Among the many issues the COVID-19 pandemic has amplified in trade policy circles, “supply chain fragility” and “resilience” seem to be major talking points. Calls for reshoring production are not limited to the United States, but U.S. policy makers have been especially vocal on the issue. Recently, U.S. Trade Representative Robert Lighthizer condemned U.S. supply chains as representing a “lemming-like” desire for efficiency that has left them exposed to unacceptable levels of risk, and he has called for the country to “maintain and grow its manufacturing base” in response to recent events. This raises two questions: is the United States as vulnerable as he claims to supply chain disruptions, and is reshoring the solution? The answer to both of these questions is an emphatic no.

Let’s take a look at some data to better understand where the U.S. sits in relation to the rest of the world on measures of dependence on trade. At the most basic level, a common way to measure the centrality of trade to a country’s wealth is to look at trade as a percentage of gross domestic product (GDP). Using this metric, the United States is far less reliant on cross border exchange than most other countries. In 2018, trade accounted for 27.5 percent of U.S. GDP. That may seem like a large number, but in comparison, China’s trade to GDP ratio sits at 38.2 percent, and the world average is a whopping 59.5 percent. In fact, of the 170 countries and economies for which the World Bank has this data, the United States ranks 3rd from last (only Cuba and Sudan rank lower, albeit for different reasons). Essentially, the U.S. is not very dependent on trade for domestic output. This makes sense, as larger markets tend to be less reliant on other markets to satisfy domestic demand. In fact, as Figures 1 and 2 show, the United States scores low among its peers in terms of how much domestic demand is satisfied by imports.

However, trade as a percentage of GDP is a blunt measure of reliance. To get a full sense of supply chain interdependence in a globalized world – where the average automobile contains 30 thousand parts and manufacturing a simple widget for an automobile entails crossing several borders and continents, or the classic case of the iPhone, where inputs come from seven different countries – requires more nuanced measures.

For example, one could look at the percentage of intermediate inputs from other countries in the manufacturing sector, or as economists Richard Baldwin and Rebecca Freeman suggest, look at both the direct and indirect inputs from external sources on manufacturing. Baldwin and Freeman find that there is a high level of interdependence in global manufacturing supply chains, and that Chinese production plays a large and growing role in global manufacturing, with “about 9% of US manufacturing output comprised [of] inputs made in China” in 2015. At the same time, there are also important regional clusters of manufacturing activity, such as Factory Asia, Factory North America, and Factory Europe. Thus, while we all make things together, we also make a lot more with our closest neighbors than distant trading partners.

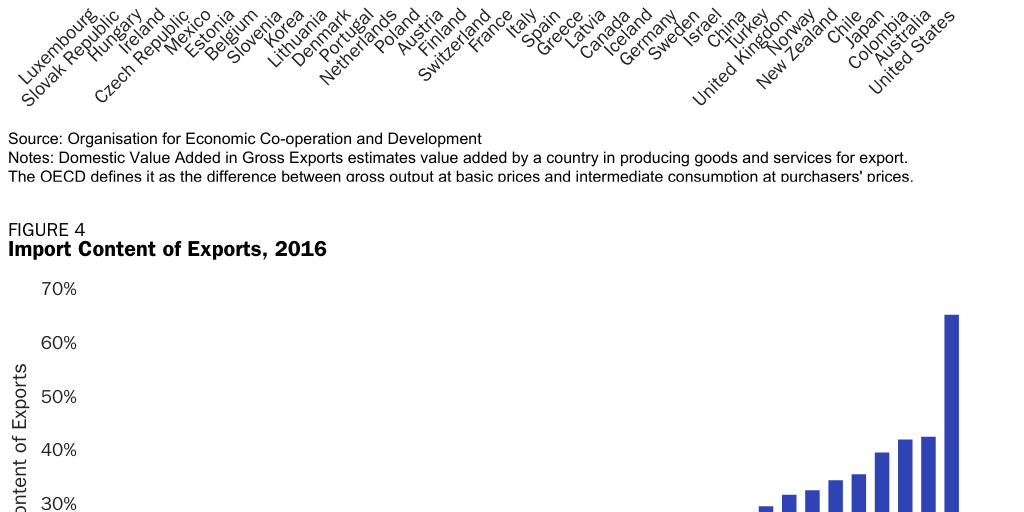

Data on value added tells a similar story. The World Trade Organization reports that foreign value added, that is the percentage of foreign inputs in U.S. exports, amounted to a mere 9.5% of total gross exports in 2015. Data from the Organisation for Economic Co-operation and Development puts this in broader context. Among the major economies, the United States has ranked near or at the top in domestic value added in exports for the last decade, and it is the least reliant on imported content for its exports. Figures 3 and 4 provide a snapshot of both measures for the most recent year that data is available. Therefore, even as China has grown as a manufacturing hub, the United States has not become as dependent on China (or any other country for that matter) as many pundits may claim.

In fact, even the shortages of personal protective equipment and pharmaceuticals early in the U.S. pandemic response cannot be blamed on supply chain dependence. A recent study from Clark Packard and Bill Watson from the R Street Institute shows that the United States is not overly reliant on China for finished pharmaceuticals and active pharmaceutical ingredients. And as Bloomberg’s Shawn Donnan reports, the “I told you so moment” for economic nationalists prompted by shortages does not reveal what they think it does:

The pandemic, they argue, has exposed the false promises and underlying evil realities of international alliances and supply chains. We live in a world where every nation is for itself, they crow. The truth is somewhat more complex and less politically potent. If there is a policy failure to learn from, it’s that governments have wasted years — and not just the early months of 2020 — in preparing for a pandemic that many predicted would arrive someday. The U.S. federal government’s inadequate stockpiles of N95 respirators and ventilators is not a failure of corporate supply chains or globalization. It’s a failure of planning for an emergency, which is the highest responsibility of governments.

This does not mean that supply chains are not vulnerable, as there is plenty of evidence that businesses have had to scramble amidst the increased uncertainty the pandemic has brought. This has led some companies, as Alan Beattie from the Financial Times noted, to rethink “just in time” production to “just in case” instead. This means building in contingency plans for situations like what we are facing now. The response should therefore not be turning inwards, but rather greater diversification and planning for disruptions—all things that companies can do on their own without government intervention. It’s also worth mentioning that even if we were able to move some production home, it would do nothing to alleviate the challenges posed by prolonged lockdowns on supply disruptions.

This has not stopped the calls for reshoring production, with some scholars going so far as to claim that it will boost domestic productivity. But the issue with this argument, as political scientist Daniel W. Drezner rightly points out, is that “[t]he problem isn’t that the United States doesn’t have a vibrant manufacturing sector. The problem is that sector does not generate the job numbers that used to be associated with manufacturing,” and furthermore, “[t]he U.S. manufacturing sector needs fewer workers because it is more productive.” Our colleague, Dan Ikenson, has repeatedly pointed out this myth of U.S. manufacturing decline.

In fact, last year, manufacturing output in the United States reached an all-time high. The United States manufacturing sector has also proven itself an attractive destination for investment. In 2018, U.S. FDI stock in that sector rose by 10% to $1.77 trillion. Furthermore, while Lighthizer and his ideological supporters may hark back to some golden age of U.S. manufacturing, Ryan Bourne aptly explains that this is an imagined reality:

In fact, even in the supposed golden era of “stable employment” from the end of the second world war to 1980, the rate of job destruction in manufacturing was 6 percent per year, not massively dissimilar to the overall rate of job destruction today, and certainly higher than the current manufacturing employment destruction rate.

Reshoring production is therefore an ill-fitting policy prescription to our current challenges. Instead of pushing for policies that would further disrupt supply chains, the United States should prioritize an economic environment conducive to trade and investment. Businesses know their supply chains better than government ever can, and allowing them the space to learn from the current pandemic and respond in kind is a better approach than trying to force sourcing decisions on them. Protectionism is being offered as a cure for our misdiagnosed overreliance on other countries, and the implications of enacting policies that isolate the United States from the world will likely undercut our competitiveness at a time when we need as many options for kickstarting growth as possible. The administration has already bungled its pandemic response. Let’s hope they don’t follow suit on the recovery.