This essay is a part of the Pandemics and Policy series.

The Federal Reserve should

-

recognize the limits of monetary policy;

-

avoid drifting into credit allocation and fiscal policy;

-

return to its pre‐2008 operating system, pay interest on required reserves only, and normalize its balance sheet;

-

resist yield curve control, which would diminish its independence and credibility;

-

work with Congress to establish a monetary commission to examine the boundary line between monetary and fiscal policy, and consider the case for adopting a monetary rule.

The 2007-08 financial crisis ushered in unconventional monetary policy, including large-scale asset purchases (also known as quantitative easing, or QE), outright credit allocation with the purchase of agency debt and mortgage-backed securities, and a new operating system—the so-called floor system—in which the Board of Governors uses interest on excess reserves (IOER) as its key tool for setting its policy rate. Unlike the pre-2008 operating system, the new system incentivizes banks to hold large reserve balances at the Fed.

Charles Plosser, former president of the Federal Reserve Bank of Philadelphia, was one of the first to recognize the danger of unconventional monetary policy—namely, “a large Fed balance sheet that is untethered to the conduct of monetary policy creates the opportunity and incentive for political actors to exploit the Fed and use its balance sheet to conduct off-budget fiscal policy and credit allocation.”

The onset of COVID-19 in March 2020 and the ensuing government lockdowns severely affected output and employment and were followed by a “dash for cash” (i.e., a decline in the velocity of money). The Fed basically promised to do “whatever it takes” to restore monetary and financial stability, and it quickly launched a number of special purpose vehicles in conjunction with the Treasury Department. For the first time, the Fed made funds available through these vehicles to corporations, “Main Street” businesses, municipalities, and states. In addition, the Fed began providing funds to the Term Asset-Backed Securities Loan Facility to purchase risky assets—including commercial mortgage securities and collateralized loan obligations—none of which show up on the Fed’s balance sheet.

The COVID-19 pandemic motivated the Fed to put QE on steroids, set its policy rate at the zero lower bound, use forward guidance to keep rates lower for longer, and launch an array of emergency credit facilities for nonbanks—backstopped by the U.S. Treasury with $454 billion provided by Congress under the Coronavirus Aid, Relief, and Economic Security (CARES) Act, which President Trump signed into law on March 27, 2020. The Fed also extended its global reach by setting up “U.S. dollar liquidity swap lines” with foreign central banks.

The Fed’s scope and power is greater than ever before. The CARES Act effectively enlarged Section 13 (3) of the Federal Reserve Act, which was intended to allow the Fed to engage in emergency lending to provide “liquidity to the financial system” but “not to aid a failing financial company.” By engaging in credit allocation and fiscal policy, the Fed risks becoming more politicized and less independent as Congress looks to it as a way to bypass the democratic process and dodge its constitutional duty to make the difficult choices about spending and taxing.

Recognize the Limits of Monetary Policy

The Fed’s primary responsibility is to ensure long-run price stability and maximum employment, as well as moderate long-run interest rates. It is not to engage in fiscal decisions about how to allocate credit or fund off-budget spending programs designed by Congress. There is no free lunch: running the monetary printing press cannot create real wealth, but it can affect real variables in the short run and be used to monetize government debt. Moreover, under the post-2008 operating system, the Fed is open to abuse by politicians who see the central bank as a means of financing government programs without increasing taxes or taking on debt.

Any stimulus effect from unconventional monetary policies will be short-lived. To generate real economic growth in the long run requires increased productive capacity, which means better institutions, additions to human and nonhuman capital, and technological progress. It’s important that the central bank avoid monetary disequilibrium by providing liquidity to meet the demand for cash balances and to keep nominal gross domestic product (GDP) on a level growth path. Monetary stability is necessary for financial stability and for the efficient operation of a market economy. But the driving force for real economic growth comes from a system of property rights and justice that protects the private sphere and personal freedom, not an untamed expansion in the money supply.

Monetary stability is necessary for financial stability and for the efficient operation of a market economy.

Quantitative easing, which is intended to lower long-run interest rates and spur asset prices and spending, is not a panacea for a strong economy. Suppressing market interest rates using large-scale asset purchases and forward guidance may create a short-run wealth effect, but once rates return to more normal levels, which could take a long time, economic growth will revert to its long-run trend as determined by market forces. Meanwhile, zero short-run interest rates, and near zero longer-run rates, create a search for yield, cause heavy indebtedness, and penalize those who depend on interest income for their retirement. In addition, by distorting interest rates and subsidizing risky investments, unconventional monetary policies—if carried on for too long—interfere with corrective market forces, misallocate resources, and reduce future growth prospects.

Related Read

The Fed’s Policy Drift

Americans should be entitled to a more substantial review that also calls into question the very foundation of the Fed’s operations. Such a review should consider alternative monetary frameworks, including NGDP targeting.

If money creation were the source of real wealth, central banks could simply print money, and people could have as many goods and services as they wanted at no cost. This “free lunch” mentality is seductive, especially to politicians. That is why it is so important to recognize the limits of monetary policy in generating real economic growth and to draw a bright line between monetary and fiscal policy—as recommended by the late Marvin Goodfriend, an economist at the Federal Reserve Bank of Richmond and Carnegie-Mellon University.

Draw a Bright Line between Monetary and Fiscal Policy

The Fed’s drift into fiscal space politicizes monetary policy and sets a precedent for further off-budget fiscal policy. As Esther George, president of the Federal Reserve Bank of Kansas City, notes, “Income from the Fed’s large balance sheet combined with our capital surplus could temp fiscal authorities to view the Fed as a source of funding for government programs.” To rein in the Fed and maintain its independence, there must be a clear demarcation between fiscal and monetary policy.

Monetary policy should not be used to allocate credit to specific uses. When the Fed expands base money (i.e., currency held by the public and bank reserves held at the Fed) by buying Treasuries, the funds go to the Treasury (the nation’s fiscal authority). Congress appropriates those funds and enacts spending bills through the democratic process. That process is circumvented when the Fed takes on fiscal responsibilities.

Goodfriend held that when the Fed sells Treasuries out of its portfolio to acquire loans or non-Treasury securities, “credit policy” is better understood as “debt-financed fiscal policy.” He recognized that “interest on reserves frees monetary policy to fund credit policy independently of interest rate policy,” which opens the door to all kinds of mischief. Moreover, he argued that “an ambiguous boundary of responsibilities between the Fed and the fiscal authorities contributed to economic collapse in fall 2008.”

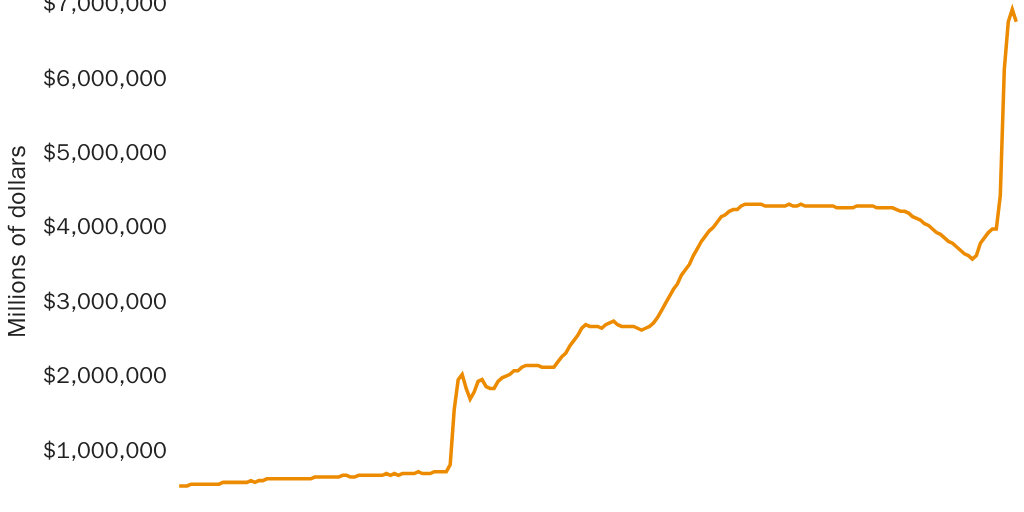

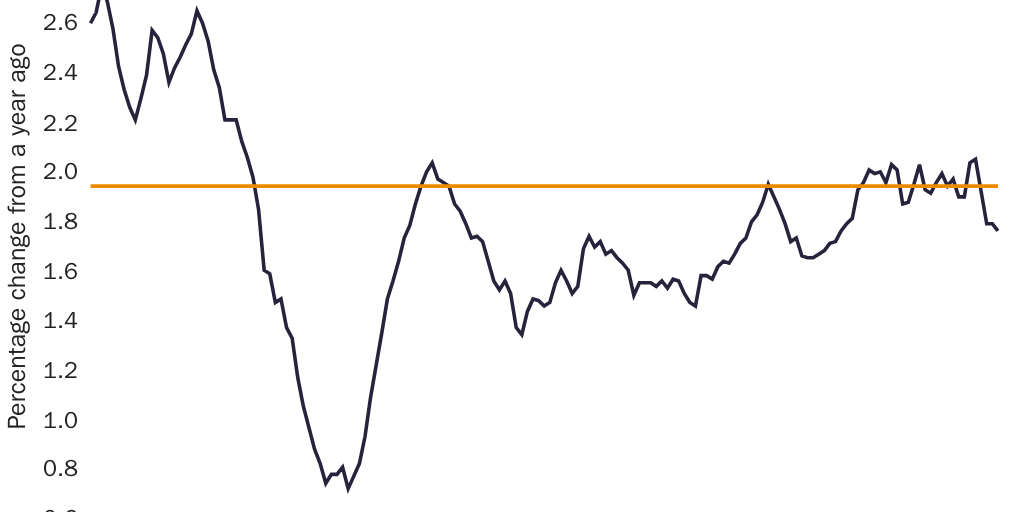

The size of the Fed’s balance sheet has expanded dramatically since 2008 (see Figure 1). Normally, such an expansion would be accompanied by a surge in nominal GDP and inflation. However, the Fed’s floor system has mitigated that effect: inflation has remained below the Fed’s 2 percent target, as shown in Figure 2. To get “more bang for the buck,” proponents of fiscal QE have called for the Fed to fund infrastructure, a Green New Deal, and pay off student loans. In this regard, Plosser warned that the Fed’s “independence is drifting away and after this [COVID-19] crisis, it will be easier and easier for politicians to seek Fed participation in off-budget fiscal actions.”

In 2001, J. Alfred Broaddus and Goodfriend proposed two rules to guide asset acquisition policy:

First, the Fed’s asset acquisitions should respect the integrity of the fiscal policymaking process by minimizing the Fed’s involvement in allocating credit across sectors of the economy. Second, assets should be chosen to minimize the risk that political entanglements might undermine the Fed’s independence and the effectiveness of monetary policy.

That was before unconventional monetary policies were introduced and before the Fed turned to Section 13 (3) to exercise its emergency lending authority to allocate credit to nonbanks. The Fed has made it clear that its balance sheet will not be normalized for a long time. Returning to “normal” would require shrinking the balance sheet and returning to an operating system that restores the link between the size of the Fed’s balance sheet and the stance of monetary policy.

Replace the Floor System

The floor system—in which the relationship between balance-sheet expansion and inflation is absent—depends on abundant reserves, an IOER that exceeds the opportunity cost of holding reserves at the central bank, and a commitment by the Board of Governors to administer both the IOER rate and the overnight reverse repo rate. If inflation were to exceed the Fed’s 2 percent target, the Board would have to increase IOER, which would mean remittances to the Treasury would fall. George Selgin provides a detailed discussion of the post-2008 operating system in his book Floored!

“Fiscal QE” occurs when Congress turns to the Fed for funding programs off budget. As Selgin writes in The Menace of Fiscal QE, this “is possible only because the Fed’s floor system allows it to resort to QE [i.e., large-scale asset purchases] without losing control of inflation.” According to Selgin, returning to a so-called corridor system “would guard against fiscal QE by constraining the size of the Fed’s balance sheet.”

The main aim of monetary policy should be to ensure a stable growth path for nominal GDP, not to engage in credit policy or serve political ends. If markets expect the Fed to support asset prices, and Congress expects the Fed to satisfy special interests, the Fed’s independence and credibility will be at risk.

Resist Yield Curve Control

Government spending and the fiscal deficit have mushroomed because of the COVID-19 pandemic and subsequent lockdowns. If inflation and nominal interest rates increase, the cost of servicing the federal debt would put a big strain on taxpayers. During the Second World War, the Treasury and Fed agreed to support the prices of government bonds by pegging interest rates at artificially low levels. That policy continued until the 1951 Treasury-Fed Accord.

Today, the idea of yield curve control (YCC)—that is, pegging rates at low levels to support government securities and lower financing costs—is gaining attention. The Bank of Japan has been using YCC for some time, and the Reserve Bank of Australia adopted it in early 2020. Since U.S. rates on 10-year Treasury securities are already low, there may not be much to gain from reverting to YCC, and Fed Chairman Jerome Powell does not appear to be in any hurry to do so.

The Fed should actively resist YCC, although that may be difficult if there is increasing pressure from Congress and the Treasury to do so. Those who lean toward yield curve policies should consider the risks, the major one being that “they put the central bank’s credibility on the line,” according to Sage Belz and David Wessel of the Brookings Institution. That is, if the Fed promises to peg rates, it runs the risk of straying from its inflation target.

Other risks include the following:

- When central banks peg rates (by supporting the prices of government bonds) and try to control the yield curve, investors are incentivized to search for yield by moving to longer‐term securities. This shift increases duration risk—that is, when the economy starts to recover and interest rates rise, holders of longer‐term securities suffer large losses. (When the Fed buys a Treasury security, its market price increases, which means its yield decreases.)

- By engineering lower rates and promising to keep them low for several years, the central bank encourages politicians to continue to run fiscal deficits.

- Pegged rates also distort the allocation of credit by diminishing the role of private markets. Placing legal ceilings on interest rates (i.e., not allowing them to rise above the maximum rate targeted by the authorities)—and thus supporting bond prices—is not a magic wand for creating a robust economy.

- Once rates are pegged at artificially low levels, they can be difficult to exit.

- YCC would further politicize central bank policy, diminish independence, and harm credibility. If inflation increases, there is the danger of broader price controls, as in 1971, which would harm personal and economic freedom and slow economic growth.

In fighting the COVID-19 pandemic, policymakers should not lose sight of the adverse consequences of pegged rates.

The pandemic was not the fault of central banks, nor was the political decision to lock down the economy that contributed to putting millions of people out of work. In such a situation, the Fed and other central banks had to provide liquidity to prevent financial instability from further damaging the real economy.

Yet unconventional monetary policies are meant to be temporary. Ensuring long‐run economic growth necessary to restore economic well-being will require adapting to new realities via markets, not manipulating interest rates to finance government deficits and providing cheap credit to favored groups.

Featured Video

Consider a Rules-Based Monetary Regime

The Fed and Congress should think about the future of monetary policy and the steps needed to normalize Fed policy so that when the pandemic ends, plans will be in place to ensure monetary stability and robust private credit markets.

Market participants now expect the Fed to support an array of asset prices—and any deviation from that policy is bound to have dire consequences. Normalization, therefore, will be difficult. An important step in getting the Fed to end its intervention in credit markets—and avoid moral hazard (i.e., underpricing risk)—would be for policymakers to end their “historic aversion to commitment and rules,” according to former Richmond Fed economist Robert Hetzel.

Congress and the Fed should consider moving toward a rules-based monetary system (e.g., one that keeps nominal GDP on a level growth path, as proposed by Scott Sumner and David Beckworth). Forward guidance based on a sound monetary rule would be superior to the current discretionary monetary regime.

Although the Fed can help smooth the path of nominal income, it cannot permanently increase wealth or real economic growth by manipulating interest rates. Monetary policy should be divorced from credit policy and fiscal policy, which means depoliticizing the Fed. Private markets, not the Fed, should allocate credit.

Independence would be more secure, and monetary policy more predictable, the more the Fed is guided by a credible rule, rather than by pure discretion in a fiat money world. The Fed should work with Congress to establish a monetary commission to examine the boundary line between monetary and fiscal policy and consider the case for adopting a monetary rule.

Conclusion

Maintaining distance between monetary and fiscal policy is a key condition for Fed independence and credibility. When the Fed extends its reach by allocating credit and engaging in fiscal QE, it sets a dangerous precedent. Instead of Congress making difficult fiscal decisions, politicians turn to the Fed for help. To prevent the drift into fiscal space, there needs to be a bright line drawn between monetary and fiscal policy. Adopting a rules-based approach to the conduct of monetary policy would help safeguard central bank independence and promote both monetary and financial stability.

About the Author

This work is licensed under a Creative Commons Attribution-NonCommercial-ShareAlike 4.0 International License.