In recent weeks much has been written about the rising cost of U.S. housing. According to Reuters News Agency, the “rising cost of steel, lumber and copper is hampering homebuilding—and pushing house prices out of reach.” In that vein, we explore the affordability of U.S. housing between 1980 and 2020, using time prices, which measure the amount of time that an American blue-collar worker needs to work to earn enough money to buy a house.

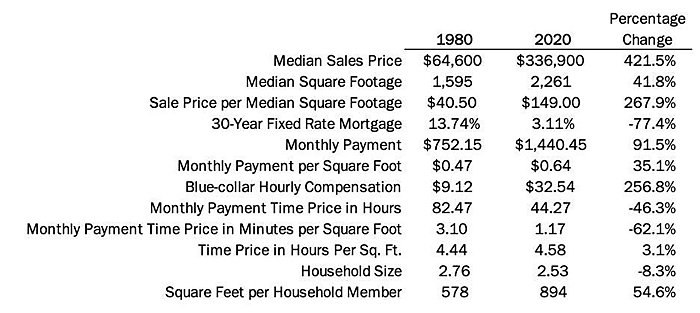

According to the U.S. Census Bureau, the median sales price of a house in the U.S. in 1980 was $64,600. Given that the mortgage loan rate at that time was 13.74%, a 30-year loan for $64,600 required a monthly payment of $752.15. The average size of an American home was 1,595 square feet, indicating a monthly payment rate of $0.47 per square foot of housing.

According to Measuring Worth, a well-known database run by economist Lawrence H. Officer of the University of Illinois at Chicago and economist Samuel H. Williamson of Miami University, the average blue-collar worker’s compensation rate was $9.12 per hour. Therefore, a $752.15 loan payment required 82.47 hours of work per month, which is equal to a monthly payment rate of 3.1 minutes of work per square foot of housing.

By 2020, the median sales price of a house rose to $336,900. The mortgage loan interest rate, however, declined to 3.11%. A 30-year loan, then, required a monthly payment of $1,440.45. The average U.S. home size also increased to 2,261 square feet, indicating a monthly payment rate of $0.64 per square foot of housing.

In 2020, the average blue-collar worker’s hourly compensation rate stood at $32.54. Therefore, a $1,440.45 loan payment required 44.27 hours of work per month, which is equal to a monthly payment rate of 1.17 minutes of work per square foot of housing.

That means that the time price of a loan payment decreased from 82.47 hours of work per month in 1980 to 44.27 hours of work per month in 2020, or by 46.3%. Over the same period, the time price of a monthly loan payment per square foot of housing decreased from 3.1 minutes of work to 1.17 minutes of work, or by 62.1%.

Between 1980 and 2020, the nominal price of a square foot of housing increased by 268%. Over the same period, the average nominal blue-collar hourly compensation rate rose by 257%. As such, the time price of a square foot of housing rose from 4.44 hours of work in 1980 to 4.58 hours of work in 2020, or 3.1%.

Note that our calculations are not adjusted for the higher quality of construction and finishes and energy efficiencies that are typically found in 2020 U.S. homes but were not present in 1980 U.S. homes. Also, note that over the last four decades the average household size decreased from 2.76 persons to 2.53 persons. The living space per household member increased from 578 square feet in 1980 to 894 square feet in 2020, or 55%.

All in all, the time price of U.S. homes remained almost the same between 1980 and 2020. On average, blue-collar workers need to work 3.1% longer to earn enough money to buy a square foot of housing in the U.S. That small increase is surprising, given the spread of “not in my back yard” opposition by residents to new developments in their local areas and the additional regulatory burdens imposed at all levels of government on the U.S. housing industry over the last four decades.

Crucially, the 3.1% increase in the time price of a square foot of housing is more than offset by the 77% decline in the 30-year mortgage interest rate, which fell from 13.74% in 1980 to 3.11% in 2020. That reduction alone saves blue-collar workers 62.1% of work per square foot of housing.

The Nobel Prize-winning economist Vernon Smith argued that swings in interest rates explain the booms and busts in the housing market, which influence the general economy as well. Contrary to what your late-night infomercial might be saying, real estate is not just about location, location, location. It is primarily about financing, financing, financing.

About the Authors