During my testimony last week before the U.S. House of Representatives Committee on Foreign Affairs, I stressed that, to establish stability and turn Venezuela’s economy around, runaway inflation must be stopped in its tracks. After all, stability might not be everything, but everything is nothing without stability.

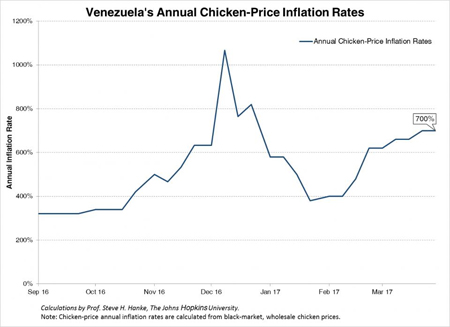

To grasp the magnitude of Venezuela’s inflation problem, take a look at the chart below. It shows the annual inflation rates (yr/yr) for chicken. Venezuela’s current chicken-price inflation is running at a whopping 700% annual rate.

{kind=link}

Venezuela's Annual Chicken-Price Inflation Rates

A New York Times editorial Thursday, “Crisis Upon Crisis in Venezuela,” picked up on my “stop inflation first” elixir. As the Times put it: “the international community could propose specific macroeconomic reforms that could curb Venezuela’s runaway inflation and stabilize its currency.”

The Times failed to offer a specific inflation-killing strategy, however. There are only two sure-fire ways to kill Venezuela’s inflation and establish the stable conditions which are necessary to carry out much-needed economics reforms. One way would be to dump the bolivar and officially dollarize the economy, an option I covered in a Forbes piece Thursday, “On Venezuela’s Death Spiral.”

A second method would be to adopt a currency board system. In such a system, the bolivar would become a clone of a reliable anchor currency, such as the U.S. dollar.

Just what is a currency board? An orthodox currency board issues notes and coins convertible on demand into a foreign anchor currency at a fixed rate of exchange. As reserves, it holds low-risk, interest-bearing bonds denominated in the anchor currency. The reserve levels (both floors and ceilings) are set by law and are equal to 100%, or slightly more, of its monetary liabilities. A currency board generates profits from the difference between the interest it earns on its reserve assets and the expense of maintaining its liabilities.

A currency board’s operations are passive and automatic. The sole function of a currency board is to exchange the domestic currency it issues for an anchor currency at a fixed rate. In consequence, the quantity of domestic currency in circulation is determined solely by market forces, namely the demand for domestic currency.

A currency board cannot issue credit. It cannot act as a lender of last resort or extend credit to the banking system. It also cannot make loans to the fiscal authorities and state-owned enterprises. In consequence, a currency board imposes a hard budget constraint and discipline on the economy.

A currency board requires no preconditions for monetary reform and can be installed rapidly. Government finances, state-owned enterprises, and trade need not be already reformed for a currency board to begin to issue currency.

Countries that have employed currency boards have maintained currency convertibility and delivered lower inflation rates, smaller fiscal deficits, lower debt levels relative to GDP, fewer banking crises, and higher real growth rates than comparable countries that have employed central banks.

It is important to mention that the currency board idea became engulfed in controversy — thanks to Argentina. What Argentina termed “Convertibility” was introduced in April 1991 to stop inflation, which it did. The system had certain features of a currency board: a fixed exchange rate, full convertibility, and a minimum reserve cover for the peso of 100% of its anchor currency, the U.S. dollar. However, it had two major features which disqualified it from being an orthodox currency board. It had no ceiling on the amount of foreign assets held at the central bank relative to the central bank’s monetary liabilities. So, the central bank could engage in sterilization and neutralization activities, which it did. In addition, it could hold and alter the level of domestic assets on its balance sheet. So, Argentina’s monetary authority could engage in discretionary monetary policy, and it did so aggressively.

Because of these flaws, I penned an article which appeared in the October 25, 1991 edition of the Wall Street Journal. I concluded that, unless Argentina embraced orthodoxy and amended the Convertibility Law, the system would eventually collapse, which it did in 2002.

The collapse of Convertibility spawned a cottage industry of currency board critiques. But, since Argentina’s Convertibility System allowed for both monetary and exchange rate policies, it was not a currency board – something most economists failed to recognize. Indeed, a scholarly survey of almost 100 leading economists who commented on the Convertibility System found that almost 97% incorrectly identified it as a currency board system. So, those that used the collapse of Argentina’s Convertibility System to argue against currency boards literally didn’t know what they are talking about.

Just what can the international community do to shine a light on the currency board solution for Venezuela’s runaway inflation? For me, the answer harks back to 1992. That’s when I worked with the then-leader of the U.S. Senate, Bob Dole, and Senators Steve Symms and Phil Gramm, to draft U.S. legislation that would encourage countries with unstable currencies and runaway inflation to install currency boards. This legislation, (HR-5368, Law no. 102–391), was signed into law on October 6, 1992.

About the Author