Three years ago, I looked into purchasing a modestly priced condo as an investment property in my hometown of Winston-Salem, NC. I found what seemed like the perfect choice: a condo tucked into a quiet and safe neighborhood. The price was right, too, at only $69,000. With our own house nearly paid off, excellent credit, and a nice-sized savings account, my wife and I thought a $69,000 mortgage would be easy to finance, especially with 20 percent down.

Then I called our friend who was a mortgage broker for assistance. “No one is going to write a loan for that small an amount,” she told us. “Our company has been told not to touch any loan less than $100,000.”

“But there is a solution,” she continued. “You have substantial equity in your home, and if you roll these two properties together into a new mortgage, it will be worth it for a bank to process it, and you can buy the condo.” The condo could be purchased, in other words, by relatively well-off people who either had cash or could wrap the condo into a larger loan. But for people living on a modest income without cash or home equity, the condo would be out of reach even if they could easily afford a $600 mortgage payment.

As I later discovered, the ramifications of this credit squeeze have rippled across entire neighborhoods, diminishing hopes for those at the bottom of the economic ladder wishing to live the American Dream of one day owning a home.

Small-Dollar Homes

For those of us who live in cities where $300,000 will barely buy a fixer-upper, the following fact may be surprising: there are millions of owner-occupied homes in the United States valued at less than $100,000. Concentrated in rural areas and in the poorest areas of many cities, these sub-$100,000 properties—either single-family homes or condos—are known as “small-dollar homes.” Renters seeking a path to home ownership once used these properties, along with sweat equity in the form of home improvements, to build wealth that could be passed down to the next generation. But today these homes are out of reach for many people, even though they could easily afford the mortgage payment.

Over the last decade, originations for mortgage loans between $10,000 and $70,000 dropped by 38 percent, and loans between $70,000 and $150,000 fell by 26 percent. The other end of the market is far healthier: originations for loans exceeding $150,000 rose by 65 percent over the same time frame.

As a result, in 2019, 77 percent of homes costing less than $100,000 were purchased with cash, and just 23 percent had a mortgage. Ironically then, the most likely buyer of a small-dollar home is not a hard-working individual with moderate income. Rather, it’s someone with thousands of dollars in the bank. Not only that, it’s getting harder to get home improvement loans for under $50,000, which also affects those with lower-valued homes. The road to the American dream appears to be blocked for those at the lower end of the economic ladder, and at first glance it’s not clear why.

The trend away from banks offering small-dollar mortgages might seem logical. There isn’t as much money in issuing a small-dollar mortgage as in a larger one, just as any real estate agent would rather earn a commission on a million-dollar home than a $100,000 one. But markets tend to fill voids, and when the highly lucrative market segments become saturated, it’s only natural that some suppliers decide that they can do better by selling lower-profit items at higher volume. Yet that’s not happening in the small-mortgage market. And despite home appreciation over the years, by 2019 one in five owner-occupied traditional homes and condos was still valued under $100,000 across the United States.

Dodd–Frank and Small-Dollar Homes

There is another, even more worrisome trend. Across the United States for many years, property values in concentrated areas of these small-dollar homes have been slowly sinking, leading to the erosion of millions of dollars in hard-earned home equity.

Certainly, concentrated poverty has multidimensional causes. In a forthcoming article in Public Choice (available online), Zachary Blizard and I investigate to what extent falling housing prices in areas of concentrated poverty are directly tied to the collapse of mortgage credit for small-dollar homes.

Let’s investigate the intuition behind why a shrinking of mortgage credit could be tied to falling property values. Imagine a local auction where prospective buyers are told that all purchases must be made in cash. Compare that to another auction where all forms of payment are accepted, including credit cards, checks, and cash. Common sense would tell us that we should expect the first auction to have fewer buyers and thus lower bids overall. In other words, restriction of the type of payment leads to a drop in demand and lower prices. Our hypothesis is that the same thing is happening with small-dollar homes, where the seller previously faced potential buyers with multiple forms of financing available. As I ruefully found out with my purchase of the condo, that no longer applies today: cash usually is king, limiting the potential pool of buyers to those who have lots of extra cash or home equity.

Indeed, there is widespread evidence that after the Great Recession of 2008–2010, the subsequent 2010 banking regulations have led to a drying up of these smaller home loans, both for mortgages and home improvement. The federal government imposed thousands of pages of new rules that resulted in banking mergers or failures because smaller banks could no longer afford the cost of their increased overhead.

Winston-Salem’s Small-Dollar Homes

Our research uses Winston-Salem as a case study to further investigate these trends. We test the following hypothesis: Did the fall in mortgage credit from increased banking regulations after the passage of the Dodd–Frank Act correspond to falling property values in a very low-income section of the city?

Located in Forsyth County, Winston-Salem is an ideal city to measure these effects because it is divided by US-52, which runs north and south. On the east side, known as East Winston, 77 percent of the homes had a tax-assessed value of under $100,000 in 2022. East Winston has primarily Black and Hispanic families. The west side of US-52 is far wealthier, and the majority of the families are White, with only 27 percent of homes having a tax-assessed value of $100,000 or less. With a population of 250,000, Winston-Salem serves as an excellent case study because it mirrors many other mid-sized cities that have racially and demographically diverse populations, as well as a broad variance in family income.

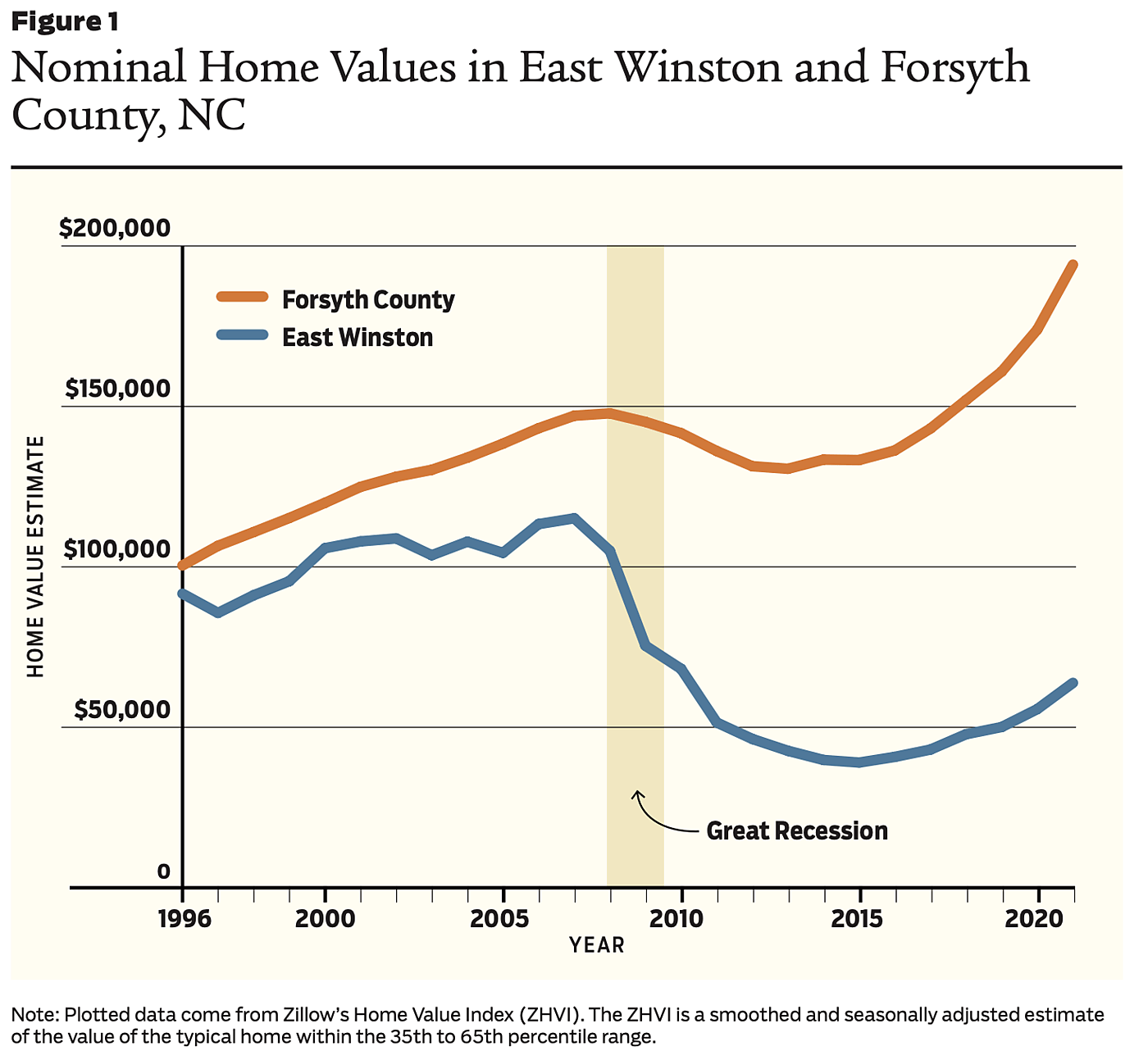

Figure 1 depicts the overall trends in home values for East Winston and all of Forsyth County. Property values across the county declined after 2010, but for the low-income East Winston that has primarily small-dollar homes, property values fell faster and have been very slow to recover relative to the county. In contrast, the rest of the county experienced slighter property declines during the Great Recession and a stronger rebound starting in 2016. Using regression analysis, we investigated the effects of several factors on property value, including the number of small-dollar loans, square footage of the dwelling, income, poverty rates, population, and the time frame since the passage of the 2010 Dodd–Frank banking regulation. Note that for all of our regression analyses, nominal rather than real property values were used, which is common in the literature as well as for official government reporting of housing prices.

Our regression results, controlling for the above variables, reveal a stunning finding that aligns with our original hypothesis: since 2010, nominal property values in low-income East Winston have dropped by over 40 percent relative to the rest of the county, driven by a measured drop in small-dollar loans as well as a wider constriction of economic activity. This finding indicates that hundreds of millions of dollars of property value has vanished from homeowners living in East Winston, in sharp contrast to the rest of the county. These findings are robust and statistically significant, with a greater than 99 percent statistical confidence.

A previous 2021 study with my colleagues Sabiha Zainulbhai, Zachary Blizard, and Yuliya Panfil showed that at the current rate of home appreciation, it will take 30 years for home values in East Winston to return to their pre-financial crisis values, in real terms. This latest research thus raises serious questions about the unintended consequences of Dodd–Frank banking regulation in hundreds of similar U.S. cities that have similarly segmented populations.

It also brings us to the looming question: just how did federal banking regulations change the incentives for lenders across the country after 2010, such that even relatively well-off individuals have problems getting a mortgage under $100,000? A better understanding might one day reverse the policies that have led to collapsing property values in our nation’s poorest neighborhoods.

Dodd–Frank’s Unintended Consequences

The beginning of this domino effect of unintended consequences began with the passage of the Dodd–Frank Wall Street Reform and Consumer Protection Act of 2010. The legislation produced thousands of pages of new regulations that were meant to prevent the nation’s largest banks from taking excessive risks in their lending practices. The act was written in response to the sudden collapse of many banks during the Great Recession and the enormous federal bailouts that followed, outraging many taxpayers. Meant to discipline the larger banks with stricter guidelines on how to operate that ostensibly made banks more resilient, Dodd–Frank treated all lending institutions in the system as if they were equally culpable. However, the vast majority of the smaller banks neither needed nor wanted bank bailouts during the Great Recession because they had responsible lending practices.

Dodd–Frank made it more expensive to be in the banking business by raising financial institutions’ costs while clamping down on their revenue. This dealt a harsh blow to small mortgages because they were low-profit products to begin with.

Overhead costs / The mortgages’ fixed costs went up in two ways. First, Dodd–Frank imposed more overhead costs on each specific loan. An extensive and intensive income-verification process was now a requirement, adding to the expense of processing a loan. This made smaller loans even less profitable relative to larger loans because the verification process ate up more of the bank’s profit. In addition, lenders were forced to provide special training to all loan officers at their branches, following specific Dodd–Frank rules, further squeezing overall profits.

Community banks were hit particularly hard by these rising fixed costs because they issued a larger share of small-dollar mortgages and had less financial capital to absorb these blows. A 2020 Federal Deposit Insurance Corporation community bank study indicates that the increased regulatory burden from Dodd–Frank was an important factor in the record number of community bank closures. Lawmakers and regulators did not consider that smaller community banks often had a comparative advantage from personally knowing their customers over many years, making the overhauled income verification processes less useful. The legislation and resulting rules treated all banks with a “one size fits all” mentality. Moreover, these community banks were less likely to sell and package these loans to secondary lenders, making them more incentivized to pay attention to riskier loans. The regulatory changes were imposed without regard to the social capital and local knowledge possessed by community banks.

The rise in overhead costs from meeting new regulatory changes also accelerated the trend toward consolidation in the banking industry. Between 2006 and 2021, the number of commercial banks fell by 43 percent, from 7,402 to 4,236, while the share of total banking assets held by small banks (defined as having less than $10 billion in assets) fell from 27.5 percent in 2000 to 18.0 percent in 2014. The small community banks that were most likely to issue small mortgages and smaller home equity lines are finding it difficult, if not impossible, to be profitable.

For example, in September 2012, Shelter Financial Bank, a $200 million community bank in Columbia, MO, was closed by its owners. Complying with Dodd–Frank was adding $1 million per year to the bank’s expenses. “It was going to cost more than what we got out of the bank,” one bank official explained.

Many Black-owned banks—known for their engagement in minority communities—went out of business in the following decade. There were over 40 Black-owned banks prior to the Great Recession but only 21 by 2021. Small banks across the country reported not only more difficulty in issuing small-dollar mortgages, but also greater difficulty in serving the business community with small loans.

Capping banks’ origination revenue / Besides raising overhead costs across the banking system, Dodd–Frank’s new rules clamped down on the revenue that banks could earn for originating loans. Ostensibly, Dodd–Frank sought to address the hidden closing costs and other fees that often caught consumers by surprise in the run-up to the financial crisis. The Qualified Mortgage Rule, implemented by the Consumer Financial Protection Bureau (CFPB), capped the fees and points that lenders can charge for processing a loan on a sliding scale based on the size of a loan. The caps were meant to prevent “exploitative behavior” by banks charging “unfair” or “greedy” prices for executing loans. However, these price caps created problems that are familiar to anyone who has taken a freshman economics class: they caused an inevitable shortage of mortgage credit.

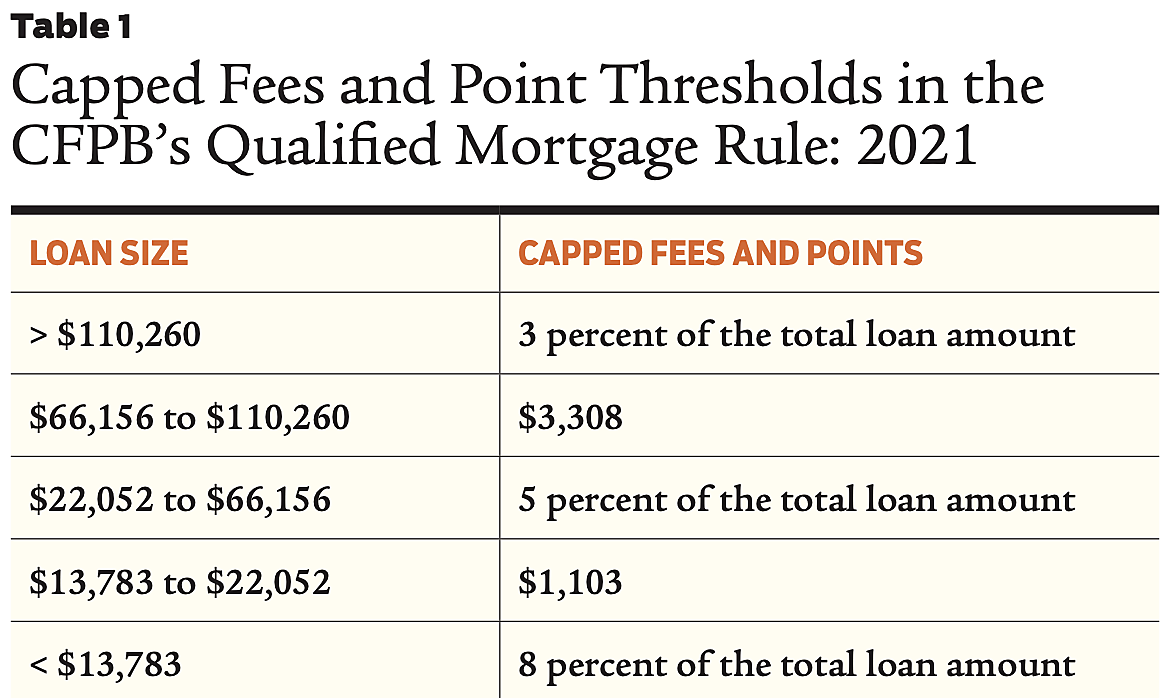

Table 1 lists the maximum amount banks could earn in 2021 from mortgages at different levels. The dollar values associated with these various mortgage levels have been regularly adjusted upward for inflation since 2008. However, there is no adjustment for the bank’s internal operating structure, risk of the client, geographic setting, local price index, or size of the bank. Although perhaps not readily apparent, the smaller the loan, the less profit a bank can make, creating an additional disincentive for banks to originate small loans—even as the intent is to protect buyers from excessive fees. As Table 1 shows, the capped fees follow a schedule of varying percentages and fixed amounts that make little sense to the ordinary consumer.

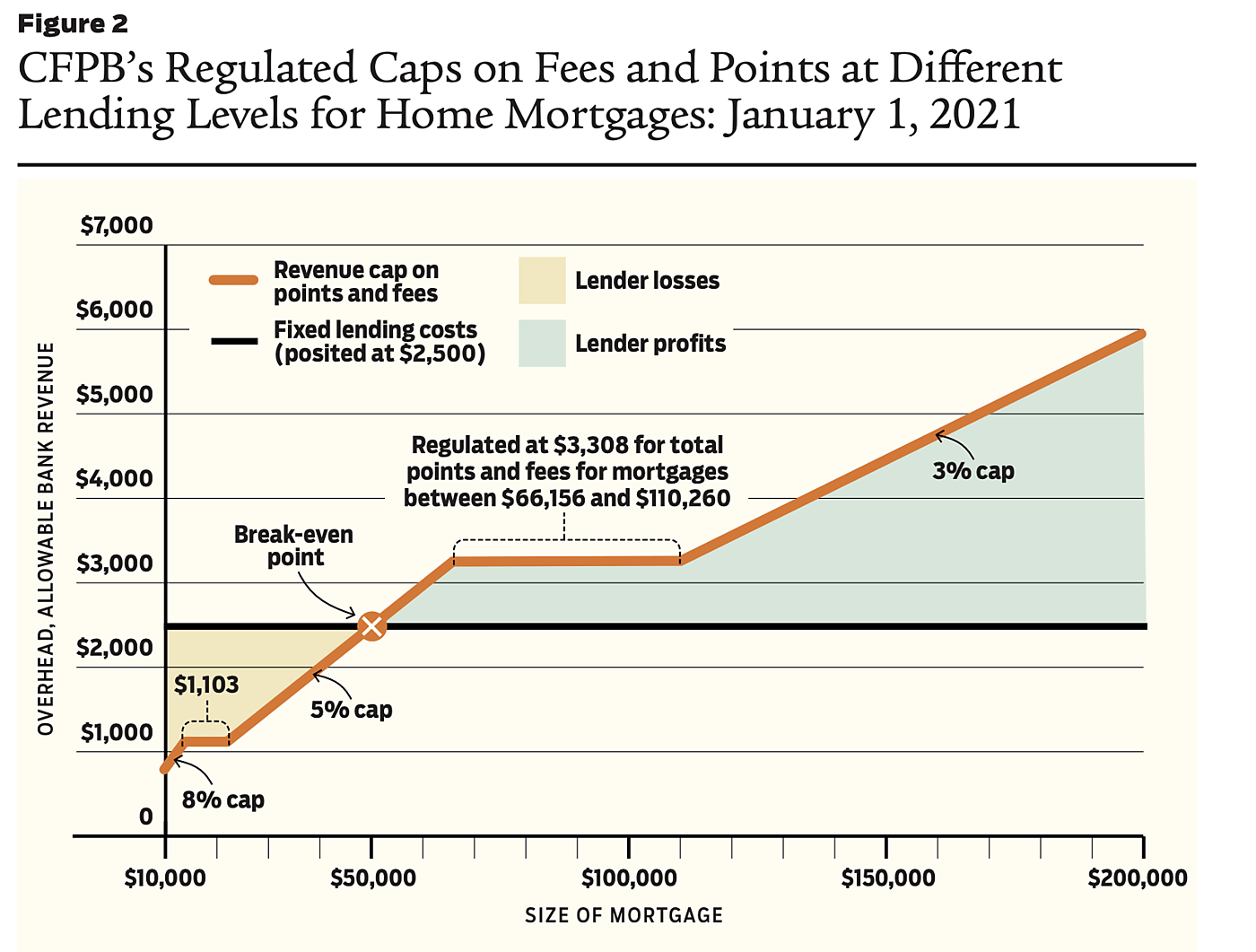

Figure 2 maps out Table 1 using continuous data and illustrates the quirkiness of the CFPB’s allowances, with their various slopes, flat spots, and kinks. This unevenness puts even more stress on a bank’s operating profits. The horizontal line at $2,500 represents the bank’s internal overhead costs to process a loan, which are fixed regardless of the size of the loan. The $2,500 in overhead costs is hypothetical but is a reasonable estimate for small community banks. Combining both lines reveals the disincentives caused by the CFPB’s arbitrary caps on lending. Note point X, where the capped revenue line meets the overhead cost line. The area to the left has revenues that fall beneath the horizonal overhead cost line and represents losses for the bank.

In a free market, the bank would raise closing costs to at least cover the overhead costs of processing a loan. Smaller loans would have relatively higher closing costs, just as convenience stores charge higher prices than Costco for a can of Coke. If the law were to forbid convenience stores from charging a higher unit price for Coke than Costco’s unit price, we would soon see the vanishing of all Cokes from convenience store shelves.

That is exactly what has happened in the small mortgage market. In this illustration, after Dodd–Frank, a profit-maximizing bank will steer clear of these loans, which are shown in this example as below $50,000. They may perform a relatively small number to promote community goodwill, but they are not incentivized to produce more. Loans up to approximately $110,000, where the bank is regulated to make no more than $3,308, will also be avoided because the profit margin is relatively small. It is not until the bank passes the $110,000 mark in this exercise that the opportunity for substantive bank profits begins.

Dodd–Frank’s effect is even easier to interpret on any future regulations on bank lending that raise overhead costs. In Figure 2, the overhead line would shift upward, which naturally pushes X to the right and establishes a new intersection that has higher mortgage sizes. Thus, we can readily see that ever-higher overhead costs result in even fewer loans at the lower end of the spectrum as they become more unprofitable.

Ironically, Wall Street banks have managed to grow stronger despite the regulations because they were far more equipped to deal with a rise in fixed costs and most have escaped the lower caps by not issuing small-dollar mortgages. Jamie Dimon, CEO of the nation’s largest bank, JP Morgan Chase, even admitted that though Dodd–Frank would be expensive to comply with, it would increase his bank’s market share because the barriers to entry for the mortgage market would be pushed higher. Other large players in the financial industry used bank lobbyists to shape the regulatory changes associated with Dodd–Frank.

There is also evidence that, along with the squeezing of small-dollar mortgage credit, existing homeowners with inexpensive homes had a far harder time getting loans for home improvement. Thus, by uniformly increasing overhead costs across the industry, Dodd–Frank penalized or eliminated many community lenders who had the most local knowledge and were most likely to issue small mortgages, business loans, and home improvement loans. Not surprisingly, the legislation’s effects have hit lower-income communities the hardest—a product of the law of unintended consequences.

Conclusion

The American dream has long been predicated on the idea of upward economic mobility and opportunity, no matter where one starts on the economic ladder. Buying an inexpensive starter home has been an important stepping stone for many families seeking to move from a rental to feeling more vested in their community, as well as potentially building wealth to pass along to their heirs.

The Dodd–Frank Banking Act has broken off some of these bottom rungs of the economic ladder by making it very difficult to obtain mortgages for the millions of inexpensive homes across the United States. Meant to protect potential homeowners, the legislation’s sweeping regulations treat all banks the same, regardless of their size or history. As a result, the act’s regulations have raised the fixed cost of originating a mortgage and put price caps on closing costs and fees, making issuing small mortgages unprofitable for most commercial banks.

Our research provides new evidence that the consequences went further: the squeeze in credit for these inexpensive properties, as well as the more onerous regulatory environment, has led to a rapid decline in housing prices in an area with the highest rates of poverty. This is the worst possible way to increase the amount of affordable housing in a city because homeowners see their equity melt away and may even end up underwater by owing more than their house is worth. Yet this problem is under-reported. Far more attention is paid to increasing the supply of housing in cities with hot real estate markets by relaxing zoning restrictions. As meritorious as that may be, it overlooks a large sector of the housing market. Maybe that’s because many policy experts tend to live in cities with relatively expensive housing, and therefore they have a blind spot when it comes to the financing problems facing small-dollar homes.

Using the case study of Winston-Salem, we find clear evidence of a tale of two cities: one that has enjoyed home appreciation and wealth-building, while the other depreciated and has seen wealth evaporate. The west side of the city—primarily White and wealthy—has enjoyed an economic rebound while the east side—primarily Black and Hispanic—languishes economically. Our regression estimates show that property values have declined over 40 percent in East Winston—a low-income area dominated by inexpensive homes—relative to the rest of the county since the passage of Dodd–Frank.

Our empirical results support our initial hypothesis: when Dodd–Frank banking regulations were imposed on banks, this led to an evaporation of potential buyers who previously could have used mortgage and home improvement credit, leading to a drop in demand for these homes. Investors offering cash to buy these properties have sometimes been maligned as predatory or greedy. But as we have seen, there are few other buyers who have the wherewithal to purchase these homes. There is strong evidence that this has negatively affected property values and, as a result, the east side of the city languishes in poverty and underinvestment. Future research may identify similar trends that have happened in other cities experiencing long-term economic decline in areas with a great concentration of small-dollar homes.

Our research thus indicates that the Dodd–Frank Act has harmed individuals and families who had already been described as victims of predatory lending practices prior to the Great Recession of 2008–2010. Though unintended, the legislation has resulted in lost home equity (potentially in the hundreds of millions, if not billions, of dollars) as well as obstructed access to home ownership for many at the bottom of the economic ladder. Therefore, federal policies that aim to improve the lending environment for small-mortgage loans deserve the highest priority, to help individuals, families, and our lowest-income neighborhoods.

Readings

- “Did the 2010 Dodd–Frank Banking Act Deflate Property Values in Low-Income Neighborhoods?” by Craig J. Richardson and Zachary Blizard. Public Choice 197(3–4): 433–454.

- “FDIC Community Banking Study.” Federal Deposit Insurance Corporation, December 2020.

- “Small Mortgages Are Getting Harder to Come By,” by Ben Eisen. Wall Street Journal, May 19, 2019.

- “Small-Dollar Mortgages for Single Family Residential Properties,” by Alanna McCargo, Bing Bai, Taz George, and Sarah Strochak. Urban Institute, April 2018.

- “The Impact of Dodd–Frank on Community Banks,” by Tanya D. Marsh and Joseph W. Norman. American Enterprise Institute, May 2013.

- “The Lending Hole at the Bottom of the Homeownership Market,” by Sabiha Zainulbhai, Zachary D. Blizard, Craig J. Richardson, and Yuliya Panfil. New America, November 2021.

- “The MicroMortgage Marketplace Demonstration Project: Building a Framework for Viable Small-Dollar Mortgage Lending,” by Alanna McCargo, Linna Zhu, Sarah Strochak, and Rita Ballesteros. Urban Institute, December 2020.

This work is licensed under a Creative Commons Attribution-NonCommercial-ShareAlike 4.0 International License.