U.S. monetary policy has undergone a lot of change over the past decade, including the arrival of large-scale asset purchases (LSAPs), the elevated use of forward guidance, and a switch from a corridor to a floor operating system.

One area that has not changed is the Fed’s basic operating framework, defined here as the instruments, tools, and targets the Fed uses in its conduct of monetary policy. The Fed’s operating framework for the past few decades has been geared toward a positive interest rate environment and an inflation target.1 This framework has become, however, increasingly strained over the past decade as the secular decline in interest rates has pushed U.S. interest rates closer to zero percent and as the Fed’s inflation targeting failed to foster a robust recovery after the Great Recession.

This article makes the case that there is an urgent need to upgrade the Federal Reserve’s operating framework to the realities of the 21st century. To do this, the Fed needs to make several important changes. First, it needs to adjust its operating framework so that it is robust to both positive and negative interest rate environments. Second, the Fed needs to tie its operating framework to a level target so that it can do meaningful forward guidance. Finally, the Fed’s operating framework needs the enhanced credibility that comes by providing the Fed explicit but constrained access to a standing fiscal facility at the zero lower bound.

This article outlines a proposal that accomplishes this goal and does so in a manner that would encourage the Federal Reserve to act in a more systematic, rules-based, accountable manner. The article motivates this proposal by looking back at two important macroeconomic developments of the past decade and then considers what they mean for the future of U.S. monetary policy. First, it looks at the secular decline in interest rates; then it reviews the accomplishments of the large-scale asset purchase programs, also known as quantitative easing (QE), undertaken by central banks. Both developments suggest that conventional and unconventional monetary policy will have limited effectiveness in the economic environment likely to prevail in the future. Moreover, they indicate that unless significant changes are made to the Federal Reserve’s operating framework, U.S. monetary policy will be largely impotent during future recessions.

The Secular Decline of Interest Rates

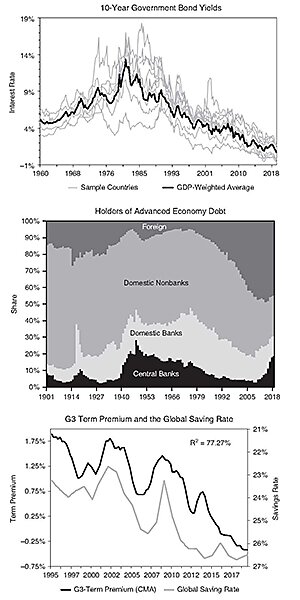

The first important development that became apparent over the past decade is that interest rates have been on a secular decline. This development has been going on since the 1980s but intensified and became more obvious in the wake of the Great Recession. For some advanced economies like the eurozone, Japan, and Switzerland, this decline has resulted in sustained negative interest rates across much of their yield curves.2 Other economies, like the United States, which have not yet joined the negative interest rate camp, appear headed in that direction.3 The top chart of Figure 1 highlights this development for 11 advanced economies: Australia, Canada, the eurozone, Israel, Japan, New Zealand, Norway, Sweden, Switzerland, United Kingdom, and the United States. It shows a GDP-weighted average of each country’s 10-year government bond yield. It now sits near 0.5 percent and should hit 0.0 percent in 2022 given its average pace of decline over the past few years.

FIGURE 1: SECULAR DECLINE OF SAFE ASSET YIELDS

NOTE: Data sources are listed in the Appendix.

Some observers attribute this decline to central banks keeping interest rates low, but the next two charts in Figure 1 suggest there are far bigger forces at work.4 The second chart shows the holders of debt securities issued by advanced economies. It reveals that while central bank holdings have increased because of QE programs in the past decade, there has been a greater and longer change in foreign holdings of advanced economy debt. The third chart shows a consequence of this shift: a rising global saving rate (inverted on the graph) driving down the term premium on government bonds in advanced economies. These last two charts tell a story of global investors increasingly investing their savings in advanced economies and, in turn, driving down their interest rates. This well-documented phenomenon is generally attributed to a global shortage of safe assets (Caballero, Farhi, and Gourinchas 2017; Caballero 2018).

Safe assets are debt instruments that are expected to preserve their value in adverse systemic events. They also provide liquidity services and can be viewed as a form of money. As a result, investors are willing to pay a premium for their “convenience yield” (Krishnamurthy and Vissing-Jorgensen 2012; Gorton 2017). The biggest sources of safe assets are government bonds from advanced economies, especially U.S. Treasuries. The global demand for them has far outstripped their supply, and this has led to the global safe asset shortage problem.

This shortage has arisen and persisted for several reasons. First, globalization has spurred rapid economic growth in emerging markets, but it has not increased their ability to create safe stores of value. Consequently, these countries have turned to advanced economies for safe assets.5 Second, many parts of the world are aging and, as a result, shifting their portfolios away from riskier assets to safer ones. Third, financial crises starting with the emerging markets in the 1990s and continuing through the global financial crisis of 2008 and the eurozone crisis of 2010–2014 have increased risk aversion and, thereby, further raised demand for safe assets. New financial regulations coming out of these crises have also raised demand for safe assets by financial firms. Finally, the uncertainty surrounding President Trump’s trade war has also strengthened demand for safe assets.

Most of these developments are structural and likely to persist.6 Moreover, they can become self-perpetuating and lead to what Caballero, Farhi, and Gourinchas (2017) call a “safety trap.” This problem emerges when the excess demand for safe assets pushes down safe asset yields to the effective lower bound (ELB) on interest rates. If the excess demand for safe assets is not satiated at that point (i.e., the equilibrium real safe asset interest rate is below the ELB), then aggregate demand will contract and push down inflation. Via the Fisher relationship, the lower inflation will drive up the real safe asset interest rate and increase the spread between it and the equilibrium real safe asset interest rate. As a result, aggregated demand will further contract and the cycle will repeat.7 This is the safety trap.

The safe asset shortage, then, is causing a secular decline in interest rates and, via arbitrage in global capital markets, making it a global phenomenon (Del Negro et al. 2018). This is why the downward march of interest rates is happening to all advanced economies and is putting downward pressure on their yield curves. Some economies, such as Japan, the eurozone, and Switzerland, already have much of their yield curve at negative values. The U.S. economy is not far behind and is likely to see further downward pressure on its yield curve (Tukker 2019).

Large-Scale Asset Purchase Programs

The second big development of the past decade was the use of LSAPs by central banks in advanced economies, beginning with the Federal Reserve in late 2008. These central banks resorted to LSAPs after conventional monetary policy ran up against the ZLB on interest rates. This so-called unconventional monetary policy was used to provide additional stimulus to aggregate demand in the wake of the Great Recession.

The LSAP programs entailed the purchase of long-term securities and were to work through a portfolio balance channel, a signaling channel, and a market calming channel. Long-term interest rates, in turn, would be lowered and spur aggregate demand growth (Gagnon 2016). There is now a fairly large literature that has evaluated the effectiveness of the QE programs and it generally finds they were moderately successful in lowering long-term yields. In the case of the U.S. economy, this literature suggests the LSAP programs lowered the 10-year Treasury yield by just over 100 basis points (Borio and Zabai 2016; Gagnon and Sack 2018; Swanson 2018).8

While many agree LSAPs had some influence on long-term interest rates, there is less agreement as to their impact on broader economic activity (Thornton 2015; Bordo and Levin 2019). Here, the empirical findings are mixed and even advocates of QE like Gagnon (2019) acknowledge the recovery that accompanied these programs was weaker than expected. Some attribute the slow recovery to the severity of the 2008-09 financial crisis, but even nominal economic measures like inflation and nominal GDP over which the central banks should have more control underperformed relative to their precrisis trends (Beckworth and Ponnuru 2018). Arguably, these outcomes could have been worse in the absence of the LSAPs, but the fact these programs were not able to generate robust recoveries suggest there may be limits to their effectiveness.

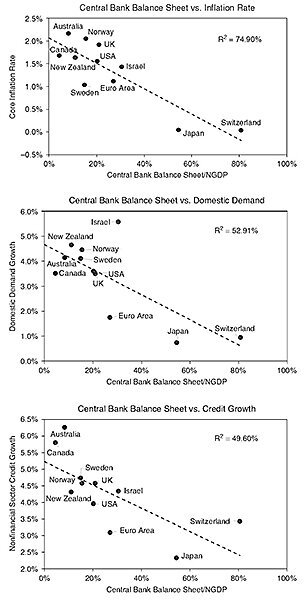

Figure 2 corroborates this view. This figure takes the average size of central bank balance sheets as a percentage of nominal GDP for the 11 advanced economies listed earlier and plots them against three nominal measures for the past decade: core inflation rate, domestic demand growth rate, and credit to the nonfinancial sector growth rate.9 Since the LSAPs expanded the central bank balance sheets and are supposed to create, all else equal, higher nominal growth, one would expect a positive relationship in the scatterplots given the time period spans an entire decade. Figure 2 reveals, however, the opposite pattern holds: the larger the central bank balance sheet, the lower the growth rate of these nominal variables. This outcome runs contrary to the goals of QE and raises questions about the effectiveness of these programs.

FIGURE 2: LARGE CENTRAL BANK BALANCE SHEETS AND NOMINAL GROWTH (2009–2019 AVERAGE)

NOTE: Data sources are listed in the Appendix.

Now, one has to be careful with causality in these scatterplots. It could be the case that the countries with the weakest nominal growth responded with the most aggressive use of the LSAP programs. This is probably true, but the data span an entire decade so one would expect to see inflation, domestic demand, and credit growth respond to the use of LSAPs over this long of a period if QE worked as advertised. Instead, there are strong negative relationships in Figure 2 that present something of a puzzle.

One explanation for this puzzle is that LSAPs were not tried aggressively enough, as argued by Gagnon (2019). If it were the case that QE never had any effect on nominal variables at the ZLB, then central banks could buy up everything on Earth with no nominal consequences. This seems unlikely, as it implies unlimited arbitrage opportunities for central banks. LSAPs, consequently, should at some point generate robust nominal demand growth. Eggertsson and Proulx (2016) show, however, that this point could require LSAPs to be 400 percent or more of nominal GDP. This size far exceeds the largest central bank balance sheets, which currently are the Bank of Japan at 100 percent and the Swiss National Bank at 117 percent, and would likely push central banks up against political and asset supply constraints. Given these practical limitations, QE may be limited in its effectiveness.

Another possible explanation for the puzzle is the way LSAPs have been implemented. In most cases, QE has operated against the backdrop of an inflation target. Eggertsson and Woodford (2003, 2004) show that this QE-inflation targeting combination at the ZLB will be relatively ineffective at stimulating aggregate demand—because it prevents central banks from credibly committing to meaningful forward guidance. This “irrelevance result” holds because inflation targeting does not allow for make-up policy and, as a result, forces central banks to prematurely tighten monetary policy following a deep recession. This premature tightening with inflation targeting is expected by the public and therefore inhibits forward guidance.

If, on the other hand, the LSAPs were tied to a price level or nominal GDP level target, there would be make-up policy and therefore central banks could provide powerful forward guidance. At an operational level, a level target implies keeping the policy interest rate low even after the ZLB ceases to bind or, alternatively, that the expansion of the monetary base created by the LSAP is expected to be permanent and greater than base money demand growth. A level target, in other words, provides a powerful form of forward guidance that is not available with an inflation target (Woodford 2012).

These two explanations for the limited effectiveness of QE can explain why there is no upward slope in the scatterplots of Figure 2. What they do not explain is why there is a downward slope. An explanation that can account for the negative relationship is that some other phenomenon may be influencing both the growth of the nominal variables and the growth of central bank balance sheets. This paper makes the case that the phenomenon is the secular decline of interest rates caused by the above-mentioned global shortage of safe assets that has persisted over the last decade. The safe asset demand shortage causes nominal economic growth to be weak via the “safety trap” and central banks are responding to this weakness by expanding their balance sheets.10

To test this story, a panel vector autoregression (VAR) with fixed effects was estimated using the variables in Figure 2 plus the 10-year government interest rates used in Figure 1.11 Specifically, the vector of endogenous variables that was estimated is as follows:

(1)

zi,t = (ddi,t, ci,t, pi,t, ii,t, bsi,t).

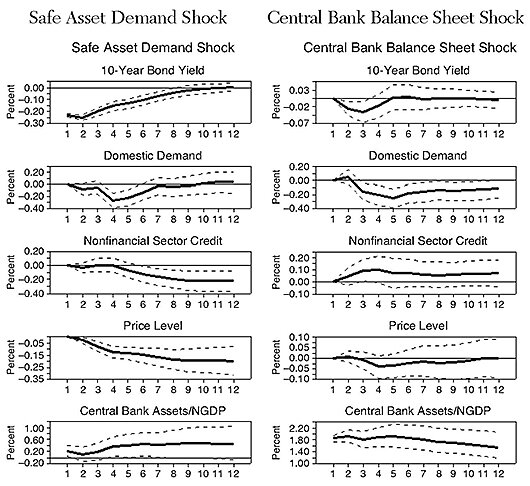

Here, zi,t is the vector of endogenous variables, ddi,t domestic demand, ci,t is credit to the nonfinancial sector, pi,t is the core price level, ii,t is the 10-year government bond yield, and bsi,t is the central bank balance sheet as a percent of nominal GDP. The subscripts i and t represent country i and time period t. The panel VAR is estimated on the data for all 11 economies over the sample period in the figures: 2009:Q1 to 2019:Q2.12 The resulting IRFs for standard deviation shocks to the last two variables in (1) are reported in Figure 3.

FIGURE 3: PANEL VAR IRF FROM STANDARD DEVIATION SHOCKS (2009:Q1–2019:Q2)

>NOTE: The solid lines are impulse responses and the dashed lines are the confidence interval bands.

Given a recursive identification and the understanding that government bond yields are safe asset interest rates, the shocks to the last two variables are interpreted as a safe asset demand shock and a central bank balance sheet shock, respectively. The first column in Figure 3 shows that a positive safe asset demand shock causes bond yields to fall, the nominal variables to decline, and the central bank balance sheet to expand. An excess demand for safe assets, then, seems to be a good explanation for the negative relationships seen in Figure 1.

The second column of Figure 3 shows that a positive central bank balance sheet shock leads to a temporary decline in the bond yield as predicted by advocates of QE. The size of the decline implies that the Fed’s QE programs had a cumulative effect of lowering the 10-year yield by about 70 basis points. Based on a survey of the literature, Gagnon (2016) estimates the LSAPs had a cumulative effect just over 100 basis points. The panel VAR, therefore, is not far from other estimates and implies the model is capturing meaningful relationships.13

Implications of the Two Developments

A key implication of the developments discussed above is that both conventional and unconventional monetary policies are likely to be of little use in future recessions. Even if the next recession were to occur within a year, there would not be sufficient interest rate space for the Fed to adjust its target interest rate or to lower long-term interest rates via LSAPs. This problem becomes more pronounced for a recession happening several years out as the safe asset shortage will continue to depress interest rates across the yield curve.

In such an environment, the Fed could resort to even larger QE programs, but as noted in the discussion above, it may require the central bank to grow its balance sheet to at least 400 percent of the economy before it began to have meaningful traction. Political and asset supply constraints are likely to kick in before the 400 percent threshold is reached. The Fed could also try targeting negative interest rates, both at the short and long end of the yield curve. Negative interest rates, however, eventually run up against the ELB, are politically toxic, and would be a big change for the Fed.

The Fed might also try relying more heavily on forward guidance via the adoption of something like a Reifschneider-Williams (2000) rule. This rule would have the Fed keep its target interest rates at the ELB even after economic conditions warrant a higher target interest rate. In the absence of a credible level target, however, the Fed is unable to commit to such behavior. This reality has been borne out since 2015 with the Fed’s raising of its target interest rate even though the Reifschneider-Williams (2000) rule indicates it should still be at zero percent in 2019.14

All of this discussion points to the Federal Reserve not being prepared for future recessions. To remedy this, the Fed needs to make several upgrades to its operating framework. First, it needs to adjust its operating framework so that it can handle both positive and negative interest rate environments. Second, the Fed needs to tie its operating framework to a level target so that it can provide meaningful forward guidance. Finally, the operating framework needs the enhanced credibility that comes from providing the Fed explicit but constrained access to a standing fiscal facility at the ZLB.

These improvements are a tall order, but the alternative is an ineffectual Fed and haphazard fiscal policy by Congress in future recessions. It is far better to have a nimble central bank that can respond to the next recession in a systematic, rules-based, and accountable manner. The next section of the paper outlines a proposal that accomplishes this goal.

Designing an Operating Framework for the 21st Century

This section of the article proposes a new operating framework for the Federal Reserve that incorporates the suggested changes listed above. Specifically, it outlines an operating framework that can handle any interest rate environment, is tied to a level target, and is empowered with a standing fiscal facility that can be used at the ZLB. The latter enhancement would allow the Fed to do helicopter drops once interest rates hit zero percent. This last feature is probably the most controversial but also is key to making this framework fully credible and builds upon recent calls for better monetary policy–fiscal policy coordination at the ZLB.15

This proposal keeps the Federal Reserve as the main institution doing countercyclical macroeconomic policy. This is a useful feature since the Fed is already viewed as playing this role by the public and therefore would provide continuity. The proposal, however, would reduce the Fed’s discretion by imposing stricter rules on how it runs its operating system. These rules would guard against the Fed abusing the extra power it would get from the standing fiscal facility. The three main parts of the proposal are sketched out next.

Part I: An Operating Framework Robust to Any Interest Rate Environment

To make the Fed’s operating framework robust to both positive and negative interest rate environments, this proposal follows Bordo and Filardo (2007) and Belongia and Ireland (2018) in calling for a two-rule approach to monetary policy. Specifically, the Fed would follow a version of the Taylor rule (1993) when interest rates were above zero percent since it is a reaction function that uses an interest rate target as the instrument. The Fed would follow the McCallum rule (1984, 1987) when interest rates were at zero percent or below since it is a reaction function that uses the monetary base as the instrument. The McCallum rule would govern how the Fed conducted its helicopter drops and, by implication, when it would tap the standing fiscal facility. In the spirit of Orphanides (2018), this two-rule approach to monetary policy would be explicitly added to the Federal Open Market Committee’s “Statement on Longer-Run Goals and Monetary Policy Strategy,” so that the public clearly understood when and under what circumstances the Fed would use each rule.

Part II: An Operating Framework Tied to a Level Target

As noted earlier, a level target provides powerful forward guidance since it forces the central bank to make up for past misses in its target. Here, a nominal GDP (NGDP) level target is used for reasons laid out in Beckworth (2019) and Binder (2020) and takes the form of a forecast target as suggested by Svennson (1997). Put differently, this article proposes a NGDP level target that aims to guide the forecast of NGDP to its intended growth path value.16

To that end, define NGDPt,t+h as the forecasted level of NGDP for period t+h and  as the targeted level of NGDP for period t+h. Given these definitions, the expected NGDP level gap can then be defined as the percentage difference between NGDPt,t+h and . With these definitions in hand, the Taylor and McCallum rules can be stated as follows:

as the targeted level of NGDP for period t+h. Given these definitions, the expected NGDP level gap can then be defined as the percentage difference between NGDPt,t+h and . With these definitions in hand, the Taylor and McCallum rules can be stated as follows:

(2)

Taylor Rule: if it > 0, then

(3)

McCallum Rule: if it ≤ 0, then

Here,  is the neutral interest rate, Δbt is the change in the log level of the monetary base, Δx* is the targeted growth rate of nominal GDP, and Δvt,t+h is the forecasted change in the log level of the monetary base’s velocity.

is the neutral interest rate, Δbt is the change in the log level of the monetary base, Δx* is the targeted growth rate of nominal GDP, and Δvt,t+h is the forecasted change in the log level of the monetary base’s velocity.

Part III: An Operating Framework Tied to a Standing Fiscal Facility

The final part of the operating framework establishes a standing fiscal facility for the Federal Reserve to use when doing helicopter drops. Specifically, the “Stella Fiscal Facility” (SFF) is proposed and named after Stella’s (2020) suggestion to institutionalize the Treasury’s Supplemental Financing Program that was used in 2008 by the Fed to help manage its balance sheet. Stella (2020) proposes the SFF as way for the Fed to shrink its large balance sheet, but it can also be used to help facilitate the Fed’s helicopter drops. Its use would be triggered when the economy hit the ZLB and would be regulated by the McCallum rule outlined above. Also, it is proposed here that its use should be approved by the Treasury secretary every time it is used. This would make the Fed’s use of helicopters drops, a form of fiscal policy, more accountable to the public.

Operationally, the SFF would create Treasury securities that would be deposited at the Fed. This increase in Fed assets could then be matched by an increase in Fed liabilities that are issued to the public via the McCallum rule-governed helicopter drops. Since these special Treasury securities would only be held by the Fed, they would not count toward the debt ceiling limit.17

The SFF is similar to proposals by Bernanke (2016), Gagnon (2019), and Bartsch et al. (2019) who also call for granting the Fed a standing fiscal facility for use in deep recessions. The SFF proposed here, however, is unique since its use would be tied explicitly to the McCallum rule that only kicks in at the ZLB. This rule satisfies the conditions of Auerbach and Obstfeldt (2005), Woodford (2012), and Buiter (2016), who show that, for monetary base injections to matter at the ZLB, the public must expect the injections to be permanent and greater than base money demand growth. The McCallum rule satisfies these conditions since it has a NGDP level target embedded in it.

Advantages of This Operating Framework

This proposal has many advantages over the current operating framework and should be seriously considered by the Fed and Congress. First, as noted above, it is robust to positive and negative interest rate environments. Therefore, no matter what the safe asset shortage does to interest rates, the Fed can still provide meaningful countercyclical monetary policy. Second, this operating framework will reduce the likelihood of recessions because it provides powerful forward guidance through a NGDP level target. Specifically, if households and firms believe the Fed will always correct past misses in its targeted NGDP growth path, then they have less incentive to change their spending in the first place. Third, the SFF gives the NGDP level target the full backing of the government’s consolidated balance sheet. This backing gives the NGDP level target credibility and, ironically, will minimize the need to actually use the SFF since it reduces the likelihood of economic downturns. Finally, the operating framework as outlined above would be implemented in a rules-based approach that includes the sign-off of the Treasury secretary when the SFF is tapped. This makes the Fed more predictable, systematic, and accountable to the public.

To be clear, this proposal is a radical departure from the current operating framework and will require congressional approval. Compared to the status quo, though, this approach is a bargain. For, if no changes are made to the Fed’s operating framework, the Fed is likely to be ineffective in future recessions and thereby force the use of fiscal policy responses. As Greene (2019) notes, however, the politics of fiscal stimulus are problematic and unlikely to be applied in a “timely, targeted, and temporary” manner (Summers 2008). Fiscal policy, in other words, if suddenly forced to provide stimulus because monetary policy is impotent, is likely to be ad hoc, ill timed, and costly.18 The proposal outlined here provides a way to employ fiscal policy in an effective and nimble manner while keeping the Fed as the main countercyclical government agency. This latter feature is important since it serves as a signal of continuity and calm to a public that already views the Fed as playing this role. This proposal, in short, provides a systematic way to do increased monetary policy–fiscal policy coordination when it is most needed.

Conclusion

As this article shows, there is an urgent need to upgrade the Federal Reserve’s operating framework to the realities of the 21st century. Both conventional and unconventional monetary policy will probably be of little use in future recessions given the secular decline of interest rates and the limited effectiveness of LSAPs in their current form. Other monetary policy innovations—like negative interest rates and forward guidance—are also unlikely to be effective under the Fed’s current operating framework.

The Federal Reserve, in short, is not prepared for future recessions. To remedy this, the Fed needs to make several changes to its operating framework. First, it needs to adjust its operating framework so that it can handle both positive and negative interest rate environments. Second, the Fed needs to tie its operating framework to a level target so that it can do meaningful forward guidance. Finally, the operating framework needs the enhanced credibility that comes by granting it limited access to a standing fiscal facility. This article outlines a proposal that accomplishes these goals and does so in a manner that encourages the Fed to act in a more systematic, rules-based, accountable manner.

References

Ainger, J. (2019) “The Unstoppable Surge in Negative Yields Reaches $17 Trillion.” Bloomberg (August 30).

Auerbach, A., and Obstfeld, M. (2005) “The Case for Open-Market Purchases in a Liquidity Trap.” American Economic Review 95 (1): 110–37.

Bartsch, E.; Boivin, J.; Fischer, S.; and Hildebrand, P. (2019) “Dealing with the Next Downturn: From Unconventional Monetary Policy to Unprecedented Policy Coordination,” BlackRock Investment Institute Report.

Beckworth, D. (2017) “Permanent versus Temporary Monetary Base Injections: Implications for Past and Future Fed Policy.” Journal of Macroeconomics 54: 110–26.

___________ (2018) “Nominal GDP as the Stance of Monetary Policy: A Practical Guide.” Mercatus Center Working Paper.

___________ (2019) “Facts, Fears, and Functionality of Nominal GDP Level Targeting: A Practical Guide to a Popular Monetary Policy Framework.” Mercatus Center Special Study.

Beckworth, D., and Crowe, C. (2017) “The International Impact of the Fed When the United States Is a Banker to the World.” In M. D. Bordo and J. B. Taylor (eds.), Rules for International Monetary Stability, 55–112. Stanford, Calif.: Hoover Institution Press.

Beckworth, D., and Ponnuru, R. (2018) “A Monetary Correction.” National Review (February 17).

Belongia, M., and Ireland, P. (2018) “Targeting Constant Money Growth at the Zero Lower Bound.” International Journal of Central Banking 14: 159–204.

Bernanke, B. S. (2016) “What Tools Does the Fed Have Left? Part 3: Helicopter Money.” Brookings Institution (April 11).

Binder, C. (2020) “NGDP Targeting and the Public.” Cato Journal 40 (2): 321–42.

Blyth, M., Lonergan, E. (2014) “Print Less but Transfer More: Why Central Banks Should Give Money Directly to the People.” Foreign Affairs (September/October).

Bordo, M. D., and Filardo, A. (2007) “Money Still Makes the World Go Round: The Zonal View.” Journal of the European Economic Association 5 (2–3): 509–23.

Bordo, M. D., and Levin, A. (2019) “Improving the Monetary Regime: The Case for U.S. Digital Cash.” Cato Journal 39 (2): 383–405.

Borio, C., and Zabai, A. (2016) “Unconventional Monetary Policies: a Re-Appraisal.” BIS Working Papers 570.

Bossone, B. (2016) “The True Costs of Helicopter Money.” VoxEU (September 5).

Buiter, W. H. (2016) “The Simple Analytics of Helicopter Money: Why It Works—Always.” Economics: The Open-Access, Open-Assessment E‑Journal 8 (2014–28): 1—45 (Version 3).

Caballero, R. J. (2018) “Risk-Centric Macroeconomics and Safe Asset Shortages in the Global Economy: An Illustration of Mechanisms and Policies.” Available at http://dx.doi.org/10.2139/ssrn.3253064.

Caballero, R.; Farhi, E.; and Gourinchas, P‑O. (2017) “The Safe Assets Shortage Conundrum.” Journal of Economic Perspectives 31 (3): 29–46.

Christiano, L.; Eichenbaum, M.; and Evans, C. (1996) The Effects of Monetary Policy Shocks: Some Evidence from the Flow of Funds.” Review of Economics and Statistics, 78 (1): 16–34.

Coppola, F. (2019) The Case for People’s Quantitative Easing. Cambridge, U.K.: Polity Books.

Del Negro, M.; Giannone, D.; Giannoni, M.; and Tambalotti, A. (2018) “Global Trends in Interest Rates.” Federal Reserve Bank of New York Staff Report No. 866 (September).

Eggertsson, G., and Woodford, M. (2003) “The Zero Interest-Rate Bound and Optimal Monetary Policy.” Brookings Papers on Economic Activity Spring (1): 139–233.

___________ (2004) “Policy Options in a Liquidity Trap.” American Economic Review 94 (2): 76–79.

Eggertsson, G., and Proulx, K. (2016) “Bernanke’s No-Arbitrage Argument Revisited: Can Open Market Operations in Real Assets Eliminate the Liquidity Trap?” NBER Working Paper No. 22243.

Gagnon, J. (2016) “Quantitative Easing: An Underappreciated Success.” Peterson Institute for International Economics (April).

___________ (2019) “What Have We Learned About Central Bank Balance Sheets and Monetary Policy?” Cato Journal 39 (2): 407–17.

Gagnon, J., and Sack, B. (2018) “QE: A User’s Guide.” Peterson Institute for International Economics (October).

Gorton, G. (2017) “The History and Economics of Safe Assets.” Annual Review 9: 547–86.

Gourinchas, P., and Rey, H. (2007) “From World Banker to World Venture Capitalist: U.S. External Adjustment and the Exorbitant Privilege.” In R. Clarida (ed.), G7 Current Account Imbalances: Sustainability and Adjustment. Chicago: University of Chicago Press.

Greene, M. (2019) “The Politics of Fiscal Stimulus Are Problematic.” Financial Times (November 4).

Greenlaw, D.; Hamilton, J.; Harris, J.; and West, K. (2018) “A Skeptical View of the Impact of the Fed’s Balance Sheet.” NBER Working Paper No. 24687.

Guiso, L. (2012) “Trust and Risk Aversion in the Aftermath of the Great Recession.” European Business Organization Law Review 13 (2): 195–209.

Ha, J.; Kose, M.A.; Ohnsorge, F.; and Unsal, F. (2019) “Sources of Inflation: Global and Domestic Drivers.” In J. Ha, M. A. Ayhan, and F. Ohnsorge (eds.), Inflation in Emerging and Developing Economies: Evolution, Drivers, and Policies,143–204. Washington: World Bank.

Hamilton, J. (2018) “The Efficacy of Large-Scale Asset Purchases When the Short-Term Interest Rate Is at Its Effective Lower Bound.” Brookings Papers on Economic Activity 2: 1–24.

Ireland, P. (2007) “Changes in the Fed’s Inflation Target: Causes and Consequences.” Journal of Money, Credit, and Banking 39: 1851–81.

Jordà, O., and Taylor, A. (2019). “Riders on the Storm.” Federal Reserve Bank of San Francisco Working Paper No. 2019–20. Available at https://doi.org/10.24148/wp2019-20.

Kiley, M. (2019) “The Global Equilibrium Real Interest Rate: Concepts, Estimates, and Challenges.” Federal Reserve Board of Governors, Finance and Economics Discussion Series 2019-076. Available at https://doi.org/10.17016/FEDS.2019.076.

Krishnamurthy, A., and Vissing-Jorgensen, A. (2012) “The Aggregate Demand for Treasury Debt.” Journal of Political Economy, 120 (2): 233–67.

McCallum, B. (1984). “Monetarist Rules in the Light of Recent Experience.” American Economic Review 74: 388–91.

___________ (1987) “The Case for Rules in the Conduct of Monetary Policy: A Concrete Example.” Federal Reserve Bank of Richmond Economic Review (September/October): 10–18.

McCulley, P., and Pozsar, Z. (2013) “Helicopter Money: Or How I Stopped Worrying and Learned to Love Fiscal-Monetary Cooperation.” GIC Global Society of Fellows Policy Paper.

Orphanides, A. (2018) “Improving Monetary Policy by Adopting a Simple Rule.” Cato Journal 38 (1): 139–46.

Reifschneider, D., and Williams, J. C. (2000) “Three Lessons for Monetary Policy in a Low-Inflation Era.” Journal of Money, Credit, and Banking 32: 936–66.

Shapiro, A., and Wilson, D. (2019) “Taking the Fed at Its Word: A New Approach to Estimating Central Bank Objectives Using Text Analysis.” Federal Reserve Bank of San Francisco Working Paper No. 2019-02.

Stella, P. (2020) “A Short Law to Enhance the Efficiency and Stability of the U.S. Financial System.” Available at www.researchgate.net/publication/339723456.

Summers, L. (2008) “Why America Must Have a Fiscal Stimulus.” Financial Times (January 6).

Svensson, L. (1997) “Inflation Forecast Targeting: Implementing and Monitoring Inflation Targets.” European Economic Review 41: 1111–46.

Swanson, E. (2018) “The Federal Reserve Is Not Very Constrained by the Lower Bound on Nominal Interest Rates.” NBER Working Paper Series No. 25123.

Taylor, J. (1993) “Discretion versus Policy Rules in Practice.” Carnegie-Rochester Conference Series on Public Policy 39: 195–214.

Thornton, D. (2015) “Requiem for QE.” Cato Institute Policy Analysis No. 783. Washington: Cato Institute, Center for Monetary and Financial Alternatives.

Tukker, M. (2019) “Hooked on Safe Assets.” Oxford Economics Research Paper (October 31).

Turner, A. (2015) “The Case for Monetary Finance: An Essentially Political Issue.” Speech presented at the 16th Jacques Polack Annual Research Conference, Washington, D.C. (November 5).

Woodford, M. (2012) “Methods of Policy Accommodation at the Interest-Rate Lower Bound.” Kansas City Federal Reserve Bank Economic Symposium. Available at www.kansascityfed.org/publicat/sympos/2012/mw.pdf.

Appendix: Data Sources

About the Author

This work is licensed under a Creative Commons Attribution-NonCommercial-ShareAlike 4.0 International License.