A little more than a quarter of a century has passed since the collapse of communism, which makes this an ideal time to evaluate the subsequent development of once communist nations. Which countries have moved the most toward economic liberalization? How have the former centrally planned (FCP) economies performed in recent decades? How have their political institutions evolved during the transition era and beyond? What lessons can be learned from the experience of these economies? This article will address each of those questions.

In some ways, the experience of the FCP countries constitutes a natural economic experiment. There is considerable diversity in the paths they have followed. Some moved rapidly toward economic reform and liberalization following the collapse of communism, but others moved more slowly, and still others have undertaken little or no reform. Some of the FCP countries had relatively high per capita incomes prior to the fall of communism, while others were exceedingly poor. Some experienced lengthy and painful transitions, while others made the move from central planning to markets more smoothly. Some of these countries are now highly democratic, while others are still governed by authoritarian political regimes. As we examine the experience of the FCP economies, we will do so with an eye to what can be learned about institutions, economic growth, and the development process.

The article is organized in the following manner. Section 1 examines the path of economic liberalization of 25 FCP economies from 1995 to 2015. Section 2 presents data on various indicators of economic performance during this same time frame. Section 3 focuses on the evolution of political institutions (e.g., protection of civil liberties, democracy, and control of corruption) in the FCP countries. Section 4 compares the income levels and growth rates of these economies relative to the world’s high-income countries and other developing economies. Section 5 examines the determinants of economic growth and life satisfaction for 122 countries and considers the implications for the FCP economies. Section 6 analyzes areas where the FCP economies have made substantial moves toward economic liberalization, as well as a major deficiency—low-quality legal systems—that is likely to restrain their future progress. The concluding section summarizes and considers the implications of the analysis.

Economic Liberalization and the Former Centrally Planned Economies

The Economic Freedom of the World (EFW) project provides a measure of the degree to which the institutions and policies of various countries are consistent with economic freedom (Gwartney, Lawson, and Hall 2017). This measure uses more than 40 different variables to construct a summary index of economic freedom. The EFW index now covers 159 countries and the data are available for 123 countries since 1995. This data set makes it possible to identify cross-country differences in economic freedom and to track changes across time.

The EFW index is designed to measure the degree to which the institutions of a country are supportive of (1) personal choice, (2) voluntary exchange, (3) open entry into markets, and (4) protection of individuals and their property from aggression by others. Because economic freedom facilitates and encourages gains from trade, entrepreneurship, innovation, and capital formation, economic theory indicates that it is an important source of economic growth and development. Several empirical studies have found that this is indeed the case.1 Moreover, economic freedom permits individuals to mold and shape their lives according to their preferences. Over and above the impact on income, this may enhance quality of life.2 There are 25 former centrally planned economies for which the EFW data are now available. These data are available continuously throughout the 1995–2015 period for 14 of these countries.

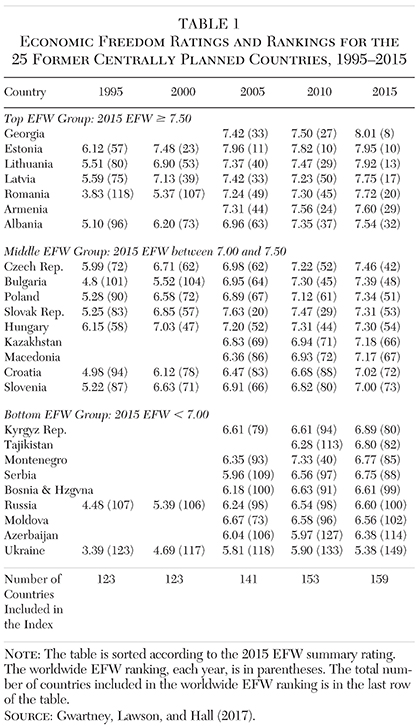

Table 1 provides the EFW summary ratings and worldwide rankings (in parentheses) for these 25 countries (when available) for 1995, 2000, 2005, 2010, and 2015. Seven of the FCP economies (Georgia, Estonia, Lithuania, Latvia, Romania, Armenia, and Albania) had a 2015 EFW summary rating of 7.5 or higher. Worldwide, these seven countries all ranked in the top quartile among the 159 countries for which the EFW data were available. Moreover, these countries have achieved dramatic increases in economic freedom. While the Baltic states all ranked in the Top 20 in 2015, in 1995 Estonia was 57th, Lithuania 80th, and Latvia 75th. Romania ranked 20th in 2015, but it was a late reformer. Romania’s worldwide ranking was 118th in 1995 and 107th in 2000 (among the 123 countries included in the index during those years). Albania has steadily improved both its rating and ranking, moving up from 96th in 1995 to 63rd in 2005 and 32nd in 2015. While the EFW data were unavailable for Georgia and Armenia in 1995 and 2000, the ratings and rankings of both have increased since 2005.

A group of nine other countries (Czech Republic, Bulgaria, Poland, Slovak Republic, Hungary, Kazakhstan, Macedonia, Croatia, and Slovenia) had 2015 EFW summary ratings between 7.0 and 7.5. Worldwide, the 2015 rankings of these countries ranged from 42nd for the Czech Republic to 73rd for Slovenia. Thus, each of these nine countries ranked in the second quartile among the 159 countries included in the EFW data set in 2015. These nine countries make up the middle group in terms of economic liberalization among the 25 FCP economies.

The Czech Republic is the highest ranked country in the middle group, and it has shown significant improvement. It ranked 42nd in 2015, up from 72nd in 1995. Other countries in this group have registered even more impressive gains in economic freedom. For example, Bulgaria’s 2015 worldwide ranking was 48th, up from 101st in 1995 and 104th in 2000. Poland ranked 51st in 2015, up from 90th in 1995 and 72nd in 2000. The ranking of the Slovak Republic rose from 83rd in 1995 to 20th in 2005, but it has subsequently receded to 53rd in 2015. The movements toward economic freedom of Hungary, Croatia, and Slovenia during 1995–2015 were more modest.

Finally, there is another set of nine FCP economies with 2015 EFW summary ratings of less than 7.0. This set of countries is composed of the Kyrgyz Republic, Tajikistan, Montenegro, Serbia, Bosnia and Herzegovina, Russia, Moldova, Azerbaijan, and Ukraine. The worldwide rankings in 2015 of these countries ranged from 80th for the Kyrgyz Republic to 149th for Ukraine. Except for Ukraine, the 2015 ranking for each of these countries placed them in the third quartile worldwide. Ukraine was in the fourth quartile. In 2015, these nine countries were the least economically free among the FCP economies. Further, there is little evidence of improvement among the countries in this group. These countries ranked in the bottom half worldwide during 1995–2005, and this was still true in 2015. The case of Russia is typical. Russia ranked 107th in 1995, 98th in 2005, and 100th in 2015.

Indicators of Economic Performance: 1995–2015

How does the performance of the FCP economies that have made more substantial moves toward economic freedom compare with those that have been slow to liberalize? In order to provide insight on this question, this section will examine the income levels, growth rates, international trade sectors, and foreign investment of the FCP economies during 1995–2015.

Per Capita GDP and Growth

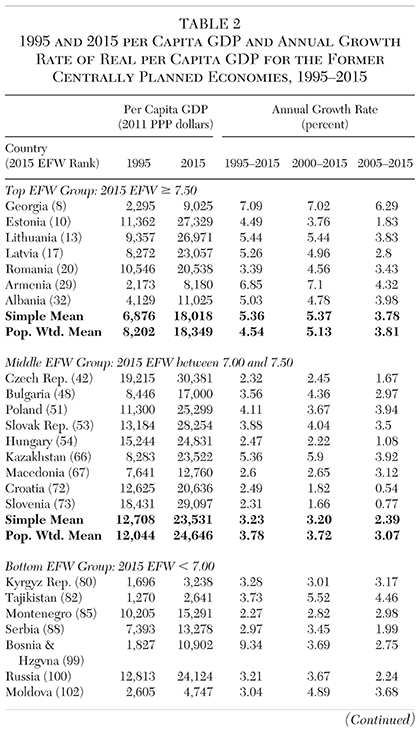

Table 2 shows the per capita GDP (2011 PPP dollars) for the high, middle, and low economic freedom FCP groups in the years 1995 (column 1) and 2015 (column 2). Within the most economically free group, the countries with the highest per capita 2015 GDP were Estonia, Lithuania, Latvia, and Romania. The 2015 per capita GDP for each of these countries exceeded $20,000. In the middle group, seven of the nine countries (Czech Republic, Poland, Slovak Republic, Hungary, Kazakhstan, Croatia, and Slovenia) all registered a 2015 per capita GDP of greater than $20,000. In this group, only Bulgaria and Macedonia failed to reach that benchmark. In the group with the lowest EFW ratings in 2015, only Russia achieved a 2015 per capita GDP of greater than $20,000. Four of the countries in this group (Kyrgyz Republic, Tajikistan, Moldova, and Ukraine) had a 2015 per capita GDP of less than $10,000.

With regard to the per capita GDP of the three groups, the simple and population weighted mean for the middle group was the highest, followed by the most-free group. The group with the lowest EFW ratings also had the lowest 2015 mean per capita income levels.

Table 2 also presents figures for the annual real growth rate of per capita GDP of the 25 countries during 1995–2015, 2000–15, and 2005–15. As column 3 shows, six of the seven countries in the most-free group had growth rates of 4 percent or higher during 1995–2015. The exception was Romania, which did not begin to liberalize until after 2000 (see Table 1). After adopting reforms supportive of economic freedom, Romania achieved an annual growth rate of per capita GDP of 4.56 percent during 2000–15. The per capita GDP annual growth rate for five of the seven countries in the most economically free group exceeded 5 percent during 1995–2015. The simple mean and population weighted growth rates for the most-free group were 5.36 percent and 4.54 percent respectively.

Among the countries in the middle group, the annual growth rates of Poland, Bulgaria, Slovak Republic, and Kazakhstan were the most impressive. However, only Poland and Kazakhstan were able to achieve an annual growth rate greater than 4 percent during 1995–2015. The simple mean annual growth of per capita GDP was 3.23 percent for the middle group, while the population weighted mean was 3.78 percent.

The simple and population weighted means for growth during 1995–2015 of the least-free group were 4.50 percent and 3.30 percent respectively. Among the eight countries in the least-free group, only Bosnia and Herzegovina and Azerbaijan were able to achieve an annual growth rate greater than 4 percent during 1995–2015. Interestingly, special circumstances underlie the growth of both of these countries. Compared to the size of its economy, Azerbaijan is the leading oil exporter among the FCP economies. The high oil prices of 2002–14 were a major factor underlying its strong growth. The 1995 per capita GDP of Bosnia and Herzegovina was depressed by the aftermath of civil war, and therefore its 9.34 percent annual growth rate during 1995–2015 was elevated. Its real growth rates of 3.69 percent and 2.75 percent during 2000–15 and 2005–15 respectively are more indicative of its long-term growth path.

The FCP countries that liberalized the most generally grew more rapidly during 1995–2015 than their counterparts that were slow to reform. Consider the number of countries in each of the three groups that achieved an annual growth rate of at least 4 percent during the two-decade time frame. Six of the seven countries in the most economically free group achieved this benchmark, but only two of the nine countries in the middle group and only two of the eight countries in the least-free group were able to achieve this figure. Moreover, the population weighted mean annual growth rate of the most-free group was 4.54 percent, compared to 3.78 percent for the middle group and 3.30 percent for the least-free group.

Like column 3, columns 4 and 5 of Table 2 present growth data; the difference is that the length of the periods examined are 15 years (2000–15) and 10 years (2005–15). The growth figures for 2000–15 have a similar pattern as those for the 20-year period. The population weighted mean annual growth rate of per capita GDP during 2000–15 of the most-free group was 5.13 percent, compared to 3.72 percent for the middle group, and 3.83 percent for the least-free group. Again, the mean growth rates of the middle and least-free group are elevated by the high growth rates of the oil exporting countries of Kazakhstan and Azerbaijan. Comparison of the 15- and 20-year growth figures for Romania and Bulgaria also highlights an interesting point. As Table 1 indicates, these countries were late reformers. Neither undertook significant reforms until after 2000. Note, their growth rates were higher during 2000–15 than for 1995–2015.

Comparison of the growth rates across the three periods also highlights a key point: the growth rates of the most recent decade were generally lower than for the earlier periods. Only two countries—Macedonia and Montenegro—had a higher growth rate of real per capita GDP in the most recent period, 2005–15, than during the two longer time frames. This illustrates that the growth rates of most of these economies have slowed in recent years. Nonetheless, the annual growth rate of per capita GDP during 2005–15 of 10 of the 25 FCP countries (Georgia, Lithuania, Armenia, Albania, Poland, Kazakhstan, Slovak Republic, Tajikistan, Moldova, and Azerbaijan) exceeded 3.5 percent. Thus, while growth has generally slowed, it remains relatively strong among these economies. As we proceed, the relationship between economic freedom and the growth rate of the FCP economies will be examined in more detail.

Growth of the Trade Sector

International trade promotes gains from specialization, economies of scale, and importation of innovative products and production methods. Further, international trade makes it possible for both consumers and producers in a domestic economy to gain from greater integration into the worldwide network of markets. Thus, economic analysis indicates that trade openness and expansion in trade will elevate economic growth.

The ratio of exports plus imports divided by GDP provides a straightforward measure for the size of the trade sector. Comparison of the beginning and ending time frames provides insight on changes in the size of the trade sector over the two-decade period.

Except for Armenia, all the countries in the most economically free group experienced substantial increases in trade as a share of GDP. The mean size of the trade sector for this group rose from 79.5 percent during 1996–2000 to 111.9 percent in 2011–15, an increase of 40 percent. The countries in the middle group also experienced sizable expansions in international trade. On average, trade as a share of GDP for this group rose from 86.4 percent during 1996–2000 to 125.0 percent during 2011–15, an increase of approximately 45 percent. Clearly the countries in both the top and middle groups in terms of economic freedom experienced substantial increases in the size of their trade sectors. However, the situation was quite different for the least economically free group. Only three of the nine countries in this group—Kyrgyz Republic, Montenegro, and Serbia—experienced significant expansions in trade. The size of the trade sector for the other six countries in this group was either similar or smaller in 2015 than in the late 1990s. The mean for this group was 93.1 percent in 2011–15, virtually unchanged from 93.7 percent in 1996–2000.

Eight FCP countries (Czech Republic, Estonia, Hungary, Latvia, Lithuania, Slovak Republic, Slovenia, and Poland) joined the European Union (EU) in 2004, and two others (Romania and Bulgaria) joined in 2007. Still later, Croatia joined the EU in 2013. In addition to its central government functions, the EU is a customs union. In fact, it is an outgrowth of a free trade agreement among several European countries. The EU sets common tariff rates and international trade policy for all member countries, but there are no tariffs or restrictions on the movement of goods within the union.

Joining the EU will generally reduce trade barriers and enhance the size of the trade sector of an FCP country. There are two reasons why this will be the case. First, joining the EU will provide domestic consumers and producers with a vastly larger “free trade” market. Thus, trade with partners in other EU countries will generally increase. Second, because tariff rates and other trade restrictions imposed by the EU are relatively low, the trade barriers with non-EU members will also tend to decline. This will be particularly true if the trade restrictions of the joining member were high prior to membership in the union.

Did joining the EU reduce trade barriers and lead to an expansion in trade? There is evidence this was the case. All ten of the FCP countries that joined the EU during 2004–07 had substantially larger trade sectors in 2011–15 than during 1996–2000. Further, the increases in the size of their trade sectors were exceedingly large. For example, between 1996–2000 and 2011–15, international trade as a share of GDP soared in Lithuania from 88 percent to 159 percent. In the Czech Republic, the size of the trade sector rose from 87 percent to 151 percent; in the Slovak Republic, the increase was from 110 percent to 180 percent; in Poland, the parallel increase was from 53 percent to 91 percent. Similarly, between 1996–2000 and 2011–15 the trade sector of Hungary rose from 107 percent to 169 percent and that of Slovenia soared from 97 percent to 144 percent. Latvia and Bulgaria experienced similar large increases in the size of their trade sectors soon after joining the EU. Moreover, the expansions in the trade sector of the FCP countries that joined the EU were substantially greater than those achieved by the non-EU FCP countries. These trade increases are consistent with the view that joining the EU reduced trade barriers, enhanced international trade, and promoted integration into the world economy.

Foreign Direct Investment

Foreign direct investment (FDI) plays a key role in the growth process. There are several reasons why this is the case. First, almost all FDI is private. Thus, it reflects investor confidence in the institutions and future of a country. Second, FDI is an important source of innovation and technology transfers among countries. This is particularly important for developing economies because they often lag well behind their higher-income counterparts in these areas. Finally, FDI is also a source of financing for capital investments, an ingredient that is often in short supply in lower-income, developing economies.

Net FDI as a share of GDP during 1995–2015 was derived for the 25 FCP economies. FDI increased as a share of GDP in most of these economies during the first decade of this century, but it has declined substantially since 2010. For example, the average net FDI as a share of the economy for the seven countries with the highest EFW ratings rose from 4.6 percent during 1996–2000 to 5.4 percent in 2001–05 and 7.5 percent in 2006–10, but it then receded sharply to 4.6 percent during 2011–15. Further, this pattern—elevated levels of net FDI during 2001–10, but declines during the past five years—was present for the mean values of the other two groups. The declining levels of net FDI as a share of the economy are a troubling sign. This is likely to slow the rate of future economic growth.

Economic Record of the FCP Countries

The economic record of the FCP countries during 1995–2015 was impressive. This was particularly true for the seven FCP countries that moved the most toward economic liberalization. The average growth of real per capita GDP of these seven countries exceeded 5 percent during 1995–2015. Real per capita GDP more than doubled in six of these seven countries during the two decades. The late-reforming Romania was the exception, and its per capita GDP almost doubled (it increased by 95 percent) in just 15 years following adoption of liberal reforms early in this century. While the real GDP growth of the middle group was slower, it was still impressive. Most of the countries in the most-free and middle group experienced large increases in international trade, an in-flow of FDI, and rapid growth rates. Economic growth, expansion in international trade, and FDI lagged in most of the least-free economies, but even this group achieved a population weighted annual growth of per capita GDP of 3.3 percent during 1995–2015.

Civil Liberties and Political Institutions

The FCP economies have a history of authoritarianism, political corruption, and abuse of civil liberties. Thus, sensitivity to the operation of political institutions is an issue of considerable importance.

Freedom House has provided ratings for both civil liberties and political rights annually since 1972. The Freedom House rating scale ranges from 1 (most free) to 7 (least free). Countries with a rating of 1 or 2 are classified as “free,” 3, 4, or 5 as “partly free,” and 6 or 7 as “not free.”

Freedom House classifies seven of the 25 FCP economies as free for both civil liberties and political rights throughout the entire period. These seven countries are Estonia, Lithuania, Latvia, Czech Republic, Poland, Hungary, and Slovenia. By 2015, Romania, Bulgaria, Slovak Republic, Croatia, and Serbia joined the “free” group for both civil liberties and political rights. Except for Serbia, all of the countries with civil liberties and political rights classifications as “free” are from the two groups with the highest EFW ratings. Moreover, other than Serbia, none of the countries in the bottom EFW group was classified as “free” in both civil liberties and political rights during any of the years. Freedom House rates Tajikistan, Russia, and Azerbaijan as “not free” in both civil liberties and political rights in 2015. The ratings for Russia are particularly interesting because of their persistent deterioration. Russia’s civil liberties rating was 4 in 1995, 5 during 2000–10, and 6 in 2015. In political rights, Russia’s rating receded from 3 in 1995 to 5 in 2000, and 6 during 2005–15.

The Polity IV data set (Marshall, Gurr, and Jaggers 2016) provides information on both democracy and constraints on the executive. The scale for the democracy variable ranges from minus 10 (strongly autocratic) to plus 10 (strongly democratic). The Polity IV data indicate that most of the FCP economies moved toward democracy during 1995–2015. By 2015, only three countries, Kazakhstan, Tajikistan, and Azerbaijan, were classified as autocratic (negative rating). Most of the 25 countries have positive ratings of 8 or more. In the most economically free group, only Georgia and Armenia had a 2015 rating of less than 8, and in the middle group, only Kazakhstan failed to meet this benchmark. However, in the least-free group, five countries—Kyrgyz Republic, Tajikistan, Russia, Azerbaijan, and Ukraine—had democracy ratings of less than 8.

The scale of the polity data for constraints on the executive variable ranges from 1 (no limitations on executive actions) to 7 (accountability groups such as legislatures have the power to constrain executive actions). As in the case of democracy, the ratings for constraints on the executive were higher in 2015 than was true two decades earlier. In 2015, all countries of the most-free group had ratings of 7 except for Georgia (rating of 6) and Armenia (rating of 5). In the middle group, eight of the nine countries had a rating of 7; the exception was Kazakhstan with a rating of 2. In the least-free group, four of the nine countries—Kyrgyz Republic, Montenegro, Serbia, and Moldova—had a rating of 7. However, the constraints on the executive were weak for four other countries in this group: Tajikistan (rating of 3), Russia (rating of 4), Azerbaijan (rating of 2), and Ukraine (rating of 5). While there are countries with democratic political institutions in each of the three groups, countries in the least economically free group are more likely to be less democratic and have weaker constraints on the executive.

Transparency International (2015) provides data on corruption, which is defined as “the abuse of public office for private gain.” These data are used to develop the Corruption Perception Index (CPI). The CPI ranges from 0 (highly corrupt) to 100 (highly clean). The CPI increased for almost all of the 25 FCP economies, indicating a reduction in the level of corruption. The CPI was unavailable for a number of countries in 1995 and 2000. Thus, we will focus on the ratings during 2005–15. For the most-free group, the average CPI increased from 37.1 in 2005 to 50.7 in 2015. For the middle group, the average CPI rose from 39.8 in 2005 to 49.1 in 2015. For the least-free group, the average CPI rose from 25.3 in 2005 to 32.7 in 2015. The 2015 average CPI is considerably higher for groups 1 and 2 than for group 3. The following four countries had a 2015 CPI of 60 or higher: Estonia (70), Lithuania (61), Poland (62), and Slovenia (60). In contrast, the 2015 CPI was less than 30 for the following countries: Kazakhstan (28), Kyrgyz Republic (28), Tajikistan (26), Russia (29), Azerbaijan (29), and Ukraine (27). Note that all four of the countries with the highest 2015 CPI are from the two groups with the highest 2015 EFW ratings. In contrast, five of the six countries (Kazakhstan is the exception) with the lowest 2015 CPI are from the group with the lowest 2015 EFW rating.

Pulling the data on political institutions together, the following nine countries had 2015 political institutions most consistent with protection of civil liberties, political democracy, and absence of corruption: Estonia, Lithuania, Latvia, Czech Republic, Poland, Slovak Republic, Hungary, Croatia, and Slovenia.3 In contrast, the political institutions of Kazakhstan, Tajikistan, Russia, and Azerbaijan were most inconsistent with civil liberties protection, political democracy, and absence of corruption.

The Income of the FCP Economies Compared to the World’s High-Income Countries and Other Developing Economies

This section will compare the relative per capita GDP of the FCP economies with the 21 high-income countries and the 82 other developing economies for which the economic freedom data were available for 1995–2015. The FCP countries with the highest income levels were Estonia, Lithuania, Czech Republic, Slovak Republic, and Slovenia. By 2015, the per capita GDP for each of these five countries had risen to 60 percent or more of the mean for the 21 high-income countries. The countries with the lowest 2015 income levels were Armenia, Kyrgyz Republic, Tajikistan, Moldova, and Ukraine. The per capita GDP of each of these five countries was less than 20 percent of the comparable mean for the high-income group.

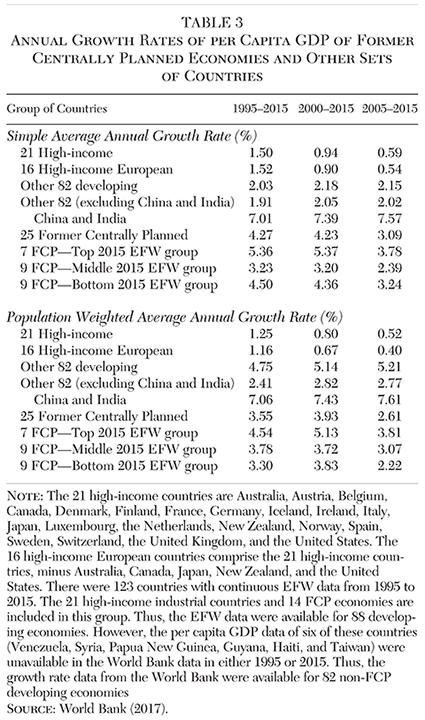

Table 3 provides the annual growth rate of per capita GDP for the 21 countries in the high-income group, 16 high-income European countries, and for the 82 non-FCP developing economies. The per capita growth data are also provided for the 25 FCP economies according to their 2015 EFW summary rating. Both the simple and population weighted mean growth rates are provided for three different time periods—1995–2015, 2000–15, and 2005–15.

How do the growth rates of the FCP countries compare to the other groups? As Table 3 shows, the centrally planned economies grew more rapidly than the high-income countries throughout the 1995–2015 period. For example, the simple mean annual growth rate of the top, middle, and bottom groups (according to 2015 EFW ratings) were 5.36 percent, 3.23 percent, and 4.5 percent, respectively. Each of these rates was well above the simple mean of 1.5 percent for the world’s 21 high-income countries and the 1.52 percent annual growth rate for the 16 high-income European countries. The population weighted mean annual growth rates for the top (most free), middle, and bottom (least free) FCP groups during 1995–2015 were 4.54 percent, 3.78 percent, and 3.3 percent, respectively. Again, these annual growth figures are all considerably higher than the 1.25 percent for the 21 high-income countries of the world and 1.16 percent for the 16 European countries. When these comparisons are also made for the 2000–15 and 2005–15 periods, the pattern of the results is the same: the growth rate for each of the FCP groups exceeds that of the high-income countries.

Turning to a comparison between the FCP economies and the other 82 developing countries, the simple average annual growth rate of the FCP groups nearly always exceeds the simple average for the 82 developing economies. For example, the simple mean annual growth rate for 1995–2015 of the 82 developing economies was 2.03 percent, compared to the annual growth rates of 5.36 percent, 3.23 percent, and 4.50 percent for the top, middle, and bottom FCP groups. The pattern was similar for the 15- and 10-year comparisons: the simple average annual growth rates of the FCP economies were generally greater than the simple average for the 82 developing countries.

However, the pattern changes when the population weighted figures are used for the comparisons. The population weighted mean annual growth rates for the 82 developing economies are generally greater than the parallel rates for the FCP countries. For example, the population weighted mean annual growth rate for the 82 developing countries during 1995–2015 was 4.75 percent compared to 4.54 percent, 3.78 percent, and 3.30 percent for the top, middle, and bottom groups among the FCP economies. The population weighted growth rates for the 82 developing economies are driven by the high growth rates of China and India, the world’s two most populous countries. When these two countries are omitted from the developing group, the mean annual growth rate of the remaining 80 countries is substantially lower. When the FCP groups are compared with the developing countries without China and India, the growth rates of the FCP economies are generally higher than those of the 80 developing economies.

To summarize: the growth rates of the FCP economies are generally higher than the growth rates of the world’s 21 high-income countries, the 16 high-income European economies, and the developing economies of the world, except for China and India. This pattern holds for both the simple average and the population weighted average growth rates and for each of the three periods.

Determinants of Economic Growth and Life Satisfaction

A regression model of economic growth was developed and tested across 122 countries.4 The dependent variable was the annual growth rate of real per capita GDP. The analysis was conducted for three periods: 1995–2015, 2000–15, and 2005–15. The lengthier time frames, particularly the 15- and 20-year periods, will minimize the impact of business cycle factors on the measurement of long-term growth. The model included the following variables with the expected sign indicated in parentheses: 1995 per capita GDP (minus), economic freedom (plus), log of population (plus), initial percentage of female population in prime working age 25–59 group5 (plus), change in the percentage of this population during the period (plus), net foreign direct investment as a share of GDP (plus), net fuel exports as a share of GDP (plus), dummy for Middle East oil exporters (minus), and dummies for the 82 less developed countries and the three categories of FCP economies (uncertain). All of the continuous variables had the expected signs and were significant at the 90 percent level or higher. The model explained approximately two-thirds of the variation in the annual growth rate of per capita GDP of the 122 countries during the 15- and 20-year periods.

The economic freedom variable was included in two forms: (1) 1995 EFW summary rating and change in the EFW rating from 1995 to 2015 and (2) average EFW summary rating during the 1995–2015 period. The economic freedom variables were always positive and significant (in most cases, at the 99 percent confidence level). This indicates that economic freedom exerts a positive and highly significant impact on economic growth, even after accounting for the other factors included in the model. The dummy variable for the FCP group with a 2015 EFW rating above 7.5 was always significant, indicating that the growth rates of these seven countries were more rapid than the world’s 21 high-income countries. The regression analysis provides additional evidence that (1) economic freedom exerts a strong impact on economic growth and (2) the FCP economies liberalizing the most grew more rapidly than those that liberalized by lesser amounts.

In addition to income, it is also important to analyze the factors underlying life satisfaction. Regression analysis was used to examine the determinants of life satisfaction, as measured by the World Values Survey (Institute for Comparative Survey Research 2017). A set of personal attributes (such as employment, relative income, gender, and age) and country-specific measures including the summary EFW rating, per capita GDP, the Polity IV democracy score, and language fractionalization were incorporated as independent variables. The results indicate that economic freedom exerts a significant positive impact on life satisfaction both directly and indirectly (through per capita GDP). While the life satisfaction of persons living in FCP countries was well below that of similar individuals in other countries during the 1990s, the gap has declined, and by 2010–2014 it was virtually eliminated.6

Area Ratings and Identifying the Strengths and Weaknesses of the FCP Economies

In addition to the summary rating, the EFW data provide country ratings for five areas: (1) size of government, (2) legal structure and protection of property rights, (3) access to sound money, (4) international exchange, and (5) regulation of credit, labor, and business. The area ratings provide insights on both the strengths and weaknesses of economies. They also make it possible to track the source of changes in economic freedom of the FCP economies and compare their ratings with other European countries.

Table 4 provides the mean area ratings in each of the five areas for both the FCP economies and the 16 high-income European countries during 1995–2015. Looking at the mean ratings for Areas 1, 3, 4, and 5, we find that, in each of these areas, the mean rating of the FCP economies rose substantially during 1995–2015; their ratings also improved relative to the 16 high-income European countries. The high-income countries have low ratings in Area 1 (size of government). Thus, in this area, the mean rating for the FCP economies was higher than the mean for the high-income European countries. Moreover, the difference expanded during the two decades. In areas 3, 4, and 5 the mean ratings of the FCP countries were persistently lower than those of the European 16. However, the mean rating of the FCP countries rose steadily throughout 1995–2015 and the gap compared to the high-income European group narrowed. In Area 3 (access to sound money) the rating improvement was huge and the narrowing of the gap dramatic. In 1995, the mean rating of the FCP countries was only 3.27 compared to 9.63, a gap of 6.63 units. By 2015, however, the mean Area 3 rating of the FCP countries had risen to 8.75 and the gap narrowed to only 0.76 units. While the gains were smaller for areas 4 (international exchange) and 5 (regulation), the pattern was the same: the mean rating of the FCP group rose substantially and the gap compared with the high-income European countries narrowed.

Turning to Area 2 (legal structure and protection of property rights), we find that, in contrast with the other four areas, the mean rating of the FCP countries changed little in this area. The mean Area 2 rating of the FCP economies was 5.68 in 1995, 5.45 in 2005, and 5.48 in 2015. Further, the gap relative to the high-income European economies was 2.13 units in 1995, but it had expanded to 2.40 units in 2015.

Perhaps the patterns observed in Table 4 are unduly influenced by the FCP countries that have largely failed to move toward liberalization. In order to see if this is the case, the mean area ratings were also derived for only the 11 FCP countries that are now part of the EU.7 None of these countries was in the least-free group of the FCP countries. Thus, with only a few exceptions, these countries are the most economically liberal of the FCP economies.

When only these 11 FCP countries are considered, the pattern is the same as that of Table 4. The mean ratings of the 11 FCP economies increased substantially in Areas 1, 3, 4, and 5, and improved relative to the high-income European countries. But once again the situation for Area 2 was dramatically different. The mean Area 2 rating for the 11 FCP countries that are now EU members changed only slightly during the two decades. The mean Area 2 rating for this group rose from 5.97 in 1995 to 6.06 in 2005 and 6.09 in 2015. Moreover, the Area 2 mean rating of these countries was approximately two units less than the figure for the high-income European countries throughout the two decades.

Weakness in the legal structure area is a major problem for almost all of the FCP economies.8 Only one of the 25 FCP economies had a 2015 Area 2 rating above 7. Estonia’s Area 2 rating in 2015 was 7.51, but the next highest Area 2 rating among the FCP group in 2015 was Georgia with a rating of 6.57. Only seven of the FCP economies (Georgia, the three Baltic countries, Czech Republic, Hungary, and Slovenia) had Area 2 ratings of more than 6 in 2015. Thus, 18 of the 25 FCP economies had Area 2 ratings of two or more units below the 16 high-income European countries. Moreover, there is evidence that the situation is worsening in several countries. For example, Poland’s Area 2 rating in 2015 was 5.89, down from 6.21 in 2010. The Area 2 rating of the Slovak Republic was 5.78 in 2010 and 5.64 in 2015, down from 6.63 in 2005. Hungary’s Area 2 rating fell from 6.66 in 2005 to 6.04 in 2015.

As we have shown, the FCP economies have grown rapidly and closed the income gap relative to the high-income countries of both Europe and the world. However, unless the deterioration in the legal structure of these countries is reversed and improved, it is unlikely these countries will continue to grow rapidly and close the income gap relative to high-income countries.

The legal system of a country is vitally important for sustained growth and achievement of a high per capita income. If investors—domestic as well as foreign—cannot count on protection of property rights and unbiased enforcement of contracts, they will be reluctant to undertake capital projects. In turn, weak investment will slow not only capital formation, but also entrepreneurial activities, dissemination of technology, and dynamic growth. There is already some evidence that this is happening in the FCP countries. Net FDI fell sharply during 2011–15. As Table 2 shows, the growth of per capita real GDP during the past five years has slowed. Perhaps these changes are caused by other factors, but they are precisely the outcomes one would expect from a poorly operating legal system.

Major Implications and Lessons for the Future

The fall of communism and the subsequent institutional change provide researchers with a natural experiment. The 25 countries involved in this analysis were diverse and they often chose different transitional paths. What are the most important lessons that can be learned from an examination of the changing institutional framework and accompanying performance of these economies? Four major factors stand out.

First, the experience of the FCP countries indicates that economic freedom enhances growth. The FCP economies that chose a course more consistent with economic freedom grew more rapidly than those that were less free. Five of the seven most-free FCP economies achieved a robust annual growth rate of per capita GDP of more than 5 percent during the 20-year period from 1995 to 2015. The most-free group systematically achieved a higher mean growth rate than the middle and least-free groups. Further, consider the economic record of the 11 countries with the highest 2015 EFW summary ratings. These countries include late reformers such as Romania and Bulgaria, which did not begin the reform process until after 2000. During 2000–15, nine of these 11 countries achieved an annual growth rate of real per capita GDP of more than 4 percent. In contrast, only four of the 14 FCP countries with lower 2015 EFW summary ratings were able to achieve annual growth rates of more than 4 percent. Moreover, the high growth rates of two of the four (Kazakhstan and Azerbaijan) were elevated by the increasing and abnormally high oil prices during 2002–14. In addition, regression analysis indicates that, other things constant, economic freedom exerts a positive and statistically significant impact on growth of per capita GDP. This was true for countries throughout the world and for the most-free FCP economies.

Second, the FCP economies with more economic freedom experienced larger expansions in international trade and attracted more FDI than those with less economic freedom. The increases in the size of the trade sector of relatively free FCP economies such as Georgia, Lithuania, Latvia, Albania, Czech Republic, Bulgaria, Poland, and the Slovak Republic were truly remarkable. Even though FDI as a share of the economy receded during 2011–15, it was strong during the first decade of this century.

Third, during 1995–2015, the political institutions of most FCP economies moved toward the protection of civil liberties, democratic decisionmaking, and better control of corruption. The following nine countries had 2015 political institutions most consistent with civil liberties protection, political democracy, constraints on the executive, and absence of corruption: Estonia, Lithuania, Latvia, Czech Republic, Poland, Slovak Republic, Hungary, Croatia, and Slovenia. In contrast, the political institutions of Kazakhstan, Tajikistan, Russia, and Azerbaijan were least consistent with protection of civil liberties, democratic principles, and absence of corruption.

Fourth, the economic freedom area ratings of the FCP countries increased substantially in areas 1 (size of government), 3 (access to sound money), 4 (international trade) and 5 (regulation of finance, labor, and business) during 1995–2015. The improvements in these four areas have narrowed the economic freedom gap of the FCP economies relative to the 16 high-income European countries. In these four areas, the economic freedom ratings of the FCP countries, particularly the eleven that are now members of the EU, are approximately the same as the ratings of the high-income European countries. However, there is a huge gap in the quality of the legal systems (Area 2) of the FCP countries compared to the high-income countries of Europe. Moreover, the FCP countries have failed to improve in this area. Unless the FCP countries improve their legal systems, their future growth is likely to slow and their gains relative to high-income countries come to a halt in the near future.

Looking back, the record of the FCP economies, particularly those that have moved toward economic liberalization, is one of growth, integration into the world economy, and increasingly democratic political decision-making. Looking forward, improvement in the legal systems of these countries is crucially important for the continuation of economic growth and rising living standards.

References

Berggren, N. (2003) “The Benefits of Economic Freedom: A Survey.” Independent Review 8 (2): 193–211.

Bjørnskov, C.; Dreher, A.; and Fischer, J. A. V. (2010) “Formal Institutions and Subjective Well-Being: Revisiting the Cross-Country Evidence.” European Journal of Political Economy 26 (4): 419–30.

Dawson, J. W. (1998) “Institutions, Investment, and Growth: New Cross-Country and Panel Data Evidence.” Economic Inquiry 36 (4): 603–19.

(2003) “Causality in the Freedom-Growth Relationship.” European Journal of Political Economy 19 (3): 479–95.

Faria, H. J., and Montesinos, H. M. (2009) “Does Economic Freedom Cause Prosperity? An IV Approach.” Public Choice 141 (1): 103–27.

Feldmann, H. (2017) “Economic Freedom and Human Capital Investment.” Journal of Institutional Economics 13 (2): 421–45.

Freedom House (2017) Freedom in the World, 2017 Report. New York: Freedom House.

Gwartney, J.; Lawson, R.; and Hall, J. (2017) Economic Freedom of the World: 2017 Annual Report. Vancouver: Fraser Institute.

Institute for Comparative Survey Research (2017) “World Values Survey.” Available at www.worldvaluessurvey.org.

Marshall, M.; Gurr, T. R.; and Jaggers, K. (2016) “Political Regime Characteristics and Transitions, 1800–2016.” Polity™ IV Project. Available at www.systemicpeace.org.

Nystrom, K. (2008) “The Institutions of Economic Freedom and Entrepreneurship: Evidence from Panel Data.” Public Choice 136 (3): 269–82.

Pitlik, H., and Rode, M. (2016) “Free to Choose? Economic Freedom, Relative Income, and Life Control Perceptions.” International Journal of Wellbeing 6 (1): 81–100.

Rode, M. (2013). “Do Good Institutions Make Citizens Happy, or Do Happy Citizens Build Better Institutions?” Journal of Happiness Studies 14 (5): 1479–1505.

Transparency International (2016) “Corruption Perceptions Index.” Available at www.transparency.org/news/feature/corruption_perceptions_index_2016.

World Bank (2017) “World Development Indicators.” Available at databank.worldbank.org/wdi.

1See for example Berggren (2003), Dawson (1998, 2003), Faria and Montesinos (2009), Feldmann (2017), and Nystrom (2008).

2For analysis of this topic, see Bjørnskov, Dreher, and Fischer (2010); Pitlik and Rode (2016); and Rode (2013).

3In 2015, these countries had civil liberties and political rights ratings of 1 or 2; democracy scores of 8, 9, or 10; constraints on the executive of 6 or 7; and a CPI of 50 or more.

4The regression equations can be found in Table 15 of the full report, available at https://coss.fsu.edu/hilton/sites/default/files/1b.%20FCP%20economies%20-%20Complete%20Study.pdf.

5The female population was chosen instead of total population because it more accurately reflects the latent composition of the population, which is sometimes contaminated by in-migration of workers, most of whom are male.

6The regression analysis of life satisfaction can be found in Table 16 of the full report, available at https://coss.fsu.edu/hilton/sites/default/files/1b.%20FCP%20economies%20-%20Complete%20Study.pdf.

7These countries are Czech Republic, Estonia, Hungary, Latvia, Lithuania, Slovak Republic, Slovenia, Poland, Romania, Bulgaria, and Croatia.

8Given the historic background, the weakness of the legal systems of the FCP economies is understandable. Under communism, judges, lawyers, and other judicial officials were trained and rewarded for serving the interests of the government. Protection of the rights of individuals and private businesses and organizations was not important. Given this background, development of an independent legal system capable of checking the powers of the executive, protecting individuals and their property, and enforcing contracts even-handedly is a challenging task.