Over the past few years I have been making the case for moving toward a more rules-based international monetary system (e.g., Taylor 2013, 2014, 2015, 2016a, 2016b, 2017). In fact, I made the case over 30 years ago in Taylor (1985), and the ideas go back over 30 years before that to Milton Friedman (1953). However, the case for such a system is now much stronger because the monetary system drifted away from a rules-based approach in the past dozen years and, as Paul Volcker (2014) reminds us, the absence of a rules-based monetary system “has not been a great success.”

To bring recent experience to bear on the case, we must recognize that central banks have been using two separate monetary policy instruments in recent years: the policy interest rate and the size of the balance sheet, in which reserve balances play a key role. Any international monetary modeling framework used to assess or to make recommendations about international monetary policy must include both instruments in each country, the policy for changing the instruments, and the effect of these changes on exchange rates.

Using such a framework, I show that both policy instruments have deviated from rules-based policy in recent years. I then draw the policy implications for the international monetary system and suggest a way forward to implement the policy.

Regarding policy interest rates, there has clearly been an international contagion of deviations from monetary policy rules that have worked well in the past, as I argued in Taylor (2009, 2013).1 This international contagion is due in part to a concern about exchange rates. If a foreign central bank with global financial influence cuts its interest rate by a large amount, then the currencies of other countries will tend to appreciate unless the other central banks react and adjust their interest rates. Central bank reactions may also include exchange market interventions, capital flow restrictions, or some form of macroprudential actions aimed at international capital flows. These actions and reactions accentuate the deviation of monetary policy from traditional policy rules. To be sure, the international contagion of policy interest rates may be due to omitted factors that push interest rates around for many central banks. However, there is considerable econometric evidence that the deviations from policy rules are caused by unusual interest rate changes in other countries. There is also direct evidence from many central bankers who admit to these reactions. Norges Bank reports on monetary policy, for example, show that its policy interest rate is adjusted in relation to interest rate decisions at the European Central Bank (ECB), as described in Taylor (2013).

Regarding central bank balance sheet operations, there has also been international contagion, and this is also likely due to exchange rate concerns. Here an important distinction must be made between the central banks in large open economies and central banks in small open economies. In large open economies, the effects of balance sheet operations on exchange rates have been harder to detect than for central banks in small open economies. However, as I show in this article, there is now empirical evidence provided in Taylor (2017) of statistically significant impacts on exchange rates of the balance sheet operations by the Federal Reserve, the Bank of Japan (BOJ), and the ECB. There are also exchange rate effects in the small open economies where explicit foreign exchange purchases are often financed by an expansion of reserve balances.

A Framework and an International Policy Matrix

To investigate the international aspects of central bank interest rate and balance sheet policies, it is necessary to introduce a simple framework that captures key features of the recent economic policy environment. In the framework I use here, central banks have two separate policy instruments: the short-term interest rate and reserve balances. By paying interest (either positive or negative) on reserve balances, central banks can separately set the interest rate and reserve balances. This enables the central bank to intervene in other markets for a variety of reasons. In fact, in recent years, central banks in large open economies have purchased domestic securities denominated in their own currency through their quantitative easing (QE) programs. The stated aim has often been to raise the price and reduce the yield of these domestic securities, though there are sometimes references to exchange rates. In contrast, the central banks in smaller countries have purchased foreign securities denominated in foreign currency. The explicit aim of these foreign exchange purchases is to affect the exchange rate.

To operationalize this framework in Taylor (2017), I examined the balance sheets of three central banks in large open economies—the Fed, ECB, and BOJ—and a central bank in a relatively small open economy—the Swiss National Bank (SNB). Most of the purchases of assets by these banks are financed by increases in reserve balances. For the Fed, purchases of dollar-denominated bonds are financed by dollar reserve balances. For the Bank of Japan, purchases of yen-denominated securities are financed by yen-denominated reserve balances. For the ECB, purchases of euro-denominated securities are financed by euro-denominated reserve balances. For the SNB, purchases of euro- and dollar-denominated securities are financed by Swiss franc–denominated reserve balances. In addition, each of these central banks sets its short-term policy interest rate, which in the case of the Fed is the federal funds rate. The private sector holds securities and deposits funds (reserve balances) at the central bank. Prices and yields are determined by market forces. The exchange rates between the dollar, the yen, the euro, and the Swiss franc are determined in the markets just as is the price of other securities.

The framework thus includes eight different policy instruments for the four central banks: the balance sheet items (R for reserve balances) RU, RJ, RE, and RS, and the short-term policy rates (I for interest rate) IU, IJ, IE, and IS, where the subscripts indicate the United States (U), Japan (J), Europe (E), and Switzerland (S). The actual data used in this article to compute international correlations and create time series charts were obtained directly from the central banks’ databases.2

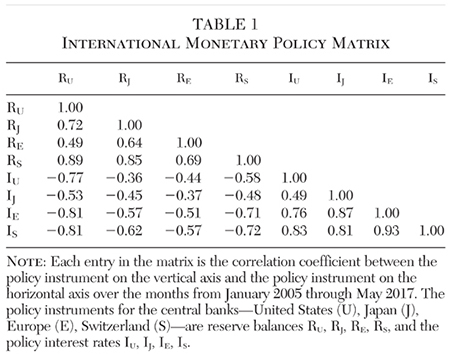

Table 1 is an international policy matrix that gives the cross correlations of the eight policy instruments in the four countries using monthly data for the dozen years from 2005 to 2017. Observe the strong positive correlation between the reserve balances in each country. This could indicate either a contagion of such policies or that they have been reacting to a common shock. Observe also the strong positive correlation between the interest rate instrument in each country, which is consistent with the recent literature on interest rate contagion. The most highly correlated of all the entries in the policy matrix in Table 1 is between the SNB policy rate and the ECB policy rate with a correlation coefficient of 0.93.

The international policy matrix also reveals a strong negative correlation between the two policy instruments within each central bank: when the interest rate is lower during this period, reserve balances are higher. This is likely due to the assumption at central banks that the impact of the two instruments is similar: a lower policy rate and an expanded balance sheet with higher reserve balances are assumed to increase aggregate demand, raise the inflation rate, and depreciate the currency.

Note also the negative correlation between reserve balances and the interest rates across countries. These are simple correlation coefficients, so the negative effect could be due to a negative correlation within each country coupled with a positive contagion effect of either the interest rate or reserve balances in each country.

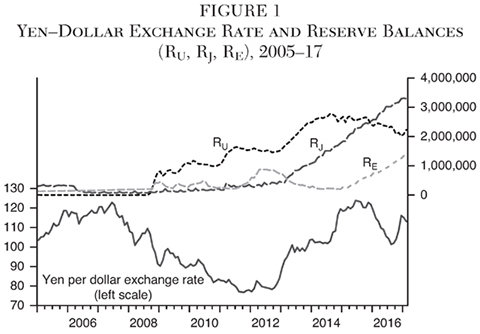

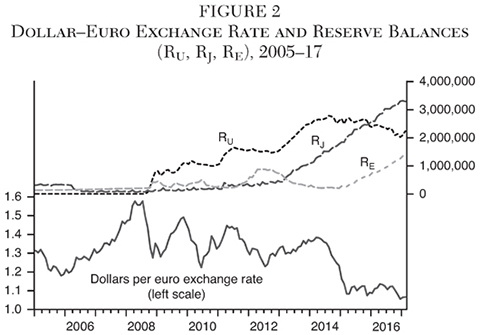

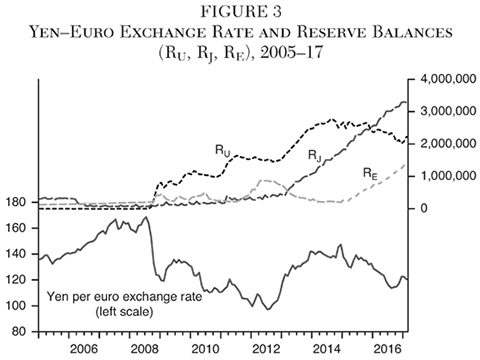

The underlying reasons for the numerical correlations between reserve balances in the different countries can be better understood by studying the actual paths of reserve balances for the Fed, the BOJ, the ECB, and the SNB. During this period, the Fed was out in front with large-scale asset purchases of U.S. Treasuries and mortgage-backed securities in 2009 following the short-lived liquidity operations during the panic in 2008. These large-scale purchases, commonly called QE I, II, and III, were financed with the large increases in reserve balances. For the past few years, reserve balances have started to decline in the United States as securities purchases were reduced in size and then were ended. Currency demand has grown, also reducing the need for financing the stock of securities with reserve balances.

This expansion of reserve balances in the United States was followed by a similar move by the BOJ at the start of 2013. Soon thereafter the ECB started increasing reserve balances. Throughout the period the SNB was expanding reserves as it purchased euros and dollars to counter the appreciation of the Swiss franc against these currencies. In other words, the positive correlations between reserve balances in the matrix are due to Japan’s following the increase in reserve balances in the United States, the ECB’s following Japan and the United States, and the SNB’s responding to all three. In the end, the increase in global liquidity was much larger than if there had not been this contagion.3

The correlations between the interest rates in the matrix are similarly due to central banks’ following each other as they make their policy decisions about their policy interest rate. This contagion has been documented with interest rate reaction functions in empirical work by Taylor (2009), Carstens (2015), and Gray (2013). With such functions, one can measure the reaction of central banks to other countries’ interest rates by including the foreign central bank’s interest rate in the reaction function. This is more difficult in the case where the balance sheet is the instrument.

Exchange Rate Effects

While the policy matrix shows a close association between the policies, there is a question about whether central banks were jointly trying to provide liquidity or whether the actions were part of a competitive devaluation process. As mentioned above and reported in Taylor (2017), I found statistically significant exchange rate effects in estimated regressions of exchange rates on reserve balances. To summarize, the regression equations showed that (1) an increase in reserve balances RJ by the Bank of Japan causes the yen to depreciate against the dollar and the euro, (2) an increase in reserve balances RU by the Fed causes the dollar to depreciate against the yen and the euro, and (3) an increase in reserve balances RE by the ECB causes the euro to depreciate against the yen and the dollar.

These results confirm the policy narrative presented in Taylor (2016b): Following the global financial crisis and the start of the U.S. recovery, the yen significantly appreciated against the dollar as the Fed extended its large-scale asset purchase program financed with increases in reserve balances. At first there was little or no response from the BOJ, but the yen appreciation became a key issue in the 2012 Japanese election. When Shinzo Abe was elected, he appointed Haruhiko Kuroda under whom the BOJ implemented its own QE. A depreciation of the yen accompanied the change in monetary policy. The subsequent moves by the ECB toward QE were also due to concerns about an appreciating euro. At the Jackson Hole conference in August 2014, Mario Draghi spoke about these concerns and suggested QE, which soon followed. This shift in policy was followed by a weaker euro.

The timing of reserve balances and exchange rate movements is illustrated in Figures 1, 2, and 3. The top part of each figure shows the time series patterns of reserve balances for the three large central banks with scale on the right-hand vertical axis measured in units of the local currency—millions of dollars, hundreds of million yen, and millions of euros. The lowest line in the three figures shows the exchange rate between the dollar, the yen, and the euro using the scale on the left-hand vertical axis.

Figure 1 shows the dollar getting weaker against the yen following the increase in reserve balances in the United States, until the BOJ increased its own reserve balances and the dollar then strengthened against the yen. Figure 2 shows the yen getting weaker against the euro as reserve balances are increased in Japan and a reversal when reserve balances are increased by the ECB. Figure 3 shows the weakening of the euro against the dollar and the yen after the action by the ECB.

Note that the positive correlations between reserve balances over the whole period in the three central banks, which was reported in Table 1, is evident in these time series charts. The timing of reserve balance changes is also evident with the Fed going first, followed by the BOJ and the ECB.

Exchange rate effects of reserve balance changes can also occur for small open economies, but they are normally due to direct intervention on the currency markets. In the case of Switzerland, for example, reserve balances are used to finance direct interventions in foreign exchange markets. Vector autoregressions can then be used to examine the impacts. In fact, according to empirical results reported in Taylor (2017), there is significant two-way causality between the Swiss exchange rate and reserve balances. More specifically, the hypothesis that RS does not Granger-cause the Swiss franc–euro exchange rate is rejected with an F-statistic of 4.74; the hypothesis that the Swiss franc–euro rate does not Granger-cause RS is rejected with an F-statistic of 4.04. In other words, changes in the exchange rate Granger-cause an expansion of reserve balances, and the expansion of reserve balances Granger-causes a change in the exchange rate. In addition, I have found that a similar pattern of causality exists when the policy instrument is the interest rate rather than the balance sheet.

Policy Implications

For both policy instruments, the empirical results show that exchange rate considerations have helped cause deviations from rules-based policy in the international monetary system. To the extent that the deviations take policy away from the better performance observed in the 1980s and 1990s, they are a source of instability to the global economy. Moreover, there appears to be a “competitive devaluation” aspect to these actions as argued by Meltzer (2016). To the extent that the policies result in excess movements in exchange rates, they are another source of instability in the global economy as they affect the flow of goods and capital and interfere with their efficient allocation. They also are a source of political instability as they raise concerns about currency manipulation. Moreover, as countries have used balance sheet operations to affect currency values, actual balance sheets have grown throughout the world, and this has raised concerns about the global impact of unwinding them.

A counterfactual exercise using the estimated regressions mentioned above shows that exchange rates would have been significantly less volatile without the balance sheet operations. For the yen/dollar equation, the standard error of the regression is 7.27 and the standard deviation of the dependent variable is 14.11, indicating that the movements in reserve balances have nearly doubled the volatility of the exchange rate. Using the yen/euro equation and euro/dollar equations in the same way shows that movements in reserve balances have increased the volatility of the yen–dollar exchange rate by 60 percent and the euro–dollar exchange rate by 40 percent.

There is other evidence that exchange rate volatility and capital flow volatility have increased in recent years. According to Rey (2013), Carstens (2015), Coeuré (2017), Taylor (2016b), and Ghosh, Ostry, and Qureshi (2017), exchange rate volatility and capital flow volatility have increased recently. Rey (2013) found that a global financial cycle, which was driven in part by monetary policy, affected credit flows in the international financial system. Carstens (2015) documented a marked increase in the volatility of capital flows to emerging markets in recent years. To be sure, there are other explanations for this increased volatility. Ghosh, Ostry, and Qureshi (2017) argue that the volatility has increased because of international externalities and market imperfections. Nevertheless, the evidence provided here and in other recent studies suggests that a deviation from rules-based monetary policy has been part of the problem.

The main policy implication is that the international economy would be more stable if policymakers could create a more rules-based international monetary system. The approach that I favor would be for each central bank to describe and commit to a monetary policy rule or strategy for setting the policy instruments. These rules-based commitments would reduce exchange rate volatility and uncertainty, and remove some of the reasons why central banks have followed each other in recent years. The strategy could include a specific inflation target, an estimate of the equilibrium interest rate, and a list of key variables to react to in certain specified ways. The process would not impinge on other countries’ monetary strategies. It would be a flexible exchange rate system between countries and between currency zones.

Each central bank would formulate and describe its strategy, so there would be no reduction in either national or international independence of central banks. The strategies could be changed or deviated from if the world changed or if there was an emergency, so a commonly understood procedure for describing the change and the reasons for it would be useful. It is possible that some central banks will include foreign interest rates in the list of variables they react to so long as it is transparently described. But when they see other central banks not doing so, they will likely do less of it, recognizing the amplification effects.

The process would be global, rather than for a small group of countries, though, as with the process that led to the Bretton Woods system in the 1940s, it could begin informally with a small group and then spread out. The international rules-based approach I suggest here is supported by research over many years, for example, in Taylor (1985). It is attractive because each country can choose its own independent strategy and simultaneously contribute to global stability.

The major central banks now have explicit inflation goals, and many use policy rules that can describe strategies for the policy instruments. Explicit statements about policy goals and strategies to achieve these goals are thus feasible. There is wide agreement that some form of international reform is needed. In any case, a clear commitment by the Federal Reserve to move in this rules-based direction would help. A prerequisite would be for the international monetary system to normalize. Getting back to balance sheets with reserve levels such that policy interest rates are determined by the supply and demand for reserves—rather than by paying interest on excess reserves—will facilitate a rules-based international system because the balance sheet decisions and interest rate decisions would be linked.

The biggest hurdle to achieving such a rules-based system is a disparity of views about the problem and the solution. Some are not convinced of the importance of rules-based monetary policy. Others may doubt that it would deal with the problems of volatile exchange rates and capital flows. Still others believe that the competitive depreciations of recent years are simply part of a necessary process of world monetary policy easing.

Such a disparity of views has existed for generations of economists and central bankers. Indeed, the current discussion of reforms in the international monetary system reminds one of the debate about exchange rates and capital flows that occurred in the 1940s and 1950s, which Eichengreen (2004) has written about. Nurkse (1944) argued that destabilizing speculation inherent in the market system was the cause of exchange rate and capital flow volatility; his solution was government controls on capital flows and fixed exchange rates. Friedman (1953) argued that monetary policy actions were the cause of the volatility; his solution was an open international monetary system with transparent monetary policy rules and flexible exchange rates. The experience over the years since that time—the improvements in economic models, the enormous volume of research on policy rules, and, especially, the poorer performance in the past dozen years as policy has deviated from a rules-based system—suggests that the answer is a more open, transparent, and rules-based international monetary system in the future.

References

Carstens, A. (2015) “Challenges for Emerging Economies in the Face of Unconventional Monetary Policies in Advanced Economies.” Stavros Niarchos Foundation Lecture, Peterson Institute for International Economics, Washington (April 20).

Coeuré, B. (2017) “Monetary Policy, Exchange Rates, and Capital Flows.” Speech given at the 18th Jacques Polak Annual Research Conference hosted by the IMF, Washington, D.C. (November 3). Available at ecb.europa.eu.

Eichengreen, B. (2004) Capital Flows and Crises. Cambridge, Mass.: MIT Press.

Friedman, M. (1953) “The Case for Flexible Exchange Rates.” In Essays in Positive Economics, 157–203. Chicago: University of Chicago Press.

Ghosh, A.; Ostry, J.; and Qureshi, M. (2017) Taming the Tide of Capital Flows: A Policy Guide. Cambridge, Mass.: MIT Press.

Gray, C. (2013) “Responding to a Monetary Superpower: Investigating the Behavioral Spillovers of U.S. Monetary Policy.” Atlantic Economic Journal 21 (2): 173–84.

Hofmann, B., and Bogdanova, B. (2012) “Taylor Rules and Monetary Policy: A Global ‘Great Deviation’?” BIS Quarterly Review (September): 37–49.

Meltzer, A. H. (2016) “Remarks” in “General Discussion: Funding Quantitative Easing to Target Inflation.” In Designing Resilient Monetary Policy Frameworks for the Future, 493. Kansas City, Mo.: Federal Reserve Bank of Kansas City.

Nurkse, R. (1944) International Currency Experience: Lessons of the Inter-war Period. Geneva: Economic, Financial, and Transit Department, League of Nations.

Rey, H. (2013) “Dilemma Not Trilemma: The Global Financial Cycle and Monetary Policy Independence.” In Global Dimensions of Unconventional Monetary Policy. Jackson Hole Conference, Federal Reserve Bank of Kansas City.

Taylor, J. B. (1985) “International Coordination in the Design of Macroeconomic Policy Rules.” European Economic Review 28: 53–81.

__________ (2009) “Globalization and Monetary Policy: Missions Impossible.” Originally presented at an NBER conference in Gerona, Spain. In M. Gertler and J. Gali (eds.) The International Dimensions of Monetary Policy, 609–24. Chicago: University of Chicago Press.

__________ (2013) “International Monetary Coordination and the Great Deviation.” Journal of Policy Modeling 35 (3): 463–72.

__________ (2014) “Nice-Squared.” Presentation at “Bretton Woods: The Founders and the Future,” conference sponsored by the Center for Financial Stability. Available at www.youtube.com/watch?v=XGMmJ2IAHJs.

__________ (2015) “Recreating the 1940s–Founded Institutions for Today’s Global Economy.” Remarks upon receiving the Truman Medal for Economic Policy, Kansas City (October 14).

__________ (2016a) “Rethinking the International Monetary System.” Cato Journal 36 (2): 239–50.

__________ (2016b) “A Rules-Based Cooperatively Managed International Monetary System for the Future.” In C. F. Bergsten and R. Green (eds.) International Monetary Cooperation: Lessons from the Plaza Accord after Thirty Years, 217–36. Washington: Peterson Institute.

__________ (2017) “Ideas and Institutions in Monetary Policy Making: The Karl Brunner Lecture.” Swiss National Bank, Zurich (September 21).

Volcker, P. A. (2014) “Remarks.” Bretton Woods Committee Annual Meeting (June 17).

1See also Carstens (2015), Gray (2013), Hofmann and Bogdanova (2012).

2The specific data series are

RU = total reserve balances maintained with Federal Reserve Banks (millions of dollars)

RJ = BOJ current account balances (100 millions of yen)

RE = current accounts + deposit facility (millions of euros)

RS = sight deposits of domestic banks + sight deposits of foreign banks and institutions + other sight liabilities (millions of Swiss francs)

IU = effective federal funds rate

IJ = call rate, uncollateralized, overnight average

IE = interest rate on deposit facility

IS = Swiss Average Rate Overnight (SARON)

3The paths of reserve balances described in this and the previous paragraph can be seen in the time series graphs in Figures 1, 2, and 3, where I examine the effects on the exchange rate.