Ever since the Old Testament patriarch Joseph advised Pharaoh to store grain against the risk of an impending famine, stockpiling for supply disruptions has been common practice. In the 20th century, ensuring adequate supplies of petroleum and its products emerged as a strategic issue during World War I when it became apparent that modern armies and economies require an uninterrupted flow of energy. Creating a strategic reserve of petroleum against the threat of disruption was first proposed toward the end of World War II. Various proposals were revisited in the 1950s, but it was not until the events of 1973–1974—the often-called “Arab oil embargo”—that President Richard Nixon made protecting the United States against petroleum supply interruption a matter of policy. Building and maintaining a large strategic reserve of petroleum was a cornerstone of this policy.

The Strategic Petroleum Reserve (SPR) was commissioned in 1975 by President Gerald Ford. The nations of the Organization for Economic Cooperation and Development were advised to keep three months or so of supply in storage; with a capacity of 727 million barrels, the SPR is the world’s largest such reserve.

Although the SPR was created to address import disruptions, over the years its role has expanded. It has been used repeatedly for situations deemed of national importance related to price stabilization. During the first Gulf War, draw-downs were authorized, as well as during Hurricane Katrina in 2005 and Hurricane Harvey in 2017. Following the Libyan revolution of 2011, the U.S. government, in coordination with other OECD countries, released 30 million barrels of petroleum from the SPR as a means of stabilizing markets. In total, oil has been released 11 times in response to domestic disruptions, including six caused by hurricanes.

After nearly half a century of operations, the facility is in extreme need of upgrades and re-investment. As a consequence of a 2016 long-term review of the SPR by the U.S. Department of Energy, Congress was advised that $375 million was needed for urgent repairs and that at least $2 billion is needed to ensure long-term operation. The current tensions in the Persian Gulf offer us an ideal time to evaluate the SPR.

Costs Versus Benefits

Providing even a few months of import protection for an economy as large as the United States does not come cheap. To date, about $5 billion has been spent on the SPR and over $20 billion in filling it with crude oil. Although the salt caverns that have been hollowed out in Louisiana and Texas for storage are literally and figuratively sunk costs, maintaining and managing the SPR has over time represented approximately 20% of its total cost. In addition, there is the opportunity cost of the money used to keep oil in the SPR as opposed to that money being in the bank or being used to reduce the national fiscal deficit. While the oil in the SPR has been acquired at different price levels, marking-to-market at today’s $60 per barrel price and assuming a cost of capital of 3% results in an opportunity cost exceeding $1.2 billion per annum for the SPR.

In addition to the opportunity cost of capital, there is the opportunity cost of not operating the SPR in a commercial manner, as is the practice of major integrated oil companies with privately owned storage facilities for crude oil, petroleum products, and natural gas. A facility such as the SPR, if commercially operated, would be “cycled” with daily injections or withdrawals of around 4.5 million barrels per day (MMbd) according to opportunities for arbitraging the differences between actual storage costs (cost-of-carry) and the cost of hedging in futures markets.

To appreciate the value potential in operating physical storage, one must understand futures markets. Futures markets are best understood as a means of artificial or synthetic storage. If a business fears higher or lower prices in the future for a key commodity (imagine jet fuel for airlines), then it can purchase the commodity now and pay the opportunity cost of capital not being in the bank earning interest. Alternatively, rather than actually purchasing the commodity and storing it, the business could take a position in the futures market, short or long depending upon underlying requirements. In equilibrium, both approaches should have the same cost, minus the actual cost of storing a physical commodity adjusted for the convenience of having the commodity at hand immediately. As one of many strategies, if financing oil in storage (“the carry cost,” in trader parlance) is less than the premium someone purchasing oil for future delivery would pay on the New York Mercantile Exchange, then someone with access to physical storage could make money by purchasing oil, storing it, and promising delivery in the future. A trader with physical storage can profit whenever the futures market is not aligned with financing costs.

What is the value potential from trading around physical storage capacity? As physical storage confers flexibility, it may be valued as the right to exchange, for example, March crude oil for June crude oil. Although the value potential is a function of assumptions about prices (variances in prices commonly known as volatility) and correlations now and into the future (given the size of the SPR), the value potential from cycling a facility of this scale would be huge. To the extent that the SPR is not used in this manner, there is the additional opportunity cost of a non-economically optimized asset.

Petroleum Markets, Then and Now

Recent debates around maintaining the SPR have focused upon the changing conditions in global petroleum markets. The world today uses about 40% more petroleum daily than it did in 1975. Yet, from slightly over 40% in 1980, today’s production from OPEC members has fallen to about 37% of total global production. Moreover, OPEC members now consume more of their own production because of their own economic development. Thus, OPEC’s net contribution to global markets is around 30%.

Notwithstanding previous concerns of the 1990s that oil production had “peaked,” today we have entire new regions of the world such as Angola, Brazil, the deep off-shore, and the Arctic contributing to global supply. New exploration frontiers have opened in Africa and South America. In the United States, it was once forecast that oil production in the Lower 48 would now be in a two-decade-long decline, yet we are seeing the opposite. A revolution in exploration and production driven by such technological advances as directional drilling and the recovery of deposits from “tight seams” through hydraulic fracturing have substantially enhanced the United States’ supply position and energy security.

Since the SPR was built, U.S. dependence on imported petroleum, especially from OPEC nations, has decreased markedly. Today, the United States is the world’s largest producer, with production exceeding 12 MMbd. And U.S. consumption of oil peaked around 2005 at 20.8 MMbd; today it is about half a billion barrels per day less, reflecting the falling energy intensiveness of America’s gross domestic product as well as the increasing role of other energy sources such as renewables. Global supplies of petroleum are much more diversified than they were half a century ago and U.S. exposure to import disruption is greatly reduced.

Energy Security and Vulnerability

For many decades now, measuring energy market security has been a concern for both policymakers and academics. The U.S. DOE and the International Energy Agency of the OECD have used large-scale economic models to measure the economic effects of supply disruptions. Even though there is a global market for crude oil and products, the focus of such models tends to be at the country or regional level, examining exposure and resilience to disruptions. Large-scale simulation models in which economic agents respond to price signals, undertake investment, and change patterns of consumption are used to inform policy design but may have limited scope for analysing the effects of short-term disruptions.

In academic research, the focus tends toward the development and calibration of metrics to measure energy market security. Some researchers look at the balance of supply and demand, consider resource estimates, examine the ratio of imports to domestic production or measures of economic structure such as producer concentration, and incorporate such factors as energy intensiveness, price elasticity, and market conditions.

These efforts are interesting and tell us much about vulnerability and resilience, but they do not tell us about the probability of a supply disruption taking place. These models focus upon exposure to disruption and the ability of a nation or region to absorb the effects of such an event, but they do not probe the chances that it may happen.

That these modeling efforts ignore the probability of a disruption occurring is curious. The arguments for maintaining the SPR surely should include the probability of a disruption taking place. In the insurance and finance literature, three parameters are used to characterize a risk:

- the exposure to potential loss if the event occurs

- the scope for mitigation or loss absorption within a specified time frame

- the probability of the event happening

The probability of supply disruption is important because we repeatedly see major events in oil market that appear capable of interrupting physical supply and affecting prices, but markets absorb the shocks and remain resilient. In 2016 we saw sabotage in Kirkuk, a strike in Kuwait, the Canadian wildfire, Nigeria’s force majeure, export blockage in Libya, Colombian pipeline disruptions, Italy’s Val d’Agri shutdown, and fire at Brazil’s Barracuda–Caratinga site. These were all serious events; none of them, however, led to disruptions or affected oil prices, which continued to trade in a range of $26 to $54 per barrel. Similar observations may be made for 2017, when—despite OPEC’s production cuts—market liquidity was unaffected. In 2018, the wave of political protests across Iran along with sanctions led to sharp declines in production, but global markets for oil remained stable, with Brent trading between $50 to $86 per barrel and historically steady price variability. Today, Venezuela produces about one-third of what it pumped in the 1970s for reasons that are well-known, but markets remain stable.

Looking further back in history, during the Suez conflict of 1956, oil production from the Middle East was reduced by approximately 1.7 MMbd in November. But the effects were short-lived, with production restored to normal by February 1957. Notwithstanding what was portrayed in the popular press, the cutbacks associated with the Iranian Revolution in 1978–1989 led to no global oil supply disruption despite many worrisome predictions.

Interestingly, those supply reductions that were disruptive historically also involved government intervention. The supply disruption in the summer of 1951 resulted from an orchestrated response to the Iranian nationalization of its oil industry. A global boycott of its production removed 19 million barrels per month of production from global markets. The effects of the boycott were exacerbated by the U.S. domestic price controls in place during the Korean War. Similarly, it has been argued that the effect of the 1973–1974 Arab oil embargo, including the long queues for transportation fuels in major U.S. cities at the time, resulted from the Nixon administration’s imposition of price controls and the misallocation of transportation fuels between Petroleum Administrative Districts (PADS) by the U.S. Department of Energy. Recent and historical events show the resilience of global petroleum markets. On those historic occasions when markets were less resilient, government policies played a pivotal role in market disruption.

The Probability of Supply Disruption

The United States, like other countries of the OECD, follows the IEA’s 90-day import replacement guidance on minimum stockholding requirements. But is this sufficient or is it wasteful?

The various models facilitate comparing the costs with the benefits of having a reserve to augment supply during disruption if an event has taken place, but they ignore the fact that such events are exceedingly rare. This oversight seems questionable. Given the infrequency of supply disruptions, as we have documented, how can we construct a probability distribution that assesses economic insecurity and resiliency? How can we compare the expected costs with the expected benefits?

In the recent Energy Strategy Reviews article “A Financial Option Perspective on Energy Security and Strategic Storage,” Laura Haar and I try to answer these questions. To introduce the probability of disruption into the measurement of energy security, we derive probabilities from traded option prices. Usefully, the forward-looking nature of option markets embodies the views of participants about prices in the future. Markets for crude oil, petroleum products, and natural gas hold the attention of countless agents seeking to secure supplies, hedge exposures, speculate, and take advantage of anomalies through arbitrage. We argue that option prices provide better insights into energy security and the threat of disruption than the metrics and models currently used by policymakers.

Traders put a premium on options that are deeply in-the-money, such as the right to purchase crude oil at $50 when the market is at $60, or to sell crude oil at $70 when the market is trading at $60. From the size of these premiums for deeply in-the-money and out-of-the money options, we can derive probabilities across a distribution of future prices. If oil market disruptions were anticipated, then greater probability would be attached to extreme prices, as calculated using well-known option-pricing formulas.

Unlike relying upon “experts,” we use the information embedded in traded option prices representing the collective views of millions of buyers, sellers, and oil traders globally. We use published data from the International Commodity Exchange (ICE) on option prices and volatilities for the crude oil benchmark, Brent, to determine the probabilities attached by the world’s traders to extreme prices embedded in option prices, allowing us to infer the chances of supply–demand imbalances.

Three Case Studies

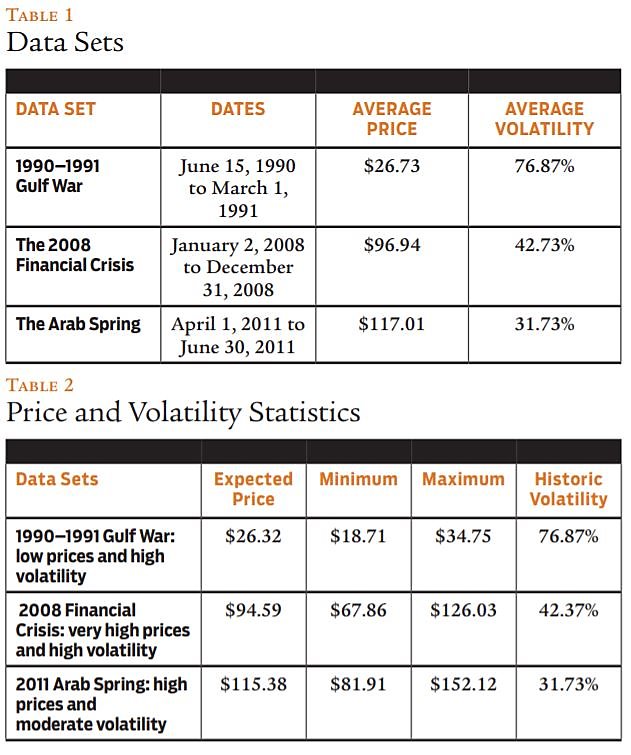

Reflecting upon whether the SPR was needed historically, Haar and I examine the perceptions of traders through the probabilities embedded in option prices during three periods when pundits and even “experts” conjectured that prices might rise inexorably. Using our method, we compute risk-neutral probability histograms for the periods shown in Table 1, with the results summarized in Table 2. From the probability histograms we can determine the market’s expectation of future prices.

Beginning with the implied risk-neutral histogram for the Brent crude oil prices during the 1990–1991 Gulf War, we see in Figure 1 that, over the dates shown, the market expectation of future prices was slightly skewed to the left. In the views of the trading community, there was a greater probability of prices falling. Although price volatility (a measure calculated from a rolling 30-day standard deviation of percentage change in price annualized to a business year of 252 trading days) at the time was high (77%), as reported in Table 1, the expected price for the year was around $26 per barrel. Notwithstanding extreme scenarios of how the Gulf War might unfold, market participants pricing options did not believe disruptions were likely: the probability of greater prices was smaller than the probability of prices softening and the probability of extremely low or high prices was much lower than the expected price of $26.

As shown in Figure 1, the probabilities ascribed to tail-events grew smaller over time. Traveling forward in time from the front of our three-dimensional graph to the back, the total probability of extreme high prices decreased dramatically (the red, green, purple, and blue areas decrease). The day after the United States and its allies attacked Iraq, oil prices in London and New York plunged an unprecedented $10.56 a barrel to $21.44, 10¢ below its price the day before Iraq invaded Kuwait. The price remained in this range throughout the conflict. Market participants correctly discounted any effect upon oil prices from the conflict.

We next turned to the 2008 Financial Crisis. Our findings are shown in Figure 2. Moving forward in time, we see that the total probability of extreme high prices (blue and red areas) decreased and the overall distribution of expected prices flattened. Emergency policies from central banks had not commenced and the potential for shale oil in the United States was yet unknown. As the year progressed, the distribution grew flatter, with growing market uncertainty. Although the shockwaves from the financial crisis were only beginning to reverberate, probability attached to extreme scenarios such as demand collapsing grew smaller. As summarized in Table 2, according to constructed probability distributions, the mean expectation was that oil prices would remain at just over $90 per barrel. As reflected in markets, oil prices during the financial crisis were high, but volatility only increased sharply toward the end of the year. It reached 103% for Brent crude on December 16th, as shown in the flattening distribution in Figure 2. Although the widening financial crisis added to oil market risks, based upon option prices, market participants were still anticipating reliable supplies at prevailing price levels and again proved prescient. Even with the ensuing banking collapses and the sovereign debt crisis, oil markets continued to function.

During the Arab Spring of 2011, the average prices of crude oil were high while volatility was moderate. As the crisis unfolded, by December 2010 some analysts were predicting that the demonstrations in Tunisia would lead to supply-chain disruptions and a sharp rise in oil prices. As unrest spread to other countries, the threat of interruption gained credibility. The IEA coordinated a draw-down of strategic reserves to calm markets. The threat of civil unrest spreading to the Gulf, for example, was raised and calamitous scenarios were suggested.

But there were some dissenting voices. A report from the Oxford Institute for Energy Studies warned against alarmism, arguing that oil markets are remarkably resilient and that the basic conditions of supply and demand were unlikely to change. A paper from the United Kingdom think tank Chatham House on the Arab uprising drew similar conclusions. Interestingly, from the probabilities derived from option prices, we see in Figure 3 a flattish distribution, reflecting a divergence of views. Compared with the previous two histograms, the distribution was flatter because market participants attached greater probabilities to prices becoming both higher and lower. According to option markets, the median view was for prices to remain around $120 per barrel. We see throughout the period only slight weight was given to prices going even higher, but like the dissenting voices, the market appears not to have taken seriously the possibility of extreme prices. Petroleum market traders were not attaching large probabilities to extreme events. There were probabilities attached to higher prices; the distribution was flattish, but the median of the distribution still had the greatest mass. In contrast to the doomsayers, the market perception was that petroleum supply and demand were sufficiently resilient to weather the various events of 2011.

Our examination of probabilities derived from option prices are illustrative. They neither prove that markets are always resilient nor that disruptions cannot take place. But the results support the following points:

- The common challenge of constructing probability distributions on rare events may be overcome through the information embedded in traded option prices.

- From a policymaking perspective, examining a potential loss if the event occurs and the scope for mitigation or loss absorption, without weighing the probability of the event taking place, provides limited insight.

- In the periods examined, markets were not anticipating extrema as might occur under a disruption scenario.

As shown in Table 2, markets did not expect price spikes and the prices to which even small probability events were ascribed were not outliers. Arguably, according to forward-looking price estimates obtained from the risk-neutral density functions, markets were not anticipating supply disruptions and proved accurate: participants correctly foresaw that market shortfalls or disruptions were unlikely. Even with output from some producers falling, in the periods examined, markets were not anticipating price levels consistent with disruptions or other forms of supply insecurity.

If, during these volatile situations, traded markets attached only small probabilities to price extremes as might occur through supply disruption, it seems fair to ask whether maintaining the SPR is justified. If, during these three historical cases, the SPR was not needed, should the United States continue supporting it?

The SPR as a Market Stabilizer

National storage of crude oil is widely seen as a precautionary public good designed to mitigate the effect of severe and sustained import disruption. Yet, petroleum products are both excludable and rivalrous in nature. Privately owned crude oil inventories in the United States frequently exceed 500 million barrels, or about three-quarters of the SPR volume. Should the United States store all that petroleum? If the SPR is not needed because petroleum markets are resilient, is there a role for government in reducing or eliminating risk even if the probability of disruption and extreme price scenarios is remote?

Like requiring medical insurance or mandating saving for retirement, might expenditure on storage be justified to avoid free-riders? Might negative externalities arise through insufficient management of risk? Is there a case for reducing risk in petroleum markets, and how might it be measured?

Although the SPR was created to address import disruptions, over the years it has been used instead for price stabilization during such events as the Gulf War, the collapse of the Libyan regime, and various hurricanes. Repeatedly, the SPR has been used to calm markets in this fashion even though oil producers, consumers, and traders have available liquid global markets in options and futures to hedge exposures and manage risks. If petroleum markets are resilient and robust to disruptions, might using a strategic reserve to dampen market volatility—making markets more predictable and reducing or even eliminating the cost of hedging—be justified as a public good?

Formally, the decision on how much of a public good should be produced requires finding the level of production that equates marginal social benefits with marginal social costs. Holding physical storage at a known price is an alternative to risk-managing the exposure using options. In Figure 4 we compare the marginal benefit from risk reduction using the prices of European call options with the approximate costs per annum of managing the SPR. As the figure indicates, unless volatility is reduced by about 20% (from an assumed volatility of 50% to about 40%), the costs of maintaining the SPR (shown by the red line) are not covered. Although the results can be re-calibrated to a different assumed initial volatility, these results reflect historical volatility values.

It would be hard to justify spending $2 billion in fresh funds today on maintaining and upgrading the SPR, given the benefits in risk reduction shown in Figure 4.

One would need to see market volatility reduced from 50% (by assumption) to 30%, or a nearly 40% reduction in market risk, for the benefits of volatility reduction (as shown by the blue line) to exceed the cost of risk reduction (as shown by the green line) to justify the investment in maintaining the SPR. And this would occur only if the SPR were used presciently, selling when the market is tightening and purchasing when the market is loosening.

Conclusion

There might be a case for keeping the SPR if it were actively used to dampen market volatility, but the gains would need to be large. And the management of exposure to petroleum markets is not a public good as economists define the term. From airlines to car manufacturers to oil companies, everyone has the right to manage exposure to oil prices according to the risk–reward tolerance of shareholders. There is no reason to believe that the benefits of risk management may be under-consumed, creating social costs and externalities. (Perhaps one could argue that the existence of such reserves helps to deter certain oil-producing countries from trying to exert their market power, but this is difficult to establish.)

Indeed, having strategic reserves may even contribute to moral hazard because parties that should manage their own risks become free-riders, like financial institutions relying on the Federal Reserve as a “lender of last resort.” This possibility has been noted in agricultural futures in the United States where, despite scope for hedging of exposures, farmers prefer to rely upon price supports from the U.S. Department of Agriculture.

Petroleum markets, like the world itself, will remain a risky place. Given the historical resilience of petroleum markets to quiet severe shocks, the scope for private parties to manage their own risks, and the costs of maintaining the SPR, the hard-earned dollars of U.S. taxpayers could be better spent.

Readings

- “A Financial Option Perspective on Energy Security and Strategic Storage,” by Lawrence Haar and Laura N. Haar. Energy Strategy Reviews 25: 65–74 (August 2019).

- “Conceptualizing Energy Security,” by Christian Winzer. Energy Policy 46: 36–48 (July 2012).

- “Energy Security: Definitions, Dimensions and Indexes,” by B.W. Ang, W.L. Choong, and T.S. Ng. Renewable and Sustainable Energy Reviews 42: 1077–1093 (February 2015).

- “Gas Storage Valuation: Price Modelling v. Optimization Methods,” by Petter Bjerksund, Gunnar Stensland, and Frank Vagstad. The Energy Journal 32(1): 203–228 (2011).

- “Historical Oil Shocks,” by James D. Hamilton. In Handbook of Economic History, edited by Randall E. Parker and Robert M. Whaples; Routledge, 2013.

- “Not All Oil Price Shocks Are Alike: Disentangling Demand and Supply Shocks in the Crude Oil Market,” by Lutz Kilian. American Economic Review 99(3): 1053–1069 (2009).

- “Oil and the Macroeconomy since World War II,” by James D. Hamilton. Journal of Political Economy 91: 228–248 (1983).

- The Prize: The Epic Quest for Oil, Money and Power, by Daniel Yergin. The Free Press, 1991.

- “The Three Perspectives on Energy Security: Intellectual History, Disciplinary Roots and the Potential for Integration,” by Aleh Cherp and Jessica Jewel. Current Opinion in Environmental Sustainability 3(4): 202–212 (September 2011).

This work is licensed under a Creative Commons Attribution-NonCommercial-ShareAlike 4.0 International License.