Conventional wisdom seems to hold that the world is moving faster and faster — that the pace of innovation is accelerating. And why not? The digital surge since 2007, when the first iPhone was released, has had a visible impact on the way we live our lives. New scientific discoveries leave us in awe. Driverless cars are arriving on our roads, drones delivering goods will soon fly over our heads. Advanced surgery can be done by robots, monitored by remote surgeons, and the revolution in robotics has just begun to reshape how the service sector is organized. And then there is modern medicine. Biomedical innovation has turned diabetes, heart disease, and HIV into chronic diseases rather than a death sentence. There are close to 1,000 new cancer drugs using frontline genomics in clinical development, many of which will be far more powerful fighting tumors and metastases than existing drugs and chemotherapy. By 2030, say some geneticists, the world will have cured cancer.

Yet for all the impressive results of science, why are we still talking about curing cancer in the future? Why aren’t we curing it now? Why did we not cure it 30 years ago? Cancer has been a known cause of death for several hundred years. Its genetic source was discovered more than a century ago. The “war on cancer” did not begin with President Nixon’s famous National Cancer Act in 1971, but with the creation of the American Cancer Society in 1913. True, cancer is a very complex cellular disease, and several recent reports suggest that scientists have made critical breakthroughs to find better ways to treat it. But it is impossible to be impressed by the speed of cancer treatment when we are burying more people than ever because of the disease.

Frustration with the slow progress of innovation shouldn’t stop with medical science. The slowdown of innovation is a much broader problem — and a growing one. It has nothing to do with limits to human ingenuity but rather reflects the flaws in the type of capitalism that has evolved in the West over the past 40 years. The great value of innovation is not merely in invention but rather diffusion and adaptation. And real innovation requires an economy that runs on the culture of experimentation and is open to innovators and entrepreneurs contesting markets — challenging incumbents to such a degree that it redefines the market (like Apple’s iPhone did with the handset market in 2007). In the past decades, however, these forces of diffusion and adaptation simply have not been powerful enough; in fact, legislators have acted to shield incumbent businesses from them. Now the existential challenge that capitalism faces is the growing resistance to innovation.

That was not what Joseph Schumpeter, a great theorist of innovation, sketched in his 1942 book Capitalism, Socialism and Democracy. Like Karl Marx, Schumpeter had a firm belief in the innovative capacity of capitalism. The capitalist system, wrote Schumpeter, was a “perennial gale of creative destruction.” In the end, however, it would become a casualty of its own success: capitalism would innovate itself to death. “Capitalism,” Schumpeter argued, “is being killed by its achievements.” Schumpeter came to regret his apocalyptic view of the economic and social fabric of innovative capitalism, yet now his dystopian vision has been given new life with warnings that innovative capitalism will put millions of workers in the developed world out of work.

It has long been known that robots can replace muscle and manual labor. But now, we are told, they are “coming to an office near you,” as the cover of The Economist magazine recently put it. Smarter, stronger, and more adaptive than white-collar graduates, the robots will put office workers out to pasture. Those of us with a college education are now at risk of losing our jobs because of artificial intelligence, supercomputers, and other innovations that will steal our jobs. It is not surprising, therefore, that studies have shown Americans fearing robots more than death.

The prophecy is wrong, however — and that’s not good news. It would be great if the West were on the threshold of a new age of fast-and-furious innovation, because that would boost the economy and give everyone new economic opportunities. Our economy, however, does not encourage innovation, experimentation, and competition as much as it should, and could. If you consider what political and corporate leaders are up to, the Western economy is not preparing for an innovation feast but an innovation famine. Companies doubt there is a payoff from investment in radical innovation — and political leaders refuse to recognize that more and faster innovation requires radical changes in regulation and government behavior.

THE GREAT SLOWDOWN

For too long, Western economies looked like high-growth societies because they made use of more and more labor and capital at home and abroad. In the last 40 years, net labor inputs grew as a result of an increasing working-age population and higher rates of female labor-market participation. The boost from labor was so strong that economists in the Obama White House have called its initial phase “the age of expanded participation.” Net capital inputs also expanded remarkably fast, first through an emerging and, later, an accelerating “debt supercycle” — the extraordinary expansion of public, corporate, and private debt that in large part made the economy grow because debt allowed states, firms, and households to borrow and spend more money. Backed by governments that protected banks and financial firms from bankruptcy, the financial sector became the new master of the universe; there seemed no end to its ability to engineer new sources of capital. While savings increased in a few countries, such as Germany, they dropped in the majority of Western economies. In the United States, for instance, gross national savings fell from about 22 percent of GDP in 1970 to approximately 14 percent in 2010. Nonfinancial corporate debt-to-equity ratios have surged since 1970.

The richest economies — those at the frontier of innovation and productivity — found growth opportunities in emerging markets. Spurred by reforms at home that freed up trade and competition, companies managed to source inputs and goods from more efficient producers. The entry of a billion or more people, many of them Chinese or Indian, into global consumer and labor markets during the period of globalization was what economists call a big “supply shock.” In that way, Western economies could import sources of growth — they could improve their economies by trading more intensively — and for Europe, with declining domestic factors of growth, that help from the emerging markets was especially important. It accelerated a positive transition in the economy from lower-productivity to higher-productivity sectors.

But then the music stopped. It is almost a decade now since the West’s financial sector began to crumble. Yet America and Europe still show a stubborn resistance to recovery. Productivity growth has been very poor. While some economies like the United States have returned to the levels of output they had before the crash, others have been unable to rise above those levels. None of the Western economies have returned to the pre-crisis trend of GDP growth.

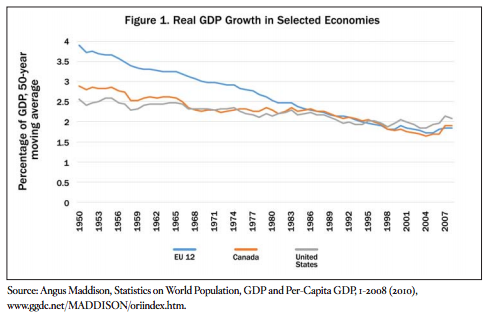

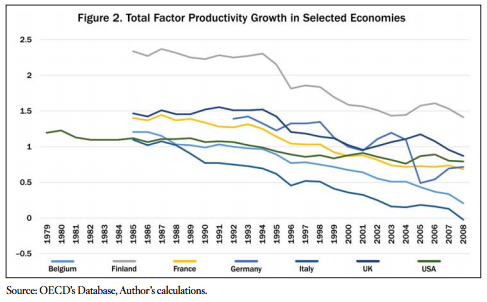

The stagnation, as Hemingway said of bankruptcy, came in two ways: gradually and then suddenly. The gradual stagnation is shown in two figures below, indicating the rate of economic growth and the rate of productivity growth over the past decades. Delineating the trend through moving averages, the charts show that the rate of value creation in the economy has declined over a longer period of time and that innovation is not powering the economies at previous rates.

SOURCES OF DECLINE

In our view, the gradual decline is a direct consequence of capitalism getting increasingly constrained. Several factors have conspired to weaken the spirit of enterprise and creative destruction in the Western economy, and — perhaps paradoxically — not all of them have been undesirable. However, they make America and Europe less capable of supporting a new innovation boom. Let’s discuss two of the most pernicious factors — gray capitalism and excessive regulation.

Gray Capitalism

In the past 40 years, capitalism has lost its leading actor — the capitalist. Ownership of public companies has become obscured by the rapid growth of investment institutions managing other people’s money — predominantly savings for retirement. These institutions are today the main owners of Western public companies, and their role as the controlling owners has grown fast. Norway’s sovereign wealth fund, for instance, owns over 1 percent of all global equity. Private investment institutions are behaving much like public investment institutions. Corporate bureaucrats run them both.

Chicago economist Frank Knight made an important distinction between risk and uncertainty, and it is critical for understanding how capitalism has changed with the growing influence of third-party money managers. Most of the time, investment institutions and asset managers perform a valuable service for savers, but they are allergic to uncertainty and manage their ownership in accordance with the finance theory formula of risk.

Writing in the 1920s, Knight sketched the two different worldviews of risk and uncertainty. The first worldview is mechanical and sees human behavior as predictable. The second worldview, which Knight called organic cognition, however, is subject to change and new iterations for development. It is the mechanistic approach to the economy that dominates corporate thinking about risk. Uncertainty, however, is different in the sense that it cannot be contracted out: neither internally within a firm nor to the market. It is inherent in the partial and incomplete knowledge of an individual and an organization, making it impossible to reduce it to probabilities that can provide guidance. In the end, the only way to deal with uncertainty is through individual judgment, and in a firm that judgment cannot be diffused between different functions or management roles; it can only rest with the entrepreneurial owner. Responsibility for and control of firms are inseparable, and the greater the distance between a firm and its owners, the more its capacity to deal with uncertainty shrinks.

Innovation and long-term investments are intimately linked to uncertainty, and the capacity of a firm to work with uncertainty. Savers and investment institutions that prefer predictability are reluctant to invest much in enterprises with innovative ambitions, even if they are not particularly bold. Under current macroeconomic conditions of low interest rates they even have problems investing in companies with modest innovation ambitions. They prefer cash-strong companies that can compensate for falling profits by using the liquidity for dividends and share buybacks.

In recent years, many companies have been aging their assets base by investing too little and returning capital to shareholders. Unfortunately the trend is not new. The ratio of business investments to cash to shareholders (dividends and share buybacks) has fallen in the United States and elsewhere for several decades — and that trend is partly linked to the growing role of investment institutions in corporate ownership. Capitalism without capitalists behaves differently from capitalism with capitalists.

Regulation

It is a myth that Western economies have been on a multi-decade journey of market and business liberalization. The United States experienced a wave of deregulation in the late 1970s and early 1980s. Europe turned to freeing up markets about a decade later. However, for the past 15 years, governments have increasingly intervened in the economy. Regulatory interference in trade, for instance, has increased continuously. Labor markets have become increasingly protected as well, not necessarily through classic hiring-and-firing legislation but the rapid rise of professions covered by occupational licenses.

Economic regulation reduces the scope for innovators and entrepreneurs to experiment and contest markets. Yet perhaps even more detrimental to innovation has been the rise of social regulations (e.g. environment, consumer, and health protection) and how they increasingly interfere with potential innovation. Product regulations in areas like medicine and medical devices have not just raised the cost of innovation, but created uncertainty about the chances of new innovations to be approved by authorities. Such uncertainty is toxic for company managers — and especially managers with owners who demand a high degree of predictability.

Consider the use of the “precautionary principle” in European legislation. It is used for many different purposes, but no one knows what it really entails for regulation. A classic example is how it has destroyed the ambitions of biotechnological firms to innovate in the field of genetically modified organisms: both approvals and rejections of a genetically modified crop cite the precautionary principle. Another example is how chemical firms have reduced their innovation investments because they have spent a decade conforming to a 2006 regulation — based on the precautionary principle — on the evaluation and authorization of chemicals that have been on (and approved for) the market for decades.

Western regulations are getting ever more complex — and with the accumulation of regulations, the regulatory landscape facing innovators is ever more opaque. Such regulations hurt innovators and entrepreneurs that aspire to contest markets. Start-ups find it ever more challenging to manage political risks and investors shy away from new innovations that face an unclear legal territory. Take drones as an example. The technological challenges facing drone manufacturers and users are less daunting to many investors than unclear legal circumstances. Large firms have problems too, but their understanding of regulation — and their capacity to use it for competitive purposes — has become a new incumbency advantage, protecting firms against competition.

CONCLUSION

There are other forces and events shaping capitalism — and making it increasingly constrained. Sometimes these were desirable, or even innocent, but as they progressed and were enforced by each other, capitalism changed its character and is now different from its textbook version. These factors now need urgent attention and capitalism in the West needs to be reconstructed to generate more innovation and new economic opportunities. In the current debate, new technology is often blamed for squeezing the middle class. It is often argued that recent innovation has caused incomes to stagnate and employment opportunities to be reduced. In our view, that analysis is completely wrong. The West’s economic illness is due to too little innovation and creative destruction — not too much.