Last Thursday, Mervyn King, the outgoing governor of the Bank of England, called for yet another round of recapitalization of the major UK banks. For some time, I have warned that higher bank capital requirements, when imposed in the middle of an economic slump, are wrong-headed because they put a squeeze on the money supply and stifle economic growth. So far, bank recapitalization efforts, such as Basel III, have resulted in financial repression – a credit crunch. It is little wonder we are having trouble waking up from the current economic nightmare.

So why would Mr. King want to saddle the UK banking system with another round of capital-requirement increases, particularly when the UK economy is teetering on the edge of a triple-dip recession? Is King simply unaware of the devastating unintended consequences this would create?

In reality, there is more to this story than meets the eye. To understand the motivation behind the UK’s capital obsession, we must begin with infamous Northern Rock affair. On August 9, 2007, the European money markets froze up after BNP Paribas announced that it was suspending withdrawals on two of its funds that were heavily invested in the US subprime credit market. Northern Rock, a profitable and solvent bank, relied on these wholesale money markets for liquidity. Unable to secure the short-term funding it needed, Northern Rock turned to the Bank of England for a relatively modest emergency infusion of liquidity (3 billion GBP).

This lending of last resort might have worked, had a leak inside the Bank of England not tipped off the BBC to the story on Thursday, September 13, 2007. The next morning, a bank run ensued, and by Monday morning, Prime Minister Gordon Brown had stepped in to guarantee all of Northern Rock’s deposits.

The damage, however, was already done. The bank run had transformed Northern Rock from a solvent (if illiquid) bank to a bankrupt entity. By the end of 2007, over 25 billion GBP of British taxpayers’ money had been injected into Northern Rock. The company’s stock had crashed, and a number of investors began to announce takeover offers for the failing bank. But, this was not to be – the UK Treasury announced early on that it would have the final say on any proposed sale of Northern Rock. Chancellor of the Exchequer Allistair Darling then proceeded to bungle the sale, and by February 7, 2008, all but one bidder had pulled out. Ten days later, Darling announced that Northern Rock would be nationalized.

Looking to save face in the aftermath of the scandal, Gordon Brown – along with King, Darling and their fellow members of the political chattering classes in the UK – turned their crosshairs on the banks, touting “recapitalization” as the only way to make banks “safer” and prevent future bailouts.

In the prologue to Brown’s book, Beyond the Crash, he glorifies the moment when he underlined twice “Recapitalize NOW.” Indeed, Mr. Brown writes, “I wrote it on a piece of paper, in the thick black felt-tip pens I’ve used since a childhood sporting accident affected my eyesight. I underlined it twice.”

I suspect that moment occurred right around the time his successor-to-be, David Cameron, began taking aim at Brown over the Northern Rock affair.

Clearly, Mr. Brown did not take kindly to being “forced” to use taxpayer money to prop up the British banking system. But, rather than directing his ire at Mervyn King and the leak at the Bank of England that set off the Northern Rock bank run, Brown opted for the more politically expedient move – the tried and true practice of bank-bashing.

It turns out that Mr. Brown attracted many like-minded souls, including the central bankers who endorsed Basel III, which mandates higher capital-asset ratios for banks. In response to Basel III (and Basel III, plus), banks have shrunk their loan books and dramatically increased their cash and government securities positions (both of these “risk free” assets are not covered by the capital requirements imposed by Basel III and related capital mandates).

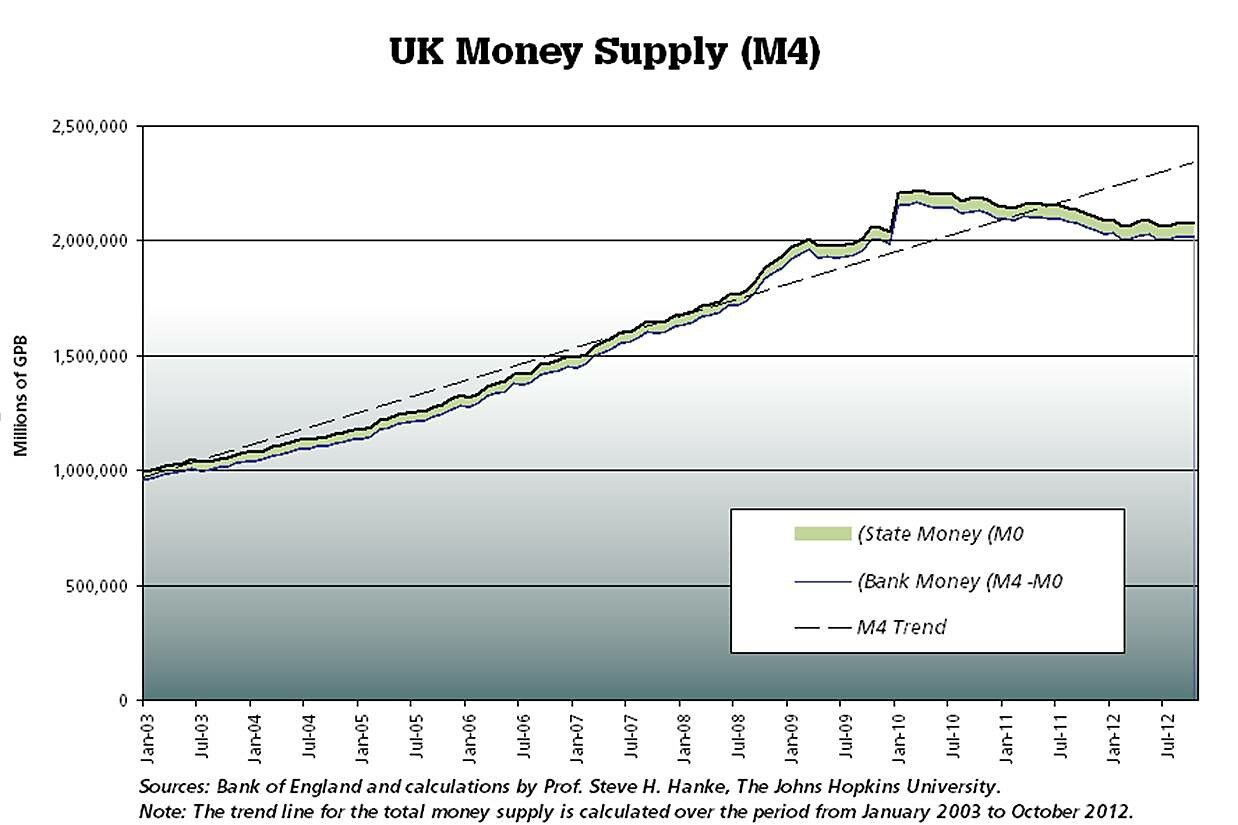

In England, this government-imposed deleveraging has been particularly disastrous. As the accompanying chart shows, the UK’s money supply has taken a pounding since 2007, with the money supply currently registering a deficiency of 13%.

How could this be? After all, hasn’t the Bank of England employed a loose monetary policy scheme under King’s leadership? Well, state money – the component of the money supply produced by the Bank of England – has grown by 22.3% since the Bank of England began its quantitative easing program (QE) in March 2009, yet the total money supply, broadly measured, has been shrinking since January 2011.

The source of England’s money-supply woes is the all-important bank money component of the total money supply. Bank money, which is produced by the private banking system, makes up the vast majority – a whopping 97% – of the UK’s total money supply. It is bank money that would take a further hit if King’s proposed round of bank recapitalization were to be enacted.

As the accompanying chart shows, the rates of growth for bank money and the total money supply have plummeted since the British Financial Services Authority announced its plan to raise capital adequacy ratios for UK Banks.

In fact, despite a steady, sizable expansion in state money, the total money supply in the UK is now shrinking, driven by a government-imposed contraction in bank money. So, contrary to popular opinion, monetary policy in the UK has been ultra-tight, thanks to the UK’s capital obsession.

Despite wrong-headed claims to the contrary by King, raising capital requirements on Britain’s banks will not turn around the country’s struggling economy – any more than it will un-bungle the Northern Rock affair. Indeed, this latest round of bank-bashing only serves to distract from what really matters – money.