under control. The division of labor is for the central bank and the industry regulatory commissions to be responsible for one financial sector and follows the principle that “whoever issues the license should be responsible for regulation.” This regulatory model worked reasonably well for quite a while. But when shadow banking transactions grew, regulatory gaps quickly emerged — for example, who should be responsible for regulation of banks selling insurance products? Even worse, a lot of fintech companies started businesses even without applying for a license. In addition, the fact that all regulators are responsible for both financial regulation and industry development could create conflict of interest situations for the regulatory officials.

The Chinese financial system also became inadequate in serving the real economy. On the one hand, Chinese households receive little returns to their financial assets. Total household financial assets rose from 24.6 trillion yuan in 2006 to 118.6 trillion yuan in 2016. Unfortunately, the households have very limited options for investment. Currently about 69 percent of their financial assets are in bank deposits, 20 percent in securities products, and 11 percent in pension and insurance products. The proportions of total household financial assets in bank deposits were much lower in other countries, such as 53 percent in Japan, 36 percent in Western Europe, and 14 percent in the United States. On the other hand, as the growth model shifts from mobilizing inputs to relying on innovation, the traditional bank-dominated and highly repressive financial system is no longer appropriate. Innovation and industrial upgrading are much more uncertain and risky than simple expansion of manufacturing capacity. They require technical expertise and flexibility in providing financial services to support economic development.

All these suggest that whatever financial system that worked in supporting economic growth and financial stability has probably hit its limit. Further reform and adjustments might be needed in order to support continuous economic development. Discussion so far points to needed changes in at least the following three areas. One is to develop multilayer capital markets. China’s financial system is bank dominated. And this may remain so for a very long time. But it is now critical to increase the role of the capital markets. This is necessary for providing asset-based income for Chinese households. Direct finance is also critical for supporting innovation and industrial upgrading. Two is to let market mechanisms play a decisive role in allocating financial resources. The negative consequences of government interventions have become clearer. Continuation of the “zombie” firms, for instance, not only worsens financial efficiency but also hinders industrial upgrading (Tan, Huang, and Woo 2016). And three is to improve the regulatory system to prevent systemic financial crises. The authorities have been taking actions in all these three areas. For instance, the State Council established the Financial Stability Development Committee in mid-2017 and combined the banking and insurance regulatory commission in early 2018 to strengthen policy coordination and improve regulation quality.

Toward a More Balanced View on Repressive Financial Policies

The conventional theory believes that repressive financial policies are bad. This is probably true, because government interventions often generate discrimination, reduce efficiency, hinder financial development, and increase risk. Therefore, the appropriate policy response is to remove those repressive financial policies as quickly as possible. But this assertion is conditional on the assumption that the financial system functions effectively and efficiently. If this assumption does not hold, then some government intervention may be helpful.

The Chinese experiences during the past four decades offer an important example. Despite its very high level of financial repression, China successfully engineered an economic miracle, with extraordinary economic growth and unusual financial stability. This at least suggests that, perhaps, the impacts of financial repression on economic and financial performance are not uni-directional. Indeed, empirical analyses confirm that those impacts could shift between positive and negative territories when conditions change. One of the key indicators identified in the existing studies was level of development. The real determining factors are probably efficiency of financial markets and effectiveness of regulation framework. Financial repression is bad, only with a well-functioning financial system.

In many developing and transition economies, however, this assumption of a well-functioning financial system does not hold. And if commercial banks and capital markets are not able to allocate financial resources efficiently, some government interventions may help improve effectiveness, if not efficiency, of financial transactions. More importantly, financial transactions are risky in nature, given information asymmetry. An underdeveloped financial system could easily suffer from financial crises. Here again, implicit guarantee of financial institutions and controls of the capital account may help shield the economy from internal and external financial shocks and maintain financial stability.

Therefore, repressive financial policies could have either the McKinnon effect or the Stiglitz effect on the economy and the financial system. The former is mainly negative as repressive financial policies reduce financial efficiency, slow financial development, and increase financial risks. But the latter is likely positive as those same policies could effectively channel saving into investment, underpin investor confidence, and support financial stability. Both of these effects exist in any economy, but their relative importance changes according to efficiency of the financial system and effectiveness of the regulatory regime.

These two effects can be clearly seen in the Chinese experience. Repressive financial policies were legacies of the central planning system. Their continuation during the reform period was initially the result of political compromise. In short, as it was politically not feasible to privatize all the SOEs, the government had to intervene in the financial system to provide de facto subsidies to the SOEs and support a smooth economic transition. In retrospect, however, during the first couple of decades, those repressive financial policies actually improved economic performance and supported financial stability. The Chinese economy would not have performed so well if it had given up all government interventions at the start of the reform. The former Soviet Union and many Central and Eastern European transitional economies that adopted the “shock-therapy” reform approach offered some counterexamples. These observations should offer useful implications for policy thinking in other developing and transition economies.

However, the positive effects of financial repression should not be exaggerated. Repressive financial policies strengthened economic performance because (1) the financial system was not well developed, and (2) financial liberalization continued. Even then, the impacts of financial repression turned negative recently in China, as the costs of such policies outweighed benefits. China now needs to accelerate its market-oriented reform, including developing the capital markets, revitalizing the market mechanisms, and improving the regulatory systems. Without these steps, the Chinese economy would not be able to move up the technological ladder and become a high-income economy; China could even be hit by serious financial crises.

References

Bonin, J. P., and Huang, Y. (2001) “Dealing with the Bad Loans of the Chinese Banks.” Journal of Asian Economics 12 (2): 197–214.

Fan, G. (1994) “Incremental Changes and Dual-Track Transition: Understanding the Case of China.” Economic Policy 9 (19, Supplement: Lessons for Reform): 100–22.

Huang, Y. (2001) China’s Last Step Across the River: Enterprise and Banking Reforms. Canberra: Asia Pacific Press.

__________ (2010) “Dissecting the China Puzzle: Asymmetric Liberalization and Cost Distortion.” Asia Economic Policy Review 5 (2): 281–95.

Huang, Y., and Duncan, R. (1997) “How Successful Were China’s State Sector Reforms?” Journal of Comparative Economics 24 (1): 65–78.

Huang, Y.; Gou, Q.; and Wang, X. (2014) “Financial Liberalization and the Middle-Income Trap: What Can China Learn from Multi-Country Experience?” China Economic Review 31 (December): 426–40.

Huang, Y., and Wang, X. (2011) “Does Financial Repression Inhibit or Facilitate Economic Growth? A Case Study of China’s Reform Experience.” Oxford Bulletin of Economics and Statistics 73 (6): 833–55.

__________ (2017) “Building an Efficient Financial System in China: Need for Stronger Market Discipline.” Asian Economic Policy Review 12 (2): 188–205.

Huang, Y.; Wang, X.; Wang, B.; and Lin, N. (2013) “Financial Reform in China: Progress and Challenges.” In Y. Park and H. Patrick (eds.) How Finance Is Shaping Economies of China, Japan and Korea, 44–142. New York: Columbia University Press.

Huang, Y.; Yin, J.; Xu, Z.; Ji, Z.; Hong, L.; Sun, G.; and Zhang, B. (2018) Jingshan Report: Strengthening the Market Mechanism, Constructing a Modern Financial System. Beijing: China Finance 40 Forum.

Lardy, N. R. (1998) China’s Unfinished Economic Revolution. Washington: Brookings Institution.

Lin, J. Y.; Cai, F.; and Li, Z. (1995) The China Miracle: Development Strategy and Economic Reform. Hong Kong: Chinese University of Hong Kong Press.

McKinnon, R. I. (1973) Money and Capital in Economic Development. Washington: Brookings Institution.

Naughton, B. (1995) Growing Out of the Plan: Chinese Economic Reform, 1978–93. New York: Cambridge University Press.

Stiglitz, J. E. (1994) “The Role of the State in Financial Markets.” In M. Bruno and B. Pleskovic (eds.) Proceeding of the World Bank Annual Conference on Development Economics, 1993: Supplement to the World Bank Economic Review and the World Bank Research Observer. Washington: World Bank.

Tan, Y.; Huang, Y.; and Woo, W. (2016) “Zombie Firms and Crowding-Out of Private Investment in China.” Asian Economic Papers 15 (3): 32–55.

USTR (2018) “Section 301 Report into China’s Acts, Policies, and Practices Related to Technology Transfer, Intellectual Property, and Innovation.” Washington: Office of the United States Trade Representative (March 27).

Wang, X.; Ji, Y.; Tan, Y.; and Huang, Y. (2016) “Understanding the State Advancing and the Private Sector Retreating in Corporate Leverage in China.” Paper presented at the NBER-CCER Conference on China and the World Economy, Peking University, Beijing.

World Bank (2012) China 2030: Building a Modern, Harmonious and Creative Society. Washington: World Bank.

1CCB was called People’s Construction Bank of China until 1996.

2At that time, China used a four-category bad loan classification system. After the Asian financial crisis, it adopted the international standard five-category loan classification system.