With the arrival of President Hugo Chávez in 1999, Venezuela embraced Chavismo, a form of Andean socialism. In 2013, Chávez met the Grim Reaper, and Nicolás Maduro assumed Chávez’ mantle.

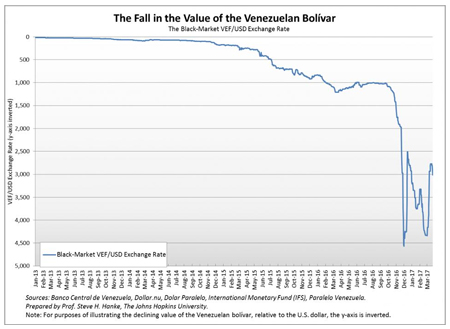

The Grim Reaper has also taken scythe to the Venezuelan bolivar. The death of the bolivar is depicted in the following chart. A bolivar is worthless.

{kind=link}

The fall in the value of the Venezuelan bolivar

With the collapse of a currency comes inflation. By the time President Nicolás Maduro arrived, inflation was in triple digits and rising.

With the acceleration of inflation, the Banco Central de Venezuela (BCV) became an unreliable source of inflation data. Indeed, from December 2014 until January 2016, the BCV did not report inflation statistics. To remedy this problem, the Johns Hopkins-Cato Institute Troubled Currencies Project, which I direct, began to measure inflation in 2013.

The most important price in an economy is the exchange rate between the local currency and the world’s reserve currency — the U.S. dollar. As long as there is an active black market (read: free market) for currency and the black market data are available, changes in the black market exchange rate can be reliably transformed into accurate estimates of countrywide inflation rates. The economic principle of Purchasing Power Parity (PPP) allows for this transformation.

I compute the implied annual inflation rate on a daily basis by using PPP to translate changes in the VEF/USD exchange rate into an annual inflation rate. The chart below shows the course of that annual rate, which peaked at 800% (yr/yr) in the summer of 2015. At present, Venezuela’s annual inflation rate is 150%, one of the highest in the world (see the chart below).

{kind=link}

Venezuela's annual inflation rates

To stop Venezuela’s death spiral, it must dump the bolivar and adopt the greenback. This is called “dollarization.” It is a proven elixir. I know because I operated as a State Counselor in Montenegro when it dumped the worthless Yugoslav dinar in 1999 and replaced it with the Deutsche mark. I also watched the successful dollarization of Ecuador in 2001, when I was operating as an adviser to the Minister of Economy and Finance.

Countries that are officially dollarized produce lower, less variable inflation rates and higher, more stable economic growth rates than comparable countries with central banks that issue domestic currencies. Dollarization is, therefore, desirable. The chart below shows the normalized values of real GDP in terms of U.S. dollars between 2001 (index value = 100) and 2016 for nine Latin American countries. Three — Panama, Ecuador, and El Salvador — are officially dollarized, while Peru is semi-officially dollarized (read: both the Peruvian sol and USD are legal tender). In the three officially dollarized countries, real GDP growth has been more stable than and generally superior to growth in the countries that issue their own domestic currencies.

{kind=link}

Dollarized vs. Undollarized Latin American GDPs

So, not all the news from Venezuela is grim. After all, there is a tried and true way to stabilize the economy, which is a necessary condition required before the massive task of life-giving reforms can begin. It is dollarization.

Just what does the Venezuelan public think of the dollarization idea? To answer that question, a professional survey of public opinion on the topic was recently conducted by Datincorp in Caracas. The results are encouraging. Sixty-two (62%) of the public favors dollarization. It's time for enlightened, practical politicians in Venezuela to embrace the dollarization idea. The public already does.

About the Author