Tax evasion limits fiscal capacity, distorts resource allocation, and can result in reliance on inefficient tax instruments. A recent literature has shifted emphasis from tax enforcement through auditing toward verifying taxpayer reports against other sources, such as employer salary reports or trading partner reports. Third-party information is central to modern tax collection in developed countries, and the global revolution in information technology has made third-party verification easier. Improvements in third-party information appear capable of transforming tax collection, particularly in developing economies.

In our work, we show a fundamental limit to the effectiveness of third-party information in improving revenue collection: the ability of taxpayers to make offsetting adjustments on less verifiable margins of the tax return.

We demonstrate that this behavior can be expected under conditions common in developing countries, where capacity on other dimensions of information and enforcement are weak. We then provide evidence of such adjustments in a natural experiment in which the tax authority notified firms about discrepancies between their declared revenues and revenue reports from third-party sources. Firms increase reported revenues in response to the notifications but offset almost the entire adjustment with increases in reported costs, resulting in only minor increases in total tax collection.

We analyze responses to third-party reporting in the context of the corporate income tax in Ecuador. In 2011 and 2012 the tax authority notified a sample of almost 8,000 firms about discrepancies on previously filed returns between their self-reported revenue and information from third-party sources. Firms were asked to submit an amended tax return to address the discrepancy. These discrepancy notifications are representative of how third-party reporting is generally used in practice.

We first document widespread misreporting of both revenues and costs relative to third-party information. Firms' self-reported revenues are lower than third-party reports in 24 percent of firm filings, suggesting substantial scope for improvements in revenue collection. We observe little bunching at the third-party amount, consistent with limited third-party reporting by the tax authorities prior to the notifications. Consistent with our conceptual framework, in which it is optimal for some firms to underreport scale in order to try to "fly under the radar," we also find that 23 percent of firm filings and 5 percent of those with positive tax liability report costs that are below third-party reported costs. Since thirdparty reporting is incomplete, these estimates provide lower bounds on cost underreporting.

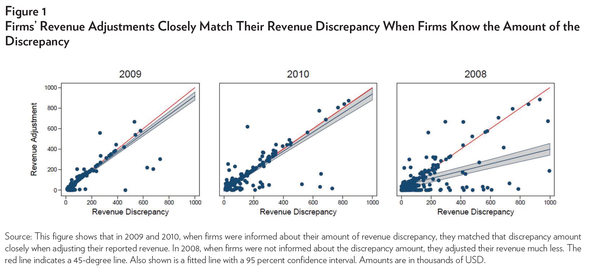

We next examine the effect of the discrepancy notifications. Consistent with the idea that lack of credible enforcement capacity can limit the effect of information reporting, we find that a substantial share of firms simply fail to file a requested amendment. Among amending firms, the discrepancy notifications induce large increases in reported revenues. When firms are given a specific third-party revenue amount by the tax authority, 35 percent of firms that file an amendment revise reported revenues to match the indicated amount. Firms that adjust reported revenues do so by 93 cents on average for every dollar of notified revenue discrepancy. When firms are told a discrepancy exists but are not provided with a specific amount, revenue adjustments are substantially lower (see Figure 1). This provides strong evidence that firms are misreporting both before and after the notifications.

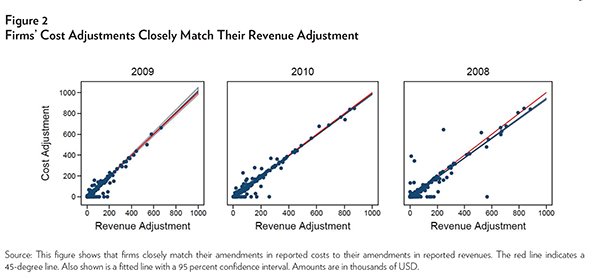

The effects of these increases in reported revenues on tax payments, however, are limited because, as shown in Figure 2, for every dollar of revenue adjustment, firms increase reported costs by 96 cents. Changes in reported profits were therefore minor, implying that third-party reporting had little effect on profit underreporting. Cost offsets are similar regardless of whether firms know the exact revenue discrepancy, and we see no correlation between pre-notification reported profit rates and implied profit rates on the amended portion of the return. Taken together, these findings indicate that firms are deliberately targeting their reported cost adjustments to their revenue adjustments. We also see evidence that firms choose cost adjustments on line items that are difficult for the tax authority to verify (e.g., other administrative costs). As a result, tax collection is an order of magnitude less than it would have been had firms only adjusted revenues.

Our paper contributes to the literature along several dimensions. First, we demonstrate important limits to tax enforcement through third-party reporting. Thirdparty reporting has primarily been studied in developed countries, in which information reporting is relatively complete and the capacity of the tax authority is high. A natural question is whether this form of tax enforcement can be equally effective in developing countries. Our results show that this method of tax enforcement— on its own—may have limited efficacy in low-capacity settings: there are likely important complementarities between tax enforcement through third-party reporting and investments in "traditional" auditing and enforcement capabilities.

Second, our findings demonstrate that optimal tax policy may differ across developed and developing countries as a result of differences in information and enforcement constraints. Specifically, governments should set the tax base taking into account the degree of third-party information on the base as a whole.

Third, we are able to study the microeconomics of firm tax misreporting using administrative data. One key novel finding is that some firms underreport their true costs, a result that is consistent with our conceptual framework but runs counter to a natural intuition that evading firms would always inflate their reported costs. Underreporting of costs also has important implications: if firms do not have incentives to fully declare costs, the self-enforcement mechanism in the value added tax (VAT) can be undermined.

Fourth, our results highlight the importance of other aspects of the enforcement environment in determining the effectiveness of third-party reporting. When thirdparty reporting is highly incomplete and enforcement capacity is weak, as is the case in many developing economies, the effect of third-party reporting on revenue can be dramatically limited as taxpayers respond by adjusting reports on less verifiable margins of the tax return. From a policy perspective, our results indicate that third-party reporting alone is unlikely to improve fiscal capacity in low-income economies. This does not necessarily mean that countries should not invest in information technologies that support third-party reporting; third-party reporting could become useful as the scope of transactions covered by third-party reporting expands and the ability to monitor and enforce compliance on non-third-party reported margins increases.

NOTE

This research brief is based on "Dodging the Taxman: Firm Misreporting and Limits to Tax Enforcement," Paul Carrillo, Dina Pomeranz, and Monica Singhal, Harvard Business School Working Paper no. 15-026, October 2014, http://www.hbs.edu/ faculty/Pages/item.aspx?num=48169.

About the Authors

Paul Carrillo, George Washington University; Dina Pomeranz, Harvard University and National Bureau of Economic Research; and Monica Singhal, Harvard University and National Bureau of Economic Research