Congress should

-

recognize that the U.S. economy has experienced a significant fall in its long-run sustainable growth rate, with a recent pace of growth one-half that seen through the postwar 20th century;

-

prioritize raising the country’s growth potential, given that faster growth would beget higher living standards, stronger public finances, and less zero-sum politics;

-

understand that policy changes can affect both the level of gross domestic product (and so short-run growth) and the long-term growth rate;

-

realize that a lot of “pro-growth” policies entail federal, state, and local governments doing less, liberalizing rules, or regulating less intrusively; and

-

seek out pro-growth reforms that attract support across broad swaths of the political spectrum.

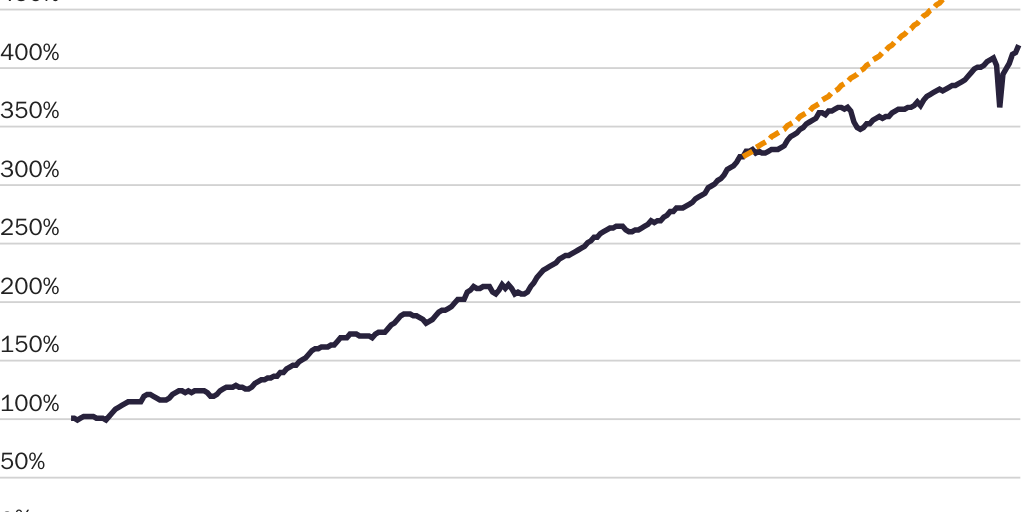

The United States has seen a major decline in its growth trajectory in the 21st century. From 1947 to 2000, real (i.e., inflation-adjusted) gross domestic product (GDP) per capita rose at an average annual rate of 2.3 percent. The long-term growth path remained remarkably steady over time, with recessions followed by strong catch-up growth. Yet between 2000 and 2021, real growth in equivalent terms averaged just 1.1 percent—less than half the rate seen in the 20th-century postwar period.

Since the turn of the millennium, the United States has endured two massive recessions. The Great Recession of 2007–2009 shrank overall GDP per capita by 5.1 percent and was followed by a historically anemic recovery. After reasonable growth in 2018 and 2019, the country was then ravaged by the COVID-19 pandemic, with its combination of government lockdowns and voluntary retreats from in-person activity. These setbacks, coupled with the fall in underlying trend growth, mean that GDP per capita at the end of 2021 was as much as 27.6 percent below where it would stand if the postwar growth rate through 2000 had persisted over the past two decades (see Figure 1).

This growth downturn is expected to endure. The Congressional Budget Office assumes, for example, that the annual sustainable real per capita GDP growth rate will be 1.1 percent per year from the late 2020s through most of the next three decades. Accounting for population growth, that translates to overall real GDP growth of 1.5 to 1.6 percent per year (compared with the 3.6 percent average rate seen from 1947 to 2000).

A “New Normal” of Slow Growth?

There are structural forces that imply that a big growth slowdown was always to be expected.

As my former colleague Brink Lindsey outlined in the 2017 Cato Handbook for Policymakers, real per capita growth can occur from (1) growth in labor participation, or annual hours worked per capita; (2) growth in labor quality, or the skill level of the workforce; (3) growth in capital deepening, or the amount of physical capital invested per worker; or (4) growth in so-called total factor productivity, or output per unit of quality-adjusted labor and capital. Sadly, there are significant headwinds against all these components of growth.

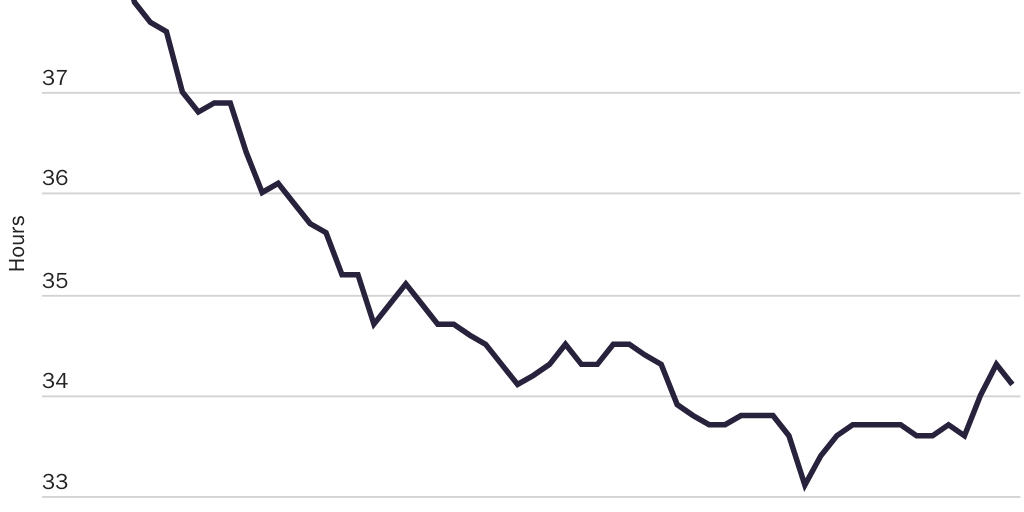

First, you can get more output per head if a higher proportion of the population works or if the average number of hours of those already working increases. Between the mid-1960s and 2000, average annual hours worked per capita increased from less than 800 to more than 950, powered by rising labor force participation among women and the influx of baby boomers into the workforce. But now we have an aging population that has pulled down the proportion of the population in the labor market (see Figure 2). Meanwhile, among employees, the secular trend as we have gotten richer and more productive is for workers to work fewer hours, not more (see Figure 3). Although in recent years this trend has plateaued—meaning it’s less of a drag on growth than before—there is no reason to expect a sharp rebound soon.

Second, in the postwar period, the United States benefited from growth occurring because of the low-hanging fruit of an increasingly better-educated workforce. Harvard economists Claudia Goldin and Lawrence Katz have estimated that rising educational attainment may have accounted for about 15 percent of total growth over the period 1915–2005, as years of education increased while access was broadened. But the education level of the workforce has since largely plateaued and, in any case, adding yet more additional years of formal education would have sharply diminishing returns.

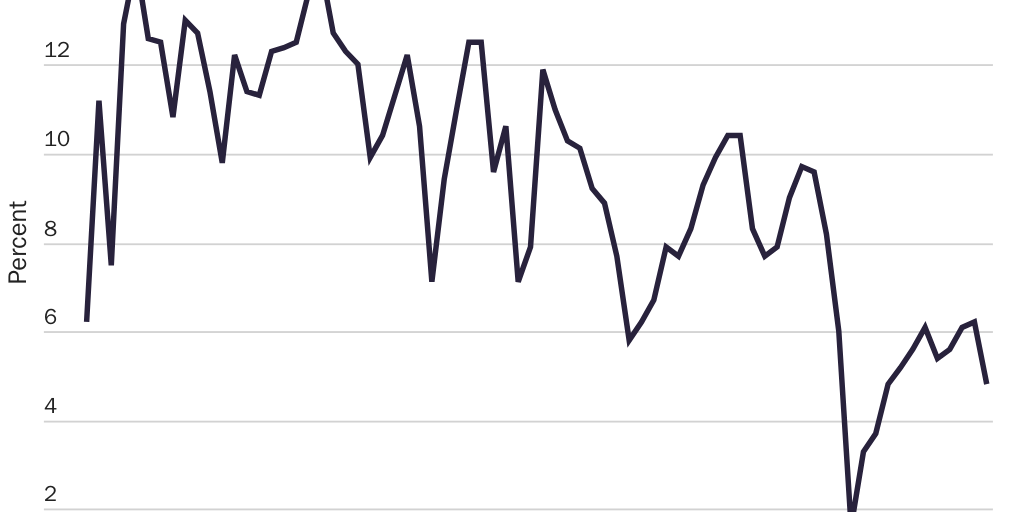

Third, capital investment can be a source of growth: workers with more and better tools can produce more. Yet net national investment (investment net of depreciation charges) as a percentage of net national product has been in a volatile, yet downward, trend for decades (see Figure 4). There are significant measurement issues with regard to this trend, not least due to the rise in importance of “intangibles”—investments in nonphysical capital, such as organizational capabilities, branding, or processes. That notwithstanding, without meaningful policy reform, it’s unclear why we would expect an investment boom to counteract the unfavorable trends regarding hours worked and worker skills.

That makes the fourth and final source of growth even more important: innovation. That is, the introduction of productive new technologies or better ways of combining inputs to produce more or new output by improving efficiency, managing resources better, or inventing popular new products.

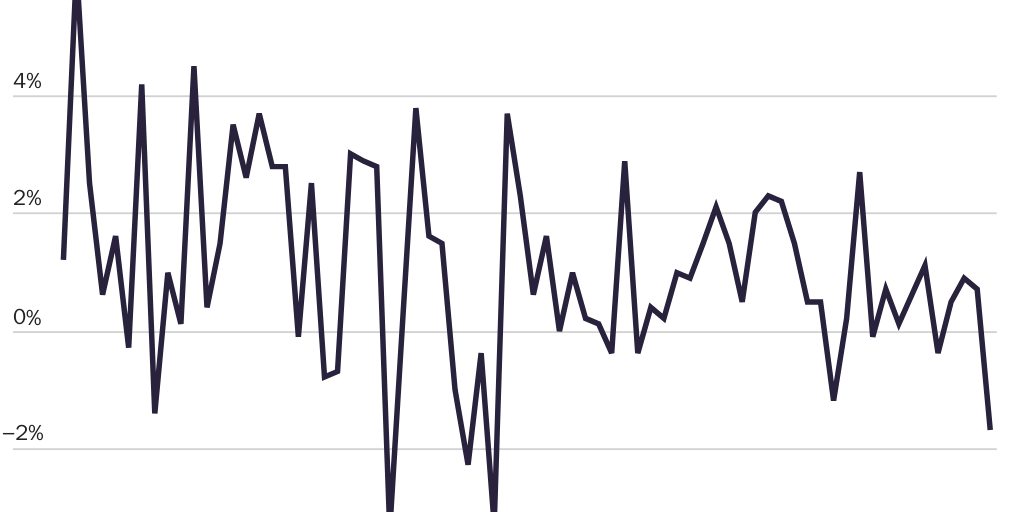

The prospects for this source of growth are unclear and unpredictable. Economist Robert Gordon’s very pessimistic book, The Rise and Fall of American Growth: The U.S. Standard of Living since the Civil War, suggests that the United States has exhausted the low-hanging fruit of certain major general-purpose technologies, such as electricity, and that we are unlikely to see similarly transformative innovations like this again. Some economic historians, such as Deirdre McCloskey, have suggested that certain ideas permeating through culture about the virtues of market-tested betterment are key to explaining the growth takeoff in the past two and a half centuries. Given the unpredictability of innovation, and of political and ideological support for it, forecasting future innovative growth trends is incredibly difficult. This source of growth is difficult to identify and measure, even retrospectively. Economists typically talk as if we can estimate it as synonymous with total factor productivity growth—a residual measure of the improvement in output after controlling for the amount and quality of labor and capital inputs. As Figure 5 shows, nothing in the data suggests a sufficient innovation takeoff to offset the trends previously mentioned. It’s possible that the integration of artificial intelligence, the metaverse, and more can lift trend growth in the future. Innovation tends to be unpredictable and volatile, with new ideas often appearing unexpectedly, but the data do not yet reflect an innovation “get out of jail free” card.

The Importance of Growth

The fact that major structural trends, such as population aging, are depressing growth, and that other advanced economies have also seen growth slowdowns, suggests that reversing these trends will be extremely difficult.

Nevertheless, we should not be resigned to growing at such a slow rate. Labor participation, labor quality, investment, and innovation are all affected by federal, state, and local policies, which shape the incentives of individuals and businesses to engage in productive activities and affect the broader allocation of resources. In other words, policy can affect our growth prospects. Better policy can make us better off.

Given the economic and political benefits of growth, in fact, the observed headwinds against it make it imperative that policies currently impairing either the level of GDP or its growth are reformed or excised. The stakes are high. If the per capita annual GDP growth rate could be increased from its current projected 1.1 percent to, say, 1.5 percent, then the power of compounding means that after 50 years, we’d be 22 percent better off than in the slower growth scenario. Put another way, with a 1.1 percent growth rate, GDP per capita would double every 64 years. With growth at 1.5 percent or even 2 percent, that figure would fall to 47 years or 36 years, respectively.

GDP is certainly not everything, as the COVID-19 pandemic showed. Curbs on our personal liberties do not all show up in GDP, but we clearly value those liberties immensely. In a free society, individuals may accept a slower growth of GDP in exchange for more leisure time to enjoy the fruits of their income, and that is perfectly reasonable. A lot of the benefits of modern technological advances, including free social media services, do not show up in GDP. GDP may also decline in the process of eliminating curbs on activities that harm the environment in unsustainable ways but that nevertheless improve human welfare. It is obvious, then, that governments should not chase GDP growth at all costs.

But subject to these constraints, a society of more sustainable abundance over time produces better results for virtually everyone. As economist Tyler Cowen has argued when advocating for the maximization of “wealth plus”—sustainable economic growth—as an ultimate societal goal, few would quibble that “it is much better to live in the United States than Albania, or better to live in Denmark than Burkina Faso.” That may sound trite, but the implications of growth apply over time for a country on the frontier of progress, just as much as between them today.

If we acknowledge that obtaining a more prosperous United States is desirable, then we should take raising the sustainable growth rate much more seriously as a policy objective. In doing so, we would worry far less about redistributive programs and far more about investment incentives. We would ponder less about how to revive struggling areas and think more about removing government constraints that prevent thriving areas from expanding. We would generally be much more open to economic freedom over providing economic security, given that the former is strongly correlated with broad-based measured prosperity.

A higher sustainable growth rate would not only leave more dollars in people’s pockets; higher living standards over time are associated with better health, more creativity, a widening of access to cultural wonders, more sustainable federal finances, and so much more. As a bonus, faster growth also makes politics less zero-sum. When living standards are rising for most, one person’s large gains are less likely to be seen as a threat to others. It should not surprise us that over the past two decades of slower growth, politics has become uglier, with scapegoats—whether billionaires, international elites, or immigrants—being blamed for our social and economic problems.

Although the growth headwinds are real, we have largely taken rising living standards for granted during recent decades. Macroeconomic debates have focused on the role of fiscal and monetary policy in reducing GDP volatility by alleviating recessions, rather than on long-run growth.

The implied consensus of the focus of much commentary was that, provided governments kept “aggregate demand” on a stable path, then sustainable growth driven by innovations and business investment would just happen on its own accord. Or, at least, that this demand-stabilizing role was more important or feasible than attempts to raise the long-run growth rate. Two decades of historically slow growth, coupled with the recent inflationary pressures, have since reemphasized the importance of the supply side of the economy: its capacity to produce more and higher-value goods and services and the way the government shapes this.

Although neither the left nor right of American politics seems ready to throw out their shibboleths in favor of a full-throated pro-growth agenda just yet, the COVID-19 pandemic does appear to have convinced many of a broader domestic economic sclerosis that is largely driven by misguided policies and institutional failures.

In the United States, it is difficult and costly to build infrastructure in the right places, to find the workers you need, or to get approval for innovative new projects. The pandemic saw a period in which the United States lagged other countries in approving cheap, at-home rapid diagnostic tests. Supply chain disruptions have been exacerbated by protectionist policies and local regulations on ports. As the case studies pile up, people are coming (often indirectly) to the view that structural reforms are required to enhance the market sector’s ability to produce goods and services or to adapt to changing circumstances. Many of these ideas could raise the level or growth rate of economic activity.

A Pro-Growth Agenda

Politicians should aspire to a more meaningful growth focus than just an ad hoc fix for certain egregious problems. In theory, better policies could create new economic capacity directly or else could lower the costs of engaging in investments or activities that later increase it.

Most economic reforms would have level effects for output (promoting a one-time, but permanent, rise in GDP, with growth increasing during the transition to this higher level of activity). Some, though, may even raise the rate of innovation, permanently raising the growth rate of the economy.

Much of the rest of this Handbook discusses policy ideas that, by liberating markets from government, would also have the happy side effect of raising the economy’s productive potential. It’s therefore unnecessary to delineate a comprehensive guide to what a pro-growth agenda would look like here. But scholars have discussed many of its headline components since 2014, when Cato asked 51 top economists for ideas on how to boost the sustainable growth rate.

Regulatory reforms that remove anti-competitive product market regulation, reduce administrative burdens on firms, limit government interventions to alleviating genuine market failures, and sunset regulations to avoid their accumulation are a set of broad but important pro-growth regulatory principles that could deliver higher market output at lower cost.

The current thicket of environmental, land-use, and zoning regulations that inflate the cost of and delay new private-sector infrastructure and housing being supplied in productive areas is especially ripe for an overhaul. They not only make the economy less adaptable to changing wages and prices, undermining efficiency, but also snuff out the benefits of dense, productive agglomeration of industries in certain cities.

Tariffs and other trade restrictions today heighten input costs and reduce competitive pressures on our producers to become more efficient. The Jones Act—a 1920 law that requires all intrastate shipping to use expensive U.S. merchant marine vessels—not only raises transportation costs, causing all sorts of downstream inefficiencies, but also causes enormous collateral damage. Then there are “Buy American” provisions, which waste resources by causing the U.S. federal government to overpay relative to world prices in procurement, while requiring an extensive bureaucracy to administer and police.

Plenty of government-erected barriers stand between workers’ taking up employment or moving to new roles. Welfare and other entitlement programs create large disincentives to work or to earn more labor income. Labor laws and regulations drive up hiring costs. Occupational licensing requirements, compulsory unionization, regulatory compliance burdens, and more create entry barriers to new jobs.

Immigration restrictions choke off a crucial source of new entrepreneurship and labor supply, especially in areas where regulatory-induced restrictions raise costs, such as health care and childcare. One consequence is the safety valve of a large illegal migration sector, with a lot of activity occurring in the shadow economy. We should make legally migrating to the United States easier, especially for the most talented researchers, scientists, and entrepreneurs.

The tax code (especially in its interaction with welfare programs) is littered with perverse incentives against work, production, investment, and innovation. Tax reform that eliminated distortions and lowered rates would increase efficiency and be pro-growth.

Then there are the relatively poor state of schooling and the high cost of health care across much of the country. More choice, fewer restrictions on entry into those respective markets, and money following students or patients could all help marry individuals’ needs in ways that deliver better human capital accumulation and cheaper health care.

Any individual regulatory or policy change in these domains might appear to have only a small impact on GDP or the economic growth rate. But the cumulative effects of a pro-growth focus could meaningfully improve the economy’s productive potential and its adaptiveness to ever-changing circumstances. Raising the sustainable growth rate as an overarching ambition should, in theory, get politicians thinking about change across all the areas of economic activity outlined.

Sadly, despite all the benefits of economic growth and the country’s shared interest in achieving it, most of these policy debates are highly polarized and politically charged. Liberalization of markets typically entails undermining incumbent special interests, whether they be unions, homeowners, administrative bureaucracies, or other constituencies. This creates additional barriers to reform. Indeed, to successfully instill a pro-growth policy environment may well require altering the policymaking process itself.

Given the difficulties of entrenched positions and vested interests, the most promising areas for reform will be those not already subject to high-profile, politically polarized debate or where one side realizes its ambitions cannot be achieved without embracing policies that have historically been the focus of its political opponents. Infrastructure regulatory policy may be a good example, given that the progressive ambition for a renewables revolution will inevitably run into the same barriers and environmental audits that free-market proponents have long bemoaned as smothering private-sector projects.

Other promising possibilities for new pro-growth coalitions will arise in areas where reform could bring the double dividend of improved efficiency and distributional wins for a key constituency. For example, reforming restrictive zoning laws could increase economic output by improving the efficiency of the allocation of housing, with people who are poor benefiting disproportionately from lower housing costs.

America’s growth slowdown remains a relatively recent problem and—given the ongoing headwinds against a high sustainable growth rate—will require a huge shift in policy to meaningfully offset. But the long-term benefits of achieving faster growth would be worth it. Economic growth should be a frontline priority that looms over all policy decisions.

Suggested Readings

Bourne, Ryan. “Government and the Cost of Living: Income‐Based vs. Cost‐Based Approaches to Alleviating Poverty.” Cato Institute Policy Analysis no. 847, September 4, 2018.

Cochrane, John. “Economic Growth.” Focusing the Presidential Debates Initiative, October 1, 2016.

Cowen, Tyler. Stubborn Attachments: A Vision for a Society of Free, Prosperous, and Responsible Individuals. San Francisco: Stripe Press, 2018.

Friedman, Benjamin. The Moral Consequences of Economic Growth. New York: Vintage Books, 2006.

Lindsey, Brink, ed. Reviving Economic Growth: Policy Proposals from 51 Leading Experts. Washington: Cato Institute, 2015.

———. “Why Growth Is Getting Harder.” Cato Institute Policy Analysis no. 737, October 18, 2013.

About the Author

This work is licensed under a Creative Commons Attribution-NonCommercial-ShareAlike 4.0 International License.