Wealth inequality has become a heated political issue. Politicians claim that wealth concentration is rising and that people at the top are gaining at other people’s expense. In this study, I examine problems with the measurement of wealth and discuss whether wealth inequality is an issue that public policy needs to address. I also consider the likely effects of wealth taxation. I concur with views from the left that political rent-seeking should be curtailed and that finding economic opportunities for less-fortunate Americans is important. But I argue that a new system of wealth taxes is more likely to hurt rather than help those goals.

Section 1 discusses how measuring the wealth distribution from capitalizing income flows produces deeply misleading results.

Section 2 shows how some measures of wealth inequality have risen in recent years due to falling interest rates and rising asset prices. Those developments do not make people better off in terms of resources available for consumption, which reinforces the conclusion that wealth inequality is not a useful concept above and beyond consumption or income inequality.

Section 3 examines the distinction between consumption, income, and wealth inequality. Market wealth is a poor indicator of well-being; it ignores taxes and transfers and thus inflates measured inequality. Top-end wealth is mainly in the form of business assets, which are used to employ people and produce the economy’s output.

Section 4 describes why wealth taxes are a poor way to raise revenues, as they would undermine growth and generate large-scale tax evasion. Consumption taxes are a better revenue source.

Section 5 examines how support for wealth taxation has less to do with economics and more to do with politics. Economists Emmanuel Saez and Gabriel Zucman, for example, argue for wealth taxes in order to confiscate the wealth of billionaires who they believe have too much political power. I argue that a wealth tax would produce more cronyism and inequality.

I conclude that wealth inequality is not a useful measure, especially of economic problems facing Americans who are less well off, and that wealth taxation would cause major economic and political damage.

Section 1: Measuring Wealth Inequality

Emmanuel Saez and Gabriel Zucman caused a big stir with a 2016 study claiming that wealth inequality has sharply increased and with a 2019 book provocatively titled The Triumph of Injustice: How the Rich Dodge Taxes and How to Make Them Pay.1 Economists quickly picked apart their numbers. Rather than embark on an eye-glazing review of all the studies disputing Saez and Zucman’s claims, I will examine one such study in detail. Matthew Smith, Owen Zidar, and Eric Zwick examined the 2016 results of Saez and Zucman and concluded that the top 1 percent share of wealth in the United States has risen since the 1970s by half of what Saez and Zucman claimed.2

Both the Saez and Zucman and the Smith, Zidar, and Zwick estimates are based on many assumptions, so comparing the results from the two studies illustrates how hard wealth is to measure—and how easy it is to put a finger on the scales.

What is wealth anyway? No, the wealthy do not have vaults full of gold like Scrooge McDuck. They do have a lot of stocks and bonds. However, there is no national database of who owns what and its market value. The best we have, and Saez and Zucman’s starting point, is tax return data on how much income people get from their wealth, from which we can try to infer their wealth.

But the uber-wealthy also own businesses and venture and private equity investments with no clear market values. As Smith, Zidar, and Zwick find, “Less than half of top wealth takes the form of liquid securities with clear market values.”3 So how do we measure the value of these assets?

Enter “capitalization.” Saez and Zucman translate income flows (from tax data) to wealth by assuming that income will last forever and then discounting it at some rate. In an equation: wealth = income / discount rate. Smith, Zidar, and Zwick show how this calculation can go wrong with wealth held in the form of bonds. This is a good case because it is clear, and bonds, unlike private businesses, conceptually have clear values. They note:

In 2014, the aggregate flow of [taxable] interest income was $98 [billion], and the stock of fixed income wealth was $11 [trillion]. The ratio gives the average yield, r = $98B/$11T = 0.89%. Using this yield to capitalize income amounts to multiplying every dollar of interest income by 1/0.89% = 113 to estimate fixed income wealth.… [This procedure] gives an estimate … of $42B × 113 = $4.7T of fixed income wealth held by the top 0.1%. The bottom 99.9% estimate is $56B × 113 = $6.4T.4

The calculation simply multiplies income by the number 113 and calls it “wealth.” But why bother measuring wealth distribution at all since you can just use the income distribution? One reason is that only some kinds of income get this treatment—kinds that are more likely to be held by wealthy people, which makes the results look much more unequal.

Even just looking at bonds, Smith, Zidar, and Zwick show how this approach overstates wealth inequality. The capitalization approach assumes everybody gets the same rate of return from fixed-income assets. But a well-established fact is that wealthy people generally earn higher rates of return on their assets than others.5

Smith, Zidar, and Zwick looked at what people actually earn on their fixed-income assets. Middle-income households, who hold savings accounts, earn about 1 percent. Their wealth is about 100 times their interest income. The wealthy, who hold high-risk bonds and other financial instruments earn about 6 percent, on average. So the value of their bonds is only 1 / 0.06 = 16.7 times their interest income.

Changing from a 1 percent to a 6 percent discount rate reduces the wealth estimate per dollar of income from 100 to 16.7. This is not a small technical adjustment. Correcting to use varying discount rates at different income levels, Smith, Zidar, and Zwick find that “the adjustment reduces the top capitalization factor—and thus estimated top fixed income wealth—by a factor of 4.7, or 80%.”6 That’s not a little technical adjustment.

Beyond fixed income, capitalization estimates get even muddier.

Most basically, “capitalization” assumes an economy in which wealth sends a steady stream of income to its owners. But in the real economy, income is tremendously volatile. Many companies do not pay dividends at all, rewarding their owners perhaps with a big payoff if the company gets sold. Perhaps with this in mind, Smith, Zidar, and Zwick follow Saez and Zucman and include realized capital gains as “income.” But doing so does not make sense. Suppose you buy a stock for $1 and it grows to $100. You sell $10 of the stock, but now you only have $90 left. You cannot keep doing this forever, as capitalization assumes.

Smith, Zidar, and Zwick, following Saez and Zucman, capitalize all sorts of income into “wealth,” though the assets cannot be sold:

For S‑corporation equities, the income flow is S‑corporation income. For proprietor and partnership wealth, the income flow is the sum of proprietor income and partnership income. In the case of real estate, property tax is capitalized to estimate housing assets.7

But they leave out all sorts of other income, such as wages, salaries, bonuses, consulting income, government benefits, and so on. Beyond the arbitrariness of which income flows to include, there is a lot of guesswork on discount rates for the income flows included:

Private business returns are harder to estimate than fixed income returns because private business wealth is harder to observe than fixed income wealth.… We focus on multiple-based valuation models.8

The bottom line? The Saez and Zucman technique starts with the pretax value of “capital” income, including asset income, proprietor income, and partnership income but not “labor” income (wages, bonuses, etc.) or Social Security income. They then assume the income stream will last forever and multiply by various huge 1/r numbers to calculate “wealth.” By doing that and using low r numbers, the wealth distribution looks much more extreme than the income distribution.

As you can see, the 1/r assumption allows great latitude in how this calculation is going to come out. The capitalization formula 1/r is very sensitive to r especially for low discount rates like the 1 percent used for bonds. Going from r= 2 percent to 1 percent doubles the estimated wealth value.

In sum, capitalizing income to get “wealth” is an inherently, even absurdly, imprecise game, and one that is easy to rig. If you put the 20 best financial economists in the world together in a room, gave them all a company’s cashflow information, they could not come within a factor of three of the actual stock market value of the company by capitalizing its income. If you put 20 top MBAs in the room and tell them to pump up the value of an initial public offering, they know how to do it: valuation mostly consists of fiddling with discount rates to get the “right” answer.

This trip through the sausage factory should get you to wonder more broadly, why should we care about the distribution of something—wealth—that is essentially impossible to measure or define? If you are making money as a partner in an LLC you help to run, why should anyone care about a fictitious accounting “value” of that partnership? And why does “wealth” include the value of that partnership income but not wages you receive from a similar business or Social Security income?

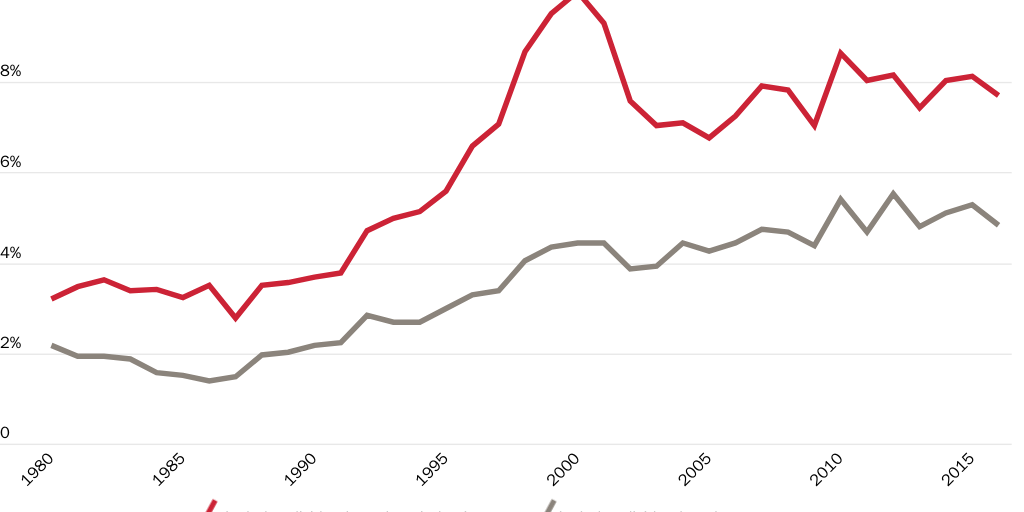

Section 2: Top Wealth and Asset Prices

Figure 1 shows the top 0.1 percent equity wealth as a share of total net wealth, according to estimates from Smith, Zidar, and Zwick.9 The top line includes capitalized realized capital gains, which is the Saez and Zucman approach I criticize in Section 1. The bottom line includes only dividends. If dividends are properly measured, the value of the firm is the value of dividends only and repurchases are irrelevant. The graph shows that decisions such as including realized capital gains as if they were dividends makes a big difference in driving up measured inequality.

The chart also makes a deeper point. The top line looks like a graph of the S&P 500 index. A lot of the supposed rise in wealth and wealth inequality—even properly defined and measured as the market value of net assets—consists of higher market prices for the same underlying physical assets.

This fact raises a deep “why do we care” question. Suppose Bob owns a company, giving him $100,000 a year in income. Bob also spends $100,000 a year. The discount rate is 10 percent; companies paying $100,000 per year dividends trade for $1,000,000. Bob’s company is worth $1,000,000. Now the interest rate goes down to 1 percent and the stock market booms. Bob’s company is now worth $10,000,000. Hooray for Bob!

But wait a minute. Bob still gets $100,000 a year income, and he still spends $100,000 a year. Absolutely nothing has changed in Bob’s life except for the nice number reported by his accountant. The value of his company is “paper wealth.”

Meanwhile, Sally earns $100,000 per year in wages, which she also spends, and she has no financial assets. The distribution of income and of consumption in this two-person society is entirely flat, but the distribution of wealth measured by the rules of Saez and Zucman is very concentrated. We ignored Sally’s human wealth, which is the present value of her future salary.

Now suppose that Bob feels richer with his newfound $10,000,000 of wealth, and he thinks about selling some stock and going on a round-the-world private jet tour. But if Bob did that, he could not continue to spend $100,000 per year as he originally planned. Originally, if he sold his company for $1,000,000 and invested it at 10 percent, he could spend $100,000 per year. But now if he sells his company for $10,000,000, he can only invest that at 1 percent per year. The most he can spend is still $100,000.

People don’t want to consume in one big spurt. They want to spread consumption over their lifetimes and pass money to their heirs. When the interest rate goes down, it takes more wealth to finance the same consumption stream. The present value of liabilities—consumption—rises just as much as the present value of assets, so on a net basis Bob is not at all better off.10

Now, if the rise in asset value came about because people expect income streams to grow a lot in the future, at unchanged discount rates, then indeed Bob is truly “wealthier” than before. But that is emphatically not the situation of today’s market value of wealth in the United States, at least on average. If anything, growth is slower than it was in the past.

It is reasonable for us to consider the distribution of consumption and, in particular, lifetime consumption. If Bob averages $100,000 consumption over his life and Sally only $10,000, that is an interesting observation about our society, and we should think about the economics, politics, and justice of the situation. But given consumption, why should we worry about an increase in paper wealth that has no implications for the overall command over resources that “wealthy” people have?

Is this paper wealth effect large? Yes. Real interest rates have plunged from a peak of about 10 percent in the 1980s to negative numbers today, computed as the 10-year bond rate less the inflation rate in the University of Michigan inflation survey. Stock prices for the same earnings or dividend streams are twice or more what they were in the 1980s.

In sum, much of the increase in wealth inequality reflects higher market values of the same income flows. Such increases indicate nothing about increases in lifetime consumption inequality, which better reflect individual command over resources.

Section 3: Wealth, Income, and Consumption Inequality

Why do we care about the distribution of wealth? Section 1 notes that wealth is poorly defined and measured. Section 2 notes changes in measured wealth distribution reflect higher market prices for the same assets that do not increase a person’s lifetime consumption.

Many people worry about income inequality. But why do people separately worry about wealth inequality, especially wealth inequality estimated from income flows? Consumption inequality is a much better measure if people are worried about inequalities in people’s lifestyles or inequalities in who is using the planet’s resources.

Wealth, income, and consumption inequality are very different. Income varies a lot from year to year, especially among the risk-taking wealthy. One year’s income is a very distorted measure of lifestyle inequality. Taxes, transfers, and savings buffer consumption from income. People generally earn more in middle age and get wealthier as they age and save for retirement, generating apparent wealth and income inequality between old and young. Most wealthy people leave their wealth invested in active businesses or give it away through charitable foundations, so wealth does not translate to consumption. Why is wealth that is not consumed but left invested in a business or given to charity a problem?

Consumption inequality is far less than income inequality, which is far less than wealth inequality. So why worry about wealth inequality, or income inequality, above and beyond consumption inequality?

Saez and Zucman claim that “carefully measuring . . . wealth is important. The public cares about the distribution of economic resources.”11 But the “distribution of economic resources” is consumption inequality, not wealth inequality. Wealth inequality, above and beyond consumption inequality, is economically meaningless.

Why Measure Wealth Based on Capital Income Only?

Suppose a lawyer, surgeon, or CEO earns $1,000,000 per year in wages. That person has a lot of human capital or wealth, which we could estimate by multiplying income by 1/r as Saez and Zucman do for capital income. But Saez and Zucman exclude such wealth in their calculations:

The current market value of all the assets owned by households net of all their debts.… Our wealth concept excludes human capital, which, contrary to non-human wealth, cannot be sold on markets.12

Smith, Zidar, and Zwick say similarly:

For aggregate wealth, we follow Saez and Zucman (2016) in defining wealth as total assets minus liabilities of individuals at market value, excluding durable goods, unfunded defined benefit pension plans and Social Security, non-profits, and human capital.13

But the separation between “labor” income produced by human capital and “capital” income is gray. People are good at reclassifying one as the other in response to changes in the tax code. When corporate income taxes go down, people incorporate. How much of small business income to its owner is “labor” vs. “capital” income? How much of even Jeff Bezos’s or Mark Zuckerberg’s huge wealth comes from sitting at home passively clipping coupons—capital income—and how much is a reward for the huge work and entrepreneurial genius they showed in starting their companies? Wealth estimates based on such distinctions are at best guesswork and at worst made up to make a point. One could define “wealth” as liquid assets only—assets that could be sold quickly to finance a round-the-world private jet tour, even though nobody wants to do that. And Saez and Zucman started that way. But then they added lots of other kinds of income from assets that can’t be sold, making the dividing line suspiciously arbitrary.

Why Take the Present Value of Pre-tax Income?

All of the calculations that capitalize income flows to estimate wealth use pre-tax income, ignoring transfers from the government and taxes. If you earn $100,000 per year and pay $50,000 a year in taxes, what sense does it make to say your wealth is $100,000/r not $50,000/r? At the other end of the spectrum, people may have little market wealth but a steady stream of income from a government entitlement program. What sense does it make to paint them as destitute?

Former Sen. Phil Gramm (R‑TX) and former Assistant Commissioner of the Bureau of Labor Statistics John Early eloquently contrast the distribution of pre- and post-tax and post-transfer income.14

Government transfers provide 89% of all resources available to the bottom income quintile of households and more than half of the total resources available to the second quintile.

In all, leaving out taxes and most transfers overstates inequality by more than 300%, as measured by the ratio of the top quintile’s income to the bottom quintile’s. More than 80% of all taxes are paid by the top two quintiles, and more than 70% of all government transfer payments go to the bottom two quintiles.15

Calculating income shares for 2015, economists Gerald Auten and David Splinter found that the top 1 percent share of U.S. pre-tax and pre-transfer income was 14.1 percent but that the top 1 percent share of after-tax and after-transfer income was 8.5 percent.16

Obviously, leaving taxes and transfers out makes income inequality appear to be a lot higher, which then is also true of wealth inequality estimates that are derived from the income data. But it is essentially dishonest.

Moreover, leaving out taxes and transfers creates a “problem” that cannot be solved by government, no matter how much taxing and transferring it does. Imagine the left’s dreams come true: the next president declares a national emergency and radically raises taxes and transfers so that income and consumption for everyone becomes the same—no inequality at all. And suppose that nobody reacts to incentives, as most on the political left seem to believe, so that pre-tax incomes stay the same. Then measured income inequality—and wealth inequality based on capitalizing that income—would remain exactly the same despite the massive redistribution! The “problem” is immune to its solution, and the left will always be calling for more.

Why Include Unfunded Government Debt and Not Unfunded Pensions as Wealth?

Saez and Zucman do not include the present value of unfunded defined-benefit pensions as “wealth.” Most of these are government employee pensions, and Saez and Zucman assume that these pensions will not be bailed out by the general taxpayer in the end. That may be a reasonable assumption, but it boosts measured inequality by removing a lot of middle-income wealth.

Likewise, Saez and Zucman do not include wealth in the form of the capitalized values of Social Security, Medicare, Medicaid, and other entitlement programs. This also removes a large source of middle-income wealth.

True, the federal government has little idea how it will pay for these entitlement programs in the future. But it also has no plan to pay back U.S. Treasury bonds. They, too, are unfunded, but they are included in wealth estimates. If we do not include unfunded pension and Social Security promises as wealth, why do we include unfunded Treasury bond promises? Well, the cynic would say, that would make measured inequality go down since rich people hold Treasury bonds.

What Harm Does Invested Wealth and Reinvested Income Do?

If you worry about wealth inequality, not consumption inequality, you are worried that wealth invested in a business and not consumed is a bad thing. A typical wealthy person leaves his or her money invested either indirectly through stocks and bonds or directly in private businesses and partnerships, and they take most of their capital income and reinvest it in existing or new companies. That is why the distribution of wealth is more extreme than the distribution of consumption.

But what harm is that wealth doing? The wealthy provide the vast bulk of national saving and investment funds. If we start taxing wealth and the wealthy respond by consuming it, giving it away, or giving it to political candidates, are we better off? Thrift and saving are a benefit, not a vice.

Why Is Wealth Inequality a Problem Requiring Policymaker Attention?

How can we care about a problem that is nearly impossible for us to define or measure and that a typical person would not even notice is a problem?

Homelessness is a real problem that you can see while you walk down the street in San Francisco. Unemployment, when it is large, is a real problem, and you can see it readily. But how is wealth inequality a problem when it is so invisible that even talented economists have difficulty defining and measuring it?

Many people, including me, are worried about a lack of opportunities and the many barriers to advancement on the lower end of America’s economic spectrum. Society as a whole is better off if the bottom end rises. This worthy impulse is what many people mean when they say they worry about “wealth inequality.” But they recognize that the life of a poor kid from Fresno is completely untouched by whether a venture capitalist in Palo Alto upgrades to a private jet and would be made no better off if a wealth tax forced that venture capitalist to drive. If you are worried about opportunity, mobility, left-out and left-behind people and areas, as I am, good for you—but “wealth inequality” is a deeply misleading term to describe those concerns. If you state the problem as “inequality,” then the logically inescapable conclusion is that society is better off if Bill Gates loses $1,000 and you and I lose $10, as inequality is now less. If you don’t agree with that proposition, then you’re not fundamentally worried about inequality. Think a bit and use a better word.

Section 4: Wealth Taxation

Economists have no professional expertise to object to redistribution or argue for it. You may not like redistribution for political, moral, or other reasons, or you may be all for it, but economists have no special insights into the right amount of redistribution. If it were possible to take money from A and give it to B without creating any adverse incentives, economists would have no special standing to cheer or to object.

Economists can tell us about incentives. Economists can point out that taking money from A and giving it to B causes A and B to change behavior, usually in ways that make things worse for all of us. Economics can tell us something about tax rates but not much about taxes.

Thus, the theory of optimal taxation is straightforward. It answers the following question: How can the government raise a given amount of tax revenue while generating the least perverse disincentives? The theory of optimal redistribution offers an additional wrinkle: How can the government give money away while generating the least perverse disincentives to recipients as well as payers?

Disincentives include evasion—what accounting moves will people make to avoid taxes? And disincentives include changes to economic behavior—will people move, stop working, invest less, choose different careers, or make other choices in response to taxes? Evasion loses the government revenue and employs a lot of lawyers and accountants. But the real damage to the economy comes from the behavioral disincentives.

In this traditional understanding of how to analyze taxes, the wealth tax is a very inefficient way for the government to raise money. It generates a swarm of avoidance and does a lot of economic damage per dollar raised. That is why most of Europe has abandoned wealth taxes and the United States has not imposed one.

One basic conclusion of optimal tax theory is “don’t tax rates of return.” Wealth taxes essentially impose a heavy tax on the rate of return to savings and investment. If you consume money fast rather than invest it, you save a bundle of wealth taxes. People react to a tax on rates of return by saving less and consuming more. Over the long run, even small changes in consumption versus investment behavior result in a lot less investment capital. Like any other famous result in economics, of course, this one attracts a beehive of theorists looking for ways to unseat it, but in my view, it is pretty solid. It stems essentially from the principle to tax inelastic things and not tax elastic things.

A tax on rates of return taxes when you consume, not your overall level of consumption. You have some money. Should you consume it all today or invest it and consume tomorrow? If there is a high tax on rates of return, you consume more today and less tomorrow to avoid the tax. It is like taxing groceries at Whole Foods but not at Safeway. A better tax would tax consumption equally today and tomorrow and not distort when you choose to consume.

Put another way, the wealth tax—like a rate of return tax—taxes money that has already been taxed. People earn money, pay taxes on it, invest it, and then pay taxes again. The government should only tax it once. A great lie is that the rich pay lower taxes than us when tax rates on capital are lower than tax rates on wages. It is a lie because it only counts the second-round tax on the returns to savings, not the first-round tax on the income that produced the savings.17

A substantial wealth tax would be a neon sign to the wealthy: Don’t save your wealth, consume it now! Take a private jet on a round-the-world tour! Give your money away to political candidates before it can be taxed! (I highlight that because supporters argue that a wealth tax would reduce the political influence of the wealthy. But its incentives are the opposite.) Also, a substantial wealth tax screams: don’t get wealthy in the first place by working hard or starting a business because the government will just take it away from you!

A progressive wealth tax, like the progressive income tax, strongly discourages risk taking. Suppose you have $20 million and a choice between investing in a Silicon Valley startup with a 1 in 4 chance of making $100 million or in the quiet safety of government bonds. A progressive wealth tax induces people to invest in the government bonds. If you are choosing careers between entrepreneur and lawyer, the wealth tax tells you to become a lawyer—especially a tax lawyer.

Underlying this analysis are the two distinctive features of modern economics: decisions are made comparing the present to the future, and considering risk, decisions respond to incentives.

A wealth tax also focuses its disincentive to invest on people who have already made a lot of money. But who will fund the next immensely valuable company? A wealth tax means that the people who made the last successful investment will not make the next one. But people who have been successful at starting companies in the past have skill at it and are precisely the ones we want investing in and starting new companies.

Now, optimal taxation theory does say that a wealth tax can be a perfect tax—if the government confiscates wealth completely and unexpectedly and promises credibly to never do it again. That way, the government gets the revenue but produces no distortions. People have no choice but to go back to work and save and build that wealth up again. Such a “capital levy” is a true tax on wealth without taxing rates of return.

The catch: such a tax has to be truly unexpected and happen only once. If people see it coming, they scramble to get out of the way. And having been impoverished once, people wonder if maybe the government might do it again; then they refuse to work, save, and build wealth that might be taken again. Capital levies are something governments can do only in extremely rare, visible, once-per-century crises, with some strong precommitment never to do it again. That is not the currently proposed wealth tax!

The proposed wealth tax would tax away the incentive to get rich. That is bad because people get rich by inventing new and better products, starting new companies, increasing efficiencies, and lowering prices.

Advocates belittle these arguments with a claim that the wealth tax rate is small. A rule of thumb from the theory of taxation is that the economic damage of a tax is proportional to the square of the tax rate. Roughly, the damage equals the price distortion times the quantity distortion. The quantity is proportional to the price, so damage is price squared.

So, a 2 percent or even 6 percent wealth tax rate might not seem so bad. But one should compare those tax rates to the rate of return, not to the principal amount. Take a fixed-income investment, which these days may only pay interest income of 1 percent per year. We currently tax that interest income at federal, state, and local levels. If you pay a 50 percent income tax, then you get 0.5 percent return after taxes. A 0.5 percent wealth tax is the same as a 50 percent income tax in this case. A 6 percent wealth tax would be effectively a 600 percent capital income tax rate!

Hank Adler and Madison Spach in the Wall Street Journal noted that to pay a wealth tax you have to sell assets, which multiplies the size of the tax.18 If you sell assets, you have to pay federal and state capital gains tax in addition to paying the wealth tax:

Consider a hypothetical founder of a California company who has to pay a 6% tax on wealth in excess of $1 billion. The founder is exclusive owner of a company with a fair market value of $6 billion.… The founder’s wealth in excess of $1 billion [i.e., $5 billion] would initially trigger a $300 million wealth tax. To raise the $300 million, he would need to sell $1.053 billion (17.6%) of the company to pay Ms. Warren’s 58.2% federal capital-gains tax, California’s 13.3% income tax, and the 6% wealth tax. (The $1.053 billion sale price minus $613 million in federal capital-gains taxes, minus $140 million of California income taxes leaves $300 million.)

Including the wealth tax on the first billion dollars, at the end of five years, sales of roughly $3.69 billion of the company would be required. The founder would have paid 61% of his net worth in taxes, losing most of the business.19

As they point out, this is only the beginning. Most businesses also borrow money, and if you sell part of the business, you have to repay debt before you do anything else. If, for example, the company is half financed with debt, then you have to sell $2 of assets, pay back $1 of debt, and then start paying all these taxes.

In sum, on standard optimal-tax grounds, the wealth tax is a terrible way for the government to raise revenue.

Evasion

Wealth taxes are extraordinarily open to evasion, which is another reason most countries that had them abandoned them. There is nothing like the prospect of an annual 6 percent tax to focus the minds of billionaires and their accountants and lobbyists. Tax evasion tends to get worse over time as individuals and businesses learn how to game the system and gain special tax rules and exemptions from Congress.

The United States currently has a wealth tax, the estate tax. It applies a 40 percent tax once a generation. It is a mess of avoidance and evasion. Wealthy families structure their businesses with the estate tax in mind from the day a grandchild is conceived. Forty percent once a generation is less than 2 percent per year. A 2 percent wealth tax doubles the estate tax. Six percent per year adds up to three times as much. The wealth tax is a big tax that people will do a lot to avoid.

How do you avoid wealth and estate taxes? First, take businesses private or invest in private businesses that do not have clear market values. Real estate is especially good because of the complex tax treatment and difficulty of valuing large investments. Then create complex share structures to spread ownership of the businesses, staying one step ahead of the Internal Revenue Service (IRS) valuation rules. For example, set up multiple share classes in which outside investors or family members with less than $1 billion in wealth hold all IRS-valued “wealth” and inside investors get all the benefits. Add multiple interlocking LLCs and Cayman Islands special entities and nobody will figure it out. The New York Times’ various exposes of President Trump’s tax dealings are wonderful examples of how wealthy dynastic families appear to get around income taxes, estate taxes, and even sales taxes, perfectly legally. It would be much worse under an annual wealth tax.

Saez and Zucman anticipate some of these objections to a wealth tax:

The greatest risk to enforcement comes from base erosion due to the exemption of specific assets, such as business assets and unlisted corporate equity.… International experience shows that base erosion tends to occur when specific constituencies (such as business owners) lobby to become exempt.20

Indeed, base erosion would be rampant. Farm businesses, small businesses, factories producing solar panels, businesses in rust-belt cities, and many other businesses would come screaming to Washington for wealth tax exemptions.

Saez and Zucman continue on the issue of valuing business assets:

Other countries such as Switzerland have successfully taxed equity in private businesses by using simple formulas based on the book value of business assets and multiples of profits. The IRS already collects data about the assets and profits of private businesses for business and corporate income tax purposes, so it would be straightforward to apply similar formulas in the United States.21

I think that misses the point. These are taxes on small businesses. The uber-wealthy don’t own businesses. They own complex claims on businesses, claims that would get more complicated as soon as a wealth tax were passed. Good luck valuing four or five classes of shares, combined with debt that includes various options, funneled through various interlocking partnerships and the like.

Valuing real estate … Local governments have a cadaster of real estate property for the administration of local property taxes. Such property taxes are based on assessed value. In most states, assessed values closely follow market value.22

Two words: Donald Trump. As with businesses, wealthy people don’t own real estate in their own names. They own shares of complex entities that eventually own real estate, all of it designed for tax avoidance. Saez and Zucman take the evidence that you and I pay property tax to infer that Trump enterprises will do so. That is silly.

Saez and Zucman address this issue:

Some assets are held through intermediaries such as trusts, holding companies, partnerships, etc. To prevent avoidance, all the assets of intermediaries should be included in the tax base of their ultimate owner (granter or grantee, in the case of a trust) at their market values, without any valuation discount. Formulaic rules can be set to divide the ownership of jointly-held assets for wealth tax purposes.23

But how do we untangle who actually owns what, especially when the structures are designed to hide that fact?

Here is a revealing Saez and Zucman footnote:

Estate tax revenue collected in 2017 from wealthy individuals who died in 2016 was only $20 billion. This is only about 0.13% of the $15 trillion net worth that the top 0.1% wealthiest families owned in 2016. This demonstrates quantitatively that the estate fails to take much of a bite on the wealthiest (in spite of a reasonably high 40% nominal tax rate above the $5 million exemption threshold, set to increase to $10 million in 2018). The main factor driving such low tax revenue is tax avoidance.24

So people react to the estate tax predictably by forming complex asset structures, which destroy the revenue from that tax. How then would the government avoid exactly this result from the wealth tax? Saez and Zucman do not say.

The overall answer strikes me as a reiteration of a classic liberal conceit: Oh yes, it is all terrible now, but it has just been done badly. Put smart people like us in charge, and we will somehow be immune to political pressure and will really put the screws on. But even the New York Times concedes, “Name a tax and there’s a way to reduce it, delay it or not pay it. Financial advisers say a wealth tax would be no different.”25

Optimal Taxes, Bottom Line

If we want to raise revenue with minimal economic distortions, the wealth tax is an awful way to do it. A consumption tax is a much better approach. It can be levied either directly or from taxing income less savings. It would tax consumption overall, and you could not avoid it by consuming earlier. It would tax the rich at the Porsche dealership while leaving them incentives to keep their money invested, which benefits the broader economy. People who support redistribution would be better to favor a progressive consumption tax or use a high consumption tax combined with benefit programs.26

Because of these realities, the U.S. tax code and tax codes in other advanced economies have slowly reduced taxes on rates of return—both directly through reduced rates on dividends and capital gains and via a plethora of special vehicles such as 401(k)s. A wealth tax would go in exactly the opposite direction of nearly every advanced economy over recent decades.

Section 5: It’s All about Political Power

Wealth is not a good way to measure inequality. The wealth tax is not a good way to raise revenues. What then is the purpose of a wealth tax and all the alarmist rhetoric about wealth inequality?

Saez and Zucman are quite clear in a New York Times op-ed:

Their [high marginal tax rates] root justification is not about collecting revenue … high tax rates for sky-high incomes do not aim at funding Medicare for All. They aim at preventing an oligarchic drift that, if left unaddressed, will continue undermining the social compact and risk killing democracy.

An extreme concentration of wealth means an extreme concentration of economic and political power.… Democracy or plutocracy: That is, fundamentally, what top tax rates are about.27

The point of the wealth tax is to destroy the supposed political power of billionaires by destroying their wealth. The arguments of Saez and Zucman in other venues, about the economic evils of wealth inequality and how much revenue the wealth tax would raise, are, by their own admission, a ruse.

Most economists want to find taxes that raise revenue and don’t kill the golden goose that lays economic eggs. Saez and Zucman want to kill the golden goose. To them, the wealth tax will be successful if it raises no revenue and destroys the wealth subject to the tax.

Saez and Zucman continue, “That few people [in the 1960s] faced the 90 percent top tax rates was not a bug; it was the feature that caused sky-high incomes to largely disappear.”28 The point is to make high incomes disappear. By the way, their comment is misleading since 90 percent tax rates only made reported incomes disappear while tax shelters exploded.

To most economists, the point of taxes is to raise revenues without disincentives—to tax the rich without discouraging people from becoming rich so that they can get rich and pay the taxes. But Saez and Zucman want the disincentives. They want to tax billionaires to the point that there are no billionaires and that nobody bothers trying to become a billionaire. Why? If you view all wealth as ill gotten, basically criminal, as perversions of democracy, then you want to destroy the incentive to engage in those nefarious activities.

However, Saez and Zucman are not particularly consistent, arguing in other places that the wealth tax would raise lots of revenue rather than just destroy wealth. They are advisers to Senator Warren, who has made raising revenues a central part of her agenda. She wants the wealth tax to fund Medicare for all, but Saez and Zucman say in the New York Times it would not.

Do Billionaires Really Run the Country?

Do billionaires have too much political power? This is a mantra of the political left. Here is John Cassidy in the New Yorker:

The Citizens United ruling, the rise of super PACs, and the lurch to the right of the Republican Party and, of course, the Trump Presidency have demonstrated the growing political power of the billionaire class.29

What billionaires is he worried about? Tom Steyer? Michael Bloomberg? George Soros? Bill Gates, who devotes billions to global charities? The Business Roundtable CEOs who endorsed “stakeholder capitalism”? The bleeding hearts of Davos? It strikes me that many billionaires in this country are progressive coastal elites.30

Wealthy people did not buy the election for Donald Trump. Chris Edwards and Ryan Bourne note:

Not one CEO in the Fortune 100 had donated to Trump’s election campaign by September 2016. His victory did not stem from influence by the wealthy but more from grassroots opposition to wealthy coastal elites.31

The money was on Hillary Clinton, who spent nearly double what Trump did. I perceived Clinton, famous for Goldman-Sachs speeches, as just the kind of candidate one who dislikes cronyism should worry about. Trump was a wild card, elected by workers in flyover states.

A wealth tax will prompt a flood of billionaires and their lawyers and accountants to come begging for exemptions on Capitol Hill. That is not a way to get rid of cronyism but to ramp it up, to force the billionaires to get close to those in power. Maybe that is the point.

Sen. Bernie Sanders (I‑VT) said, “Billionaires should not exist.” He echoes George Bernard Shaw, who said, “The more I see of the moneyed classes, the more I understand the guillotine.”32 So the point is decapitation. “Wealth inequality” is supposedly such a crisis that we are better off getting rid of billionaires and throwing all their businesses that generate the nation’s jobs and incomes into the ocean.

Ill-Gotten Wealth

Wealth tax advocates view all wealth at the top as ill gotten or gained by luck. Saez and Zucman claim, “Progressive income taxation … restrains all exorbitant incomes equally, whether they derive from exploiting monopoly power, new financial products, sheer luck or anything else.”33 Can you think of any sources of income that are missing here?

Robert Reich opines that there are only five ways to make a billion dollars: “exploit a monopoly … get insider information unavailable to other investors … buy off politicians … extort big investors … get the money from rich parents or relatives.”34 Just who made Reich’s iPhone, I wonder?

Edwards and Bourne document a view more consistent with my reading of the facts:

Most of today’s wealthy are business people who built their fortunes by adding to economic growth, and some have created major innovations that benefit all of us. The share of the wealthy who inherited their fortunes has sharply declined in recent decades.35

Thomas Piketty’s story of centuries-old inherited wealth growing at r > g is a fable. The existing rich are not getting richer. Almost all of today’s super-rich are nouveau rich. At best, this generation’s self-made internet billionaires and hedge fund managers made more money than the last generation’s Waltons and bond traders.

There is an element of truth, as in all fables. Edwards and Bourne go on:

Cronyism, which refers to insiders and businesses securing narrow tax, spending, and regulatory advantages. Cronyism is one cause of wealth inequality, and it has likely increased over time as the government has grown.36

The really big billionaires in places such as Silicon Valley built tremendous products and pocketed only a tiny fraction of the resulting benefit. But there is a lot of government cronyism in the U.S. economy, such as government-created barriers to competition.

But to the extent that wealth is amassed by exploiting regulations, barriers to entry, subsidies from the government, or narrow tax breaks, how in the world is more government the answer? If the politically connected wealthy get narrow tax breaks today, wouldn’t they also get them under a wealth tax? If too much government activism and micromanagement is the problem, how could larger government be the answer? Hangovers are not cured by bloody marys.

Section 6: Conclusions

I like conciliation and finding common ground. In that spirit, here is something Saez wrote that I agree with entirely:

My sense is really that the public will favor more progressive taxation only if it is convinced that top income gains are detrimental to economic growth of the 99%, and that taxation can ameliorate this. In America, people do not have a strong view against inequality per se, as long as inequality is fair. And what does fair mean? As an economist, you would say fair means that individual income and wealth reflect the value of what people produce or otherwise contribute to the economic system. This is why distinguishing between the standard supply side scenario versus the rent-seeking scenario is so important.37

Amen, brother Saez. In my view, people do not really regard “inequality” as unfair. The real concern is rent seeking. But an enormous, complex wealth tax would make that problem worse by attracting the same swampy lobbyists who game the regulatory system and income and estate taxes today.

In the end, this is all about political power. Saez, Zucman, and others on the left want to transfer power from private hands to the government while eliminating other sources of financial power that may compete with the government. Whether that is a good idea depends on your view of how bad private versus government power is.

Even in the worst excesses of private economic power, I see some discipline of competition or potential competition restraining it. But the defining character of government power is a lack of competition and a monopoly of force. The essence of Saez and Zucman is to reduce the competition for power faced by whoever runs the government, by eliminating a center of well-financed opposition. In my view, historically, the damage of extreme government power—Soviet and Chinese Communism, German Nazism—is orders of magnitude worse than even the worst caricatures of private economic power.

I presume that with a wealth tax in place, Saez and Zucman would not want to hand the reins of government to a new Trump administration or a Republican Congress, or maybe even to Democrats who also hand out cronyist goodies to billionaires. So their argument must be that the “good politicians” will take over in their world and will never hand the reins over to a future Trump. And this time the leaders won’t misuse a monopoly of power even though they have been made stronger by a lack of private power to challenge them under their system. That certainly would be a triumph of hope over long experience.

About the Author

This work is licensed under a Creative Commons Attribution-NonCommercial-ShareAlike 4.0 International License.