Janice Lynch Schuster sat crouched at her computer keyboard last January 29 at 9:59 a.m. The heater sputtered; the snow flurried; and—as she recounted in a February 3, 2012 Washington Post op-ed—Schuster was ready to compete in the 100-click dash for tickets to Bruce Springsteen’s “Wrecking Ball Tour” stop at Washington, D.C.‘s Verizon Center. Waiting with her were thousands of other die-hard Springsteen fans and hundreds of ticket-purchasing “software robots” (bots).

For good luck, Schuster wore her “Tramps like us” t‑shirt (“’cause tramps like us, baby, we were born to run”). Bots don’t rely on luck; they rely on science—computer science. Schuster hoped to grab a couple of tickets for herself; the bots, to grab a boatload of tickets for scalpers.

The dash was over by 10:10 a.m. Schuster banged her fist on the desk. The bots tugged their winnings off to the scalpers, while Schuster was empty-handed. Still fuming, she swore not to pay scalpers “$300 or $400 for tickets in the nosebleed seats.”

Congressman Bill Pascrell (D, N.J.) agrees, lamenting that secondary markets ask fans to pay a “king’s ransom” to see Springsteen, AKA “the Boss,” in concert. He argues that the “average” fan can’t compete and worries that soon “only people who can afford a $10,000 ticket [will] be able to see the Boss.”

Schuster wrote that she would like to “take a wrecking ball to the [bots].” New York already has, recently making it “unlawful for any person to utilize automated ticket purchasing software to purchase tickets.” Congressman Pascrell hopes to have the federal government swing its wrecking ball at bots as well, recently announcing plans to reintroduce the Better Oversight of Secondary Sales and Accountability in Concert Ticketing Act, nicknamed the BOSS Act, a not-so-subtle nod to Springsteen. One of its new provisions would explicitly outlaw “computer software” designed to buy up tickets as soon as they go on sale.

The BOSS Act would do more than just outlaw bots; it would shackle secondary ticket sellers. The act would prohibit brokers who resell more than 25 tickets a year from buying tickets in the first 48 hours they are on sale. According to Pascrell, the goal is to “reel in” secondary ticket markets—the act is a net designed to scoop up large-volume scalpers while letting die-hard fans and small fish swim on. With fewer scalpers in the water, Schuster would have a much better chance to snag some tickets.

Average Fans Can’t Compete?

We are fans of Bruce Springsteen, but not die-hard ones. We first heard about the Wrecking Ball Tour long after tickets first went on sale, but immediately agreed, “We gotta go.” After a 100-click meander, we bought a couple of tickets in the secondary market to see him perform at Gillette Stadium near Boston. We got great seats, ones that are on the field, 55 rows from the stage.

Listening to Schuster and Pascrell, you’d think we paid thousands of dollars for our tickets. We actually paid $124 per ticket, only $11 over the face value. How is that possible? Our short answer is, “The internet.” Our longer answer is that the internet has made secondary ticket markets more competitive by moving most of the trading from parking lots to online resale marketplaces where consumers can more easily compare the ticket deals offered by different sellers.

Secondary ticket markets have evolved from local, isolated trades characterized by a woeful lack of information to a national market with hundreds of thousands of participants who have their fill of information. From an economist’s perspective, it’s been an evolution from primitive markets to advanced ones, moving closer and closer to the ideal of a perfectly competitive market. The evolution has not been steady, instead marked by periods of rapid change initiated by important innovations in technology.

The most important innovation was StubHub, founded in 2000. Suddenly there was an online marketplace where thousands of people could resell their tickets to concerts, plays, and sporting events. For a while, the market stayed static because, while StubHub made it easy to compare seats within sections, it was harder to do so across them. Another pivotal innovation, SeatGeek, which was founded in 2009, solved that problem. For every ticket listed, SeatGeek predicts its market value and uses that prediction to produce a “deal score,” supplying the consumer with information about prices conditioned on the quality of the seat. SeatGeek not only rates tickets, but also aggregates them, collecting and displaying tickets for sale on the websites of brokers and online marketplaces such as StubHub.

Foot-tappers and head-bangers | This evolution of secondary ticket markets has been squeezing out the profits arising from poorly informed consumers being out-bargained by scalpers. But these improvements don’t eliminate the potential profits from sellers’ attempts to reward their most strident fans, who make performances more exciting for everyone else. Musicians often want to put their most enthusiastic fans up front because their enthusiasm is contagious. It’s like a virus but a healthy one, creating spillover benefits as it spreads from person to person. We are foot-tappers, not jump-and-jivers—and certainly not head-bangers—so it may be efficient to relegate us to sections farther from the stage.

Markets often unravel attempts to favor one type of fan over another. The problem is that foot-tappers often have the money to buy seats up front, creating profit opportunities that attract bots. Hence, it is possible to tell stories that rationalize legislation like the BOSS Act as repairing a market failure.

The BOSS Act was first introduced in 2009 but died in committee. It seems like a no-brainer that if it were enacted, different people would be sitting in the best seats at Springsteen’s concerts this year—more die-hard fans like Schuster and fewer foot-tappers like us. But while enacting the BOSS Act would have changed who first got their hands on tickets, it might not affect who ends up with them. If die-hard fans are rational and markets are frictionless, the hands of die-hard fans will be slippery and the tickets will still end up in the mitts of foot-tappers like us. But the hands of die-hard fans may be sticky, so endowing them with a head start in the race for tickets might succeed in changing who sits in the best seats.

The danger of the BOSS Act is that it’s a wrecking ball that swings too wildly, harming consumers by knocking down structures that have evolved to make secondary ticket markets more competitive. The happy ending to the story of how we got our tickets resulted from the recent evolutionary progress of secondary ticket markets and might have been wrecked by unnecessarily aggressive public policies. Nonetheless, we will explain how the spillover benefits of enthusiastic fans justify attempts to reward them, how markets have evolved to do so, and how government policies might help—but probably will hinder—markets.

SeatGeek: An Evolutionary Jump in Competition

We first heard about the Wrecking Ball Tour from a Red Sox announcer, who mentioned that the Boss would be performing at Fenway Park in August. Within minutes we were on Ticketmaster, where we discovered that the only concert that fit into our schedule was at Gillette Stadium in Foxborough, Mass., on August 18.

After entering our request for two of the best available tickets, Ticketmaster asked us to type “genest wrexham,” a hurdle designed to thwart the bots of ticket scalpers. It’s a test that humans can pass more easily than bots can. In computer science lingo, these sorts of tests are called CAPTCHAs, or Completely Automated Public Turing Tests to Tell Computers and Humans Apart. Put simply, CAPTCHAs are automated systems used to distinguish other automated systems from flesh-and-blood ones.

In response, scalpers have hired bot-complements, commonly known as humans, who sit in boiler rooms and specialize in passing CAPTCHAs, lending their human hands to lift the bots over the hurtle.

By the time we got to Ticketmaster, the race between the bots and die-hard fans was over, having been run months earlier. Hence, we were being tested by a CAPTCHA that was standing guard over a nearly empty castle of tickets. The best tickets available were in Row 15 of Section 303, just 11 rows from the top of the stadium. “They are just like the ones that my mother bought for me and your aunt to see the Beatles at Philadelphia’s JFK Stadium,” David told Emma. “We could see the Beatles—they looked like little bugs on a faraway stage—and heard them singing, but couldn’t make out the lyrics.”

We left Ticketmaster’s website and went to SeatGeek’s, leaving the primary market and entering the secondary one without ever leaving our seats. On the day we bought our tickets—May 28—SeatGeek displayed tickets offered on StubHub and the websites of 51 other secondary ticket sellers. Slightly more than 50 percent of the tickets displayed were from StubHub, including the ones we eventually bought. In the parlance of the Internet, SeatGeek is a ticket aggregator.

One of the best known aggregators is Kayak, which compares the prices of flights offered by different airlines. Kayak sorts airline tickets by price because most consumers just care about getting from city A to city B, making airline tickets nearly a homogenous commodity. People don’t feel the same way about tickets to concerts and sports events, preferring to sit near the action rather than far away in the upper deck. In this case, sorting by price isn’t as helpful because cheap seats in the upper deck aren’t necessarily preferable to expensive ones near the stage.

SeatGeek sorts tickets by their deal score, which reflects the gap between the asking price and the predicted market value of the ticket. How does SeatGeek predict the market value of tickets? It starts by estimating each seat’s quality. This requires that it answer questions such as, “Is Seat A in the last row of the lower deck better or worse than Seat B in the first row of the upper deck?” SeatGeek lets the fans decide by looking at occasions when the seats were offered for sale at the same price. If more fans chose Seat A than Seat B, then A is deemed better than B. By looking at these sorts of choices throughout the stadium, SeatGeek creates a function that summarizes the quality of different seats. It then adjusts the function for a particular event using information on the seats already sold to produce an estimate of the market value of the seats. These are then compared with the asking prices, and voilà, deal scores.

Tickets are then tagged as “best deals,” “great deals,” “good deals,” “okay deals,” “so-so deals,” “bad deals,” and “awful deals.” On SeatGeek’s seating chart, the “best deals” are marked with a large green dot, screaming “Go, buy me!” while the awful deals get a small red dot, whispering “Stop, don’t get swindled.”

Looking at SeatGeek’s seating chart of Gillette Stadium, we eyed a pair of tickets five rows from the stage in Section A2. We drove through the Stop sign and clicked on the tickets. When we saw the asking price of $1,085 per ticket, we slammed on the brakes and backed up into our price range.

We next checked out a Go 40 rows farther back but still in A2, speeding toward what we thought would be the finish line. The price was $194 and we were itching to buy. A glance at the seating chart revealed other green dots a bit farther back. After some investigation, we settled on a pair of tickets for $124 apiece, 50 rows back from our dream seats, but a whole lot less expensive. They were only $11 above face value. No swindling here.

Before we entered the secondary market, we agreed that we would spend up to $200 per ticket for good seats. We expected to have our resolve tested, never dreaming that we would snag good seats for $124. Lift your hands and praise markets!

And praise SeatGeek! After driving through the first Stop sign, we obeyed SeatGeek’s traffic signals, clicking only on tickets earning high deal scores until we reached our destination. We ignored tickets that earned lower scores because their prices were higher than those of similar seats. Normally, we would have worried that the low price of our tickets indicated low quality. With the aid of SeatGeek, we knew that its low price was an indicator of a great deal, not bad seats. If most people behave like us, sellers who set prices higher than the market price will lose all their customers, meaning the demand curve they face is very elastic.

Ticket aggregators like SeatGeek also offer the potential of making the demand for listing tickets on StubHub more elastic. Many people view StubHub as the “place to go” to resell their tickets, giving it some market power in setting its fee, which is currently 25 percent of the selling price. Prior to ticket aggregators, potential competitors would have to incur significant costs to get their names “out there.” Now they can get exposure via SeatGeek and other ticket aggregators, putting pressure on StubHub to reduce its fees.

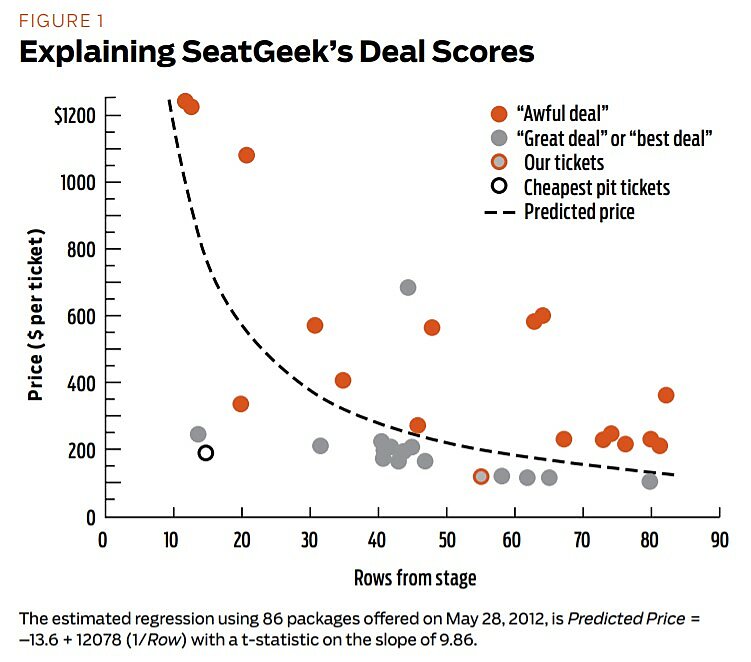

Graphing great (and awful) deals | Looking at SeatGeek’s seating chart for Gillette Stadium, we knew that we wanted seats on the field. We had no interest in the front-and-center “pit area,” which sounded vaguely dangerous and certainly exhausting. We also had little interest in the border sections—we wanted to be safely in the center of the action. To illustrate the idea behind SeatGeek’s deal scores, we created a data set of the 86 packages of tickets that satisfied our criteria. Regressing Price per ticket on the inverse of the number of Rows from the stage produced the predicted price curve illustrated in Figure 1. The dots represent our best and worst options according to SeatGeek.

All of the great deals identified by SeatGeek are below our predicted price curve, and all but one of the awful deals are above the curve. That makes sense: great deals are less expensive than expected given the row and awful ones are more expensive. The tickets we bought are represented by the grey dot circled in orange—they are in Row 55 and cost $124 per ticket. There were other great deals closer to the stage, but we opted to go with one that was stunningly less than our price cap, which to us was the best deal.

The dot circled in black is the least expensive pair of pit tickets, at only $195 per ticket. Judged by the distance below our price curve, it ought to be a spectacular deal. But SeatGeek only gives it a deal score of 72, a passing but not high grade. Why? SeatGeek’s algorithm is flexible: able to reflect the differences in seats that are not caused by discrepancies in the distance from the stage. The algorithm doesn’t know what it is about the pit tickets; it just knows that their market value is lower. We know that the pit is pricy in its own way: in wear and tear on your sneakers and your muscles and your time. If you add these implicit costs to the purchase price, the yellow dot would move closer to the line and wouldn’t appear to be a great deal.

The pit occupies the most valuable real estate at a Springsteen concert—right in front of the stage and stretching nearly its entire length. But it has no actual seats. It is like building slums on Park Avenue, but as we will see below, it serves a purpose: only some people—the die-hard fans—like to slum it. And, Springsteen wants them there.

The Spillover Benefits of Head-Banging Fans

Making secondary markets more competitive is a great thing, but it won’t eliminate the bots as long as the prices of some of the best seats are set below their market value. Many bands, including Springsteen and his buddies in the E Street Band, want to give their die-hard fans a break on ticket prices, especially on seats near the stage. These head-banging, gyrating fans produce spillover benefits for the rest of the crowd and for Springsteen, who is fueled by their energy. Quite simply, they are part of what everyone else comes to see.

New York Times columnist David Brooks credits Springsteen and his lyrics with influencing the way Brooks interprets the world. In a column about his “Other Education,” he describes taking his daughter to her first Springsteen concert. “She had her hands clapped to her cheeks and a look of slack-jawed, joyous astonishment on her face. She couldn’t believe what she was seeing—10,000 people in a state of utter abandon.”

The people who astonished her were not fans like us. We don’t do utter abandon, let alone head-banging. The only evidence of our enthusiasm is a tapping foot and a slight smile. Unlike the head-bangers, we don’t share our joy, but rather bottle it up in our private consumption. The social benefits of us going to the concert are the private ones, accurately measured by our demand for tickets. On the other hand, the demand of the head-bangers underestimates their social benefit by the spillover joyous astonishment of others, which is what buttoned-up economists call a positive externality.

Rewarding head-bangers | From an efficiency perspective, die-hard fans ought to be paid for their head-banging efforts. Many bands try to do this by lowering the price of the best seats below their intrinsic market value, hoping that their die-hard fans will grab them up when they first go on sale. While die-hard fans are likely to know about the “on-sale” date, so are bots.

Bands are struggling to price-discriminate in favor of their die-hard fans, not the bloodless bots, leading them to experiment with alternative strategies and enlist the government to help. To think more about these alternatives, let’s create a simple economic model.

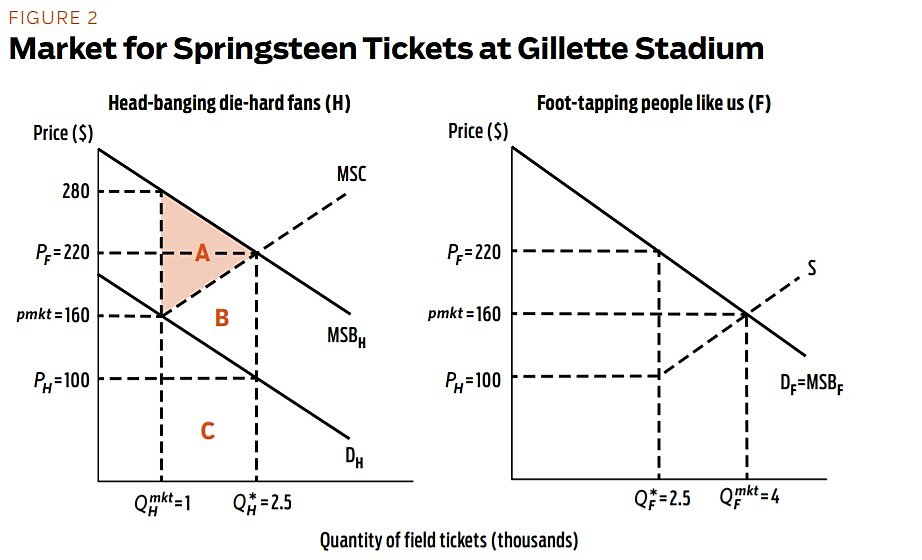

Suppose the market for tickets to the concert at Gillette Stadium is composed of two types of fans: head-bangers (H) and foot-tappers (F). Also assume that the best seats are the ones on the field near the stage and that there are a fixed number of them, say 5,000. Figure 2 illustrates a couple of hypothetical demand curves, one of die-hard fans (DH) and the other of foot-tappers (DF). The marginal social benefit curve of the die-hard fans (MSBH) is above their demand curve by the value of the spillover benefits they produce. In contrast, there is no gap between the MSB curve and the demand curve of foot-tappers like us, i.e., the social value of having us there just equals the amount we are willing to pay.

In our example, the market separates fans into winners and losers—those having tickets and those deprived of them—by setting the price at $160 per ticket. At this price, the quantity of tickets demanded by head-banging die-hard fans (QHmkt = 1,000) plus the quantity demanded by foot-tappers like us (QFmkt = 4,000) equals the fixed supply of field tickets (QS = 5,000).

Markets are blind to spillover benefits and, as a result, fail to take into account the importance of head-bangers as producers of joyous astonishment in others. They are also blind to spillover costs, such as the spilled beer, obstructions, and grunts of increasingly corpulent people trying to find their seats after the concert has started. Our model ignores spillover costs because we assume—for simplicity and kindness—that only die-hard fans and punctual people like us attend concerts.

The market fails to allocate tickets efficiently, dampening the mood and straight-lacing the experience. More die-hard fans should be let through the gate. But how many more? The answer is easy—you should continue to let them through the gate as long as the social benefits exceed the social costs.

Look again at Figure 2 and focus on the market solution, where head-bangers buy 1,000 tickets (QHmkt = 1,000) and foot-tappers buy 4,000 (QFmkt = 4,000). The social benefit of adding another head-banger equals her willingness to pay for the ticket (≈$160) plus the value of the spillover astonishment she produces (≈$120). Hence, it equals the height to the marginal social benefit curve at QHmkt = 1,000 in the left-hand-side graph.

But what about the social costs? What’s given up? That’s easy: head-bangers displace people like us, the great overly washed masses. Hence, the social cost of adding more head-bangers equals the loss in social benefits of the foot-tappers they displace.

The very last foot-tapper who bought a ticket wasn’t sure he wanted to go to the concert because his willingness to pay was just equal to the market price. Hence, the social cost of giving his ticket to someone else is just the market price. However, as more and more tickets are taken away from foot-tappers, the social cost increases as foot-tappers with a higher and higher willingness to pay are displaced. What is happening graphically is that transferring more and more tickets to die-hard fans moves foot-tappers up their demand curve, implying that the marginal social cost curve on the left is just a mirror image of the demand curve on the right.

Starting at 1,000 die-hard fans (QHmkt = 1,000), Bruce and his E‑fficiency Street Band should continue adding head-bangers as long as the social benefits (height to MSB) are greater than or equal to the social costs (height to MSC). Given the hypothetical curves of Figure 2, Springsteen should let an additional 1,500 head-bangers through the gate so that the best tickets to his concert are evenly split between head-bangers and foot-tappers. Society is better off because the enjoyment of the additional die-hard fans (area C) plus the value of the astonishment they create (areas A plus B) exceeds the disappointment of displaced foot-tappers (areas B plus C). Hence, reallocating these tickets increases net social benefits by area A; equivalently, area A equals the deadweight loss of leaving the allocation of tickets to markets that are blind to spillover benefits.

The solution is easy, at least theoretically. To achieve the efficient number of head-bangers (QH = 2,500), Springsteen needs to offer them a lower price than foot-tappers, a practice economists call price discrimination. In our example, he should set the head-banging price (PH) at $100 and the foot-tapping one (PF) at $220.

Divide and barricade | This solution, however, is hard to implement. It requires Springsteen to distinguish between head-bangers and foot-tappers, i.e., he must divide them up. And then it requires him to stop head-bangers from earning a quick buck by reselling their tickets to foot-tappers, i.e., he must put up barricades between them.

Prior to the internet, tickets were sold at brick-and-mortar box offices. Die-hard fans would often come the night before, staking their tents and their places in line. Overly washed foot-tappers would never suffer through tent-life for a coveted place in line. Hence you could be pretty sure that the people at the front of the line were die-hard fans. Scalpers did hire some professional line-waiters, but only for foot-tappers willing to pay a “king’s ransom.”

Now physical lines have turned into virtual ones as fans troll websites looking for news of the next tour and then wait at their computer screens hoping to snag seats the minute they go on sale. But scalpers can troll and wait with the best of them. They are in the best position to know every on-sale date—it’s their job—and they have the bloodless bots to do the waiting for far less than the flesh-and-blood line-waiters. Hence you can be pretty sure that the “people” at the front of the virtual line are not die-hard fans. In fact, they aren’t people at all—they’re bots.

The internet has also lowered the barricades, making it easier for die-hard fans to fall for the easy buck. Back before the internet, it wasn’t always easy to find foot-tappers willing to pay a “king’s ransom” for tickets. Now, die-hard fans can make a quick buck more easily by selling tickets on StubHub.

The cult-band Phish goes to great lengths to get tickets into the hands of its “phans” at discount prices. Their attempts are subverted, however, by the fallen Phishes, who sell their tickets on the secondary market. “True Phish fans” intervene by sneering “at those [among them] who would scalp lawn seats for double the price.” But money is money; even Phish Heads are human; and only sticks and stones can hurt them.

The BOSS Act: Head Start for Die-Hard Fans

Congressman Pascrell introduced the BOSS Act to give fans a better chance to grab tickets when they first go on sale. He believes that the current system is rigged in favor of professional brokers whose bots claw tickets away from fans. The BOSS Act would give fans a head-start by prohibiting brokers from buying tickets in the first 48 hours that tickets are on sale and from using bots. Without it, Congressman Pascrell asks, “How is the average guy or gal supposed to compete?”

They can’t, he answers, saying, “The fan is getting ripped off, period.” Janice Lynch Schuster felt ripped off. As did Jamie Brown, who spent four frustrating hours at his computer trying to buy Springsteen tickets on the day they went on sale, only to be booted off empty-handed. As he told the Wall Street Journal, Jamie then faced an unpleasant choice: either pay much more than he planned for a couple of tickets from a secondary ticket seller or skip seeing Springsteen perform this year.

Suppose Brown chose to skip the concert rather than buy tickets in the secondary market. He is a rational guy, and he could have weighed the benefits and costs of buying tickets on the secondary market and concluded, “No way.” He may have thought, “Thank goodness I didn’t tell my fiancée Courtney that I planned to take her to the concert.”

Suppose the BOSS Act were enacted in 2009 and scalpers strictly obeyed the letter and spirit of the law. Given a two-day head start and a bot-free marketplace, die-hard fans should have gotten their hands on most of the best seats. No question—die-hard fans would be better off. But would the BOSS Act change who sits in the seats? The answer depends on whether die-hard fans have slippery or sticky hands.

Slippery hands | With the help of the BOSS Act, Brown would have been able to snag tickets in the primary market. But would he have gone to the concert? Once he discovered how much tickets were selling for on the secondary market, he might have thought to himself, “Wow! Thank goodness I didn’t tell Courtney I got tickets.” Selling the tickets is what a rational guy would do; if Jamie felt that seeing Springsteen wasn’t worth the cost of buying tickets on the secondary market before the BOSS Act, then it shouldn’t be worth forgoing the opportunity to sell them for the same amount after the BOSS Act. It doesn’t make him a greedy jerk; it makes him a predictable guy with slippery hands.

The BOSS Act would put more money into the pockets of die-hard fans because some of them would cash in and others would save money because they wouldn’t have to buy their tickets from scalpers. Since the BOSS Act would enrich die-hard fans, their demand would increase and more of them would go to the concert. But not many more, assuming die-hard fans are rational and it is not too difficult to resell tickets. Foot-tappers are likely to pay enough to displace large numbers of die-hard fans regardless of whether or not the BOSS Act is enacted.

In this scenario, the BOSS Act would not eliminate the arbitrage opportunities. It would just change who exploits them. It would no longer be brokers armed with heartless bots; it would be die-hard fans who know about the on-sale date. Changing the law to protect fans would help them financially, but it would not change who sits in the seats as long as fans are rational and reselling tickets is easy to do.

Sticky hands | Brown is a sensitive man. He’s in a band himself; he’s a bit of a poet. Once he got his hands on the tickets, he began to imagine the experience of listening to “The River” live and looking at the joyous astonishment on Courtney’s face. He couldn’t let those tickets go; they already meant too much to him.

Going back to the real world—the one in which the BOSS Act wasn’t enacted—we thought Brown wouldn’t pay enough to buy tickets on the secondary market. But in our imaginary BOSS Act world, the instant he clicked on “complete purchase,” the amount that someone would have to pay him in order to purchase his tickets exceeded Brown’s old willingness to pay for them. In this scenario, he holds onto the tickets and takes Courtney to the concert. His hands are sticky.

In this case, the enactment of the BOSS Act would change who sits in the seats because of the endowment effect, which is behavioral economists’ fancy name for sticky hands. A famous experiment involving coffee mugs found evidence for the endowment effect: when some people were randomly given coffee mugs, the mug-less were willing to pay less to acquire the mugs than the mug owners were willing to accept to sell them. Ziv Carmon and Dan Ariely, in a 2000 Journal of Consumer Research paper, found evidence that Duke basketball fans likewise have sticky hands for NCAA tournament tickets: students who won tickets in a lottery were willing to sell them, but only for much more than the losers of the lottery were willing to pay for them. If the endowment effect is as significant for Springsteen tickets, the BOSS Act would increase prices in the secondary market and likely increase the number of die-hard fans in attendance. That’s bad news for foot-tappers.

Theoretically, the effect of the BOSS Act on the ultimate allocation of the seats to concerts and other popular events depends on the stickiness of fans’ hands. The outcome is different depending on whether you apply the behaviorists’ endowment effect or the logic of rational fans in a world of easy reselling.

What me? I’m not a scalper! | The BOSS Act would need to be implemented in the real world, not an imaginary one where you can assume that scalpers strictly obey the letter and spirit of the law. The BOSS Act requires anyone reselling more than 25 tickets per year to register with the Federal Trade Commission and stand on the sidelines when tickets first go on sale. Scalpers don’t like standing in lines to register with the government or on the sidelines while others are making a buck.

Many states imposed price ceilings on secondary ticket sales prior to the internet. Most of those laws have been repealed because they were unenforceable in the age of the internet and had little or no effect on prices. The BOSS Act is likely to be unenforceable as well, while soaking up enforcement resources that would be better spent elsewhere.

Our greater fear is that the BOSS Act would be a costly hindrance to the smooth functioning of secondary ticket markets. The BOSS Act would inevitably have loopholes and limitations, which large resellers, seasoned in dodging anti-scalping laws, would exploit with ease. Some small civic-minded resellers might exit the market, allowing larger resellers to raise their prices. Other not-so-civic-minded resellers might go underground, fearing that registering with SeatGeek or placing tickets on StubHub could attract the attention of the police. They might go back to relying on personal contacts with consumers and return to the world of bilateral bargaining. Others might stay on the internet but change names frequently, reducing the benefits of branding in a market where trust matters. The point is that the BOSS Act could reverse the evolutionary gains of secondary ticket markets, which have increased transparency and provided information to consumers.

The rage against bots felt by fans has led Pascrell to add a new provision to the BOSS Act, banning the software. This strikes us as something that would be difficult, if not impossible, for government to enforce. Fortunately, fans’ rage also creates incentives for sellers in the primary ticket market to ban bots from their websites. These sellers use increasingly sophisticated CAPTCHAs designed to distinguish flesh-and-blood fans from bots. CAPTCHAs are not without their catches, especially now that scalpers recruit human complements to work alongside the bots. But it is still a lot easier for the primary ticket sellers to guard the castle of tickets than for government to prosecute electronic looters after the fact. The government would be tilting at virtual windmills.

Keeping Head-bangers in Their Seats (or Not)

Springsteen doesn’t need the BOSS Act because he has found other ways to ensure that his die-hard fans capture the best real estate at his concerts.

He knows that his die-hard fans are more likely than foot-tappers to be crouched over their keyboards when his concert tickets first go on sale. But he also knows that die-hard fans are human, liable to succumb to the temptations of the secondary market. He wants to lessen the temptation for them to sell their tickets, saving the die-hards from themselves. Hence he raises the transaction costs, turning the temptation into too much of a hassle. Specifically, Springsteen sells the best seats using paperless tickets, which require purchasers to bring their credit cards and driver’s licenses to get through the gate. Now if a die-hard fan buys four tickets intending to resell three of them, he must accompany the foot-tapping buyers through the gate, to the sneers of other fans. He may even have to wait for the nonchalant foot-tappers to show up. Similarly, foot-tappers may not like associating with grungy fans, who are potentially unreliable escorts.

Paperless tickets may allow Springsteen to better price-discriminate and, as a result, enhance efficiency. But this assumes that making tickets paperless doesn’t change the fundamental nature of the tickets, and hence has no effect on the demand curves of Figure 2. But it does. It is unavoidable. It says to consumers, “You use them or you lose them.” Even the most die-hard of fans will have a lower willingness to pay for paperless tickets. People know that, well, stuff happens. A head-banger could get a concussion; a family member could die; a job could be lost. Foot-tappers could have a parent-teacher conference; be invited to a hoity-toity dinner party; stub a toe.

Paperless tickets are more perishable and, hence, less valuable to consumers than easily tradable ones. Over the course of history, the trend has been to make goods less perishable, not more. Refrigerators, preservatives, and genetic modification have all made food less perishable. Even cars last longer than they once did. Making tickets more perishable flies in the face of all that. We believe that the efficiency losses from making tickets more perishable, and hence less valuable would swamp the gains from better price discrimination.

Many of the best seats to this year’s Springsteen concerts were sold using paperless tickets, but not in New York, where a state law requires sellers to give consumers the option of buying transferable tickets. Hence, the New York law means that paperless tickets cannot enhance price discrimination—anyone who intends to arbitrage will simply choose to get a transferable ticket. No such law exists across the Hudson River in New Jersey. According to Ticketmaster, its unfettered use of paperless tickets for Springsteen’s concerts in New Jersey reduced the supply of the best seats on StubHub by 63 percent relative to the New York concerts.

StubHub and its allies in secondary markets are lobbying legislators in other states to enact laws similar to New York’s. So far, they have convinced legislators in Connecticut and Minnesota to introduce bills restricting the use of paperless tickets, but they haven’t been able to get them enacted. Not surprisingly, they are being opposed by Ticketmaster and its allies.

Congressman Pascrell recognizes that stuff happens, but takes a different tact than New York to protect consumers holding paperless tickets. Rather than offering fans the option of transferable tickets, Pascrell plans to add a new provision to the 2012 tour of the BOSS Act, requiring that sellers offer refunds to owners of paperless tickets up to two weeks before the event. Pascrell wants to make paperless tickets more convenient for consumers while still curtailing arbitrage opportunities.

The pit | Springsteen has discovered a straightforward way to keep foot-tappers at bay—take away some of the best seats and create an open space, which he calls “the pit.” One fan described the pit as an “amazing, exhausting, and exhilarating experience,” a non-stop four hours of jumping, jostling, and jiving. Another said that it’s “not for the faint of heart.” Head-bangers love the pit; foot-tappers love their seats. Quite simply, their preferences differ, allowing Springsteen to reserve the best spaces for his die-hard fans, even if he can’t guarantee them actual seats.

The prospect of standing for hours on a concrete floor jostling for space with sweaty strangers was too big a pill for us to swallow in order to be near the stage. Similarly, we wouldn’t want to swallow horse pills, but in the 1990s a drug maker used a similar mechanism to discriminate between human and equine consumers of one of its medications. Johnson & Johnson sold Levamisole to cancer patients and farmers. The version bought by cancer patients cost $6 per pill; the one used to deworm horses cost 6 cents a pill. The active ingredient was the same, but the pill for cancer patients was easier to swallow, lacking the inert fillers of the horse pill.

The active ingredient of a Springsteen concert is the performance by Bruce and his buddies in the E Street Band. The pit is much more than inert filler because it adds to the vibrancy of the concert. But it serves the same role as inert filler, making it more difficult for foot-tappers to swallow the best real estate at the concert, reducing the likelihood that die-hard fans will be able to resell their pit tickets. Hence it allows Springsteen to price discriminate in favor of his die-hard fans.

If we were the Boss… | Americans spent nearly a billion dollars in 2007 going to concerts, $5.4 billion going to plays, and a whopping $18.8 billion going to major sporting events. Selling tickets on the internet is a big business with interesting characteristics. It deals with perishable goods that are first sold by musicians, theater companies, and sport teams, and then often resold in secondary markets. There are genuine concerns that markets fail to reward die-hard fans and artists sufficiently and, as a result, government ought to intervene. But with so much money at stake, the greater concern ought to be that calls for government intervention are profiteering disguised as consumer protection.

Secondary ticket markets have become increasingly competitive over time because of innovations like online resale marketplaces and ticket aggregators made possible by the internet. These innovations have increased the size of markets and the amount of information accessible to consumers. The increase in competition has squeezed out most of the profits that used to be gouged from ill-informed consumers buying from sellers with market power.

Now, most of the profits that are attracting the bots and brokers are due to the pricing decisions of economic agents in the primary ticket market, including people like Springsteen. Bruce is a smart guy—listening to his lyrics ought to convince you of that. If he wants to funnel tickets to his die-hard fans, he can figure out how to do it without the help of government regulations. In fact, he already created the pit, uses paperless tickets for some seats, and partners with Ticketmaster to combat the bots.

Congressman Pascrell wants to “reel in” secondary ticket markets using the BOSS Act. If successful, it would scalp the profits of scalpers and benefit die-hard fans, largely by letting them become scalpers themselves. Getting more tickets into the hands of die-hard fans might cause more of them to be in the best seats, but logic and the ease of reselling make this unlikely. Also, reeling in professional scalpers is not easy; states have tried to do it in the past with anti-scalping laws and failed. Aggressively enforcing the BOSS Act would move some trades back into the shadows, reversing many of the gains of greater transparency via the internet. Hence, the BOSS Act could unintentionally scalp consumers rather than scalpers. The best way to scalp scalpers is to arm consumers with information, and the evolution of secondary markets has increased fans’ weaponry over time.

It’s fine that Springsteen wants to reserve the best real estate at his concerts for his die-hard fans and move foot-tappers like us farther back. We are grateful to him and secondary markets for allowing us to foot-tap on the field, just 55 rows back from the stage. Maybe one day we will start humming.

Readings

- “10 a.m. Freeze-Out for a Springsteen Fan,” by Janice Lynch Schuster. Washington Post, February 3, 2012.

- “ ‘Boss’ Fans Again Run into Ticket Problems,” by Jennifer Maloney. Wall Street Journal, January 28, 2012.

- Bruce Springsteen and the Promise of Rock ‘n’ Roll, by Marc Dolan. W. W. Norton, 2012.

- “Focusing on the Forgone: Why Value Can Appear so Different to Buyers and Sellers,” by Ziv Carmon and Dan Ariely. Journal of Consumer Research, Vol. 27, No. 3 (2000).

- “Lessons from a Scalper,” by David E. Harrington. Regulation, Vol. 32, No. 1, (Spring 2009).

- “The Other Education,” by David Brooks. New York Times, November 26, 2009.

- “Ticket Buyers Deserve to Have Their Rights Protected,” by Lawrence White. Huffington Post, June 12, 2012.

- Ticket Masters: The Rise of the Concert Industry and How the Public Got Scalped, by Dean Budnick and Josh Baron. ECW Press, 2011.

- “Uncapping Ticket Markets,” by David E. Harrington. Regulation, Vol. 33, No. 3, (Fall 2010).

- “The Welfare Effects of Ticket Resale,” by Phillip Leslie and Alan Sorensen. Working paper, 2011.

This work is licensed under a Creative Commons Attribution-NonCommercial-ShareAlike 4.0 International License.