[T]his state of affairs … would mean the euthanasia of the rentier, and, consequently, the euthanasia of the cumulative oppressive power of the capitalist to exploit the scarcity-value of capital.… I see, therefore, the rentier aspect of capitalism as a transitional phase which will disappear when it has done its work.

John Maynard Keynes ([1936] 1977: 375–76)

The development of Britain’s economy in the years following the end of the Napoleonic Wars was heavily influenced by the peculiar nature of British government wartime finance. Instead of issuing bonds with higher coupons as interest rates rose, which governments normally did in wartime, British governments from the 1750s onward relied mostly on 3 percent “Consols”, i.e., perpetual bonds with a 3 percent coupon issued at deep discounts. In a world in which equity markets were almost nonexistent and in which there was a gigantic government bond market swollen by war financing, fluctuations in the prices of Consols caused swings in investor wealth that had major economic effects, which have been much underappreciated. After a positive wealth effect in the postwar 1780s and a negative one in the late 1790s, the large, long-lasting bond price increase after 1813 played a major role in capitalizing the Industrial Revolution’s final take-off and the acceleration of economic growth to near-modern levels. As Jeffrey Williamson (1984: 688) noted when discussing the slow start to the Industrial Revolution, “Somewhere around the 1820s Britain passed through a secular turning point.” In this article, we argue that the key to that turning point was the massive wealth effect of the postwar increase in Consols’ prices.

The Napoleonic Wars’ Financing Mechanism

Normally, when a government wants to borrow to finance a war, it knows that its borrowing will cause interest rates to rise, especially if there is inflation. For example, if peacetime interest rates are about 3 percent, the government might issue a 5 percent bond of 20-year maturity rather than say the usual 3 percent peacetime bond. When the bond matures 20 years later and peace reigns again, the government can refinance the bond at 3 percent. Investors holding the 5 percent bond receive a higher interest rate, but no capital gain if they hold the bond to maturity and only a modest gain if they sell mid-term at a premium while bond prices are higher than normal.

That approach broadly describes how the U.S. wars in Korea and Vietnam were financed, as well as both U.S. and British contributions to the two world wars. Earlier, the U.K. government had used a similar approach to finance the War of the Spanish Succession (1702–13), mostly at interest rates of 8–10 percent and with heavy use of tontines and lotteries.

The U.K. government adopted a different approach with its next major wars. In 1751, Sampson Gideon, a brilliant Jewish-British financier, persuaded Prime Minister Henry Pelham to convert most of the outstanding British government debt into 3 percent Consolidated Annuities (the famous Consols). Until their ill-advised redemption in 2015, these were perpetual — that is, they had an infinite maturity — and paid 3 percent interest each year.1 When the government wanted to finance a war, instead of issuing 5 percent bonds at par, it issued 3 percent Consols at perhaps 60 percent of the “par” principal amount, which would then yield 5 percent (i.e., 3 percent/60 percent) on a running yield basis.

Gideon’s thinking was as follows: since all wars were temporary, people who bought 3 percent bonds at 60 percent would make generous 5 percent yields during the war and would then make a large capital gain afterwards, when yields dropped to 3 percent and the bonds went back to par. The Consols were therefore an attractive investment. The government could then find buyers even in war years, provided (as was the case) that there was confidence that Britain would later repay its debts in full.

Not only did investors enjoy strong yields, but they also made big capital gains when peace came: 21 percentage points in six years after the bottom in 1762 as the Seven Years Wars (1756–63) drew to an end, and 33 percentage points in 10 years after the wartime bottom in 1782, as the American War of Independence (1775–82) drew to an end.2

There was then strong demand for new issues of Consols throughout the major wars over the course of the following 50-plus years — the Seven Years War, the American Wars, and the French Revolutionary and Napoleonic Wars (1793–1815, with short remissions).

The Consols enabled Britain to finance heavy military expenditures when its rival France, which had no such mechanism, was unable to do so without financially crippling itself. Gideon’s clever structure, which gave windfall profits at the end of each war to inventory-holding bond dealers like himself, was central to Britain’s acquiring its empire and to not losing it again after the American colonies broke away.

The disadvantage of Gideon’s structure from the fiscal point of view was that, for each £100 of war expenditure on 3 percent Consols issued at 60 percent of par, £167 was typically added to the debt. But since the debt was perpetual and never needed to be redeemed, this feature of Consols finance was not regarded as a major fiscal disadvantage. Lord North, chancellor of the exchequer from 1767 to 1782 and prime minister through the American War of Independence, liked the structure because “it was the interest that the people were burdened with the paying of and not the capital.”3

The interest cost was indeed the same, or even slightly lower than through issuing new 5–6 percent debt at par, because the Consols’ attractiveness to speculators allowed them to be sold at a slightly lower running yield. However, over the course of the century after peace returned in 1815, Britain’s outstanding debt would decline only to £650 million in 1914, although the growth in the British economy meant that debt represented only 30 percent of GDP compared to a peak of around 260 percent of GDP in 1819.

The rise in the prices of British Consols from 1813 onward appears to have been due, in part, to a reduction in their perceived risk as the Allies approached France and peace returned, and, in part, to a drastic reduction in the annual supply of new Consols through budget deficit financing.4

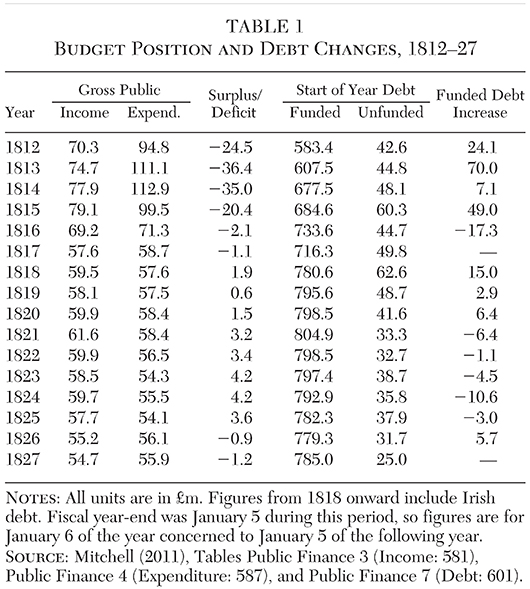

Table 1 shows gross public income and expenditure for the years 1812–27, with the surplus or deficit; it also shows the funded and unfunded debt outstanding at the start of each year, and the increase in debt during the year.5

The deficit figures and debt increase figures in Table 1 do not tally because of the timing of government payments and debt financings. For example, the 1814 military campaign was largely financed by a £22 million debt issue (increasing the amount of 3 percent debt outstanding by £38.9 million) on the morning of the supplementary Budget of November 15, 1813. Nevertheless, the overall trend is clear: huge deficits and increases in the supply of Consols during the war years of 1812–15 were followed by near-balanced budgets in 1816–19 and surpluses thereafter, while the supply of Consols stopped increasing from 1816 onward, except for a modest blip in 1819–20 caused by funding £10 million of the Bank of England’s holdings of Exchequer Bills in connection with the return to gold.6

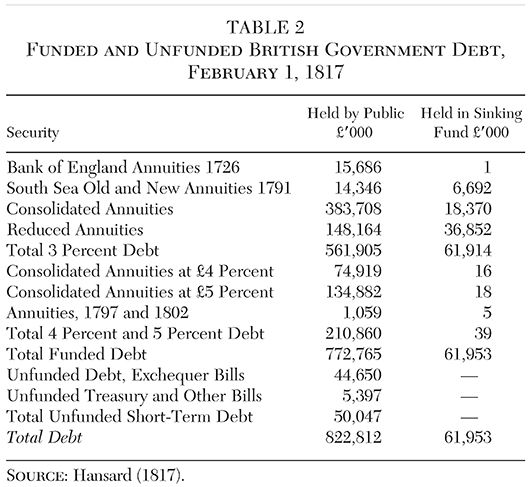

Table 2 sets out the £823 million of British and Irish government funded and unfunded debt that was held by the public on February 1, 1817, a date chosen so the special “emergency” financings for the Waterloo campaign were out of the way.

By far the greatest part of the outstanding debt, £562 million or 68 percent of the total, consisted of perpetual securities bearing a 3 percent interest rate, payable twice yearly. The largest single tranche, £384 million, consisted of “Consolidated Annuities,” the 3 percent Consols, which paid interest in January and July. There was also an exactly equivalent obligation, the Reduced Annuities, with principal amount of £148 million, which differed from Consols only in paying interest in April and October. Dealers would arbitrage between these two securities, with the Reduced Annuities generally trading at a small discount (subject to fluctuations before and after their interest payment dates) because of their somewhat lesser liquidity. There were also two relatively small older issues with 3 percent coupons, reflecting refinancings of debt incurred early in the 18th century, for the Bank of England and the South Sea Company, of £16 million and £14 million, respectively.

In addition to the perpetual 3 percent debt, there was £211 million of 4 percent and 5 percent debt, which would be refinanced after the war as interest rates declined. The 4 percent debt, totaling £75 million, took the form of 4 percent Consols, while the 5 percent debt, totaling £136 million, originally contracted in many cases by the Navy and Army directly, had been consolidated into 5 percent Consols. By the 1820s, the 5 percent debt was trading above par. There were then two refinancing operations carried out at the end of 1823 and in early 1824, one converting £135 million of 5 percent Consols into 4 percent Consols and the second converting £80 million of 4 percent Consols into a new issue of 3.5 percent Consols.7

Finally, in 1817 there was £50 million of short-term debt, mostly in the form of Exchequer Bills, which were short-term instruments, generally converted into long-term debt as new issues were undertaken. The £50 million outstanding in February 1817 was high by historical standards, a residue of the emergency financings undertaken at the Napoleonic Wars’ climax in 1813–15, and was over the next few years reduced by being converted into long-term debt. Reducing the amount of Exchequer Bills outstanding, thereby mopping up excess market liquidity, was an important pre-condition for the subsequent return to the gold standard.

In addition to the £822 million of debt held by the public, the government had since 1786 built up a sinking fund, intended to accrue at compound interest and allow the debt to be redeemed within 45 years. This fund had been established by William Pitt the Younger because redeeming debt at par, under Gideon’s structure, was expensive and the sinking fund allowed other debt to be redeemed through market purchases. Payments had been made into the sinking fund throughout the war years, even though the government was running deficits, on the principle that the gradual accrual of the sinking fund, with each new issue of debt having an amortization provision to be paid into the sinking fund, would reassure the nation’s creditors. By February 1817 the sinking fund totaled £62 million. It would be modified in 1819 and eliminated in stages in the early 1820s, with the government debt it purchased being canceled in the process.

As an example of how war finance was structured, we can examine the last major financing undertaken during the Napoleonic Wars, which was also the largest single tranche undertaken, and which was announced by Chancellor of the Exchequer Nicholas Vansittart to the House of Commons on June 14, 1815, four days before the Battle of Waterloo, and had been completed that morning. The loan raised £27 million in net proceeds, for each £100 of which buyers would be given £130 in 3 percent reduced stock, £10 in 4 percent Consols, and £44 in 3 percent Consols. The £27 million of net proceeds was obtained by issuing a total of £49.68 million principal amount of new debt, at a running interest cost of 5.62 percent and an average issue price of 54.35 percent of par. In addition to the interest payable, a sinking fund provision of 2.81 percent was made on the £27 million raised, for a total annual debt service charge of 8.43 percent.8

Vansittart told the House of Commons that this record-sized issue, the pricing of which was determined by negotiated tender and not by competitive bid, was only just fully subscribed; a great proportion of the issue was initially left with the underwriters. Four days later the Battle of Waterloo took place, news of which was received on the late evening of June 21.

Contrary to widespread belief, there was no great immediate “bounce” in the market by which (in separate legends) Nathan Rothschild and the broker/economist David Ricardo were both supposed to have made £1 million each through trading on early (and, effectively, inside) information of the battle. However, given the price rise in Consols over the next decade, their holdings of this issue alone played a major role in generating the Rothschild and Ricardo fortunes.

As anticipated by Gideon 60 years earlier, City of London financiers did well from the postwar surges in bond prices. It is no coincidence that Rothschilds, led by Nathan Meyer Rothschild, and Barings, led by the second-generation Alexander Baring, became very powerful after 1815. Their capital base dramatically increased, from 1810 or so as their large long positions in Consols rose in value. Ricardo also became very rich by the same dynamic.

Postwar Surge in Consol Prices Causes Rentier Apotheosis

The deep discount debt issuance structure had major implications for the post–Napoleonic War economy because the volume of debt was so large, both in absolute terms and in relation to other assets in the economy:

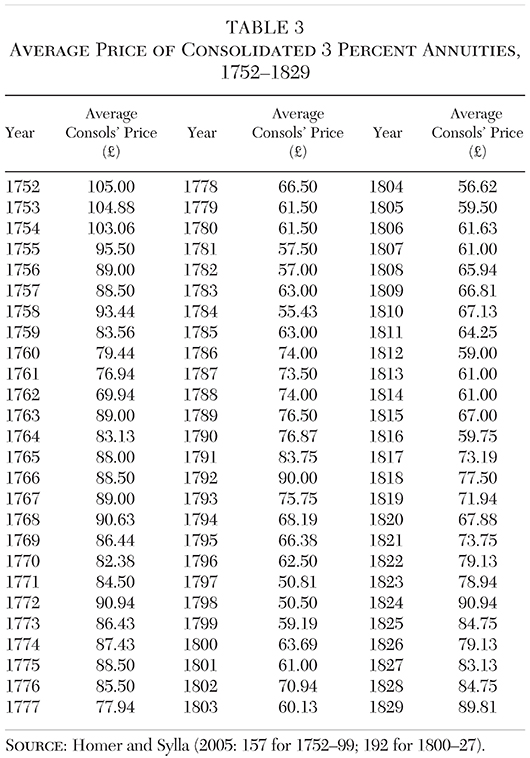

More precisely, there was a total of £562 million of 3 percent debt outstanding on February 1, 1817, in the month preceding which Consols’ average yield had been 4.72 percent, for a price of 63.6 percent (ignoring accrued interest), with holders having already enjoyed a 7 percentage point price appreciation since the recent low of August 1815. By April 1824, Consols’ yield had dropped to 3.16 percent, so the price had risen to 94.9 percent. In the period between August 1815 and April 1824, holders of 3 percent Consols enjoyed a capital profit of 38.3 percentage points, or a total of £215 million on the £562 million of 1817’s 3 percent debt. An additional profit of perhaps £10 million would have been received on the £75 million of 4 percent Consols, as their price rose toward and above par. Total profits to Consols holders over this period would then have been around 75 percent of GDP, equivalent to a profit of $14 trillion in current U.S. dollars. In addition, investors’ 1824 pounds were worth around 20–30 percent more than their 1815 pounds had been based on any of the Gayer-Rostow-Schwartz price series, the Rousseaux price series, or the Lindert and Williamson “best guess” cost of living index (Mitchell 2011: 721–22, 737). Taking the annual figures for 1815 and 1824, these give a deflationary rise in value of 28 percent, 25 percent, and 18 percent, respectively, primarily due to the resumption of gold payments in 1819–21.

One might say that this wealth was mostly brand new. Investors in August 1815 had put in only 57 percent for their 3 percent Consols and within a few years received a profit of 37 percentage points in capital gains plus interest at around 5 percent per annum on their initial investment. This profit was tax-free after the income tax had been abolished in 1816, and in any case capital gains had been untaxed. The capital gain was also permanent: once Consols had risen back to peacetime levels in the early 1820s, they fluctuated only moderately and indeed rose further until their price peaked late in the century.

Consequently, there was some 60 percent (from 1817) to 75 percent (from 1815) of GDP of new liquid capital in the early 1820s economy. In the early 1820s, this new money financed not only a number of subprime South American governments but also innumerable new factories and inventions that became the backbone of the Industrial Revolution.

Previous Periods of Rentier Enrichment and Impoverishment

It is interesting to observe that the same effect had occurred in the opposite direction in the 1790s. The price of Consols dropped from an average of 90 in 1792 to below 51 in 1797 and 1798. Since the nominal value of government debt in 1792 was about 120 percent of 1792 GDP, this fall caused a capital loss of about 47 percent of GDP in the first five years of the war.

Both Liverpool, the future prime minister (in 1796), and his father Charles Jenkinson (in 1798) wrote pamphlets proclaiming that Britain’s wartime economy was prospering, based on a substantial rise in exports and output over those years. However, the impoverishment of many savers during those years and the capital losses suffered by banks and other financial institutions starved the economy of capital. This latter point explains why Pitt in the 1790s had much more difficulty raising the necessary war finance than Perceval, Liverpool, and Vansittart did after 1807, and was a contributory factor to Britain’s going off gold in 1797.

One can trace this Consols’ wealth effect back further; Pitt’s benign economic conditions and growth in the 1780s were largely caused by a rise in Consols’ prices from £55 to £90 between 1784 and 1792.

It is clear that, owing to Gideon’s financing technique, the size of the government bond market, and its importance in the national economy, the “wealth effect” of fluctuations in bond prices far exceeded any Keynesian stimulus from wartime spending.

Consols in the Context of Overall Wealth Holding

Government bonds were only one of the forms in which wealth was held in the years after 1815. However, unlike other wealth they were highly liquid, and indeed were the only security quoted on the stock exchange from its founding in 1801 until 1822. Over the course of the 18th century, government securities (“the funds”) and Consols in particular had become the principal nonlanded form of wealth holding for merchants and the middle class, who tended to be more liquid than all but the richest aristocracy.

Nevertheless, agricultural land and to an increasing extent urban real estate remained an important component of British elite fortunes. Such forms of wealth storage as gold and silver plate had declined in importance since the 17th century as banks had proliferated, while bank deposits and insurance policies had appeared and at lower levels of wealth the savings bank movement was beginning its long 19th century climb.

The most important form in which wealth was held was still land, though its importance was beginning to decline during this period as mercantile relative wealth increased and landowners diversified their wealth into Consols. Prices of land had enjoyed a massive boom during the Napoleonic Wars, as corn prices had soared from an average of 43 shillings per quarter in 1794 to 127 shillings per quarter in the dearth year of 1812 (Mitchell 2011: 756). Then from 1813 to 1822 corn prices fell, bottoming out at 45 shillings per quarter in 1822 in spite of the 1815 Corn Laws, which had banned imports when the price was below 80 shillings. Jean-Baptiste Say, visiting England in late 1814, commented on the extraordinary profits made by agriculturalists during the war, and on their large investments both in bringing marginal land into cultivation and in mechanizing and up-scaling their operations (Say 1815).

Some of the landowner wealth acquired during the war was redeployed into industrialization, both during the war and in the years after, partly because the profitability of agricultural land declined after the war and did not recover for several decades.9

Consider the case of John Crichton-Stuart, 2nd Marquess of Bute (1793–1848). In 1814, he inherited a very large and liquid landed estate from his grandfather, including major land holdings in South Wales acquired through the 1st Marquess’s advantageous marriage as well as substantial holdings in the funds.

In 1817 he began surveying the Glamorgan coal fields, consolidating his local land holdings as he did so and building the Welsh coal mining industry during the 1820s. Between 1822 and 1848, he also developed the Cardiff Docks, opening the new Docks in 1837 at a cost of £350,000. His activity in both areas brought him huge debts of £494,000 at his death, although his assets greatly exceeded that value, and their profitability developed further, so that in the 1870s his grandson and heir was claimed (probably incorrectly, given the rise of American fortunes by that stage) to be the richest man in the world.

Between 1813 and 1822 the agricultural prosperity went into reverse. While costs fell somewhat, with the deflation attendant on returning to the gold standard in 1819–21, income from land fell considerably further, and landowners who, unlike Bute, did not have substantial outside holdings were sorely pressed. Their situation is well illustrated in an 1822 conversation between the diarist Harriet Arbuthnot, the young (28) wife of Charles Arbuthnot, a Treasury Secretary (junior minister) whose wealth was primarily in Consols, and her older (62) cousin the 10th Earl of Westmorland, Lord Privy Seal (a cabinet minister) and a large landowner:

I insisted that the cry of agricultural distress was grossly exaggerated, that the pressure felt by that class now was nothing compared to that suffered by the manufacturing districts in 1819, when 10,000 able and willing workmen were starving in one town (Glasgow) for want of work, and every other manufacturing town suffering in a like degree; that the farmers had got into luxurious habits which they did not choose to give up and therefore joined in the cry of “No Taxes;” that those persons who had borrowed money at 5 per cent interest during the war to buy land would suffer as any body did who borrowed money to buy any thing; but that the great landed proprietors would weather the storm and be just as well off as ever; that there would certainly be a transfer of property, but that the country generally would be as rich as ever and that there could not be a greater proof of it than the enormous increase of the Revenue in every branch. He said I talked nonsense and was very childish (which, by the way, is no argument) and that the transfer of property I talked of so quietly would be a greater revolution than even a bankruptcy of the funds.10

Shares were a relatively insignificant store of wealth in post-1815 Britain, with total public share capital paid in of £49 million in 1827, of which £34 million related to companies formed before 1824. The 624 companies floated in the bubble of 1824–25 had a nominal capital of £372 million, but only £15.2 million of this capital was ever paid in; by 1827, when the dust settled, that had declined in value to £9.3 million. Share prices in 1815–27 were not especially buoyant, in spite of the bubble of 1824–25; on a quarterly average basis the share index rose by only 61 percent, from 3.1 in the second quarter of 1815 (1962 = 100) to 5.0 at the peak in the third quarter of 1824. The bubble thereafter deflated, with the index in the fourth quarter of 1825 being only 4.44, and 4.1 in the fourth quarter of 1827. Changes in share wealth were clearly not economically significant during these years.11

There was one final form of nonland wealth that underwent a major boom in the early 1820s before collapsing in 1825–26: foreign bonds. In 1817–18 several European governments floated bonds totaling £10 million, while in the boom of 1821–25 some £43 million12 was invested in foreign bonds, of which £37 million related to Latin American issues. These investments were a substantial absorber of British capital, especially during the 1822–25 period as declining yields on Consols caused investors to seek higher returns elsewhere. However, the profits and losses involved do not appear to have been significant, except in the immediate aftermath of the 1825–26 crash.

Who Were the Rentiers?

Information on the owners of Consols can first be gained by examining the estates of the very wealthiest. Three died between 1809 and 1839 who are believed to have been Britain’s first millionaires: (1) Nathan Rothschild (1836), worth £5 million, whose fortune was largely in Consols and other liquid securities, and who is known to have grown very much richer in the decade after 1815; (2) the 1st Duke of Sutherland, formerly Marquess of Stafford (1833), worth £2 million, whose fortune was largely in land, but with substantial agricultural and industrial development including the Bridgewater Canal; and (3) Sir Robert Peel (1830) father of the future prime minister, worth £1.5 million, whose fortune was derived from the family cotton mill business that had employed 15,000 people at its peak, but by his death consisted largely of Consols, houses, and land.13

Lower down the scale it is notable that the five-year average of the annual number of nonland fortunes above £100,000 among the newly deceased took a sharp upward turn, from 16.5 in 1809–14 and 18.2 in 1815–19 to 25.6 in 1820–24, and 29.0 in 1825–29. It then did not rise significantly further until after 1855 (Robinson 1985: 47). Although Robinson could think of no explanation for this increase, the jump’s coincidence with the recovery in Consols’ prices suggests that Consols formed a high proportion of the wealth covered by these statistics, which derive from probate valuations that do not include real property and therefore relate primarily to mercantile rather than aristocratic fortunes. At the same time, including land changes the wealth picture considerably: more than 80 percent of people worth more than £100,000 in 1825 were primarily landowners.

Of the nonlanded rich dying in the 1820s, a high proportion were in the City of London, either as merchants, bankers, or in insurance or stockbroking — 15 of the 24 with nonland wealth from £500,000 to £1 million died between 1820 and 1839. It can safely be assumed that the great majority of these fortunes would have been held in Consols. Of the other nine, the three in textiles, the one in publishing, and the two in public administration and defense will also have held a high percentage of their nonland wealth in Consols, since none of those occupations is capital intensive. Only three of the 24, with principal occupations in iron/steel, chemicals, and brewing may have held relatively small stocks of Consols, with the majority of their nonland wealth in their primary businesses.

The same analysis carried out on the “lesser wealthy” who died with nonlanded wealth between £100,000 and £500,000 in the years 1809–29 shows a similar pattern: 117 of the 154 such people either were merchants, worked in finance, were professionals, or worked in public administration. Since these people had little need for plant and equipment, the majority of their nonland wealth would have been held in Consols.14

We can then conclude that the capital gains from the Consols’ price increase in 1815–24 had a major effect on the net worth of nearly all those with substantial nonlanded wealth, many of whom like Bute may also have had large landholdings.

In this context, the wealth accumulation patterns of early 19th century industrialists, from Sir Robert Peel downward, should also be borne in mind. There was no public equity market available to raise money for industrial companies, and bank loans were not available for long maturities except for a moderate proportion of the value of buildings and land. Hence, businesses were built up by collaboration between entrepreneurs through private partnerships, formed, and dissolved as needed.15

The members of those partnerships, once the initial investment in plant had been made, kept substantial balances of liquid assets to meet the need for new investment and to protect the business against downturns, which could be severe and unexpected. Consols, utterly safe, highly liquid, and yielding a decent return (and a superb return in 1815–24) were a favorite holding for such people, who in the early 1820s found themselves through their Consols’ holdings very much richer than before. It is then fair to presume that Consols’ windfalls paid for much of the industrial expansion in the 1820s and its accompanying capital intensification.

Economic Effects of Rentier Apotheosis

Britain’s economy in 1814 was already qualitatively different from any other in the world, or from its own state 30 years earlier. The French economist Jean-Baptiste Say visited Britain in late 1814, after the peace but before Napoleon’s return from Elba, and set out his impressions in a pamphlet De l’Angleterre at des Anglais:

But it is principally the introduction of machines in the arts, which has made the production of riches more economical. There are almost no big farms in England, where for example, threshing machines are not used, by means of which, in a large operation, more work is done in a day than was done in a month by ordinary methods.

At last human labor, which has rendered the high cost of consumer goods so expensive, is in no circumstances replaced so advantageously, as by steam engines, improperly called “fire-pumps” by some. There is no work which cannot be reached to be executed by them. They go to the mills, weaving cotton and wool; they brew beer, they cut crystals. I have seen them embroider muslin and beat butter. At Newcastle, at Leeds, I have seen moving steam engines dragging after them carts of coal; and nothing is more surprising, at first sight, for a traveler, than to meet in the country long convoys which advance by themselves and without the help of any living being.

Everywhere steam engines are prodigiously multiplied. There were no more than two or three in London thirty years ago, there are thousands at present. There are hundreds of them in the large manufacturing towns; one sees them even in the countryside, and industrial works could not be sustained profitably without their powerful help. But they must have abundant coal, that combustible fossil which Nature seems to have reserved to supplement the exhaustion of forests, the inevitable result of civilization. Thus one could, with the help of a simple mineralogical map, trace an industrial map of Britain. There is industry everywhere there is coal in the ground [Say 1815: 29–31].16

Say also noted that high British taxation and the gigantic government debt were of immense importance in raising the cost of everything in Britain and depressing the profits of business and commerce. He believed British goods would be uncompetitive in Europe once the European economies had recovered from the war. Writing while Consols’ prices were still depressed, Say failed to foresee the effect of their subsequent rise. Liverpool however foresaw that effect in the following year, during the postwar economic downturn. Writing to George Canning on February 13, 1816, and discussing the clamor to abolish the income and malt taxes (which in the event succeeded) he wrote, “I am satisfied likewise that those who raise this clamour have a narrow view of their own interest, as the restoration of public credit, the run of the funds, and the consequent fall of the interest on money will afford more relief to the existing distress of the country than any other measure of relief that could be adopted.”17

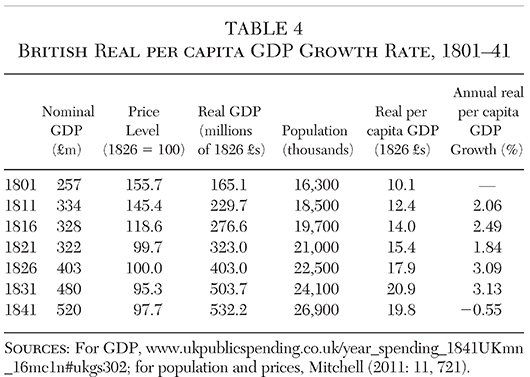

Table 4 sets out U.K. (including Ireland) population, GDP, and GDP per capita figures for 1801–41, at 10-year intervals, with five-year additions for 1816 and 1826. The GDP figures are of course a backward extrapolation of a statistic (and a questionable one at that!) that was only invented a century later, but for what they are worth they show a distinct acceleration in growth of per capita GDP, from 2.16 percent per annum to 3.11 percent per annum between the decades 1811–21 and 1821–31. Note also that, with population expanding at a very rapid rate of around 1.3 percent annually, the 1820s growth rates are spectacular even by modern standards, indeed considerably higher than was to be achieved in any subsequent decade.

Gayer, Rostow, and Schwartz use brick production as a measure of economic activity in capital goods; this increased from an annual average of 791.2 million in 1815–18 to 992.4 million in 1819–22 to 1,501.7 million in 1823–26; the 1825 figure of 1,948.8 million was the highest in any year before 1846 (Gayer, Rostow, and Schwartz 1953: 121, 147, 186).

Other indicators show a similar picture of economic acceleration after 1820. Coal shipments from Newcastle and Sunderland rose from an annual average of 1,083 thousand chaldrons in 1814–19 to 1,249 thousand chaldrons in 1820–26 (Mitchell 2011: 243).18 Pig iron production rose from an annual average of 305 thousand tons in 1814–19 to an annual average of 453 thousand tons in 1820–26 (Mitchell 2011: 280). Raw cotton consumption rose from an annual average of 96 million pounds in 1814–19 to an annual average of 147 million pounds in 1820–26 (ibid., 332). Manufactured goods exports at constant prices, mostly textiles, rose from £15.3 million in 1814–19 to £17.9 million in 1820–26 (ibid., 520).

The Hoffman index of industrial production rose from an average of 9.39 in 1815–18 to 10.67 in 1819–22 and then to 12.28 in 1823–26 (ibid., 431). Perhaps most significantly, the annual average number of English patents granted fell slightly from 114 in 1815–18 to 105 in 1819–22, but then soared to 177 in 1823–26 — surely a sign of entrepreneurial activity in those years, though it fell back to 153 in 1827–30 (ibid., 438).

Thus, the overall real return to Consols’ investors over the period 1813–24 was in excess of 300 percent. If they held on and reinvested income during that period, Consols holders quadrupled their money in real terms.

The mechanism by which British economic growth benefitted from the 1815–24 rise in Consols’ prices is well set out in Gayer, Rostow, and Schwartz (1953: vol. 1, 185):

The character of the (1822–26) cycle as a whole, however, can be distinguished from earlier cycles by the scale and the scope of new private investment. There was an increase in railways construction, new docks were built, and what appears to be the greatest building boom until the forties took place. Gas-light, insurance, building, trading, investment, provision companies, in addition to many others, were formed on a large scale. These, the fluctuations of foreign government and mining issues and the fabulous Stock Exchange boom and crash (1824–25) impart to these years their unique character.

The economics is clear. For the British economy to industrialize, its capital intensity had to increase. This increase accelerated in the decade after Waterloo, and Consols’ profits provided wealth enabling this increase to take place more quickly, more smoothly and with less pressure on workers’ living standards than would otherwise have occurred.19

Gayer, Rostow, and Schwartz (1953: vol. 1, 185) blame the excess speculation in 1824–25 on two additional factors, both of which seem pertinent. First, in April 1822, the government had extended the privilege of country banks issuing £1 and £2 notes, which had the effect of an unexpected increase in the money supply. Second, the double refinancing of 5 percent and 4 percent Consols in 1823–24 produced “a restless feeling and a disposition to hazardous investment,”20 and a surge in foreign bond purchases.

The extent of the speculative fervor was spelled out by a contemporary stockbroker, Henry English, and his analysis has remained authoritative to this day.21 Briefly, English listed 624 companies that were floated in the years 1824 and 1825. They had a capitalization of £372,173,100. By 1827, only 127 of these existed with a capitalization of £102,781,600, of which only £15,185,950 had been paid in; but the market value had sunk even lower to only £9,303,950. Of the 127 still existing in 1827, 44 were mining companies (mostly in Latin America), 20 gas companies, 14 insurance, and 49 miscellaneous, including salt, silk, lard, bridge, emigration, glass distilling, brick, bank, and agricultural companies.

In addition, 15 railway companies were formed by Acts of Parliament in 1823–26, for a total projected construction cost of £3.64 million, of which the Stockton and Darlington, authorized in 1823 at a cost of £450,000 and opened in 1825, and the Liverpool and Manchester, authorized in 1826 at the immense construction cost of £1,832,375, more than all the rest put together, and opened in 1830 in the presence of the Duke of Wellington, are the most famous. The experimental and dangerous nature of this technology is indicated by the fact that the Stockton and Darlington used steam trains only for goods traffic, with passengers being drawn by horse carriages until 1833, while the Liverpool and Manchester accidently knocked over and killed the former Cabinet Minister William Huskisson at its opening on September 15, 1830.

Mrs. Arbuthnot was a keen observer of the stock market bubble of 1825, which she discussed in detail with Wellington, who thought it would all end in a crash (as did Liverpool, who said so in the House of Lords). However, she could not resist a good speculation herself:

There is a railway going to be made between Liverpool and Manchester which promises to answer immensely. We have 10 shares in it for which we gave £3 a piece and which are now worth above £58 each and they are expected to be worth above £100. I am very fond of these speculations and should gamble greatly in them if I could, but Mr. Arbuthnot does not like them, and will not allow me to have any of the American ones as their value depends on political events and he thinks in his official situation it would be improper [Bamford and Wellington 1950: vol. 1, 382].

Improper or not, Mrs. Arbuthnot got in on the ground floor. Her diary entry was dated March 16, 1825, and the Liverpool and Manchester Railway Company had been formed in 1823. However, its first attempt to get Parliamentary authorization in 1825 failed (largely through opposition by the Marquess of Stafford, owner of the competing Bridgewater Canal), and it gained authorization only at a second attempt in May 1826.

Since Arbuthnot had been what today would be called the government’s Chief Whip in the House of Commons (though he had given up that job in 1823 while remaining a junior minister as Commissioner for Woods and Forests) his 10 shares (of an eventual total of 4,233, spread among 308 shareholders, with Stafford eventually owning 1,000) may have been a special allocation. It was however not quite the handout it appears. Following corporate finance practices of the time, the shares will have been partly paid, with say £10 paid on a £100 share, and Arbuthnot will have been called for the other £90 when Parliament had approved the company and construction began. While £900 was affordable for the comfortably off Arbuthnots, larger sums would not have been, so Arbuthnot was right to stop his wife punting on South American mining companies. Nevertheless, their Liverpool and Manchester Railway investment was a successful one, if they kept it; the company paid an average dividend of 9.5 percent in its 15 years as an independent company.

Since the Bubble Act, requiring an Act of Parliament to form a new company, was not repealed until 1826, much of the new investment in 1822–25 was informal and small-scale, in start-ups and other kinds of experimentation. The surge in patents granted in 1823–26 itself confirms that the surge in Consols’ wealth allowed exploration of projects that were not immediately profitable. One such project, far more famous in 2017 than it was at the time, was that carried out by Charles Babbage.

Babbage was a typical beneficiary of the surge in Consols’ prices. His father was a partner in the banking house of Praed & Co., whose wealth, like that of most bankers, will have been substantially augmented by the rise in Consols. Babbage was partly supported by his father and inherited a fortune of £100,000 when his father died in 1827. However, the initial funding for his difference engine project came not from his father but from Liverpool’s government, which made a grant to Babbage of £1,700 in 1823 to start work on the project. Alas, endless redesigns meant the prototype was never finished, and the government, under the unimaginative Sir Robert Peel (son of the textile millionaire) canceled further funding for the project in 1842 after it had absorbed £17,000 of public money.

In spite of Babbage’s failure, the statistics show that the pace of innovation, industrialization, and Britain’s overall economic growth quickened substantially in the early and middle 1820s, and that the new wealth produced by the return of Consols’ prices to peacetime levels substantially contributed to this quickening. Britain’s industrial lead established during this period was not to be relinquished until the last quarter of the century.

Conclusion

The rise in Consols’ prices in 1815–24, under the able economic management of Lord Liverpool created not the “euthanasia of the rentier” of Maynard Keynes’ leftist fantasies but his apotheosis, in which, combining the rise in Consols and given the decline in prices that accompanied the return to gold, rentier nonland wealth nearly quadrupled in real terms during Liverpool’s premiership. That increase in wealth coincided with and likely produced a surge in capital investment and innovation, which, apart from the follies of the Latin American bond market, produced the first great surge of the Industrial Revolution, with U.K. economic growth accelerating to unprecedented levels.

References

Ashton, T. S. (1948) The Industrial Revolution 1760–1830. Oxford: Oxford University Press.

Bamford, F., and Wellington, 7th Duke, eds. (1950) Journal of Mrs. Arbuthnot. London: Macmillan.

Gayer, A.; Rostow, W. W.; and Schwartz, A. J. (1953) The Growth and Fluctuation of the British Economy, 1790–1850. Oxford: Clarendon Press.

Hansard, T. C. (1815) The Parliamentary Debates from the Year 1803 to the Present Time, Vol. 31.

__________ (1817) The Parliamentary Debates from the Year 1803 to the Present Time, Vol. 36.

Homer, S., and Sylla, R. (2005) A History of Interest Rates, 4th ed. Hoboken, N.J.: Wiley.

Keynes, J. M. ([1936] 1977) The General Theory of Employment, Interest and Money. London: Macmillan.

Mitchell, B. R., ed. (2011) British Historical Statistics. Cambridge: Cambridge University Press.

Neal, L. (1998) “The Financial Crisis of 1825 and the Restructuring of the British Financial System.” Federal Reserve Bank of St. Louis Review 80 (May–June): 53–76.

Say, J. B. (1815) De l’Angleterre et des Anglais. Paris: Chez Arthur Bertrand.

Tooke, T. (1838) A History of Prices. London: Longman.

Ventura, J., and Voth, H. J. (2015) “Debt into Growth: How Sovereign Debt Accelerated the First Industrial Revolution.” NBER Working Paper No. 21280.

Williamson, J. G. (1984) “Why Was British Growth So Slow during the Industrial Revolution?” Journal of Economic History 44 (3): 687–712.

Yonge, C. D. (1868) The Life and Administration of Robert Banks Jenkinson, Second Earl of Liverpool. London: Macmillan.

1 The securities issued in the 1751 refinancing paid 3.5 percent interest for the first six years, then 3 percent from 1757. There was a further refinancing in 1888, carried out by Chancellor of the Exchequer George Joachim Goschen, into new securities paying 2.75 percent from 1888 to 1903, then 2.5 percent thereafter. Thus, the classic “3 percent Consols” existed without refinancing from 1757 to 1888.

2 Homer and Sylla (2005: 57 for 1752–99; 192 for 1800–27). We take the Homer–Sylla estimate of annual average prices as the basis for these calculations.

3 Quoted in The Economist, “Percents and Sensibility,” December 20, 2005.

4 A more elaborate explanation might go as follows. The prices of Consols surged primarily because of a decline in supply as the Napoleonic Wars ended and the government moved toward fiscal surplus. Moreover, because Consols were almost the only store of liquid wealth, their price rise would have made investors wealthier — thereby creating an even greater demand for Consols. It is noteworthy that the two main investments available to the rich were Consols and land, but land became much less profitable after 1815 as grain prices declined. Stocks and bonds were relatively unimportant (though a small foreign bond market arose in the 1820s), while direct investment in companies was risky, illiquid, and poorly diffused among the investing public.

In loanable funds terms, the primary driving factor in the market for Consols — the decline in supply — would correspond to a reduced demand by the government for loanable funds.

5 The debt figure jumps in 1818 because of the inclusion of Irish government debt from that year onward.

6 There is, thus, the following implied counterfactual. Reduced supply of Consols, itself associated with a move toward fiscal surplus, combined with increased demand for them and the anticipated then actual resumption of specie payments at the old parity to create a secular decline in interest rates. Falling yields also suggest that, contrary to Ashton (1948) or Williamson (1984), fiscal crowding out was no longer an issue by this period.

7 This, and much other useful information about British government financing in 1815–25, is set out in Neal (1998).

8 Vansittart’s budget is contained in Hansard (1815: cols 795–822, June 14).

9 This is largely consistent with the theoretical analysis of Ventura and Voth (2015): landholders experienced wealth gains from their Consols that led them to switch out of low-return agricultural investments, thereby lowering factor demand in the old sectors and raising profitability in the new sectors.

10 Bamford and Wellington (1950: vol. 1, 139), diary entry for February 2, 1822.

11 Flotations in 1824–25: Stockbroker Henry English, quoted in Neal (1998: 64). Share price index: Bank of England Statistics “Share Prices in the United Kingdom” held in the St. Louis Fed.’s FRED database, accessed March 3, 2017.

12 Figures quoted on foreign bond issues are from Neal (1998: 63) and the detail is from Gayer, Rostow, and Schwartz (1953: vol. 1, 188–89).

13 Data on these holdings of the very rich are contained in Robinson (1985).

14 Data on the occupations of the dying wealthy in these paragraphs come from Robinson (1985: 82–87).

15 Manufacturers themselves did not borrow for long-term plant investment, but accumulated retained earnings and savings, much of them in Consols, which were more secure than the local English banks. The brokers and embryonic “merchant banks” did not invest directly in industry, but country banks lent to it, and would have been encouraged to lend more by the Consols-driven increase in their capital. The capital gains accrued to small holders as well as large and gave manufacturers more capital with which to expand their own factories or invest in other people’s. The holdings of Consols in manufacturing districts were also more significant for industrialization than those among the gentry, who had limited ability to access industrial investment opportunities and tended like Mrs. Arbuthnot to buy South American bond issues and shares, mostly in canals and early railways.

16 Martin Hutchinson’s translation.

17 Quoted in Yonge (1868: vol 2: 253–55). The italics are ours, and we take “the run of the funds” to be a direct reference to the price rise to be expected as public credit recovered.

18 The chaldron was a volume measure used for coal. By a law of 1694, the Newcastle chaldron of coal was defined to weigh 5,940 pounds.

19 There is a good counterexample in the 1831–46 period that supports our main thesis, a decade without significant Consols’ profits but with the massive capital needs for the railways. During this period, the economy underwent the “Engels pause” without rising living standards, as manufacturing was starved for capital. Engels believed living standards would never rise and had never risen. He was wrong but writing in 1844, after a decade of stagnant real wages and the 1820s ebullience had been forgotten. Our point is that, without the Consols’ profit, new capital needs for the industrializing and capital-intensifying economy were hard to come by, and could only be gotten slowly by the workers being squeezed.

20 Gayer, Rostow, and Schwartz (1953) quoting Tooke (1838).

21“A Complete View of the Joint Stock Companies Formed during the Years 1824 and 1825,” Henry English, 1827, quoted in Neal (1998: 64).

About the Authors