For some time, the flavor of the day has been “green.” Indeed, companies around the world are scrambling to go green. Some are so desperate that they engage in “greenwashing.” This practice amounts to little more than the use of public relations campaigns to assert greenness. McDonalds, for example, literally became green by changing the colors on its signature logo. Now, McDonalds’ classic yellow “M” is displayed with a green, not a red, background. That said, many companies are, and have been, engaged in producing products and employing production processes that, by any definition, would qualify as green.

Just how large is the green investment space? Well, it’s large, and it’s growing rapidly. For example, the FTSE4Good, which is a sub-index of London’s FTSE, has the largest market capitalization of any of the green equity indices. At the end of May 2017, the global FTSE4Good’s market capitalization stood at a whopping $20.9 trillion. That’s somewhat larger than the current GDP of the United States &mdashl $19.0 trillion.

With investors favoring green, and investment flows being earmarked as green, an obvious question arises: “How does an investment qualify for the coveted green designation?” The current methods used to measure green and qualify an investment as “green” fail to meet rudimentary standards of measurement. The most basic principal of measurement is replication. But, the current methods are, for the most part, subjective and opaque. They are “black boxes,” yielding results that can’t be replicated. This leaves a multi-trillion dollar green investment house wobbling on stilts, rather than a sound foundation.

In order to firm up the green investment house’s foundation, Dr. Heinz Schimmelbusch, Founder & CEO of the Advanced Metallurgical Group (where I am a member of the Supervisory Board), and I have developed a methodology that is simple, transparent, and replicable. Our metric is determined by starting at the origin of the supply chain. It is from that starting point that we measure the amount of greenness ultimately enabled by the production of a so-called green enabler.

For example, the reduction in CO2 is a green good. If a company produces graphite that enables the production of more efficient insulation, which results in lower demand for energy required for heating and cooling, then the graphite producer is a net supplier of a green good – the net reduction in CO2. In short, the enabler of the production of the green good is the supplier of graphite. So, the source of greenness resides at the very beginning of the supply chain. When it comes to the measurement of greenness, this enabling notion leads to simplicity and transparency, as well as an objective measure of the amount of greenness associated with each supplier that is enabling the production of green goods.

To operationalize the enabling concept in the context of CO2 emissions, the following transparent and replicable formulation for measuring greenness with precision can be used:

The enabling greenness ratio is simply the net CO2 reduced by a company divided by the level of a company's invested capital. Because this metric is divided by a company's total assets, it provides net CO2 reduction relative to a company's size. This is analogous to the traditional accounting measure – return on assets.

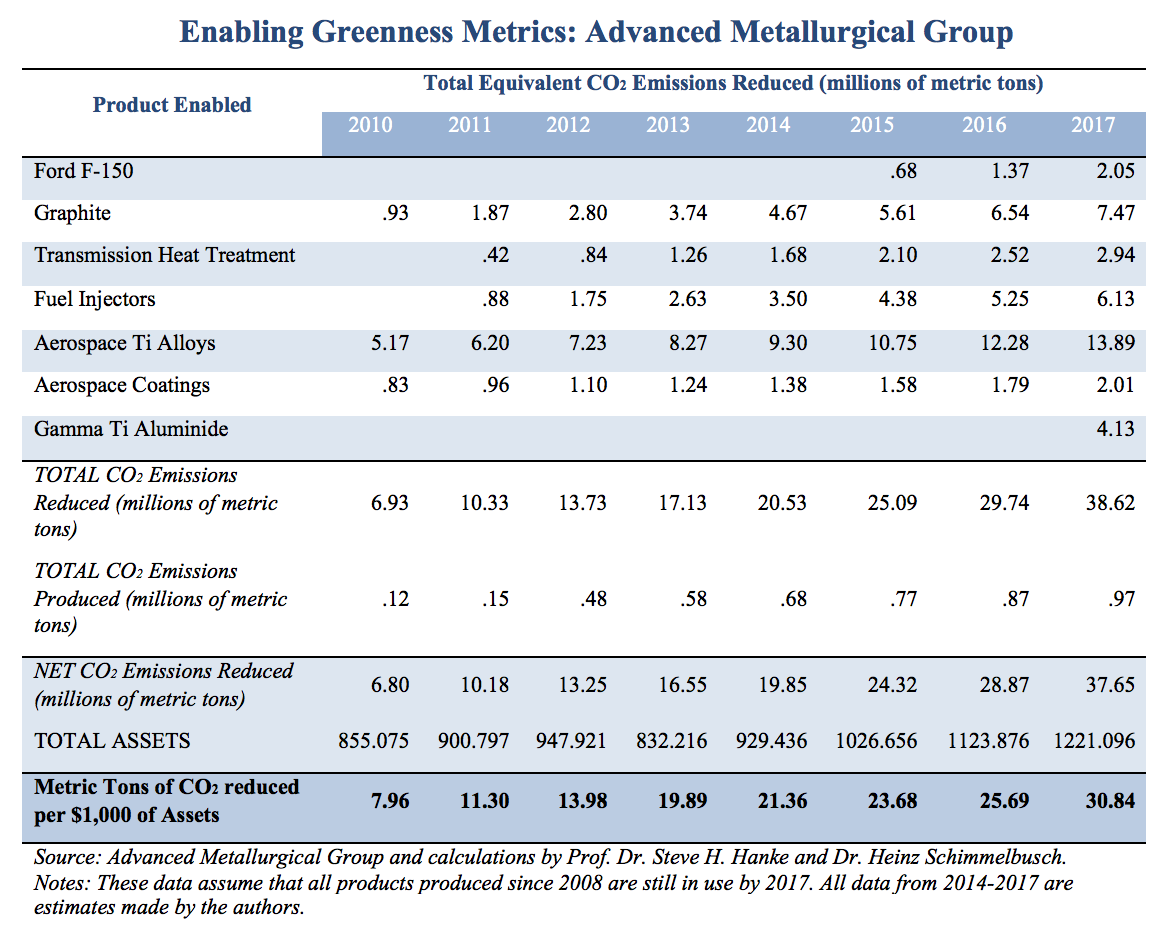

Our suggested methodology can be applied with precision. We use the Advanced Metallurgical Group (AMG) to illustrate. The table below contains our results.

Over the past eight years AMG has produced products that have enabled an estimated net CO2 reduction of 157.47 million metric tons. Very green, indeed. And yes, there’s more; due to the cumulative nature of supplying raw materials that enable the production of green goods, AMG’s greenness enabling ratio soars over time – indicating that AMG’s green rate of return is growing rapidly.

About the Author