Ever since the Federal Reserve began to consider raising the federal funds rate, which eventually it did in December 2015, a cottage industry has grown around ‘taper talk’. Will the Fed raise rates or not? Each time a consensus congeals around the answer to that question, all the world’s markets either soar or dive.

This obsession with taper talk — the interest rate story — is simple, but strange. Indeed, it is misguided — wrongheaded. So, why the obsession? It is, in part, the result of a Keynesian hangover. The Keynesians focus on interest rates. The mainstream macro model that is widely in use today is referred to as a ‘New Keynesian’ model. The thrust of monetary policy in this model is entirely captured by changes in current and expected interest rates. However, money is nowhere to be found. And it is not just the New Keynesian model that is defective. Money and credit do not fit into the general equilibrium model, which requires a pure barter economy.

This interest rate obsession is amazing, particularly since Keynes dedicates quite a few pages in A tract on monetary reform (1923) to money and its role in national income determination. Then, in his two-volume 1930 work, A treatise on money, Keynes devotes a great deal of space to banks and their important role in creating money. In particular, Keynes separates money into two classes: state money and bank money. State money is high-powered and is produced by central banks. Bank money is produced by commercial banks through deposit creation.

Keynes spends many pages in A Treatise on money dealing with bank money. This is not surprising because, as Keynes makes clear, bank money dominated state money in 1930. Not much has changed since then. Today, bank money accounts for almost 82% of the broad money supply (M4) in the UK.

We should scrutinise money broadly measured (state plus bank money) and money properly measured (when available, Divisia, not simple sum measures). A monetary approach to national income determination is what counts over the medium term. The link between growth in money supply and nominal GDP is unambiguous and overwhelming.

Since the collapse of Lehman Brothers in 2008, there has been a dramatic change in monetary policies around the world. Bank regulations have been tightened, and supervision has become much more severe. Large-scale bank recapitalisations and deleveraging have become the order of the day. These policies, which affect the production of bank money, have been ultra-tight and procyclical.

In an attempt to expand the total supply of broad money, many central banks have had to engage in quantitative easing (QE). This state money policy is ultra-loose and countercyclical. However, broad money has been growing slowly in many countries, as state money accounts for a relatively small portion of broad money. In consequence, nominal GDP growth has come in below its trend rate.

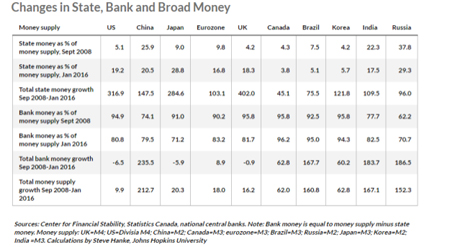

The accompanying table shows the changes in state money, bank money, and broad money for the 10 largest economic regions in the world. The US, Japan, eurozone, UK and South Korea lead the field in terms of QE. All have ramped up their production of state money. This can be observed by noting that the proportion of state money to broad money jumps up from September 2008 to January 2016 in these countries. For China, Canada, Brazil, India and Russia, the picture is different. The share of state money to broad money declined, indicating that they did not engage in QE.

{kind=link}

When we look at bank money, the situation in the US, Japan and the UK has been stunning. For these countries, the amount of bank money in the economy was lower in January 2016 than in September 2008, showing tight bank money policies. It is not surprising that the US, Japan and the UK embraced QE early in the game. If they had not done so, the growth in broad money would have been much more anaemic than it was, resulting in deep recessions.

The eurozone arrived at the QE party a bit late, but it arrived nevertheless. Now, European Central Bank (ECB) president Mario Draghi and QE face a wave of criticism. Many in Germany, for example, oppose QE. Many even argue that the ECB is out of ammunition. This is nonsense. As long as a central bank purchases assets from the non-bank public, broad money and nominal GDP will grow.

To say that money and monetary policies are misunderstood is an understatement. Populist bankbashing rhetoric by politicians and new financial regulations are weighing down the growth of bank money and economic activity.

About the Author