Almost anyone can buy shares in a public company. However, the regulatory requirements for making a public securities offering can be expensive and time-consuming, and require the company to meet extensive disclosure requirements. As a result, many companies prefer to raise capital through “private offerings.” In recent years, public offerings have dwindled and private offerings have increased.

But investment in private offerings is overwhelmingly restricted to company insiders, institutional investors, and wealthy individuals. Indeed, the Securities and Exchange Commission’s “accredited investor standard” effectively means that only those with at least $1 million in assets or $200,000 in annual income can participate in private offerings. The result of these changes in the composition of the securities markets combined with existing regulation is that most Americans are increasingly cut off from investment opportunities.

The existing regulatory approach assumes that private offerings are uniquely risky, that wealthy investors are more financially sophisticated and better able to withstand a loss than ordinary Americans, and that only the well-off can access the information they need to make wise investments in private securities markets. However, these assumptions do not withstand scrutiny: public offerings can be risky too; wealth isn’t necessarily a good proxy for sophistication; and many concerns about access to information belong to a pre-internet age.

More fundamentally, excluding retail investors from the private securities markets establishes a troubling precedent by making it the prerogative and duty of the federal government to protect individuals from the choice to take certain kinds of financial risk. Why should this be the case in private securities markets when such government intervention is deemed unacceptable in other spheres of economic life?

A better approach would open investment in all offerings to all investors. “Registered” offerings could retain the disclosure requirements and other investor protections that currently exist for public offerings, while “unregistered” offerings could come with a mandatory disclosure of the protections a would-be investor must forgo. Ultimately, it should be up to individual investors to decide what investments are right for them.

Introduction

Downtown Washington, D.C., has a new shopping center. It is lined with boutiques selling labels seen only in the wealthiest closets: Gucci, Ferragamo, and Hermès. Although few Americans have $3,000 to spend on a pair of crocodile-skin loafers, most would assume that if they had such a windfall and wanted nothing more than a pair of Italian reptile-clad shoes, they would soon be walking out the shop door, Gucci shoebox in hand. And they would be right. Most of the time, one person’s cash is just as acceptable as the next person’s. Having cash in hand is good enough for any purchase one might wish to make.

Federal securities laws do not adhere to this principle, however. Although almost anyone is permitted to buy shares in companies that have conducted a registered public offering, the private securities markets are far more exclusive. Indeed, participation in the “private” sale of securities is overwhelmingly restricted to company insiders, institutional investors, and wealthy individuals. A categorical restriction on what some people may buy with their money is never a good idea, but as public offerings have dwindled in recent years and private offerings increased, the effects on average investors have become increasingly problematic.

What Are Private Offerings?

The distinction between public and private securities markets stems from the original federal securities law, the Securities Act of 1933. That act requires that whenever an issuer sells securities, both the offering and securities themselves must be registered with the federal government through the Securities and Exchange Commission (SEC). However, that registration process is onerous, and Congress understood from the beginning that it risked making some legitimate offerings uneconomic. So Congress included in the Securities Act certain exemptions, which in limited circumstances would allow issuers to sell securities without registering them. One such exemption was for sales “not involving any public offering.” Thus, the private securities market was born.

Today, so-called private offerings provide considerable capital to America’s corporations. Indeed, given certain market trends away from public offerings, the importance of private offerings has only increased in recent years.1 In some parts of the economy, almost all securities offerings are private: very new start-up companies rely heavily on private offerings, for example, and almost all early-stage investment—whether from venture capital firms or so-called angel investors—takes place in private.2

In some cases, private offerings appeal to issuers precisely because they are private. Public companies must divulge their financial health, executive compensation, business strategies, and many key trade secrets to the public, thereby exposing that information to competitors. As the scope of disclosure requirements has widened over the years—sometimes in an arbitrary or politicized fashion—more and more companies have preferred to avoid the glare of public registration.

It may also be the case that the increasing reliance on private offerings is due at least in part to the financial cost of the public alternative. To register an offering with the SEC, a company will typically need a team of lawyers and accountants to prepare the necessary documentation and to ensure that it meets the SEC’s exact specifications. The costs of satisfying these requirements can run well into six figures and beyond, and the process can take months to complete. For a company that is looking to raise only a few million dollars, the expense and delay are often prohibitive.

Whereas private offerings may be the right choice for small companies—not every company must or should be a public one—this isn’t just about small companies. Because it is legally possible to raise unlimited sums through private offerings, large corporations have increasingly come to rely on them as well. According to Dow Jones VentureSource and the Wall Street Journal, the number of private start-up firms valued at $1 billion or more increased from 32 in January 2014 (the first month with data available) to 103 as of January 2018.3 In fact, high profile private companies like Airbnb, Uber, and Spotify raised more than $1 billion in private offerings over the past few years.4 To put that in context, the median size for an initial public offering (IPO) in 2016 was about $95 million.5

Who Can Invest in Private Offerings?

The Securities Act of 1933 created the exemption from registration for securities sales “not involving any public offering,” but it did little to define exactly what that exemption meant. As a result, it was initially left to the courts to decide what would qualify. In the early days, courts seemed to understand a private offering as one made only to a limited number of people, who were typically known to the securities issuer. As the 20th century wore on, however, both the courts and the SEC developed a new understanding of “private” offering—one that increasingly focused more on the nature of the investor than the offering itself.

That shift in emphasis will be explored in detail below, but the result was that by the 1980s, the concept of the private offering had evolved. Rather than ensuring that private offerings were genuinely “private” transactions, the authorities began focusing on the investors, attempting to ensure that only those who were “able to fend for themselves” could buy securities in the private market.

The law surrounding this interpretation of private offering was complicated, however, and often left companies unsure where they stood. In response to that perception, the SEC promulgated Regulation D in 1982, with the aim of providing clear guidance on what constituted a nonpublic offering.6 Regulation D effectively created a safe harbor for private offerings—that is, an offering will be deemed nonpublic as long as it is made in accordance with Regulation D, with no further administrative or judicial assessment needed.7

Under Regulation D, a company can raise an unlimited amount of money with no required disclosures if it offers its securities only to “accredited investors”—institutions and individuals with at least $1 million in assets (excluding their primary residence) or at least $200,000 in annual income (or $300,000 jointly with a spouse). By focusing on wealth or income, the SEC’s interpretation of private offerings has rendered them the private playground of elite investors. Venture capital, private equity, and hedge funds dominate the private securities markets.8 More pedestrian investors, such as mutual funds, also participate but are limited in the amount they can invest in these markets.

The Trouble with Regulation D

Regulation D has some benefits. By effectively providing a regulatory checklist to issuers and their lawyers, Regulation D makes it easy for a company to know whether its offering is exempt from registration. By removing any cap on the number of investors and size of the offering, it allows companies to raise large amounts of capital with relative ease.

Nevertheless, there are three major problems with Regulation D. First, it has in practice acted as a kind of safety valve, allowing companies to escape the onerous requirements of the public markets while still raising capital. That might be good for business, but it is bad for public policy. The Regulation D safety valve essentially removes much of the pressure lawmakers might otherwise be under to implement beneficial regulatory and legislative reforms in the public markets.

Second, as much of the action in capital markets has moved to private offerings, retail investors have suffered. Unlike wealthy individuals, who are permitted to invest in private offerings, moderate- and low-income Americans are effectively barred by regulation, shutting them out from any potential opportunities the private markets provide. Having money in hand is not sufficient to invest in many of the more dynamic companies currently offering securities.

This exclusion becomes a more serious problem in light of concerns over wealth inequality. To return to the earlier example, lacking access to designer shoes has (at worst) no long-term effects on wealth. But lacking access to investment opportunities can. By effectively excluding middle- and lower-income individuals from many of the offerings in the market, the current regulatory regime limits the ability of such individuals to amass wealth, diversify holdings, and hedge certain risks. Not only does this reduce investment opportunities, it also risks artificially increasing the wealth gap between the richest Americans and everyone else.

Finally, the exclusion of retail investors from the private securities markets establishes a troubling precedent by making it the prerogative and duty of the federal government to protect individuals from the choice to take certain kinds of financial risk. Why should this paternalism be the case in private securities markets, when it isn’t in other spheres of economic life? This precedent is especially troubling given that the government’s private market paternalism has little empirical justification.

The Problem Restated

As regulation has increased in the public markets, more and more companies have opted to use private offerings. This shift to private offerings has siphoned a great deal of economic activity away from the public markets, where anyone can buy, to secluded markets that only a small subset of investors can access. The losers have been average investors who are overwhelmingly unaware, not only of the existence of private securities markets, but also of the regulation that effectively bars them from participation.

The following analysis begins with a detailed account of the evolution of the nonpublic offering exemption, moving from its origins in the Securities Act of 1933, through court rulings and the promulgation of various SEC regulations, to the predominance of Regulation D offerings today. Then, current regulatory reform proposals are explored, with a focus on broadening participation in the private securities markets. Finally, a better approach to the regulation of private offerings is outlined.

The good news is that the problems in private securities offerings could be fixed without legislative action. Congress has already granted the SEC the authority it needs to act. Ultimately, this analysis builds a case for the SEC abandoning the concept of the accredited investor altogether and replacing it with the approach that prevails in many other sections of the federal securities law—namely, that anyone with the financial means to invest should be allowed to do so. Additionally, abandoning the accredited investor concept would allow regulators to focus their activity on uncovering, punishing, and deterring fraudulent practices.

The History of the Nonpublic Offering

The private offering exemption established by the Securities Act of 1933 caused the SEC headaches almost from the beginning. Early documents suggest that the agency was itself grappling with what a nonpublic offering might be and simultaneously trying to provide clear guidance to the public and stamp out any ideas that conflicted with the agency’s own interpretation.

For example, a February 1935 report of the agency’s activities included “study and analysis of the problem involved in the so-called ‘private offering’ of securities, and methods of controlling the same.”9 In a speech a few days after that report was issued, SEC Chairman Joseph P. Kennedy implored his audience not to “seek refuge in so-called ‘private issues’ to a few purchasers and thus attempt to avoid registration.”10 He acknowledged the following:

During the early months of the Securities Act administration the opinion had been expressed in Washington that an offering of securities to an insubstantial number of persons was a transaction not involving any public offerings, and hence was exempted from registration under the Securities Act.… The guess was made that an offering to not more than 25 persons might be regarded as a private offering.11

But he assured attendees that “the mere number of prospective customers cannot be the sole determining of circumstance. It is one circumstance it is true, but there are others equally important, the number of units offered; the size of the offering and the manner of the offering.”12 Notably, among the harms he listed as arising from choosing a private offering over a registered public one was the fact that it would deprive the general public “of an opportunity to participate by investment in new and attractive offerings.”13 That is exactly what has come to pass in today’s market.

An earlier draft of the Securities Act had exempted from public registration all transactions by an issuer not involving an underwriter.14 There is a certain logic to this distinction. An underwriter acts as a distributor, buying securities from the issuer and then turning around to sell them. If the issuer knows a particular buyer or a small group of buyers willing to buy the entire offering, no underwriter is needed. The purpose behind engaging an underwriter is to reach potential buyers otherwise unknown to the issuer. If this language had remained in the statute, it might have made the distinction between public and private easier to understand. That it was removed suggests that the absence of an underwriter is not, on its own, sufficient to establish a nonpublic offering absent other evidence.

The earlier version of the statute also included an exemption for sales to current stockholders and for sales to employees of the issuers. These, too, were removed. The House Report stated that “[s]ales of stock to stockholders become subject to the act unless the stockholders are so small in number that the sale to them does not constitute a public offering.”15 That is, the buyers’ status as stockholders was irrelevant to the determination of whether the offering was public, but the number of buyers did matter. The exemption for employees was removed “on the ground that the participants in employees’ stock investment plans may be in as great need of the protection afforded by availability of information concerning the issuer for which they work as are most other members of the public.”16

Ralston Purina and Investor “Protection”

In 1953, the question of what constituted a “private” offering remained unsettled. The issue came before the U.S. Supreme Court for resolution in SEC v. Ralston Purina.17 The Court’s answer encapsulated an existing trend toward focus on the investor instead of the offering—and it set the tone for how private offerings would be evaluated going forward.

Between 1947 and 1951, Ralston Purina Company sold approximately $2 million in stock to a number of its employees. The stock was sold to “key” employees, a definition that encompassed a broad range of employees, including the following:

An individual who is eligible for promotion, an individual who especially influences others or who advises others, a person whom the employees look to in some special way, an individual, of course, who carries some special responsibility, who is sympathetic to management and who is ambitious and who the management feels is likely to be promoted to a greater responsibility.18

Ultimately the purchasers included a number of lower-ranked (and therefore lower-paid) employees. The offering was not registered with the SEC. Instead, the company relied on a belief that an offering just to its own employees could not be a public offering.

The Supreme Court disagreed. Instead of focusing on the nature of the offering itself, as the SEC had often done, the Supreme Court homed in on the investor, finding the following:

The design of the [Securities Act of 1933] is to protect investors by promoting full disclosure of information thought necessary to informed investment decisions. The natural way to interpret the private offering exemption is in light of the statutory purpose. Since exempt transactions are those as to which “there is no practical need for [the Act’s] application,” the applicability of 4(1) [the requirement that issuers register offerings with the SEC] should turn on whether the particular class of persons affected needs the protection of the Act. An offering to those who are shown to be able to fend for themselves is a transaction “not involving any public offering.”19

With this understanding of the purpose of the Securities Act and of the exemption from its requirements, the Court found that Ralston Purina’s offering was indeed a public offering. The company had several hundred employees throughout the country who were eligible to buy the stock. Crucially, although these employees worked for the company, they were not sufficiently close to upper management to have any significant advantage over the general public when it came to having knowledge about the company’s operations, strategy, or finances.

The SEC’s Interpretations

Although Ralston Purina attempted to determine what constitutes a “transaction . . . not involving any public offering,” the definition remained murky even post-Ralston. In 1962, the SEC issued a release intended to clarify the correct use of the private placement exemption. The relevant section of the Securities Act was intended, the release noted, to “provid[e] an exemption from registration for bank loans, private placements of securities with institutions, and the promotion of a business venture by a few closely related persons.”20 The increased use of the exemption for “offerings of speculative issues to unrelated and uninformed persons” prompted the SEC to issue the release in an attempt to “point out the limitations” on the exemption’s availability.21 However, the release simply stated that “[w]hether a transaction is one not involving any public offering is essentially a question of fact and necessitates a consideration of all surrounding circumstances, including such factors as the relationship between the offerees and the issuers, the nature, scope, size, type and manner of the offering”22—which is to say, a consideration of everything. This provided little guidance to those considering whether a planned offering would later be determined a public offering and therefore illegal if unregistered.

Beginning in 1974 and continuing through 1982, the SEC promulgated a series of rules intended to bring further clarity to the private offering exemption and promote small business capital formation. These rules continued on the path laid by Ralston Purina, focusing on protecting investors viewed as vulnerable. The new rules, however, went beyond Ralston Purina’s concern for investors who can fend for themselves and began to assess whether investors could afford a loss.

The SEC’s Rule 146 was one of the first attempts to define private offerings through regulation. It could be used by any issuer and had no limit on the amount an issuer could raise.23 Before Ralston Purina, courts had focused on the number of offerees, reasoning that an offering made widely and indiscriminately strongly suggested a public nature. Rule 146 followed this logic, restricting the offering to a total of 35 purchasers.

Rule 146’s chief innovation was the inclusion of a prototype “accredited investor,” restricting offers and sales to those who have “such knowledge and experience in financial and business matters that [they are] capable of evaluating the merits and risks of the prospective investment” or are individuals who are “able to bear the economic risk of the investment.”24 That is, there were two sufficient conditions: an investor had to be either sophisticated or able to bear the risk. To put it bluntly, a sharp poor person or a dull rich person was as eligible as a sharp rich person. The rule also required that offerees have access to or be provided with information that would have been included in a registration statement.

Yet Rule 146 failed to provide the stability the SEC had wanted. The SEC tried again in the late 1970s, issuing Rules 240 and 242.25 Rule 240 permitted companies with fewer than 100 beneficial owners (both before and after the offering) to raise up to $100,000 per year, but restricted advertising and solicitation.26 Rule 242 further developed the concept of the “accredited investor.” In addition to company insiders like directors and executives and certain entities, accredited investors were those individuals who purchased $100,000 or more of an issuer’s securities. Rule 242 permitted sales to up to 35 non-accredited investors; however, if the offering were limited to accredited investors, no specific disclosures were required. As with similar rules, Rule 242 prohibited general solicitation and advertising.

To introduce greater certainty into the process, the SEC promulgated Regulation D in 1982, and in the process repealed Rules 146, 240, and 242. Regulation D marries two related but statutorily distinct exemptions: the exemption for private placements and another exemption for small offerings. It includes several rules under which offerings may be made, but Rule 506 addresses the private placement exemption, providing a safe harbor for private offerings.27 Specifically, if an offering adheres to the requirements of Rule 506, it will be deemed to be a private one; it will not be subject to a separate inquiry as to its size, number of offerees, or any of the other factors otherwise used to determine private status.

It is important to note that this safe harbor is nonexclusive. That means that an offering that does not adhere to the requirements of Rule 506 may still be found to be private by the courts; the nonpublic offering exemption as a whole is broader than Regulation D, and issuers can still rely on the original legislative language and subsequent judicial interpretations if they prefer. In reality, however, issuers like the certainty that Regulation D’s safe harbor provides, and as a result the majority of today’s private offerings are conducted under the terms of Rule 506.28

Whereas Rule 506 closely mirrors the earlier Rule 146, it sweeps away the remaining pre-Ralston requirements for private offerings. Rule 506 firmly entrenches the notion that a private offering is distinguished by the sophistication and economic standing of its purchasers. Although Rule 146 introduced the concept of the sophisticated accredited investor, it also retained the pre-Ralston understanding of a private offering as one that is limited in size. Rule 506 includes no such limitations. As long as the offering is sold only to accredited investors, there is no limit on the number of offerees or number of purchasers.

Regulation D Today

The current version of Rule 506 contemplates two related types of private offerings. The first, known as Rule 506(b) offerings, comprises the original 1982 version of Rule 506 offerings. The second, Rule 506(c) offerings, reflects recent changes to the rule that were enacted through the Jumpstart Our Business Startups (JOBS) Act of 2012.29

Under Rule 506(b), an issuer may raise an unlimited amount of capital through the sale of any type of securities to any number of accredited investors. Accredited investors are defined as certain corporate insiders, large institutional investors, and individuals who meet certain wealth criteria. Although the sophistication of institutional investors has not been immune from scrutiny,30 it is the application of the definition to individual investors that has both caused the most mischief and attracted the most scholarly attention.31

Doing away with early formulations that relied on investors’ access to information about the issuer or their ability to leverage potential investment to obtain access, Regulation D’s accredited investor is defined by one characteristic: money. Individuals are considered accredited investors if they have at least $1 million in assets (excluding their primary residence) or at least $200,000 in annual income (or $300,000 jointly with a spouse). In the latter case, they must have earned that much in the past two years and reasonably anticipate earning the same amount going forward. The wealth criterion reflects a recent change in the law that has further constricted the pool of potential investors. Before 2012, a person who had $1 million in any assets qualified as an accredited investor. The 2010 Dodd-Frank Wall Street Reform and Consumer Protection Act, however, directed the SEC to change this rule to exclude the primary residence from the calculation. The new rule went into effect at the beginning of 2012.32 Because the family home is often a large portion of a household’s assets, this change had a considerable effect on the number of people who fit the definition of an accredited investor.

The issuer may also offer its securities to up to 35 non-accredited investors, provided that those investors are nonetheless “sophisticated.” The regulation deems non-accredited investors to be sophisticated if they, or their representatives (such as an adviser), “ha[ve] such knowledge and experience in financial and business matters that [they are] capable of evaluating the merits and risks of the prospective investment[.]”33 If the offering is made only to accredited investors, there is no requirement as to the disclosures that must be made to potential or actual investors. If, however, the securities are offered to even one non-accredited investor, the issuer must provide disclosures similar to those provided in a registered public offering. Given that issuers who opt to use this exemption are generally trying to avoid the cost and burden of producing the disclosures required of a registered offering, this requirement means that these offerings almost never include non-accredited investors.34

Rule 506(b) also includes a proscription on “general solicitation.” The rule states that general solicitation includes, but is not limited to, “any advertisement, article, notice or other communication published in any newspaper, magazine, or similar media or broadcast over television or radio; and. . . [a]ny seminar or meeting whose attendees have been invited by any general solicitation or general advertising.”35 This proscription applies even if no non-accredited person was exposed to the advertisement. Generally, if the issuer has a “preexisting and substantial relationship” with anyone to whom the securities are offered, the SEC will find that there was no general solicitation.

The result of both the broad definition of “offer” and the blanket prohibition on general solicitation for 506(b) offerings has been to restrict the ability of issuers to locate potential investors absent existing networks. Many issuers turn to brokers to serve as intermediaries, but this can freeze out smaller issuers because brokers may not find such offerings sufficiently profitable to merit their attention. For smaller companies, the ability to tap individual investment through the private placement exemption may be the key not only to growth but also to survival. Any changes to regulation that increase the pool of investors stand to benefit not only the investors themselves, but also the issuers who rely on private offerings. Given the current limitations on the pool of potential investors, those who are able and willing to invest in small companies wield considerable power over both the companies themselves and the consumers who may be interested in the products or services the companies wish to sell. Expanding the investor pool would increase the diversity of potential investors and may result in an allocation of funding that better reflects consumers’ interests.

Until recently, Rule 506 still hewed to the one principle on which courts and regulators had always agreed: any offering that is widely advertised is not a private placement. However, in response to a provision of the JOBS Act of 2012, the SEC recently introduced a new category of private offerings for which “general solicitation” is permitted.36 These Rule 506(c) private offerings may be advertised by any means whatsoever, provided that they are sold only to accredited investors.37 Moreover, whereas Rule 506(b) allows investors to self-certify their accredited status, Rule 506(c) requires issuers to take reasonable steps to verify that an investor has the requisite income or net worth. That increased compliance burden may partly explain why Rule 506(c) offerings have not yet become widespread.

Ultimately, although the private placement exemption initially focused on the offering and the market more broadly, it has now evolved into a restriction focused on protecting the individual investor. No matter the size of the offering or the information the investor may obtain about the issuer, current law recognizes a public interest in protecting even a single investor from making a risky investment if that investor is not wealthy.

Why We Need Reform

The current approach to the private placement exemption, as embodied in Regulation D, rests on a series of assumptions. The first is that investment in private offerings is a universally risky endeavor and therefore not suitable for ordinary investors—who should be excluded from private markets for their own good. But are private offerings really so dangerous? It is not readily apparent that this is the case.

The second assumption follows from the first: if private offerings are indeed universally risky, then only sophisticated investors who are able to withstand a loss should be allowed to participate. The accredited investor standard relies on a wealth or income criterion, to determine whether a given investor makes the grade, and thereby it assumes that the relatively well-off are more financially sophisticated and better able to withstand a loss than are ordinary investors. Superficially, such an assumption seems reasonable; in fact, things are far less clear-cut than advocates of the accredited investor standard imagine.

A third assumption harkens back to the pre-Ralston era and revolves around access to information. Specifically, it is thought that wealthy individuals know what information they need to make a wise investment and that they are uniquely able to gain access to it. In other words, well-off investors do not need the mandatory disclosures that public registration requires, whereas ordinary investors, being inherently less powerful and less well-informed, do. Yet this assumption is also questionable, especially in the context of an ongoing technological revolution that makes ever more information available to all, much of it for free and at the click of a button.

So what if private offerings are not, in fact, universally risky? And what if wealth and income are not necessarily good proxies for financial sophistication and the ability to withstand a loss? What if concerns about access to information actually belong to a pre-internet age? And what if, finally, you have a changing corporate funding landscape in which more and more of the most dynamic investment opportunities are hidden from most investors?

Should all these things turn out to be true, current public policy toward private offerings is not only inappropriate, and based on false assumptions, but also has the potential to be economically harmful—both to those trying to raise capital and to those seeking a decent return on their investment. In other words, public policy toward private securities offerings is sorely in need of reform.

Are Private Offerings Universally Risky?

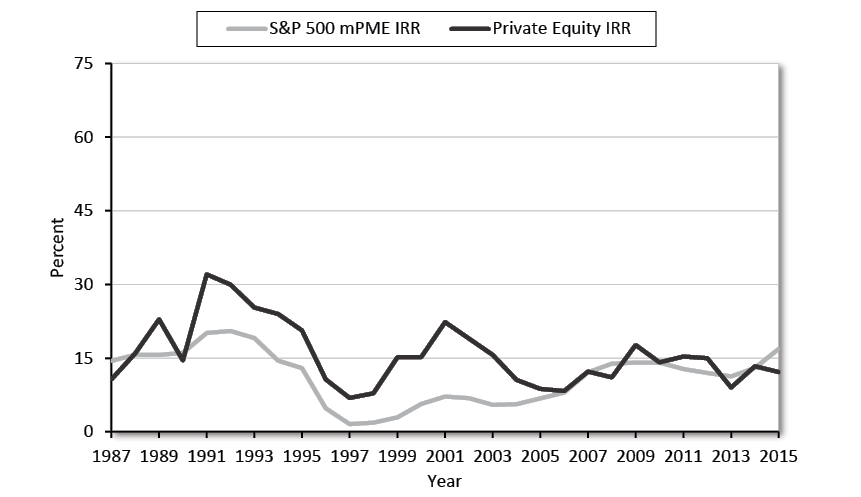

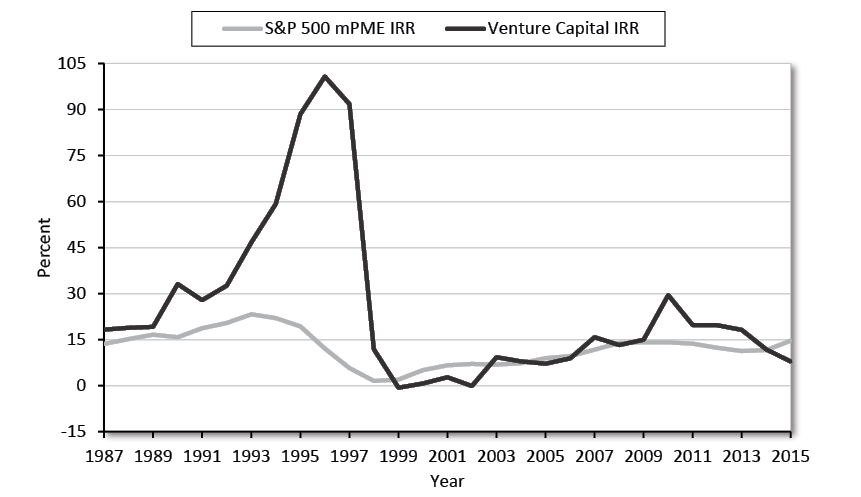

Restrictions on private offerings are often justified by assertions that private offerings are inherently risky, presenting investors with a greater chance of loss. But the numbers are not so clear. Cambridge Investments provides an index of available private investment performance data and constructs benchmarks of public indexes that allow for a comparison of the internal rate of return (IRR), that is of the projected profitability of potential investments.38 Figures 1 and 2, drawn from this data, compare the IRR for private equity funds and venture capital funds with the S&P 500 Index between 1987 and 2015.39 Private equity and venture capital funds invest in private offerings, whereas the S&P 500 is an index of 500 publicly traded companies. Private equity and venture capital funds are, of course, actively managed, which means that simply comparing the performance of these three asset classes is not comparing apples to apples. Nevertheless, excluding investors from the private markets necessarily excludes them from the kinds of investments that private equity and venture capital funds pursue. And, as figures 1 and 2 illustrate, private equity and venture capital funds can obtain results that frequently surpass what an index fund might offer, although they also demonstrate greater volatility. Additionally, these funds are often able to hedge market risk—that is, make investments that protect the funds’ assets even when the entire market tumbles.

Figure 1: Private Equity vs. S&P 500 Index Internal Rate of Return, 1987–2015

Source: Cambridge Associates, “US Private Equity Index and Selected Benchmark Statistics,” March 31, 2017, https://40926u2govf9kuqen1ndit018su-wpengine.netdna-ssl.com/wp-content/uploads/2017/08/WEB-2017-Q1-USPE-Benchmark-Book-1.pdf.

Note: IRR = internal rate of return; mPME = Modified Public Market Equivalent calculation.

Figure 2: Venture Capital vs. S&P 500 Index Internal Rate of Return, 1987–2015

Source: Cambridge Associates, “US Venture Capital Index and Selected Benchmark Statistics,” March 31, 2017, https://40926u2govf9kuqen1ndit018su-wpengine.netdna-ssl.com/wp-content/uploads/2017/08/WEB-2017-Q1-USVC-Benchmark-Book.pdf.

Note: IRR = internal rate of return; mPME = Modified Public Market Equivalent calculation.

As for the risk presented by specific private securities, it is not clear that these are universally riskier than those offered publicly. Many publicly offered securities fail spectacularly. For example, many of the companies that failed in the late 1990s were public. These failures suggest that a company’s public status does not guarantee its value. An investor can see stunning losses with investment in these companies as well. For example, General Motors, once considered a blue-chip stock—among the most well-established and financially sound public companies—traded above $40 in 2007 before falling to $20 in May 2008. A year later, in May 2009, the stock price had fallen below $1; by June, the company was bankrupt.40

Moreover, even if a given private offering is riskier than a public one, it is worth noting that current law permits anyone to invest any amount of money in public offerings. If the purpose of current securities regulation is to prevent unsustainable losses, it is logically inconsistent to permit unlimited investment in one type of offering while effectively prohibiting even a small investment in another.

Three additional points about risk should be borne in mind. First, while any single offering may indeed be risky—and there may be very risky investments in the private offering world—it does not necessarily follow that all investment in the private markets is riskier than investment in public companies. Appropriate risk should not be determined on the basis of a single investment but rather on an entire portfolio. A risky investment may be a prudent option if it balances an investor’s portfolio as a whole. If an investor is unable to access an investment that would provide the correct hedge, that may actually expose the investor to increased risk.

Second, to the extent that the perceived riskiness of private offerings arises from their connection to smaller and newer companies, some of that risk may be decreasing now that more companies are deferring IPOs or forgoing them altogether. This shift should result in a cadre of older, larger, and more stable companies that have nonetheless remained private.

Third, in some cases, it is precisely the riskiness—or dynamism—of private offerings that make them appealing to investors. Investors are compensated for risk with the chance at higher returns. If some investors are categorically excluded from a type of investment specifically because it presents a greater risk, then they are not just protected from exposure to the potential downside; they are also prevented from realizing the potential upside. Additionally, a trend toward companies deferring their IPOs in recent years means that the company’s greatest growth—and greatest dynamism—has already passed by the time the company is public. The public is therefore excluded from the opportunity to capture the returns generated by that surge in growth.41

Other concerns about private offerings center on the fact that the securities tend to be illiquid or difficult to sell, that the issuers are not compelled to provide comprehensive disclosures to the market, and that certain types of liability do not apply to the issuer.

Yet these properties of private securities offerings are not beyond the comprehension of the average investor. In fact, they are no more complicated than many aspects of investing in publicly offered securities. The fact that there may not be a buyer for the security at the time the investor would like to sell is straightforward. The fact that the issuer is not required by law to provide information is similarly simple. Illiquidity and limited disclosure both equally apply to many transactions ordinary Americans complete every day. Buying a house involves assessing the ability to sell the house at a later date. Individuals who buy items through private transactions facilitated by websites such as eBay or Craigslist contend with the potential for limited disclosure.

Liability is perhaps a more sophisticated concept, but—once explained—it too should be comprehensible to the average investor. The most notable difference in disclosures between a public and private offering is the lack of a registration document for the latter, as well as the lack of ongoing mandatory reporting. These materials, filed with the SEC in a public offering, are the source of much liability for issuers—arguably excessive liability at times, because an issuer is liable for any material misstatement in a registration document.42 Investors need not even show that they relied on the mistaken document in making their investment; the mere presence of the error is sufficient for liability. Other provisions provide further liability on the basis of misstatements or omissions in other documents filed with the SEC, for failure to file these documents in the first place, or for other errors committed in complying with filing and reporting requirements.43

Because there are no materials filed with the SEC in a private offering, there cannot be liability for misstatements in such materials. Yet despite these limits on liability, there is still substantial liability for any type of fraud related to private securities transactions. General prohibitions on fraud apply, and there are also specific rules that prohibit fraud in securities transactions. For example, under Rule 10b-5—the great catchall provision in federal securities regulation—it is unlawful to use any type of fraud or deceit in connection with the purchase or sale of a security. This rule sweeps broadly and includes any actor: issuer, underwriter, buyer, or intermediary. It also includes a crucial provision that expands its reach beyond common law fraud. It is not only unlawful to make untrue statements of material fact when buying or selling securities, it is also unlawful to “omit to state a material fact necessary in order to make the statements made, in the light of the circumstances under which they were made, not misleading[.]”44 In other words, although there is no obligation to provide disclosures when selling a security through a private offering, a seller is not permitted to make false promises—and investors have legal recourse if they do.

Although there are no required disclosures for a private offering, most investors demand relevant information from issuers. It is therefore customary for issuers to provide what is known as a private placement memorandum, a document that provides the information that most investors would want to know before buying any securities. The statements made in this document are subject to Rule 10b-5 and so must be accurate, not misleading, and must not omit information that is necessary to make any other statements not misleading.

The principal difference between liability under Rule 10b-5 and other federal securities rules is that plaintiffs must prove that not only was the statement or omission false or misleading but also that the defendant intended to mislead the plaintiff. By comparison, in a public (registered) offering, a material misstatement can mean liability even if its inclusion was entirely innocent. Whereas Rule 10b-5’s intention requirement is a higher bar, it is no higher than what is required for claims of fraud in other commercial transactions.45

As to securities fraud more generally, it is not easy to determine whether fraud is more common among private offerings than public ones. Certainly a criminal who creates an entirely fraudulent offering—one in which there is no actual company issuing the securities and investors’ money is going directly into the criminal’s pockets—will not attempt to register the offering. Thus the offering may appear indistinguishable from a private offering. To the extent that the concern is not about offerings that are wholly fraudulent, but rather about fraud within legitimate organizations, history shows that registration is not necessarily a bulwark against that type of fraud: Enron and WorldCom, for example, were public companies at the time they engaged in considerable fraudulent activities.

To sum up: investment in private offerings can be risky, but that risk must be assessed as part of a whole portfolio. It is usually unwise to invest too heavily in any one company—whether public or private—given that all businesses can fail. Private securities may be illiquid, but illiquidity is not a difficult concept for ordinary investors to understand—as is evidenced by people’s ability to understand real estate purchases. Private offerings involve some limitations on liability, but these limitations are not overly complex and are similar to limitations on liability for other commercial transactions. And although many of the rules applicable to public offerings are aimed at preventing fraud, many major frauds have nevertheless occurred at public companies.

None of this is to say that allowing wider participation in private markets is some sort of silver bullet. Opening up private offerings would obviously not result in instant riches for new investors. On the other hand, it would allow access to new opportunities that are currently hidden behind locked gates.

Does the Accredited Investor Standard Make Sense?

The theory underlying the accredited investor standard requires the SEC to use broadly applicable regulations to identify those investors least likely to cause themselves harm through imprudent investment. Yet regulation is a blunt instrument and is badly suited to this task. In using wealth or income as the only criterion, the SEC has created a standard that is both under-inclusive and over-inclusive, excluding investors entirely able to fend for themselves while opening the gate to investors with little sophistication. Attempts to fix the wealth threshold at the right level only tie the SEC in knots. In reality, wealth is not necessarily tied to its regulatory objective—that is, identifying those who are able to withstand a financial loss46 and are sufficiently knowledgeable to appreciate the risks inherent in certain investments.47

For one thing, whereas it may be true that a wealthy individual can withstand a much greater financial loss than a person of lesser means, no one’s wealth is unlimited. A person with a net worth of $50,000 may lose $100 without adverse consequences. But a person with $1 million could be ruined by a loss of $900,000. Under current law, however, the first person would be barred from making even a very modest investment whereas the second person could freely wipe out a life’s savings.

The wealth/income requirement also privileges age because people tend to amass wealth as they approach retirement and tend to earn higher incomes later in their careers than when they are just starting out. Yet age does not make a person better able to withstand a loss. In fact, a 30-year-old worker who earns a middle-class income could likely bounce back from even a substantial loss, given decades of future earning potential. A 70-year-old retiree, however, has little or no serious opportunity to recoup even moderate losses in wealth. And for many retirees, even a net worth of $1 million is not enough for a lavish lifestyle; a decrease in that figure could have a noticeable effect on the retiree’s standard of living.

Finally, the wealth cutoff makes no distinction among costs of living in various parts of the United States. Nor does it account for other differences in lifestyle. A single person living in Omaha with a $300,000 income has much more disposable income than someone living in Manhattan earning the same amount and supporting a spouse and three children.

The accredited investor standard is equally flawed as a means of discerning financial sophistication. First, although it is often argued that the complexity of private offerings makes restrictions necessary,48 it is not clear that all or even most of the investments limited to accredited investors require great sophistication to understand. It is true that some private offerings are complex, but that is the case in public markets too. In fact, the underlying issuers may be considerably less complex when they relate to early-stage or small companies. A publicly traded company such as Coca-Cola, with international operations and a complex supply chain, can be much more difficult for an investor to evaluate than a small company with only a handful of employees.49

Wealth and income requirements also ignore the value of industry experience. Consider, for example, a small company developing a particular type of valve or other medical device. A nurse might have only a basic understanding of how to read a company’s financial statements and yet also have an incredibly sophisticated understanding of how such a medical device would be used and whether there would be significant uptake if the product were available. The nurse’s wealth, or lack thereof, would be immaterial to understanding the value of the company’s product.

Furthermore, although there is some evidence that financial sophistication increases with wealth,50 that evidence is mixed, and there are clearly many ways a person could attain wealth without the least understanding of investments. And, as Felicia Smith of the Financial Services Roundtable has argued, the Madoff Ponzi scheme demonstrates that even very wealthy people are not always able to ask the right questions.51

At the same time, many investment advisers who earn their living advising wealthy clients on which assets to buy are not wealthy enough to qualify as accredited investors themselves, despite their obvious financial sophistication. The same goes for many junior associates in law or underwriting firms—they might work daily on private offerings, preparing and researching the very documents investors will review, but they are still locked out of the private markets.

Ultimately, employing an income or wealth test to decide whether a person is legally permitted to buy an item is an odd restriction that is wholly absent from other areas of commercial life. People may walk into a designer boutique and spend $20,000 on a handbag without any inquiry into their earnings or wealth. They may gamble everything they own in Las Vegas or buy as many lottery tickets as the local convenience store will sell them. Adult Americans can do these things whether they are “accredited” or not, and the law will not prevent them from incurring even an unsustainable loss through such activities. So why can’t they invest in a private offering? After all, investing in a company, even a risky company, is likely to be a more prudent use of an investor’s funds than luxury shopping or high-stakes gambling.52

Should We Worry about Access to Information?

In some ways, the accredited investor standard harkens back to the access criterion pre-Ralston. Wealthy individuals are presumed knowledgeable enough to ask for the right information and powerful enough to induce the issuer of private securities to provide it. As such, they do not need the protections that registration and disclosure requirements provide in the public markets. They, unlike ordinary investors, can fend for themselves.

The first problem with this view is that there is no particular reason why an investor would be able to exert influence simply because of his or her wealth. It is true that a person with $1 million has the potential to invest more than a person with only $50,000. But if both are offering an investment of $10,000, the existence of an additional $990,000—sitting in an account somewhere and not designated for investment in the company—would not necessarily give the holder additional persuasive ability.53

Furthermore, the belief that wealth is required for access and knowledge assumes that the investor is engaging one-on-one with the issuer—and that no one other than the investor can make such a request. In fact, providing retail investors with access to private offerings would encourage the development of third-party providers who focus specifically on obtaining and making available to investors exactly the information needed to make a sound investment decision. Changes in technology, most notably in information technology, make this type of service increasingly easy to provide.

Indeed, arguably the greatest change in daily life in the past several decades—even from the time Regulation D was issued in 1982 to the present—is the increased access to information and the ease with which information can be disseminated to the public. A quick Google search can yield links not only to a company’s website and whatever information it chooses to post, but also to any news articles across the world that may have covered the company. Review sites like Yelp can provide information about customer experiences with the company, and employee sites like Glassdoor reveal information about pay structure, hiring practices, and employee morale. Many organizations conduct and post research about corporate practices that may affect public perception, such as the use of overseas labor, working conditions at company facilities, or the company’s environmental impact.54 And social media sites like Twitter and Facebook allow anyone to share information quickly and cheaply across the entire world, making scandal difficult to keep quiet.

Crowdfunding sites like Kickstarter and GoFundMe have illustrated how this exchange of information can work in practice. These sites do not host securities offerings. People providing funding may receive token gifts in exchange for their money or other benefits such as priority on a waitlist for a new product. But these funders do not share in any wealth generated by the companies. Nevertheless, such sites typically provide robust opportunities for company founders to interact with potential funders.

In fact, it can be easier for companies to provide information in this setting because the regulations surrounding securities offerings do not apply. That may seem counterintuitive—after all, the very point of those regulations is to require the disclosure of important information. However, the flip side is that what companies may say—as well as how and when they may say it—is tightly regulated. As a result, a company’s lawyers may advise its executives to say as little as possible during an IPO, fearing—quite correctly—that a stray remark could have disastrous consequences.

The problem, in simple terms, is that anything a company says during an offering—or even while preparing for an offering—can be construed as effectively marketing that offering. This kind of marketing is strictly regulated, and the rules are easy to break inadvertently. For example, when Google was preparing for its IPO, founders Larry Page and Sergey Brin gave an interview to Playboy magazine. Although they made no mention of the IPO, their participation in the interview was feared to be an effort to condition the market. The IPO had to be delayed while the SEC investigated the ramifications of the interview.55

Kickstarter and GoFundMe campaigns are typically based on donations and so trigger none of the securities laws. Those seeking funds are free to engage in any kind of discussion and provide any information they wish about their enterprises.56 Whereas donations on a crowdfunding site are not perfect proxies for investments in securities, these sites do demonstrate the potential for new technology to connect people in a way unimaginable to Congress in 1933, when the first federal securities laws were passed. None of this information replaces cold, hard financials, of course; but the information does provide excellent context, fleshing out the company’s overall appearance. Such information may once have been available only to those close to a company’s management; now even outsiders have access to it. This access changes the rationale that drove early legal decisions about the private offering exemption, such as Ralston: in some important respects, anyone with internet access can become better informed about a company, its industry, and its prospects than well-connected investors were in the 1930s.

There is certainly still information that only someone very close to a company would have, and there is information that can be gleaned only from a financial statement. But any would-be investor is capable of requesting financials and can withhold investment if the financial information is not forthcoming. Moreover, the current accredited investor standard includes no requirement that the investor be close to anyone in the company at all. If access to company information still matters, it must be reexamined in light of the staggering changes in information access the internet has brought.

Problems in the IPO Market

IPOs in the United States have been in decline. In 2015, there were 152 IPOs raising a total of $25.2 billion.57 Those numbers represent a substantial decline from a high of 677 IPOs raising $42.05 billion in 1996. (See Figure 3.) Whereas that high was almost certainly inflated by the dot-com bubble that burst five years later, the market has been especially anemic in the past 15 years.58 The trend has been especially noticeable among smaller firms. Although there has been some consolidation in the market with larger companies buying up smaller ones—which may have led to fewer IPOs—that does not explain why overall volume has declined to such an extent.59 Another development is that the companies that do go public tend to do so later in their development than similar firms did in earlier times.

Figure 3: Number of Initial Public Offerings, 1981–2015

Source: Jay R. Ritter, “Initial Public Offerings, Updated Statistics,” University of Florida, March 8, 2016, https://site.warrington.ufl.edu/ritter/files/2016/03/Initial-Public-Offerings-Updated-Statistics-2016-03-08.pdf.

Note: IPO = initial public offering.

These changes in the IPO market make the private markets all the more important to the U.S. economy. At the same time that IPO activity has been down, there has been considerable growth in private offerings.

There are a number of theories as to why IPO activity seems to be depressed. One theory is that, as the economy has changed, it has become more profitable for a small company to merge with and become part of a larger organization than it is to gain financing through an IPO.60 Another is that changes in regulation that changed how stocks are quoted resulted in smaller bid-ask spreads. The argument is that that change has reduced the compensation available for trading in the stocks of smaller companies, and that may in turn have resulted in less profitability for small companies that do go public.61 Another theory lays the blame on the Sarbanes-Oxley Act of 2002, which increased regulatory burdens on public companies. Because many compliance costs are fixed and do not correlate with firm size, these costs represent a greater share of operating expenses for a small public company than for a large one. The JOBS Act of 2012 sought to partially address these effects, giving most companies a few years’ hiatus from some of Sarbanes-Oxley’s requirements. While there is evidence that this change had some effect on the number of IPOs, it has not brought the market roaring back to life.62

To the extent that Sarbanes-Oxley or other regulations have made the public markets unattractive, however, the flourishing private market acts as a safety valve. As Brooklyn Law School professor and former SEC Commissioner Roberta Karmel has noted, “the problem with regulating by exemption is that it does not incentivize the SEC to adjust regulations that discourage capital market participants from entering a regulated system.”63 Not only is there little incentive for the SEC to address problems in the public markets, there also are considerable incentives for the agency to retain the status quo.64 As Zachary Gubler, associate professor at Arizona State’s College of Law, has argued, “by expanding the private securities market, the SEC is able to respond to the increased demand for the services provided by a securities market without risking the loss of political slack that would accompany efforts to reform the IPO market.”65 That is, the current regulatory structure does not provide the correct incentive for the SEC. The regulator is rewarded not for expanding its control over the private markets, but for avoiding the glare of public scrutiny by passing ever more stringent regulations, reaping the benefit of showing the public “toughness” without actually stifling capital formation. Of course, the new regulations have little real effect because issuers avoid the regulated market. The people who pay the price for this evasion are not the issuers or the SEC, but the investing public the new regulations are designed to protect. The risk is that new regulations make the public markets so unattractive that the best investments go elsewhere.

It is possible that the heyday of the IPO has passed and that the current market favors large, well-established public companies and smaller, more nimble private ones. But if these trends are driven and continue to be driven by government regulation, then considerable economic harm could come from excluding the vast majority of investors from precisely those private markets that contain the most growth and dynamism.

Reforming Private Securities Markets

A number of proposals have been put forward to reform the private offering exemption. Many of them were discussed in a recent report by the SEC, which examined the accredited investor standard.66 Some of these proposals actually seek to tighten the exemption by increasing the wealth or income requirements that would-be investors have to meet. Other proposals would open up private offerings to potential investors who fail to meet those financial criteria but who can nevertheless prove that they are financially sophisticated. A few of these were endorsed in the U.S. Treasury Department’s recent report on capital markets and have also made their way into a bill introduced in the House in 2017.67

None of the reform proposals, however, grapple with the underlying issue: the SEC should not be the arbiter of what individuals can do with their money. It is this foundational premise, and not its practical implementation, that requires fixing. Without such reform, the securities markets will continue to exacerbate inequalities, perpetuate a singularly undemocratic legal structure, and permit the public markets to atrophy.

Proposals on Wealth and Income Thresholds

The accredited investor standard’s wealth and income thresholds were set at $1 million and $200,000 respectively in 1982. Of course, a person meeting those criteria in the 1980s was, in real terms, much richer than a person with the same amount of money today. In fact, $200,000 in 1983 dollars is equivalent to between $430,000 and $490,000 now; 1983’s $1 million would be more than $2 million. As a result, whereas fewer than 2 percent of households qualified as accredited in 1983, an estimated 10 percent of households do so today.68 Some people therefore advocate increasing those wealth and income thresholds and indexing them to inflation to ensure that they continue to rise apace in the coming years.69

For example, Greg Oguss, formerly of Northwestern School of Law, would increase the net worth threshold to about $2.5 million for a household (excluding the primary residence), raise the income threshold to about $490,000 per year for an individual and $600,000 for a couple, and index both thresholds to inflation going forward.70 The SEC estimates that only about 4 percent of U.S. households would qualify as accredited if wealth and income thresholds were raised to reflect more than three decades of inflation in this way.71

There are, however, three main problems with such proposals. First, their proponents tend to argue that thresholds should be raised because they have remained fixed since 1982. This is not correct: Dodd-Frank actually required a change in 2012, excluding equity in the primary residence from the calculation of a household’s wealth. Given that households with a net worth above $500,000 have, on average, $250,000 in equity in their primary residence,72 this exclusion has effectively raised the wealth threshold by a quarter of a million dollars already.

Second, and more importantly, there was nothing particularly special about the thresholds established in 1982 in the first place. The SEC’s adopting release for Regulation D includes no discussion of why the thresholds were set at $1 million in assets or $200,000 in annual income.73 The only hint of such a discussion comes in a brief explanation of why the asset level was set at a flat $1 million instead of $750,000 with certain assets (home, cars) excluded. The release implies that a flat $1 million is functionally equivalent to $750,000 with exclusions. But this does not explain why $1 million is the sweet spot, as opposed to, say, $100,000 or $100 million.

Finally, it is not clear that increased access to private offerings has had a negative effect on investors. A larger pool of potential investors does not, in and of itself, establish a need for greater restrictions. In fact, eligibility numbers are only relevant if investors who qualify as accredited today, but who would not qualify under an inflation-indexed threshold, show a particular inability to cope with the complexities of private offerings. Advocates of raising the accredited investor standard’s wealth and income thresholds cite no data showing that there has been an increase in fraud or ill-advised investment. If there has been no noticeable harm from the erosion in value of the original threshold, what is the argument for changing it?

Another proposal would exclude retirement savings from the calculation of an individual’s or couple’s net worth. For example, Larissa Lee, a Utah attorney, has proposed lowering income and wealth thresholds while simultaneously requiring that retirement accounts be excluded and that investors be required to diversify their private offering investments. Others recommending the exclusion of retirement assets have argued, first, that individuals should not put their retirement savings at risk by investing in private placements, and second, that retirement accounts are not easily accessible and therefore cannot effectively cushion the blow from a major investment loss.74

It is, of course, probably unwise to heavily invest one’s retirement savings in start-up enterprises. It is also true that tax-preferred retirement accounts tend to be difficult to access because of the heavy penalties early withdrawal can incur. But that does not mean that regulation should be used to force investors to make decisions regulators believe are wise.75

There are other problems with this proposal. For one thing, it could lead investors wishing to buy privately offered securities to refrain from using tax-advantaged retirement savings vehicles, in an effort to ensure that all their assets can be counted toward the accredited investor threshold. Excluding retirement savings from the wealth criterion would also represent an inconsistent treatment of equally illiquid assets. A vacation home, for example, is much less liquid than a retirement account. Where is the sense in counting the former toward the wealth threshold while excluding the latter? It is hard, after all, to cushion an investment loss with a summer cottage.

A further proposal presents even more problems than the two already mentioned. So-Yeon Lee, a Boston attorney, has proposed opening investment in private offerings to non-accredited investors but limiting their investment to “discretionary” income. She defines this as adjusted gross income minus taxes and other necessities, such as mortgage payments, utilities bills, and food costs.76

Lee expressly does not address whether such a rule would be administratively feasible. Prima facie, it almost assuredly would not. Aside from the differences in personal taste that might lead one person to believe she “needs” a six-bedroom house whereas another is content with a studio apartment, there are expenses that, although discretionary, are nonetheless fixed. The excess cost for a luxury car over a simple sedan is a discretionary expenditure, but if the car is financed with a multiyear loan, the monthly car payment is fixed regardless of whether the car itself is a Ford or a Mercedes. It is also unclear whether Lee’s proposed regulatory scheme would consider the number of dependents an investor has, the cost of living in the area where the investor resides, whether any member of the investor’s family has an illness requiring expensive medical treatment, or any of the many costs that individuals may have.

Even if it were possible to create a standard list of what constitutes necessities for all investors, such a standard would require a considerable invasion of investors’ privacy. It is unlikely many would enjoy disclosing to strangers, for example, their monthly grocery bills. Additionally, while income and housing expenses may be somewhat fixed, at least on an annual basis, other necessities can fluctuate considerably—making a precise calculation extremely difficult.

Of course, this all assumes that there must be a specific admonition to use only discretionary income for investment in private offerings. Such a distinction seems strange because investment of any kind is almost by definition discretionary; no one would seriously suggest that an investor should use the mortgage money to buy even the most blue-chip public security. However, if an investor has any discretionary income at all, why shouldn’t she be able to spend it in any way she chooses—whether on a designer dress, a trip to the casino, or securities issued by a start-up? Ultimately, any rule based on Lee’s proposal would be even more paternalistic than the current one.

Several other articles have proposed opening investment in private offerings to non-accredited investors while placing some sort of cap on the amount an individual may invest. Abraham Cable, professor at the University of California Hastings College of the Law, has proposed allowing each investor to have a set amount of “mad money” to invest in high-risk investments, with the amount to be determined in proportion to the individual’s wealth.77 Another proposal, put forward by Syed Haq, formerly of University of Michigan Law School, would set a sliding scale that would allow increased levels of investment as an individual’s wealth or income increased.78 Haq would exclude illiquid assets from the calculation of wealth, including only a “fire sale” value—the assumption being that, if an asset is to cushion a loss, it must be valued at the price the investor could get for it in a hurry.

These proposals are at least more administratively feasible than Lee’s. However, reforming private securities markets must be about more than just building a better mousetrap. There are numerous ways the SEC could attempt to pinpoint what a sustainable investment loss would be. But the truth is that this is an extremely personal determination, based not only on an individual’s expenses but also on the person’s tastes and temperament. A sustainable loss for one person earning $50,000 may be $50, whereas another person with the same income could stand to lose $5,000. Wealth alone does not make a person immune from loss.

Proposals on Financially Sophisticated Investors

Although “financial sophistication” has been tied to wealth since the beginning of the private placement exemption, wealth is only a proxy for knowledge and not a direct measure of an individual’s understanding of financial matters. For this reason, many have argued for expanding the definition to include those who have demonstrated actual financial knowledge or who possess other qualifications that may also serve as a proxy for sophistication.79

One of the most prominent proposals encourages the use of a test of actual understanding of basic financial principles. For example, Stephen Choi, professor at New York University School of Law, has proposed a test administered by the SEC or by another government actor, which would serve as a “financial driver’s license.”80 Whereas there are obvious flaws in the proposal—who would administer the test, and how would “sophistication” be tested?—it would at least avoid some of the most absurd results of the current wealth-based system.

A simple fix, under this theory, would be to deem those who pass certain tests already administered by the Financial Industry Regulatory Authority (FINRA) as demonstrating the requisite sophistication. For example, those who have passed either the test for securities brokers (Series 7) or investment advisers (Series 65) could be dubbed “accredited.”

Using the FINRA examinations does not completely address the problem of identifying “sophisticated” investors, however. These examinations are currently available only to individuals whose employers are FINRA-registered firms or who are otherwise required by a regulator to register with FINRA. Whereas including securities brokers and investment advisers in the definition of accredited investors would at least improve the current system, it would still leave out many individuals who are in fact financially sophisticated.

It is hard to think of a reason why an individual who desires to become an accredited investor, and who undertakes a course of study to that end, should not have an opportunity to demonstrate the attainment of the requisite level of understanding. If a person is in fact financially sophisticated, it is unclear why that person should be excluded from the definition of accredited investor.

Ultimately, of course, improving the definition of accredited investor does nothing to justify the existence of offerings open only to a select few. But it would at least make the process more logical.

A Better Approach to Private Offerings

The current use of the accredited investor standard is illogical. Worse, it exacerbates wealth inequality and places a glaringly undemocratic framework over the securities markets. Current recommendations for reform fail to grapple with the basic question of whether excluding investors from private markets is either just or desirable. A better solution would eliminate the existing accredited investor framework and replace it with a menu of disclosure regimes from which investors and issuers would be free to choose.81

A regime that permits anyone to invest also ensures that it is the market, and not an individual regulator, that determines which companies should receive investment. The alternative—to have the regulator sit in the role of superinvestor, determining which projects should be funded—has been shown to be undesirable. An example from state regulation illustrates the point. In addition to the SEC, each state has its own securities regulator. Although the state regulator’s role in IPOs has been greatly reduced since a 1996 change in the law, each state still maintains laws governing the registration and sale of securities within its borders.82 Many state securities laws require what is known as “merit review.” Securities offerings subject to state regulation have to be reviewed by a state regulator, which determines whether they are, in the words of many state statutes, “fair, just, and equitable” to the investor. In some cases, the regulator also ascertains whether the securities are likely to present a return on investment to the purchaser.83 In 1980, regulators in Massachusetts deemed a young computer company’s IPO to be too risky and refused to allow the company to sell to the Commonwealth’s investors. That “risky” company that regulators “saved” the people from was Apple Inc.84

Congress fortunately chose a different path when passing the Securities Act in 1933. No public offering is off limits to any investor. Investors are free to invest as much as they want in such offerings. Whereas questions remain about whether mandatory disclosures are necessary—and, certainly, the number and type of disclosures currently required may be excessive—the principle underlying federal securities law is that the market, not regulators, should determine which companies receive funding. This is a better approach to government regulation of securities.

When it comes to private offerings, merely refining the requirements of the accredited investor standard is not the answer. If someone has money in the bank, that person should be free to spend it at will. Having assets that are legally deemed to be too risky or complex for one person to purchase but not another is patently paternalistic. Other areas of law that operate this way are those that apply to children. It is legal for an adult to buy tobacco or alcohol but illegal for a child to do so. Such restrictions typically stem from the understanding that children developmentally lack adequate judgment to recognize the harm these products could cause them.85 Adults should not be restricted in the category of purchases they may make based only on the total amount of money they have.

The solution is therefore to open investment in private offerings to all investors. This would not diminish any value that currently exists in having registered “public” offerings with their attendant disclosures. These offerings would continue to exist unchanged.86 What would change is the SEC’s definition of private offerings, or rather, those offerings the Securities Exchange Act described as “not involving any public offering.” Such nonpublic offerings would be redefined as any offering not registered with the SEC. There would be no restrictions on who could invest in the unregistered offerings. Although, if it were deemed necessary, the law could require that the issuer provide investors with a disclosure stating that the offering is unregistered and that the issuer provide a summary of the protections available through registered offerings that the investor would forgo. Those investors who preferred the protections available through registered offerings could restrict their investment to those securities.