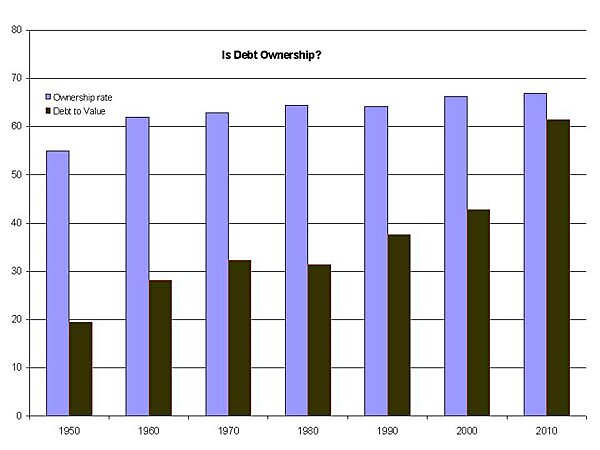

One of the rationales commonly given for massively subsidizing our mortgage market is that without such homeownership would be out of reach for many households. Such a rationale implies that more debt should be associated with more homeownership. (Let’s set aside the obvious, how are you actually an owner without any equity?)

But is that the case. The chart below compares the homeownership rate with the average debt-to-value ratio of U.S. households. (Data on debt-to-value is from the Fed’s Flow of Funds and homeownership is from the Census Bureau).

By 1960, the homeownership rate was already over 60%, yet debt-to-value was less than 30%, half of the current value. Even in 1990, when homeownership reached over 64%, debt-to-value was still under 40%. From 1990 until today, the percentage of mortgage debt to value increased by over 50%, all to gain a 2 percentage point increase in homeownership. So it seems the story of the last 20 years has been a massive increase in home debt with very little increase in actual homeownership rates. The converse should also hold: reducing homeowner leverage should have little, if any, impact on homeownership rates.