Did the Fed’s set its policy interest rate below the market-clearing or ‘natural’ interest rate level in the early-to-mid 2000s? Or did it simply lower its policy interest rate down to a depressed natural interest rate level during this time? The answers to these questions determine whether U.S. monetary policy was loose during the housing boom.

John Taylor believes the Fed pushed interest rates below their natural interest rate level. He views this departure from a neutral stance as a key contributor to the housing boom. Ben Bernanke and Larry Summers believe otherwise. They see the Fed simply doing its job back then by adjusting its policy rate down to a low natural interest rate level. Bernanke believes the natural interest rate level was low because of a saving glut while Summers holds that its was depressed because of secular stagnation. Either way, both individuals do not blame the Fed for any role the low interest rates played in fostering the housing boom. The Fed’s lowering of interest rates was simply an endogenous response.

George Selgin, Berrak Bahadir, and I recently published an article that lends support to John Taylor’s view of Fed policy during this time. It received some pushback from Scott Sumner who is sympathetic to both the saving glut and secular stagnation views. At the same time, Tony Yates provided a critique of John Taylor’s argument on the financial crisis that was heartily endorsed by Paul Krugman. So the debate over the Fed policy during this period continues.

What I want to do here is to step back from this debate and review what I see as the key economic developments that affected U.S. interest rates at this time. Then, given these considerations, I will jump back into the debate and ask whether Fed policy pushed interest rates in the same direction as that implied by these developments.

The key developments as I see them are threefold: a falling term premiums, a spate of large positive supply shocks, and the emergence of a monetary superpower. Let us consider each one in turn.

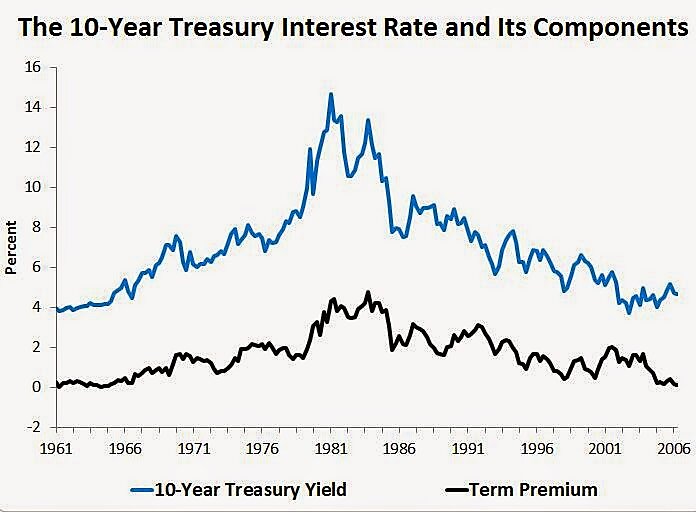

I. Falling Term Premiums on Long-Term Treasuries

The term premium is the extra compensations investors require for the risk of holding a long-term treasury bond versus a sequence of short-term treasury bills over the same period. The term premium had been declining since the early 1980s and therefore put downward pressure on long-term interest rates. This development can be seen in the figure below which is created using the Adrian, Crump, and Moench (2013) data. (For more on this data see here.)

The decline has been attributed to several factors. First, there was a decline in inflation volatility and an overall improvement in macroeconomic stability during this time that made investors less risk averse to holding long-term bonds. They therefore demanded less compensation. Second, regulatory and accounting changes for certain firms increased their demand for treasury securities relative to their supply. This further reduced the term premium. Third, globalization was taking off, but without a concurrent deepening of financial markets in many of the affected countries. That meant that global income was growing faster than the world’s ability to produce safe assets. Consequently, many developing countries started turning to the United States for safe assets. This further depressed the term premium and is the basis for Bernanke’s saving glut theory.

A close look at the above figure shows this term premium decline intensified in 2003, falling about 1.4 percentage points over the next two years. This happened right during the time the Fed pushed its policy rate to record-low levels. This, then, appears to support the endogenous view of the low policy rates argued by Bernanke and Summers.

However, this conclusion needs to be tempered. For the next two developments discussed below suggest that a sizable portion of the declining term premium at this time may have been an endogenous response to the Fed’s low interest rates policy during that time.

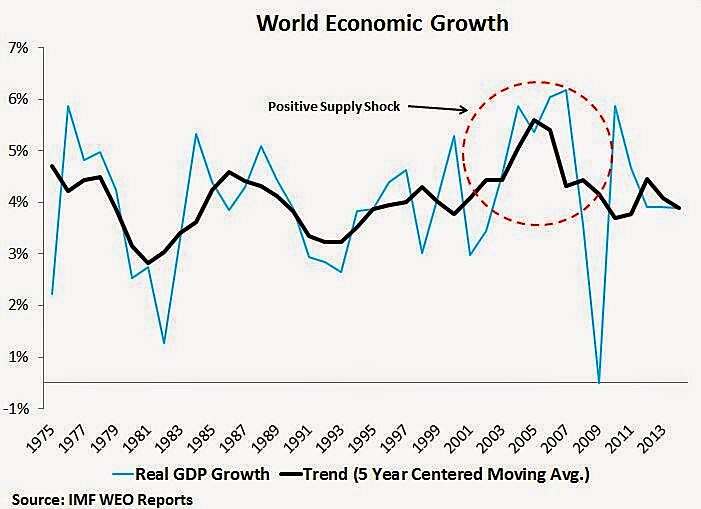

II. A Spate of Large Positive Supply Shocks

The second important development is that the global economy got buffeted with a series of large positive supply shocks from the opening up of Asia–especially China and India–and the rapid technology innovations that reached a crescendo in the early-to-mid 2000s. Global growth accelerated because of these developments as seen in the figure below:

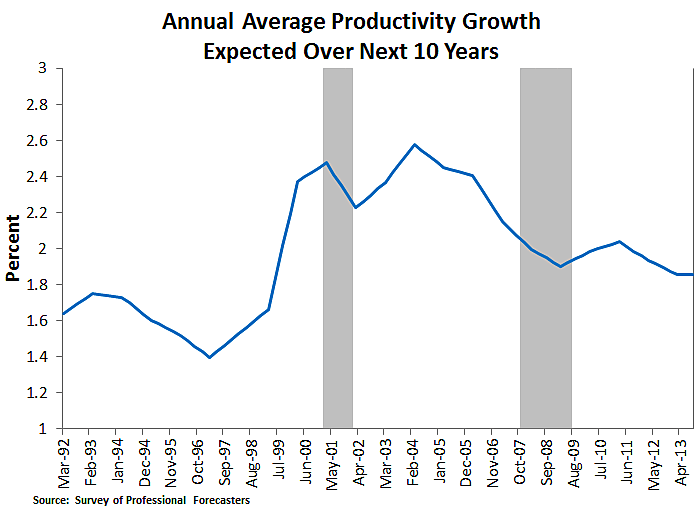

The opening up of Asia significantly increased the world’s labor supply while the technology gains increased productivity growth. The uptick in productivity growth, which peaked between 2002 and 2004, was widely discussed in the early 2000s and raised long-run expected productivity growth at the time. This can be seen in the figure below which shows a consensus forecast of annual average productivity growth over a ten year horizon:

Note that the rise in the labor force and productivity growth rates both raised the expected return to capital. The faster productivity growth also implied higher expected household incomes. These developments, in turn, should have lead to less saving and more borrowing by firms and households and put upward pressure on the natural interest rate. Interest rates, in short, should have been rising given these large positive supply shocks during this time.

III. Emergence of a Muscle-Flexing Monetary Superpower

The third development is that in the decade leading up to the financial crisis that the Fed became a monetary superpower that could flex its muscles. It controlled the world’s main reserve currency and many emerging markets were formally or informally pegged to dollar. Thus, its monetary policy got exported across much of the globe, a point acknowledged by Fed chair Janet Yellen. This meant that the other two monetary powers, the ECB and the Bank of Japan, were mindful of U.S. monetary policy lest their currencies became too expensive relative to the dollar and all the other currencies pegged to the dollar. As as result, the Fed’s monetary policy got exported to some degree to Japan and the Euro area as well. Chris Crowe and I provide formal evidence for this view here as does Colin Gray here.

Now let’s tie all these points together and see what it says about the Fed’s role in the housing boom. Let’s begin by noting that when the large positive supply shocks buffeted the global economy they created disinflationary pressures that bothered Fed officials. They did not like the falling inflation. So Fed officials responded by easing monetary policy. Recall, though, that the supply shocks were raising the return to capital and expected income growth and therefore putting upward pressure on the natural interest rate. The Fed, consequently, was pushing down its policy rate at the very time the natural interest rate was rising. Monetary policy was inadvertently being loosened.

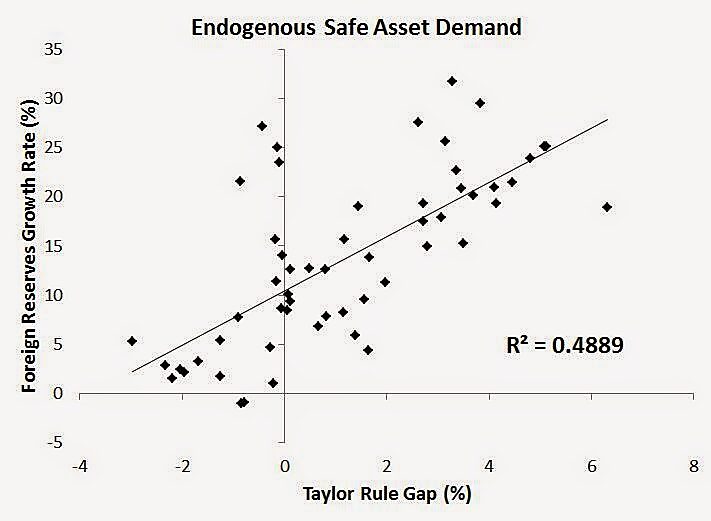

This error was compounded by the fact that the Fed was a monetary superpower. The Fed’s easing in the early-to-mid 2000s meant the dollar-pegging countries were forced to buy more dollars. These economies then used the dollars to buy up U.S. treasuries and GSE securities. This increased the demand for safe assets and ostensibly reinforced the push to transform risky private assets into AAA assets. To the extent the ECB and the Bank of Japan also responded to U.S. monetary policy, they too were acquiring foreign reserves and channeling credit back to the U.S. economy. Thus, the easier U.S. monetary policy became the greater the demand for safe assets and the greater the amount of recycled credit coming back to the U.S. economy. The 2003–2005 decline in the term premium, in other words, was to some extent an endogenous response to the easing of Fed policy during this time.

The figure below highlights this relationship for the period 1997–2006. It comes from my work with Chris Crowe and shows that almost 50% of the foreign reserve buildup was tied to deviations of the federal funds rate from the Taylor Rule. Colin Gray estimates several regression models on this relationship and finds that for every 1% point deviation of the federal funds rate below the Taylor Rule, foreign reserves grew by $11.5 billion. The Fed, therefore, was putting downward pressure on interest rates not only directly via the setting of its federal funds rate target, but also by raising the amount of credit channeled into the long-term U.S. securities.

Given these points, I think it is reasonable to conclude the Fed contributed to the housing boom. I hope they give Scott, Tony, and Paul something to think about.

Let me be clear about my views. Even though the Fed kept its policy rate below the natural rate for a good part of the housing boom period, the opposite happened after the crash due to the ZLB. This is a point Ramesh Ponnuru and I made in a recent National Review article. So unlike some observers who see the Fed as being eternally loose, I take a different view: the Fed was too loose during the boom and too tight during the bust.

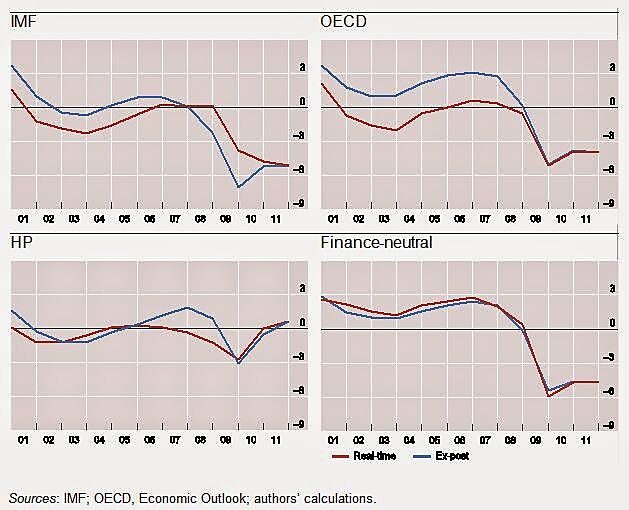

Update: There are multiple measures of the output gap that show the U.S. economy overheating during this time. Below is a figure from this article that compares the real-time and final measures of the U.S. output gap. Everyone shows ex-post an overheating economy during the housing boom:

[Cross posted from Macro and Other Market Musings]